Some Notes on the Formation of a Pair in Pairs Trading

,

,  and

and

Abstract

:1. Introduction

2. Pair Selection

2.1. Co-Movement

- denotes the Pearson correlation coefficient, applied to the rank variables

- , is the covariance of the rank variables.

- and , are the standard deviations of the rank variables.

- is the mean of the cointegration model

- is the cointegration residual, which is a stationary, mean-reverting process

- is the cointegration coefficient.

2.2. The Distance Method

2.3. Pairs Trading Strategy Based on Hurst Exponent

2.4. Pairs Trading Strategy

- In case the pair will be sold. The position will be closed if or .

- In case the pair will be bought. The position will be closed if or .

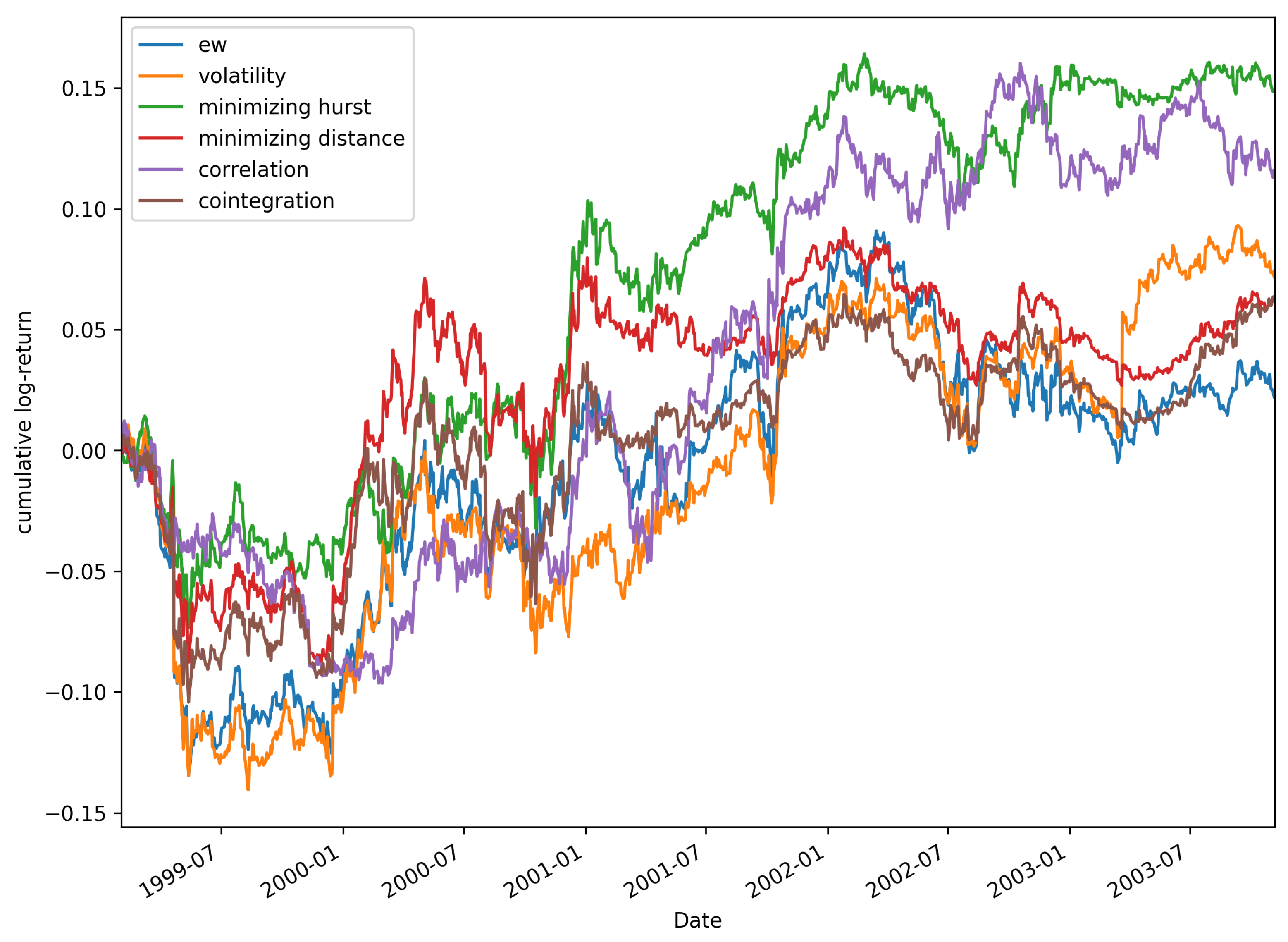

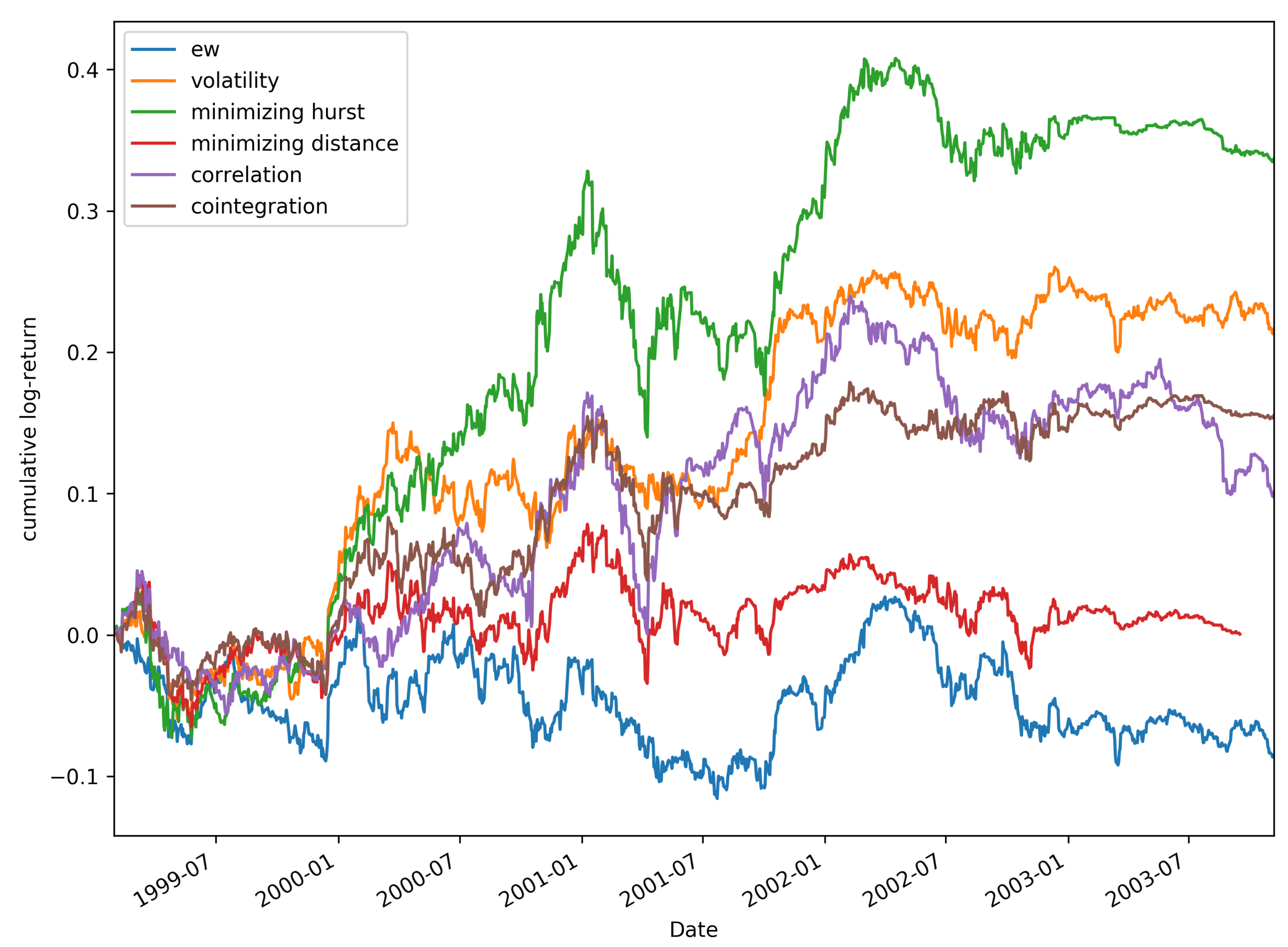

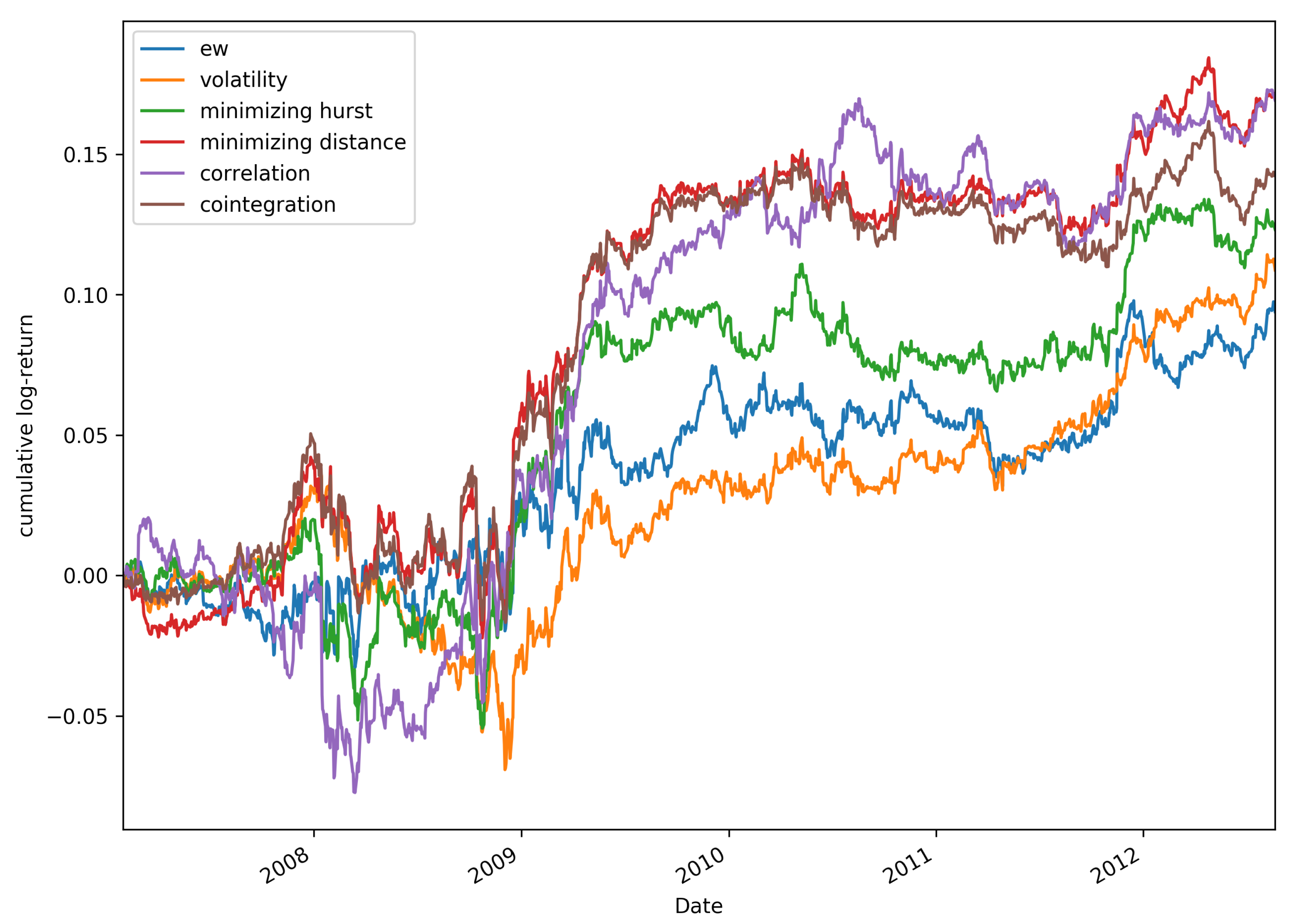

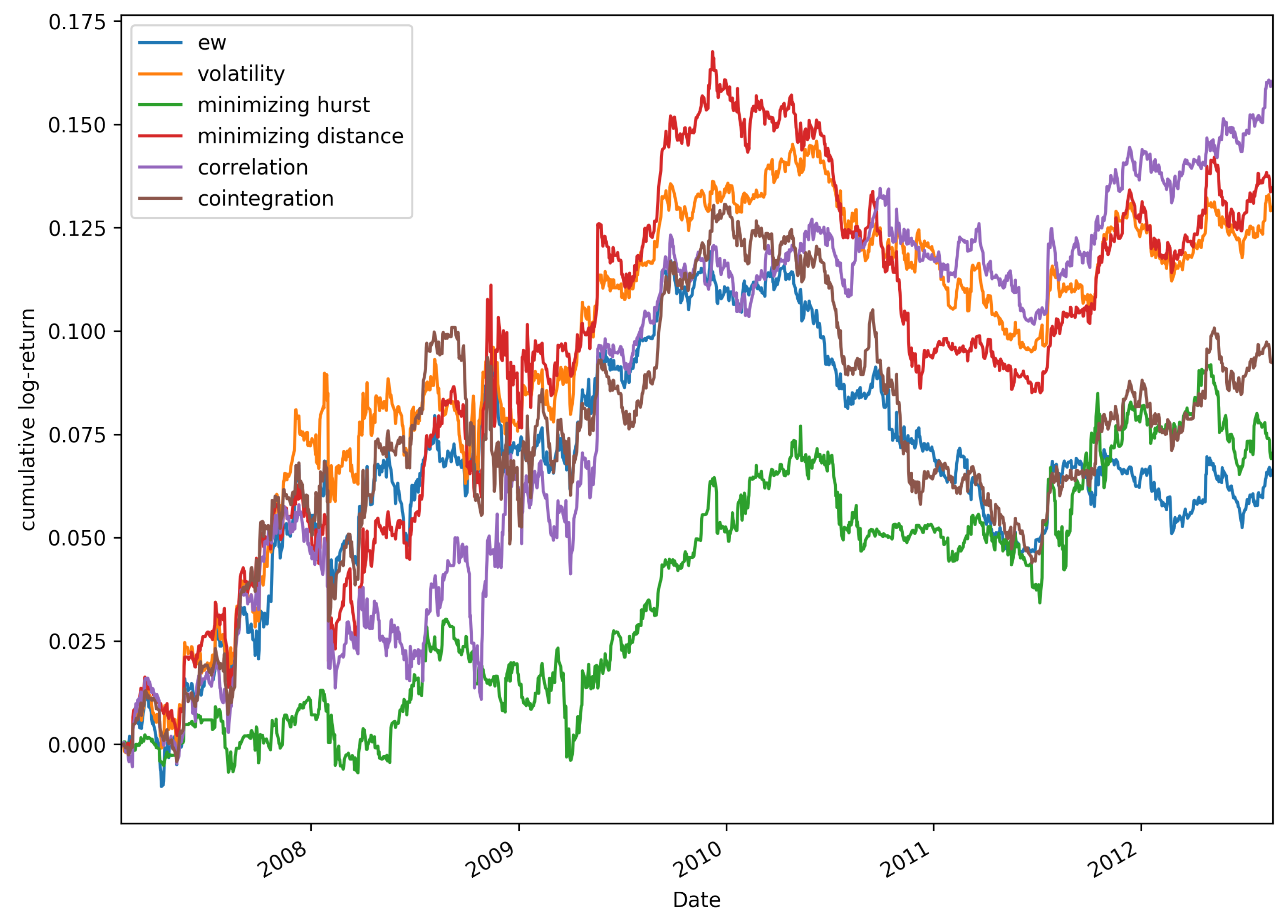

3. Forming the Pair: Some New Proposals

- 1.

- Equal weight ().In this case . This is the way used in most of the literature. In this case, the position in the pair is dollar neutral. This method was used in Reference [16], and since then, it has become the more popular procedure to fix b.

- 2.

- Based on volatility.Volatility of stock A is and volatility of stock B is . If we want that A and have the same volatility then . This approach was used in Reference [11] and it is based on the idea that both stocks are normalized if they have the same volatility.

- 3.

- Based on minimal distance of the log-prices.In this case we minimize the function , so we look for the weight factor b such that and has the minimum distance. This approach is based on the same idea that the distance as a selection method. The closer is the evolution of the log-price of stocks A and , the more reverting to the mean properties the pair will have.

- 4

- Based on correlation of returns.If returns are correlated then is approximately equal to , where b is obtained by linear regression . In this case, if returns of stocks A and B are correlated, then the distribution of and will be the same, so we can use this b to normalize both stocks.

