1. Introduction

American options are a special type of vanilla option that can be considered among the most basic financial derivatives. By allowing for the possibility to exercise at any time before the day of expiration, they add a new dimension to their valuation that escapes the consolidated hedging and arbitrage-free pricing frameworks. The methodology to value an American option can be traced back to [

1], which suggested transforming this problem into a free-boundary problem. However, even in the simplest case first proposed by [

2], where the underlying stock is modeled by a geometric Brownian motion, it took almost 40 years to reach a complete and rigorous derivation of its solution. This was given in [

3], where it was finally proved that the free-boundary equation characterizes the optimal stopping boundary. A good historical survey on the topic can be found in [

4].

The literature on the valuation of American options is considerable, and there have been many attempts to extend the classes of stochastic processes that could model the dynamics of the underlying stock. However, sometimes this has been achieved at the cost of reducing the completeness of the result. For example, Detemple et al. [

5] treats more general diffusion processes and proves that the optimal strategy satisfies the free-boundary equation, but it leaves open the proof of the uniqueness of the solution. The more recent work [

6] provides a closed-form expression of the optimal stopping boundary for a fairly general class of diffusion processes by expressing it in terms of Maclaurin series. However, as in [

5], it requires a boundedness assumption on the derivative of the drift term that excludes the class of Gaussian bridges. This class of processes has recently attracted attention to model situations where some future knowledge about the dynamics of the underlying assets is disclosed to the trading agent, see, e.g., [

7,

8,

9,

10]. However, these results are mostly focused into quantifying the value of the disclosed information and do not deal with its effect on the execution strategy of a held option.

In the area of option pricing, a first analysis of the Brownian bridge was done in [

11] by exploiting a time transformation that converts the problem into one about the more tractable Brownian motion. Later, the applicability of this work in the problem of optimally selling a bond was highlighted in [

12]. Successively, in [

13], the authors take up the problem in [

11] by reframing it into the wider context of the free-boundary problem and they extend its solution to a wider class of gain functions. In particular, in [

13], the Brownian bridge process is presented as a possible model for financial applications under special market conditions, such as the so-called “pinning effect”.

The pinning effect refers to the situation in which the price of a given stock approaches the strike price of a highly-traded option close to its expiration date. Evidence for the pinning effect was first reported in [

14], where the authors employ a bridge process to model stock pinning by tuning a geometric Brownian motion. In [

15], the authors postulate that the pinning behavior is mainly driven by delta-hedging of long option positions and consider, as a model for the stock price, a stochastic differential equation with a drift that pulls the price towards a neighborhood of the strike price. Later, the results in [

16] add real data evidence in support for this model. In [

17], the same assumption is validated and a comprehensive set of evidence for the pinning phenomenon is reported. The model of [

15] is generalized in [

18] by adding a diffusion term that shrinks the volatility near the strike price.

Motivated by these findings, we study in this paper the best strategy for executing an American put option in the presence of stock pinning. Similarly to [

13], we model the underlying stock by a Brownian bridge. Differently, we include a discount factor in the gain function that makes the problem more realistic. This addition makes more challenging the associated optimal stopping problem, as it involves a non-perpetual option that is non-homogeneous in time. We solve this corresponding optimal stopping problem, in the spirit of [

3,

19], by characterizing the optimal stopping boundary as the unique solution of a Volterra integral equation up to some regularity conditions.

Besides contributing with the solution to this original problem, we also explore its applicability in real situations. The studied model may be too simple to be applied with real data, but it allows for computing exact solutions and to easily quantify the uncertainty about the knowledge of its parameters. For this reason, we describe an algorithm to numerically compute the optimal strategy and provide the confidence curves around the optimal stopping boundary when the stock volatility is estimated via maximum likelihood. This inferential method is potentially relevant for an investor that only has access to discrete data.

In addition, we test our results on a real dataset comprised by financial options on Apple and IBM equities. Our model is competitive when compared with a model based on a geometric Brownian motion and, in accordance with the motivation of our work, the best performances are obtained when the stock price exhibits a pinning-at-the-strike behavior. Finally, since our mathematical model is strongly based on the particular assumption of the pinning-at-the-strike behavior, we briefly show what effects we should expect in case of relaxing this assumption, at least from a qualitative point of view, and why a more complete analysis would require more sophisticated tools.

We conclude by mentioning related works using similar models. In [

20], the authors tackle the non-discounted problem for a Brownian bridge with a normally-distributed ending point. More recently, Ekstrom et al. [

21] solves the same problem for small values of the variance, finding bounds for the value function when the pinning point follows a general distribution with a finite first moment. A double stopping problem, for which the aim is to maximize the mean difference between two stopping times, is analyzed in [

22]. The recent paper [

19] solves the non-discounted problem using the exponential of a Brownian bridge to model the stock prices. A Brownian bridge with unknown pinning random distribution and a Bayesian approach is advocated by [

23]. The analytical results in [

13] are extended in [

24] by looking at a class of Gaussian bridges that share the same optimal stopping boundary. The discounted problem with a Brownian bridge and in the presence of random pinning point is addressed in [

25], under regularity assumptions on the gain function that allow for an application of the standard Itô’s formula (something that does not hold in our setting).

The rest of the paper is structured as follows. In

Section 2, we introduce the model along with notations and definitions.

Section 3 provides the theoretical results required for obtaining the free-boundary equation.

Section 4 deals with the problem of computing the optimal stopping boundary and quantifying the uncertainty associated with the estimation of the stock volatility.