- 5.

- Based on cointegration of the prices.If the prices (in fact, the log-prices) of both stocks A and B are cointegrated then is stationary, whence b is obtained by linear regression . In this case, this value of b makes the pair series stationary so we can expect reversion to the mean properties of the pair series. Even if the stocks A and B are not perfectly cointegrated, this method for the calculation of b may be still valid, since, thought may be not stationary, it can be somehow close to it or still have mean-reversion properties.

- 6.

- Based on lowest Hurst exponent of the pair.The series of the pair is defined as . In this case, we look for the weight factor b such that the series of the pair has the lowest Hurst exponent, what implies that the series is as anti-persistent as possible. So we look for b which minimizes the function , where is the Hurst exponent of the pair series . The idea here is similar to the cointegration method, but from a theoretical point of view, we do not expect to be stationary (which is quite difficult with real stocks), but to be anti-persistent, which is enough for our trading strategy.

4. Experimental Results

- In case the pair will be sold. The position will be closed if or .

- In case the pair will be bought. The position will be closed if or .

Discussion of the Results

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A. Stocks Portfolio Technology Sector Nasdaq 100

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Ticker | Company |

|---|---|

| AAPL | Apple Inc. |

| ADBE | Adobe Systems Incorporated |

| ADI | Analog Devices, Inc. |

| ADP | Automatic Data Processing, Inc. |

| ADSK | Autodesk, Inc. |

| AMAT | Applied Materials, Inc. |

| ATVI | Activision Blizzard, Inc. |

| AVGO | Broadcom Limited |

| BIDU | Baidu, Inc. |

| CA | CA, Inc. |

| CERN | Cerner Corporation |

| CHKP | Check Point Software Technologies Ltd. |

| CSCO | Cisco Systems, Inc. |

| CTSH | Cognizant Technology Solutions Corporation |

| CTXS | Citrix Systems, Inc. |

| EA | Electronic Arts Inc. |

| FB | Facebook, Inc. |

| FISV | Fiserv, Inc. |

| GOOG | Alphabet Inc. |

| GOOGL | Alphabet Inc. |

| INTC | Intel Corporation |

| INTU | Intuit Inc. |

| LRCX | Lam Research Corporation |

| MCHP | Microchip Technology Incorporated |

| MSFT | Microsoft Corporation |

| MU | Micron Technology, Inc. |

| MXIM | Maxim Integrated Products, Inc. |

| NVDA | NVIDIA Corporation |

| QCOM | QUALCOMM Incorporated |

| STX | Seagate Technology plc |

| SWKS | Skyworks Solutions, Inc. |

| SYMC | Symantec Corporation |

| TXN | Texas Instruments Incorporated |

| VRSK | Verisk Analytics, Inc. |

| WDC | Western Digital Corporation |

| XLNX | Xilinx, Inc. |

Appendix B. Empirical Results

- 1.

- Number of standard deviations.Table A2. Comparison of results using the Hurst exponent selection method for the period 1999–2003 with 20 pairs and different numbers of standard deviations.Table A2. Comparison of results using the Hurst exponent selection method for the period 1999–2003 with 20 pairs and different numbers of standard deviations.

b Calculation Method k Sharpe Profit TC Cointegration 1.0 0.39 14.55% Cointegration 1.5 0.60 26.00% Cointegration 2.0 0.59 24.08% Correlation 1.0 0.15 6.10% Correlation 1.5 0.17 8.21% Correlation 2.0 0.31 13.82% EW 1.0 −0.28 −11.25% EW 1.5 0.38 15.49% EW 2.0 0.21 7.74% Lowest Hurst Exponent 1.0 0.70 40.51% Lowest Hurst Exponent 1.5 0.51 28.00% Lowest Hurst Exponent 2.0 0.57 28.51% Minimal Distance 1.0 0.03 0.05% Minimal Distance 1.5 0.39 15.70% Minimal Distance 2.0 0.31 11.48% Volatility 1.0 0.49 18.22% Volatility 1.5 0.41 16.37% Volatility 2.0 0.25 9.12% number of standard deviations; Sharpe Ratio; Profitability with transaction costs. - 2.

- Distance (1999–2003).Table A3. Comparison of results using the distance selection method for the period 1999–2003.

b Calculation Method N Oper AR %Profit TC Sharpe Max Drawdown Cointegration 10 1375 0.40% 0.72% 0.05 13.70% Correlation 10 1357 −0.60% −4.36% −0.07 18.60% EW 10 1403 −1.30% −7.30% −0.15 19.60% Minimal distancie 10 1389 −0.90% −5.49% −0.10 16.30% Lowest Hurst Exponent 10 1352 −1.50% −8.55% −0.16 19.20% Volatility 10 1370 −1.30% −7.57% −0.16 13.90% Cointegration 20 2786 3.50% 16.31% 0.47 7.40% Correlation 20 2630 2.80% 12.68% 0.36 9.20% EW 20 2884 1.00% 3.36% 0.14 12.30% Minimal distancie 20 2794 2.50% 11.00% 0.34 8.30% Lowest Hurst Exponent 20 2685 0.60% 1.66% 0.08 12.00% Volatility 20 2812 0.40% 0.39% 0.06 8.70% Cointegration 30 4116 2.80% 12.83% 0.42 8.00% Correlation 30 3830 2.00% 8.62% 0.27 12.60% EW 30 4247 1.10% 4.18% 0.18 14.80% Minimal distancie 30 4105 1.90% 7.93% 0.28 8.40% Lowest Hurst Exponent 30 3861 0.30% 0.01% 0.04 11.80% Volatility 30 4160 0,10% -0,99% 0.01 9,20% Number of pairs; Number of operations; Annualised return; Profitability with transaction costs; Sharpe Ratio. - 3.