Section 5 compares our method with the optimal exercise time based on a geometric Brownian motion by using real data exhibiting various degrees of pinning.

Section 6 comments about the relaxation of the pinning-at-the-strike assumption and, finally,

Section 7 offers some conclusions.

2. Problem Setting

We introduce next the model of the financial asset and we define the optimal stopping problem whose solution constitutes the best strategy to exercise an American put option based on that asset.

We assume that the financial option has a strike price

and a maturity date

. To model the pinning effect, we use a Brownian bridge process for the dynamics of the underlying asset. Indeed, this process may be seen as a Brownian motion conditioned to terminate at a known terminal value, that in our case is fixed to the strike price

S (see

Section 6 for a discussion on the relaxation of this assumption). That is, by calling

to the asset price process, with

, we assume it satisfies the SDE:

with

or, equivalently, it has the explicit expression

again with

and where, in both equations,

denotes a standard Brownian motion. To emphasize that the process almost surely satisfies the relation

, we will use the notation

and

to denote the corresponding probability and mean operators.

Denoting by

the

gain function of the put option and by

the discounting rate, we can finally write the optimal expected reward for exercising the American option as the

Optimal Stopping Problem (OSP)

The function V is called the value function and the supreme above is taken over all the stopping times of with respect to its natural filtration .

Under mild conditions, namely

V being lower semi-continuous and

G upper semi-continuous (see [

26], Corollary 2.9), it is guaranteed that the supremum in (

3) is achieved. The

Optimal Stopping Time (OST),

, is defined as the smallest stopping time attaining the supremum (

3) and can be characterized as the hitting time of a closed set

D, referred to as the

stopping set. Since these conditions on

V and

G are satisfied in our settings (see [

26], Remark 2.10), we can write

where

D is defined as

We then define the continuation set C as the complement of the set D and we denote by its boundary.

The OST, defined in (

4), can be interpreted as the best exercise strategy for the American option, and it allows for rewriting the value function

V in the simplified form

To solve the OSP given in (

3), we follow the well-known approach of reformulating it as a free-boundary problem, for the unknowns

V and

. The latter is commonly called the

Optimal Stopping Boundary (OSB). Our OSP is a finite-horizon problem that involves a time non-homogeneous process, with its associated free-boundary problem being

where

is the infinitesimal generator of the Brownian bridge

. Given a suitably smooth function

, the application of the operator

to it returns the function

Equations (

7a), (

7b), and (

7c) easily come from the definitions of

D,

C, and

(see Proposition 2 below), whereas (

7d), generally known as the

smooth fit condition, depends on how well-behaved the OSB is for the underlying process. The regularity of the OSB is an important factor in finding and characterizing the solution of the problem itself, and for this reason we will study it in detail in later sections. An in-depth survey on the optimal stopping theory that exploits the free-boundary approach can be found in [

26].

3. Optimally Exercising American Put Options for a Brownian Bridge

We present in this section the main result, consisting of the solution of the problem (

3). In particular, we solve the free boundary problem defined in (

7) by showing that the OSB can be written in terms of a function

that is

, and that this function can be computed as the solution to a Volterra integral equation.

From an applicative perspective, the function b defines the optimal strategy to follow in order to maximize the profit from the execution of the American put option. It is the best to exercise the option the first time the price of the underlying financial asset crosses at time the level .

Theorem 1. The optimal stopping time in (4) can be written aswhere the function b is defined as the unique solution, among the class of continuous functions of bounded variation lying below S, of the integral equation In addition, the value function V in (6) can be expressed as The kernel in (9) and (10) is defined aswhere Φ

and ϕ are, respectively, the distribution and the density functions of a standard normal random variable,and . The proof is in Appendix A. The proof of the theorem makes use of some important partial results that we state in the following propositions. All the proofs are deferred to

Appendix A.

The next result sheds some light on the shapes of the sets D and C, by showing that their common border can be expressed by means of a function b that satisfies some regularity conditions. In the proof, we focus on regions where it is easy to prove that the value function either exceeds or equals the immediate reward, thus revealing subsets of C and D, respectively. Those regions come from the fact that G is null above S and positive below, the paths of the process decrease with x (for a fixed realization), and V is non-increasing with respect to x, t, and .

Proposition 1. There exists a non-decreasing right-continuous function such that for all , , and . The proof is in Appendix A. The next proposition analyzes the regularity properties of the value function and proves that the smooth fit condition holds. It uses an extended version of the Itô’s formula (see Lemma A2) to prove the monotonicity property that exploits the regularity properties of the function b proved in Proposition 1. We later use these results in Proposition 3 to show the continuity of b. Part (i) comes from standard arguments on parabolic partial differential equations in conjunction with the Markovian property of the Brownian bridge. The rest of the proposition employs different methods, but they all rely on the fact that the OST for a pair is sub-optimal under different initial conditions.

Proposition 2. The value function V defined in (3) satisfies the following conditions: - (i)

V is on C and on D, and on C.

- (ii)

is convex and strictly decreasing for all . Moreover, - (iii)

The smooth fit condition holds, i.e., for all .

- (iv)

is non-increasing for all .

- (v)

V is continuous.

From the previous result, we are able to get a stronger result on the regularity of b that is used to characterize b as the unique solution of the Volterra equation. We prove it by assuming that the OSB allows discontinuities of the first type and reaching a contradiction. Then, since b is non-increasing and finite, it does not allow discontinuities of the second type either and must be continuous.