- Distance (2007–2012).Table A4. Comparison of results using the distance selection method for the period 2007–2012.

b Calculation Method N Oper AR %Profit TC Sharpe Max Drawdown Cointegration 10 1666 1.80% 8.73% 0.35 10.20% Correlation 10 1594 3.50% 19.51% 0.55 12.10% EW 10 1677 1.20% 5.42% 0.22 9.40% Minimal distance 10 1649 2.80% 15.15% 0.56 8.80% Lowest Hurst Exponent 10 1677 2.60% 13.42% 0.51 8.00% Volatility 10 1684 1.20% 5.22% 0.24 11.90% Cointegration 20 3168 2.60% 13.82% 0.60 6.50% Correlation 20 2985 3.10% 16.91% 0.58 9.30% EW 20 3219 1.70% 8.19% 0.36 4.20% Minimal distance 20 3172 3.10% 17.01% 0.72 6.20% Lowest Hurst Exponent 20 3116 2.20% 11.54% 0.51 7.20% Volatility 20 3221 2.00% 9.89% 0.48 10.00% Cointegration 30 4714 1.50% 7.33% 0.38 6.70% Correlation 30 4453 1.40% 6.42% 0.29 10.90% EW 30 4791 1.40% 6.50% 0.34 5.30% Minimal distance 30 4709 1.70% 8.43% 0.44 5.90% Lowest Hurst Exponent 30 4545 1.40% 6.48% 0.35 6.80% Volatility 30 4785 1.60% 7.60% 0.43 9.00% Number of pairs; Number of operations; Annualised return; Profitability with transaction costs; Sharpe Ratio. - 4.

- Spearman Correlation (1999–2003).Table A5. Comparison of results using the Spearman correlation selection method for the period 1999–2003.Table A5. Comparison of results using the Spearman correlation selection method for the period 1999–2003.

b Calculation Method N Oper AR %Profit TC Sharpe Max Drawdown Cointegration 10 1274 4.10% 19.93% 0.50 14.30% Correlation 10 1432 3.00% 13.67% 0.36 11.20% EW 10 1400 4.30% 20.80% 0.56 9.30% Minimal distance 10 1219 4.00% 19.68% 0.51 12.50% Lowest Hurst Exponent 10 1103 5.70% 29.20% 0.64 10.70% Volatility 10 1405 3.30% 15.39% 0.45 8.40% Cointegration 20 2583 4.70% 23.41% 0.69 12.30% Correlation 20 2833 3.90% 18.78% 0.55 10.90% EW 20 2814 2.80% 12.69% 0.45 8.30% Minimal distance 20 2538 4.40% 21.63% 0.65 12.50% Lowest Hurst Exponent 20 2176 3.50% 16.71% 0.48 10.40% Volatility 20 2781 2.50% 11.01% 0.41 9.30% Cointegration 30 3776 4.90% 24.54% 0.79 8.10% Correlation 30 4196 2.80% 12.90% 0.41 8.60% EW 30 4168 0.40% 0.71% 0.08 9.90% Minimal distance 30 3717 4.20% 20.76% 0.69 8.30% Lowest Hurst Exponent 30 3236 4.20% 20.72% 0.56 8.20% Volatility 30 4125 1.20% 4.52% 0.22 9.50% Number of pairs; Number of operations; Annualised return; Profitability with transaction costs; Sharpe Ratio. - 5.

- Spearman Correlation (2007–2012).Table A6. Comparison of results using the Spearman correlation selection method for the period 2007–2012.Table A6. Comparison of results using the Spearman correlation selection method for the period 2007–2012.

b Calculation Method N Oper AR %Profit TC Sharpe Max Drawdown Cointegration 10 1614 1.70% 8.09% 0.38 8.30% Correlation 10 1653 2.90% 15.75% 0.75 4.60% EW 10 1620 1.20% 5.28% 0.37 7.00% Minimal distancie 10 1551 2.50% 13.05% 0.58 7.80% Lowest Hurst Exponent 10 1117 1.30% 6.18% 0.42 4.20% Volatility 10 1668 2.30% 12.13% 0.72 5.00% Cointegration 20 3022 1.00% 4.09% 0.29 6.80% Correlation 20 3268 2.60% 13.77% 0.75 4.00% EW 20 3236 1.40% 6.78% 0.46 5.70% Minimal distance 20 2944 1.10% 4.93% 0.34 7.80% Lowest Hurst Exponent 20 1966 0.40% 1.12% 0.14 3.90% Volatility 20 3282 1.30% 5.76% 0.42 4.70% Cointegration 30 4342 0.80% 3.15% 0.27 5.80% Correlation 30 4872 2.60% 13.58% 0.74 4.30% EW 30 4814 1.60% 7.80% 0.57 4.90% Minimal distance 30 4222 0.90% 3.69% 0.30 7.00% Lowest Hurst Exponent 30 2718 0.60% 2.49% 0.26 2.80% Volatility 30 4864 1.90% 9.28% 0.67 3.60% Number of pairs; Number of operations; Annualised return; Profitability with transaction costs; Sharpe Ratio. - 6.