Proposition 3. The optimal stopping boundary b for the problem (3) is continuous. The proof is in Appendix A. Finally, the next proposition shows that the OSB satisfies the Volterra integral Equation (

9) and that it is the only solution up to some regularity conditions. The proof follows well-known procedures based on probabilistic arguments (see [

3]) rather than relying on integral equation’s theory, which usually uses some variation of the contraction mapping principle.

Proposition 4. The optimal stopping boundary b for the problem (3) can be characterized as the unique solution of the type two nonlinear Volterra integral Equation (9), within the class of continuous functions of bounded variation such that for all . The proof is in Appendix A. Remark 1. All the results in this section have their own analog when it comes to optimally exercising American call options, that is, when the gain function in (3) is substituted with . Indeed, exploiting the symmetry of the Brownian bridge and the gain functions, it is easy to check that the relation holds, where and stand for the OSBs for the call and the put option, respectively. Remark 2. Setting , we can recover the OSB that maximizes the mean of a Brownian bridge, and using the results in [11,13,27], we get an explicit expression for the OSB that is , with . 4. Boundary Computation and Inference

4.1. Solving the Free-Boundary Equation

The lack of an explicit solution for (

9) requires a numerical approach to compute the OSB. Let

be a grid in the interval

for some

. The method we consider builds on a proposal by [

28]. They suggested to approximate the integral in (

9) by a right Riemann sum, hence enabling the computation of the value of

, for

, by using only the values

, with

. Therefore, by knowing the value of the boundary at the last point

, one can obtain its value at the second last point

and recursively construct the whole OSB evaluated at

.

Under our settings, the right Riemann sum is no longer a valid option because we know from (

11) that, depending on the shape of the boundary

b near the expiration date,

could explode as

, so we cannot evaluate the kernel

K at the right point in the last subinterval

. To deal with this issue, we employ a right Riemann sum approximation along all the subintervals except the last one, ending up with the following discrete version of the Volterra integral Equation (

9):

for

, where

. It can be shown that

, where

by using (

12) and (

13), the form of the kernel (

11), and the fact that

and

for all

. Therefore,

can be seen as a reasonable approximation, admitting an upper bound for the error

, namely

. Moreover,

as

. After substituting

for

in (

15), we get

The procedure for computing the estimated boundary according to the previous approximations is laid down in Algorithm 1. From now on, we will use

to denote the cubic-spline interpolating curve that goes through the numerical approximation of the boundary at the points

via Algorithm 1.

| Algorithm 1: Optimal stopping boundary computation |

![Mathematics 08 01159 i001]() |

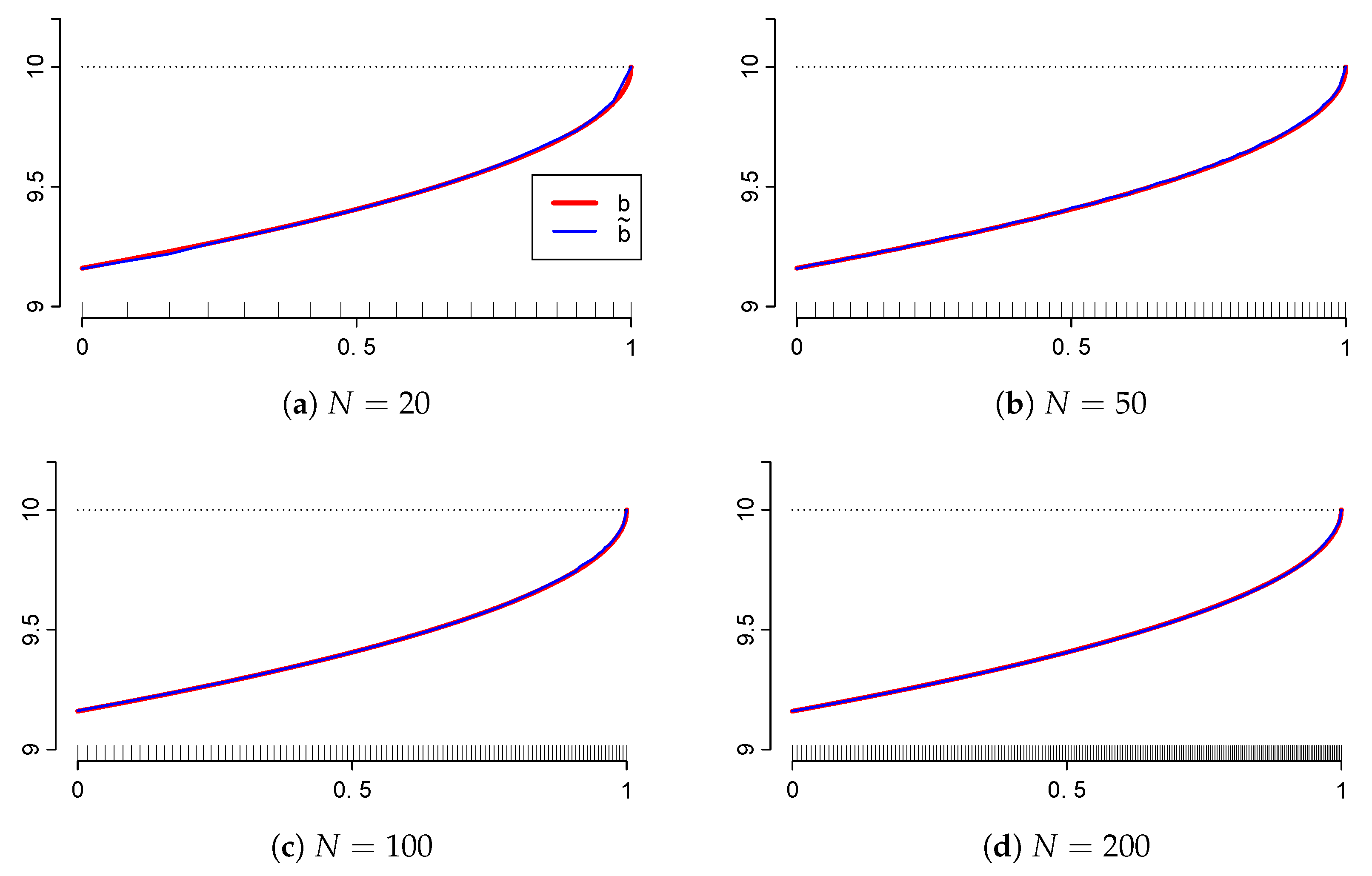

Recall from Remark 2 that our OSB for takes the form . Having the explicit form of allows us to validate the accuracy of Algorithm 1 and to tune up its parameters. We empirically determined that offers a good trade-off between accuracy and computational time. This value was considered every time Algorithm 1 was employed.

We decided to use a logarithmically-spaced grid that is

, with

, after systematically observing that uniform partitions tend to misbehave near the expiration date

T. In addition, it is preferable that the partition gets thinner close to

T in a smooth way.

Figure 1 shows how precise the Algorithm 1 is by comparing the computed boundary

versus its explicit form for

,

,

, and

.

4.2. Estimating the Volatility

We assume next that the volatility of the underlying process is unknown, as it may occur in real situations. It is well known that, under model (

1), one can exactly compute the volatility if the price dynamics are continuously observed. However, investors in real life have to deal with discrete-time observations and thus they would have to estimate

to obtain the OSB.

We start by assuming that we have recorded the price values at the times

, for

, so at

, with

, we have gathered a sample

from the historical path of the Brownian bridge

with

. From (

2), we have that

and the log-likelihood function of the volatility takes the form

where

C is a constant independent of

. The maximum likelihood estimator for

is given by

Under an equally spaced partition (

,

), standard results on maximum likelihood (see [

29]) give that

when

(hence

) and

such that

remains constant, with

.

4.3. Confidence Intervals for the Boundary

We present as follows the uncertainty propagated by the estimation of

to the computation of the OSB. In order to do so, we assume that the OSB is differentiable with respect to

, so we are allowed to apply the delta method, under the previous asymptotic conditions. This entails that

where

represents the OSB defined at (

9) associated with a process with volatility

. Plugging-in the estimate

into (

18) gives the following asymptotic

(pointwise) confidence curves for

:

where

represents the

-upper quantile of a standard normal distribution. Algorithm 1 can be used to compute an approximation of the term

by means of

for some small

. We denote by

the approximation of the confidence interval (

19) coming from this approach at

. Through the paper, we use

, as has been empirically checked to provide, along with

for Algorithm 1, a good compromise between accuracy, stability, and computational speed in calculating the confidence curves.