- Cointegration (1999–2003).Table A7. Comparison of results using the cointegration selection method for the period 1999–2003.

b Calculation Method N Oper AR %Profit TC Sharpe Max Drawdown Cointegration 10 998 5.30% 26.80% 0.58 12.40% Correlation 10 1015 7.30% 39.38% 0.78 9.30% EW 10 1369 4.30% 20.83% 0.41 10.30% Minimal distance 10 945 4.00% 19.45% 0.47 9.40% Lowest Hurst Exponent 10 1123 7.70% 41.68% 0.79 11.90% Volatility 10 1376 6.90% 36.62% 0.68 11.00% Cointegration 20 1984 5.50% 28.41% 0.78 9.00% Correlation 20 1985 5.50% 28.31% 0.76 6.40% EW 20 2718 2.90% 13.24% 0.36 9.90% Minimal distance 20 1876 4.50% 22.36% 0.67 8.10% Lowest Hurst Exponent 20 2031 6.90% 36.88% 0.90 7.70% Volatility 20 2688 4.10% 19.76% 0.50 11.50% Cointegration 30 2957 0.90% 3.51% 0.14 11.00% Correlation 30 3132 2.40% 11.06% 0.36 10.30% EW 30 4064 −0.10% −1.85% −0.01 12.20% Minimal distance 30 2783 0.70% 2.67% 0.12 9.40% Lowest Hurst Exponent 30 2924 3.60% 17.23% 0.50 7.50% Volatility 30 4040 0.90% 3.25% 0.12 13.00% Number of pairs; Number of operations; Annualised return; Profitability with transaction costs; Sharpe Ratio. - 7.

- Cointegration (2007–2012).Table A8. Comparison of results using the cointegration selection method for the period 2007–2012.

b Calculation Method N Oper AR %Profit TC Sharpe Max Drawdown Cointegration 10 1516 −1.00% −6.82% −0.19 15.50% Correlation 10 1512 −0.10% −2.11% −0.02 14.70% EW 10 1604 1.40% 6.80% 0.30 9.60% Minimal distance 10 1478 0.70% 2.32% 0.12 12.50% Lowest Hurst Exponent 10 1502 −1.60% −9.90% −0.32 10.90% Volatility 10 1635 −0.10% −2.14% −0.02 12.90% Cointegration 20 2884 −0.70% −5.44% −0.19 9.90% Correlation 20 2955 −0.70% −5.28% −0.16 11.70% EW 20 3195 1.80% 8.90% 0.48 4.40% Minimal distance 20 2709 0.20% −0.15% 0.06 9.50% Lowest Hurst Exponent 20 2666 −0.90% −6.53% −0.26 9.00% Volatility 20 3189 0.50% 1.31% 0.14 8.90% Cointegration 30 4142 0.00% −1.38% 0.00 8.80% Correlation 30 4373 0.20% −0.56% 0.04 9.50% EW 30 4720 2.70% 14.63% 0.75 4.90% Minimal distance 30 3923 1.10% 4.69% 0.28 7.90% Lowest Hurst Exponent 30 3694 −0.30% −2.93% −0.09 7.60% Volatility 30 4742 1.30% 5.82% 0.36 7.00% Number of pairs; Number of operations; Annualised return; Profitability with transaction costs; Sharpe Ratio. - 8.

- Hurst exponent (1999–2003).Table A9. Comparison of results using the Hurst exponent selection method for the period 1999–2003.

b Calculation Method N Oper AR %Profit TC Sharpe Max Drawdown Cointegration 10 1136 −0.60% −3.94% −0.06 15.60% Correlation 10 1176 0.50% 1.32% 0.04 24.40% EW 10 1334 2.80% 12.87% 0.29 12.20% Minimal distance 10 1166 −1.20% −6.87% −0.12 13.50% Lowest Hurst Exponent 10 1234 4.60% 22.77% 0.37 21.40% Volatility 10 1401 7.40% 39.60% 0.72 14.40% Cointegration 20 2104 3.10% 14.55% 0.39 11.10% Correlation 20 2400 1.50% 6.10% 0.15 15.70% EW 20 2695 -2.10% −11.25% −0.28 12.30% Minimal distance 20 2093 0.20% 0.05% 0.03 10.60% Lowest Hurst Exponent 20 2375 7.50% 40.51% 0.70 17.10% Volatility 20 2755 3.80% 18.22% 0.49 8.90% Cointegration 30 2984 3.10% 14.91% 0.48 7.80% Correlation 30 3516 2.00% 8.83% 0.22 16.50% EW 30 4066 −1.30% −7.56% −0.19 11.80% Minimal distance 30 2915 2.70% 12.63% 0.41 6.50% Lowest Hurst Exponent 30 3411 7.10% 37.86% 0.78 13.40% Volatility 30 3994 4.40% 21.57% 0.63 6.50% Number of pairs; Number of operations; Annualised return; Profitability with transaction costs; Sharpe Ratio. - 9.

- Hurst exponent (2007–2012).Table A10. Comparison of results using the Hurst exponent selection method for the period 2007–2012.Table A10. Comparison of results using the Hurst exponent selection method for the period 2007–2012.

b Calculation Method N Oper AR %Profit TC Sharpe Max Drawdown Cointegration 10 1596 3.00% 16.40% 0.55 8.00% Correlation 10 1587 3.70% 21.51% 0.57 9.80% EW 10 1643 3.00% 16.26% 0.59 9.10% Minimal distancie 10 1581 2.10% 11.02% 0.41 8.70% Lowest Hurst Exponent 10 1649 4.80% 28.15% 0.83 8.30% Volatility 10 1724 1.30% 5.98% 0.27 8.40% Cointegration 20 2795 0.80% 3.40% 0.21 7.10% Correlation 20 3001 2.60% 14.10% 0.50 7.50% EW 20 3258 1.70% 8.27% 0.40 9.10% Minimal distancie 20 2758 −0.40% −3.48% −0.10 10.60% Lowest Hurst Exponent 20 3129 1.90% 9.84% 0.39 8.30% Volatility 20 3204 0.40% 0.90% 0.11 6.40% Cointegration 30 4100 −0.20% −2.27% −0.05 9.30% Correlation 30 4418 2.00% 10.23% 0.43 8.10% EW 30 4666 1.90% 9.34% 0.46 7.60% Minimal distancie 30 4049 0.00% −1.55% −0.01 10.50% Lowest Hurst Exponent 30 4248 0.40% 0.78% 0.09 9.20% Volatility 30 4790 0.60% 1.50% 0.15 8.40% Number of pairs; Number of operations; Annualised return; Profitability with transaction costs; Sharpe Ratio.

References

- Fama, E. Efficient capital markets: II. J. Financ. 1991, 46, 1575–1617. [Google Scholar] [CrossRef]

- Dimson, E.; Mussavian, M. A brief history of market efficiency. Eur. Financ. Manag. 1998, 4, 91–193. [Google Scholar] [CrossRef] [Green Version]

- Di Matteo, T.; Aste, T.; Dacorogna, M.M. Using the scaling analysis to characterize their stage of development. J. Bank. Financ. 2005, 29, 827–851. [Google Scholar] [CrossRef] [Green Version]

- Di Matteo, T. Multi-scaling in finance. Quant. Financ. 2007, 7, 21–36. [Google Scholar] [CrossRef]

- Peters, E.E. Chaos and Order in the Capital Markets. A New View of Cycle, Prices, and Market Volatility; Wiley: New York, NY, USA, 1991. [Google Scholar]

- Peters, E.E. Fractal Market Analysis: Applying Chaos Theory to Investment and Economics; Wiley: New York, NY, USA, 1994. [Google Scholar]

- Lo, A.W. The adaptive markets hypothesis: Market efficiency from an evolutionary perspective. J. Portf. Manag. 2004, 30, 15–29. [Google Scholar] [CrossRef]

- Sanchez-Granero, M.A.; Trinidad Segovia, J.E.; García, J.; Fernández-Martínez, M. The effect of the underlying distribution in Hurst exponent estimation. PLoS ONE 2015, 28, e0127824. [Google Scholar]

- Sánchez-Granero, M.A.; Balladares, K.A.; Ramos-Requena, J.P.; Trinidad-Segovia, J.E. Testing the efficient market hypothesis in Latin American stock markets. Phys. A Stat. Mech. Its Appl. 2020, 540, 123082. [Google Scholar] [CrossRef]

- Zhang, H.; Urquhart, A. Pairs trading across Mainland China and Hong Kong stock Markets. Int. J. Financ. Econ. 2019, 24, 698–726. [Google Scholar] [CrossRef]

- Ramos-Requena, J.P.; Trinidad-Segovia, J.E.; Sanchez-Granero, M.A. Introducing Hurst exponent in pairs trading. Phys. A Stat. Mech. Its Appl. 2017, 488, 39–45. [Google Scholar] [CrossRef]

- Taqqu, M.S.; Teverovsky, V. Estimators for long range dependence: An empirical study. Fractals 1995, 3, 785–798. [Google Scholar] [CrossRef]

- Kristoufek, L.; Vosvrda, M. Measuring capital market efficiency: Global and local correlations structure. Phys. A Stat. Mech. Its Appl. 2013, 392, 184–193. [Google Scholar] [CrossRef] [Green Version]

- Kristoufek, L.; Vosvrda, M. Measuring capital market efficiency: Long-term memory, fractal dimension and approximate entropy. Eur. Phys. J. B 2014, 87, 162. [Google Scholar] [CrossRef] [Green Version]

- Zunino, L.; Zanin, M.; Tabak, B.M.; Pérez, D.G.; Rosso, O.A. Complexity-entropy causality plane: A useful approach to quantify the stock market inefficiency. Phys. A Stat. Mech. Its Appl. 2010, 389, 1891–1901. [Google Scholar] [CrossRef] [Green Version]

- Gatev, E.; Goetzmann, W.; Rouwenhorst, K. Pairs Trading: Performance of a relative value arbitrage rule. Rev. Financ. Stud. 2006, 19, 797–827. [Google Scholar] [CrossRef] [Green Version]

- Vidyamurthy, G. Pairs Trading, Quantitative Methods and Analysis; John Wiley and Sons: Toronto, ON, Canada, 2004. [Google Scholar]

- Dunis, L.; Ho, R. Cointegration portfolios of European equities for index tracking and market neutral strategies. J. Asset Manag. 2005, 6, 33–52. [Google Scholar] [CrossRef]

- Figuerola Ferretti, I.; Paraskevopoulos, I.; Tang, T. Pairs trading and spread persistence in the European stock market. J. Futur. Mark. 2018, 38, 998–1023. [Google Scholar] [CrossRef]

- Alexander, C.; Dimitriu, A. The Cointegration Alpha: Enhanced Index Tracking and Long-Short Equity Market Neutral Strategies; SSRN eLibrary: Rochester, NY, USA, 2002. [Google Scholar]

- Perlin, M.S. Evaluation of Pairs Trading strategy at the Brazilian financial market. J. Deriv. Hedge Funds 2009, 15, 122–136. [Google Scholar] [CrossRef] [Green Version]

- Caldeira, J.F.; Moura, G.V. Selection of a Portfolio of Pairs Based on Cointegration: A Statistical Arbitrage Strategy; Revista Brasileira de Financas (Online): Rio de Janeiro, Brazil, 2013; Volume 11, pp. 49–80. [Google Scholar]

- Burgess, A.N. Using cointegration to hedge and trade international equities. In Applied Quantitative Methods for Trading and Investment; John Wiley and Sons: Chichester, UK, 2003; pp. 41–69. [Google Scholar]

- Galenko, A.; Popova, E.; Popova, I. Trading in the presence of cointegration. J. Altern. Investments 2012, 15, 85–97. [Google Scholar] [CrossRef]

- Lin, Y.X.; Mccrae, M.; Gulati, C. Loss protection in Pairs Trading through minimum profit bounds: A cointegration approach. J. Appl. Math. Decis. Sci. 2006. [Google Scholar] [CrossRef]