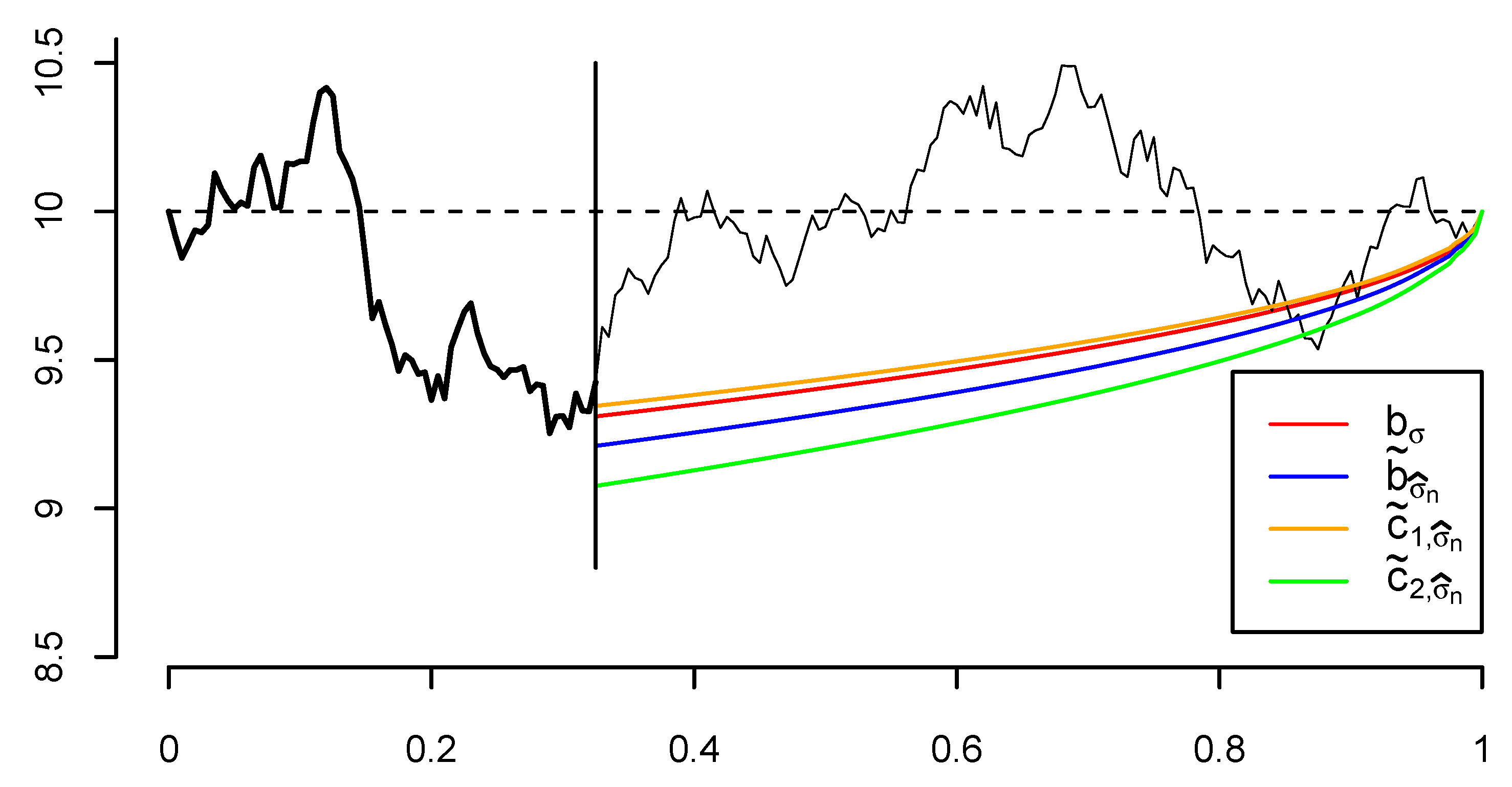

Figure 2 illustrates, for one path of a Brownian bridge, how the boundary estimation and its confidence curves work.

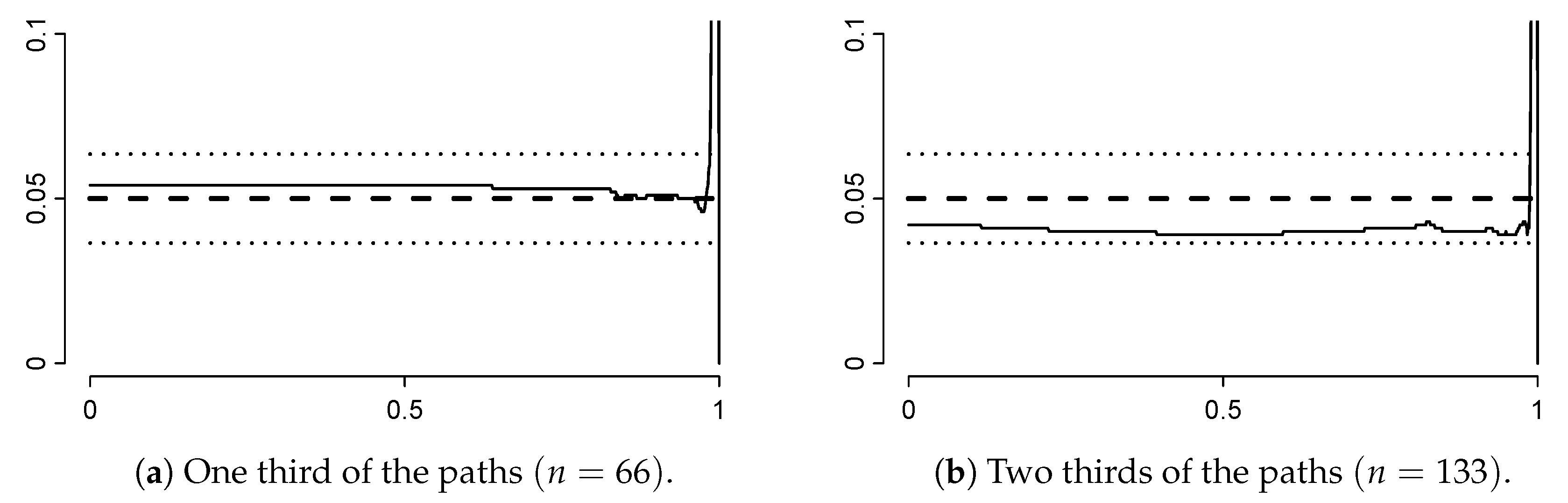

Figure 3 empirically validates the approximation of the confidence curves by marginally computing for each

the proportion of trials, out of

, in which the true boundary does not belong to the interval delimited by the confidence curves.

The spikes visible in

Figure 3 near the last point

indicate that the true boundary rarely lies within the confidence curves at those points. This happens because the confidence curves have zero variance at the maturity date

T (actually

), and the numerical approximation of

given at (

16) is slightly biased. This affects the accuracy of the estimated boundary by frequently leaving the true boundary outside the confidence curves near maturity. This drawback is negligible in practice, since the estimated boundary and the confidence curves are very close to the true boundary in terms of absolute distance.

4.4. Simulations

The ability to perform inference for the true OSB rises some natural questions: how much optimality is lost by when compared to ? How do the stopping strategies associated with the curves , , compare with the one for ? For example, a risk-averse (or risk-lover) strategy would be to consider the upper (lower) confidence curve () as the stopping rule, this being the most conservative (liberal) option within the uncertainty on estimating . A balanced strategy would be to consider the estimated boundary .

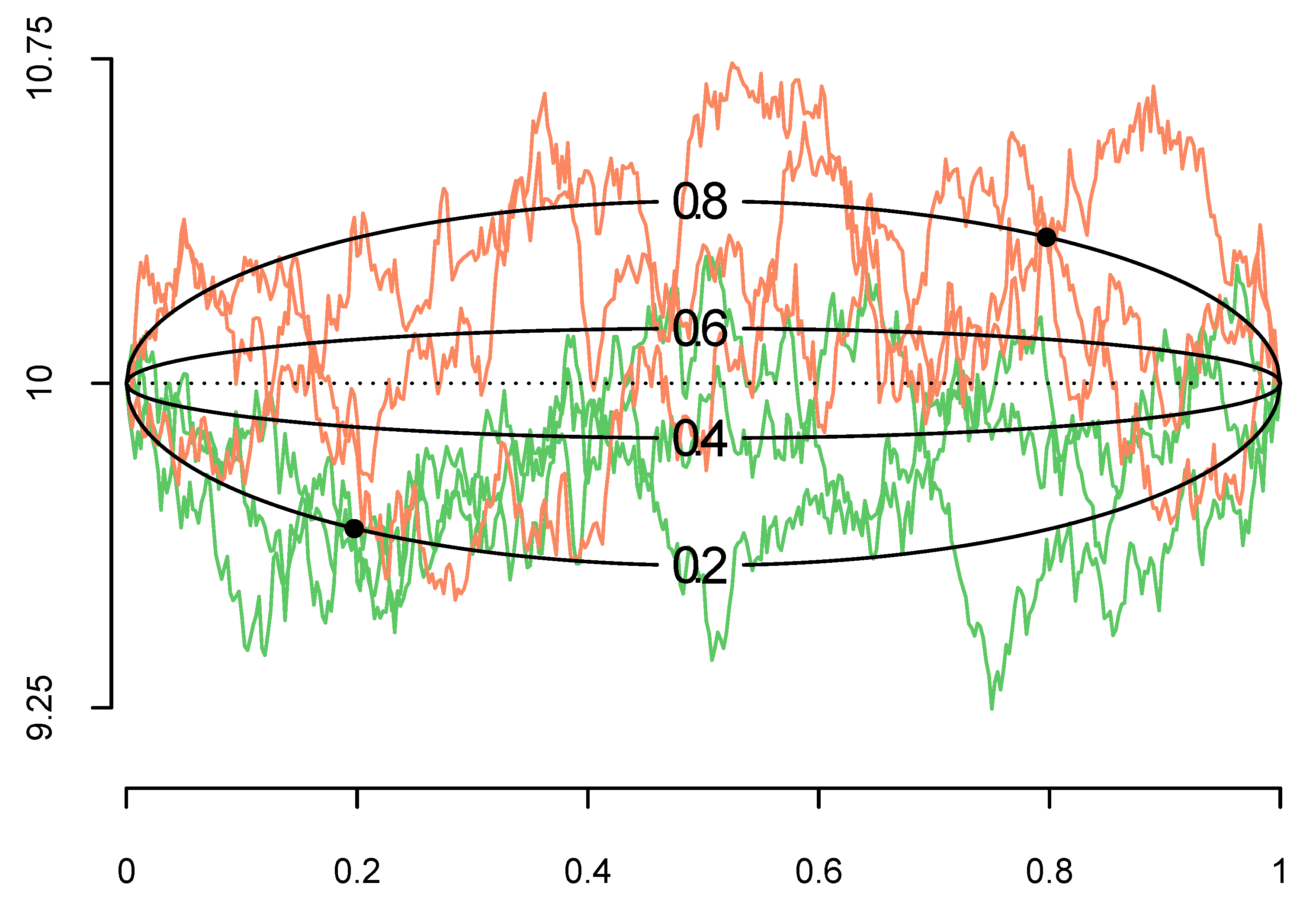

In the following, we investigate how these stopping strategies behave, assuming , , , , and . We first estimate the payoff associated with each of them, and then we compare these payoffs with the one generated by considering the true boundary in its explicit form (see Remark 2). The choice of is not restrictive as it is enough to rescale time by and space (i.e., the price values) by .

To perform the comparison, we defined a subset of

where the payoffs were computed. We carried out the comparison along the pairs

, for

,

, and

, where

and

represents the

q-quantile of the marginal distribution of the process at time

that is

(see

Figure 4).

For each

i and

q, we generated

different paths

of a Brownian bridge with volatility

going from

to

. Each path was sampled at times

, for

, for

and

. The idea behind this setting is to tackle both the low-frequency scenario, which regards investors with access to daily prices or less frequent data, and the high-frequency scenario, addressing high volumes of information as it happens to be when recording intraday prices. We forced each path to pass through

(see

Figure 4), and used the past

of each trajectory to estimate the boundary and the confidence curves. The future

was employed to gather

M observations of the payoff associated with each stopping rule, whose means and variances are shown below in