- Nath, P. High frequency Pairs Trading with U.S Treasury Securities: Risks and Rewards for Hedge Funds; SSRN eLibrary: Rochester, NY, USA, 2003. [Google Scholar]

- Elliott, R.; van der Hoek, J.; Malcolm, W. Pairs Trading. Quant. Financ. 2005, 5, 271–276. [Google Scholar] [CrossRef]

- Dunis, C.L.; Shannon, G. Emerging markets of South-East and Central Asia: Do they still offer a diversification benefit? J. Asset Manag. 2005, 6, 168–190. [Google Scholar] [CrossRef]

- Ramos-Requena, J.P.; Trinidad-Segovia, J.E.; Sánchez-Granero, M.A. An Alternative Approach to Measure Co-Movement between Two Time Series. Mathematics 2020, 8, 261. [Google Scholar] [CrossRef] [Green Version]

- Baur, D. What Is Co-movement? In IPSC-Technological and Economic Risk Management; Technical Report; European Commission, Joint Research Center: Ispra, VA, Italy, 2003. [Google Scholar]

- Hauke, J.; Kossowski, T. Comparison of values of Pearson’s and Spearman’s correlation coefficients on the same sets of data. Quaest. Geogr. 2011, 30, 87–93. [Google Scholar] [CrossRef] [Green Version]

- Engle, R.F.; Granger, C.W.J. Co-integration and error correction: Representation, estimation, and testing. Econometrica 1987, 5, 251–276. [Google Scholar] [CrossRef]

- Do, B.; Faff, R. Does simple pairs trading still work? Financ. Anal. J. 2010, 66, 83–95. [Google Scholar] [CrossRef]

- Do, B.; Faff, R. Are pairs trading profits robust to trading costs? J. Financ. Res. 2012, 35, 261–287. [Google Scholar] [CrossRef]

- Hurst, H. Long term storage capacity of reservoirs. Trans. Am. Soc. Civ. Eng. 1951, 6, 770–799. [Google Scholar]

- Mandelbrot, B.; Wallis, J.R. Robustness of the rescaled range R/S in the measurement of noncyclic long-run statistical dependence. Water Resour. Res. 1969, 5, 967–988. [Google Scholar] [CrossRef]

- Peng, C.K.; Buldyrev, S.V.; Havlin, S.; Simons, M.; Stanley, H.E.; Goldberger, A.L. Mosaic organization of DNA nucleotides. Phys. Rev. E 1994, 49, 1685–1689. [Google Scholar] [CrossRef] [Green Version]

- Lo, A.W. Long-term memory in stock market prices. Econometrica 1991, 59, 1279–1313. [Google Scholar] [CrossRef]

- Sanchez-Granero, M.A.; Trinidad-Segovia, J.E.; Garcia-Perez, J. Some comments on Hurst exponent and the long memory processes on capital markets. Phys. A Stat. Mech. Its Appl. 2008, 387, 5543–5551. [Google Scholar] [CrossRef]

- Weron, R. Estimating long-range dependence: Finite sample properties and confidence intervals. Phys. A Stat. Mech. Its Appl. 2002, 312, 285–299. [Google Scholar] [CrossRef] [Green Version]

- Willinger, W.; Taqqu, M.S.; Teverovsky, V. Stock market prices and long-range dependence. Financ. Stochastics 1999, 3, 1–13. [Google Scholar] [CrossRef]

- Barabasi, A.L.; Vicsek, T. Multifractality of self affine fractals. Phys. Rev. A 1991, 44, 2730–2733. [Google Scholar] [CrossRef]

- Barunik, J.; Kristoufek, L. On Hurst exponent estimation under heavy-tailed distributions. Phys. A Stat. Mech. Its Appl. 2010, 389, 3844–3855. [Google Scholar] [CrossRef] [Green Version]

- Goulart Coelho, L.M.; Lange, L.C.; Coelho, H.M. Multi-criteria decision making to support waste management: A critical review of current practices and methods. Waste Manag. Res. 2017, 35, 3–28. [Google Scholar] [CrossRef]

- Meng, K.; Cao, Y.; Peng, X.; Prybutok, V.; Gupta, V. Demand-dependent recovery decision-making of a batch of products for sustainability. Int. J. Prod. Econ. 2019, 107552. [Google Scholar] [CrossRef]

- Roth, S.; Hirschberg, S.; Bauer, C.; Burgherr, P.; Dones, R.; Heck, T.; Schenler, W. Sustainability of electricity supply technology portfolio. Ann. Nucl. Energy 2009, 36, 409–416. [Google Scholar] [CrossRef]

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ramos-Requena, J.P.; Trinidad-Segovia, J.E.; Sánchez-Granero, M.Á. Some Notes on the Formation of a Pair in Pairs Trading. Mathematics 2020, 8, 348. https://doi.org/10.3390/math8030348

Ramos-Requena JP, Trinidad-Segovia JE, Sánchez-Granero MÁ. Some Notes on the Formation of a Pair in Pairs Trading. Mathematics. 2020; 8(3):348. https://doi.org/10.3390/math8030348

Chicago/Turabian StyleRamos-Requena, José Pedro, Juan Evangelista Trinidad-Segovia, and Miguel Ángel Sánchez-Granero. 2020. "Some Notes on the Formation of a Pair in Pairs Trading" Mathematics 8, no. 3: 348. https://doi.org/10.3390/math8030348

APA StyleRamos-Requena, J. P., Trinidad-Segovia, J. E., & Sánchez-Granero, M. Á. (2020). Some Notes on the Formation of a Pair in Pairs Trading. Mathematics, 8(3), 348. https://doi.org/10.3390/math8030348