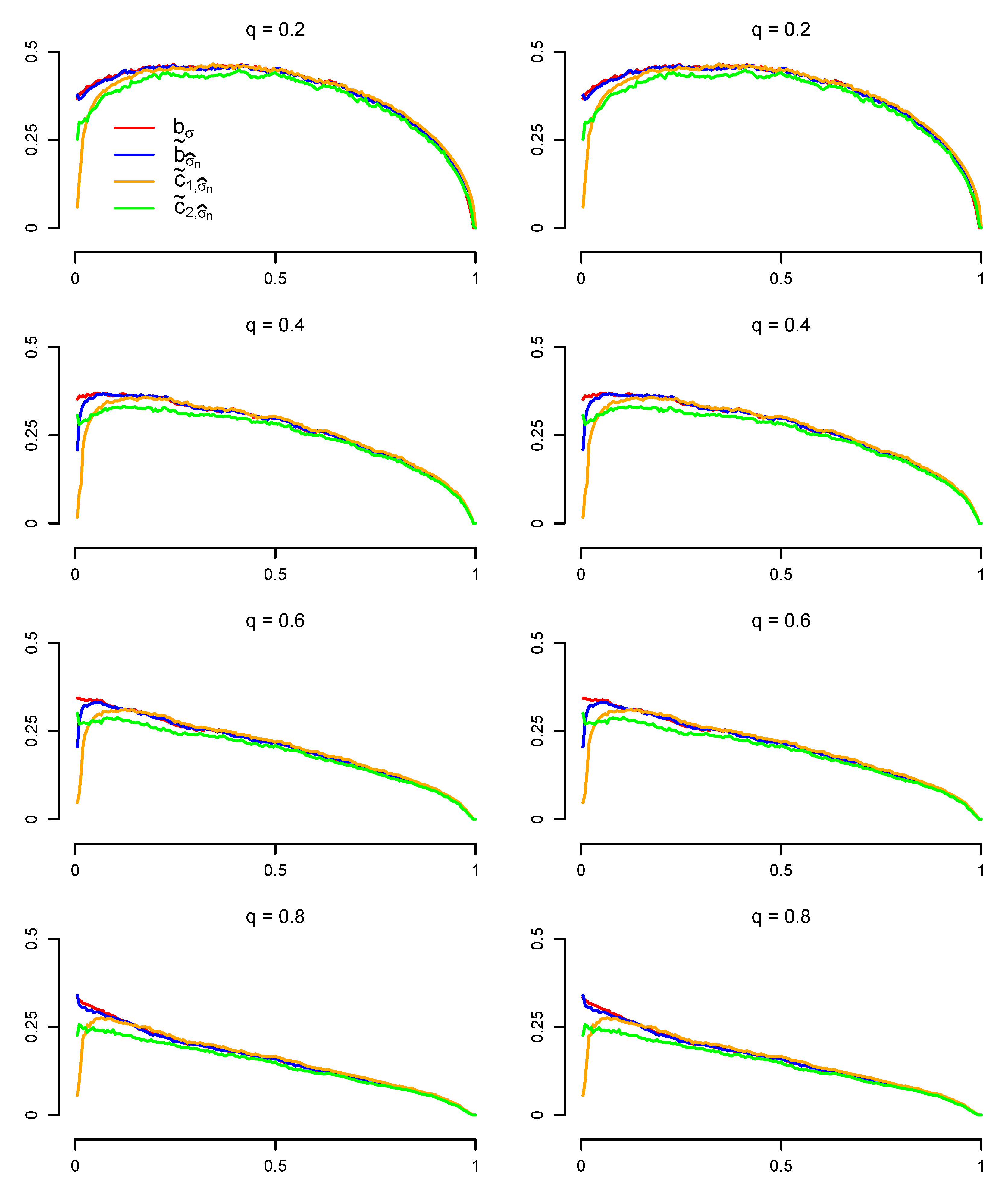

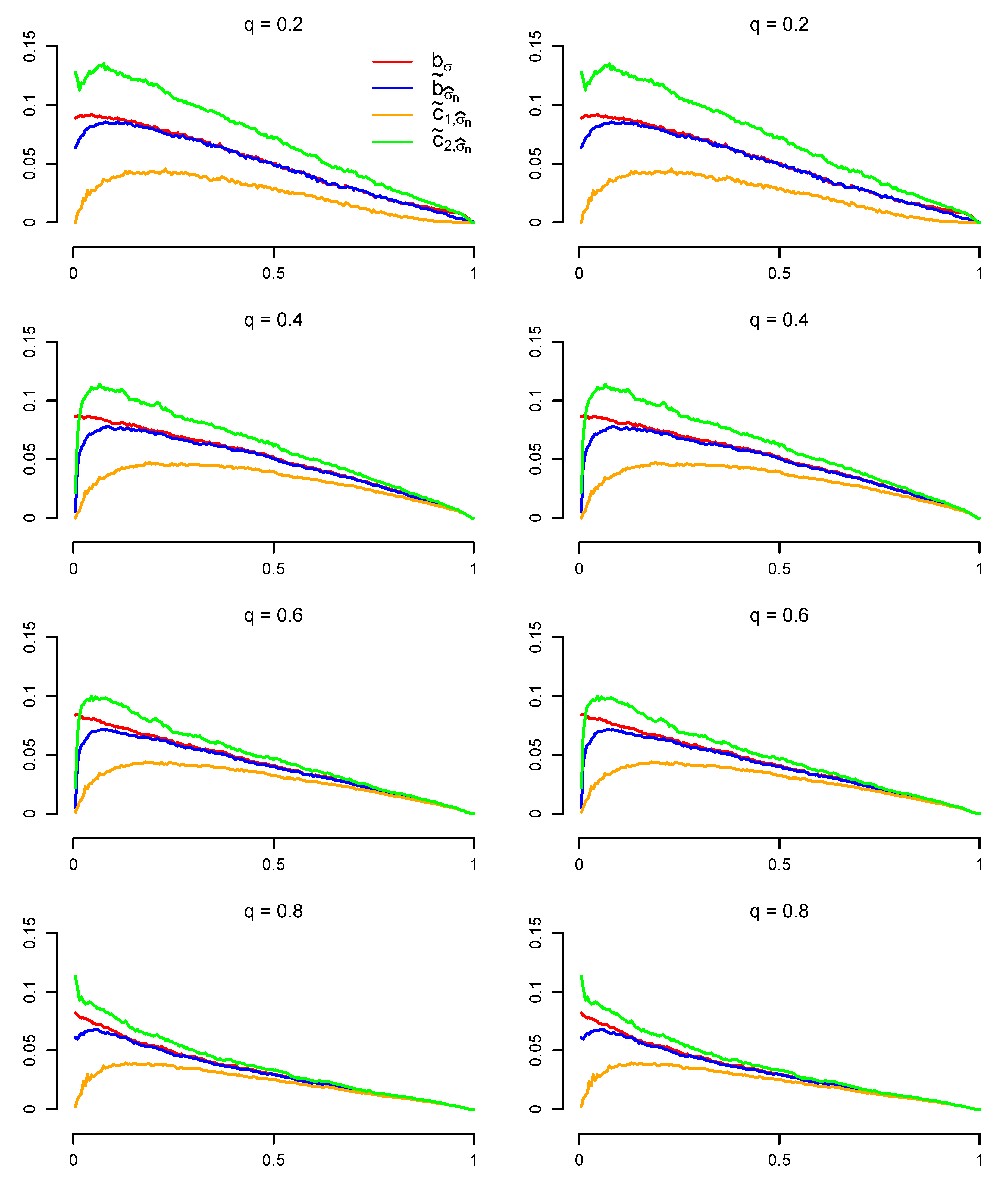

Figure 5 and

Figure 6, respectively.

Figure 5 shows the value functions associated with each stopping rule, the red curve being the one associated with the OSB. An important fact revealed by

Figure 5 is that in both the low and high-frequency scenarios the estimate

behaves almost indistinguishably to

in terms of the mean payoff after just a few initial observations.

Despite the variance payoff not being an optimized criterion in (

3), it is worth knowing how it behaves for the three different stopping strategies, as it represents the risk associated with adopting each stopping rule as an exercise strategy. As expected, for any pair

, a higher stopping boundary implies a smaller payoff variance.

Figure 6 not only reflects this behavior by suggesting the upper confidence curve as the best stopping strategy, but also reveals that the variance does exhibit considerable differences for the stopping rules in the low-frequency scenario. These differences increase when the time gets closer to the initial point

and also when the quantile level

q decreases. In the high-frequency scenario, this effect is alleviated.

Figure 5 and

Figure 6 also reveal that both the mean and the variance of the payoff associated with the estimated boundary

converge to the ones associated with the true boundary as more data are taken to estimate

.

The pragmatic bottom line of the simulation study can be summarized in the following rules-of-thumb: if , it is advised to adopt the upper confidence curve as the stopping rule because has almost the same mean payoff as all the other stopping rules while having considerable less variance; if , the means and the variances of the payoff of the three stopping rules are quite similar, being the most efficient option to just assume without computing the confidence curves.

For , the best candidate for the execution strategy is not obvious, and it would depend on which criterion is chosen to measure the mean-variance trade-off of the three strategies.

5. Pinning-At-The-Strike and Real Data Study

In this section, we compare the performance of the optimal stopping strategy using the Brownian bridge model with a classical approach that uses the geometric Brownian motion [

3]. The latter does not take into account the pinning information of the asset’s price at maturity. We do so by a real data study analyzing various scenarios showing different degrees of intensity of pinning-at-the-strike.

The pinning behavior is more likely to take place among heavily traded options, as shown in [

14,

17]. This is why we consider the options based on Apple and IBM expiring within the span of 11 January–18 September, in particular 8905 options for Apple and 4833 for IBM. We denote by

M the total number of options of each company and, for the

j-th option, we let

be the 5-min tick close price of the underlying stock divided by the strike price

. In order to quantify the strength of the pinning effect, we define the

pinning deviance as

,

. Therefore, under perfect pinning, we should expect

and

.

We perform the following steps in the real data application:

We split each path into two subsets by using a factor . We call historical set to the first values of the prices and future set to the remaining part (including the present value) . Here, while represents the proportion of life time of the option.

We use the historical set to estimate the volatility as described in

Section 4.2.

We compute the risk-free interest rate

as the 52-week treasury bill rate (extracted from [

30]) held by the market when the split of

was done.

We set the drift of the geometric Brownian motion to the risk-free interest rate such that the discounted process is a martingale.

We compute the OSBs using Algorithm 1 for the Brownian bridge model (

9) and use the method exposed in ([

28], p. 12) for the geometric Brownian motion model studied in [

3]. Both numerical approaches are similar, the only subtle difference relies on the Brownian bridge requiring the last part of the integral to be computed as in Algorithm 1, while the geometric Brownian motion needs no special treatment. The OSBs are computed with

(the stock prices were previously normalized by using the strike prices),

(all the maturity dates were standardized to 1), and 201 nodes for the time partitions described in

Section 4.1.

We compute the profit generated by optimally exercising the option within the remaining time by using the future set. This is done by calculating and , where and are the OSTs associated, respectively, to the Brownian bridge and geometric Brownian motion strategies under the initial condition .

We compute the “

-aggregated” cumulative profit, as defined below, to measure the goodness of both models (BB stays for Brownian bridge while GBM stays for geometric Brownian motion):

where

, and

and

are the number of elements in

and

, respectively.

We finally compute the relative mean profit .

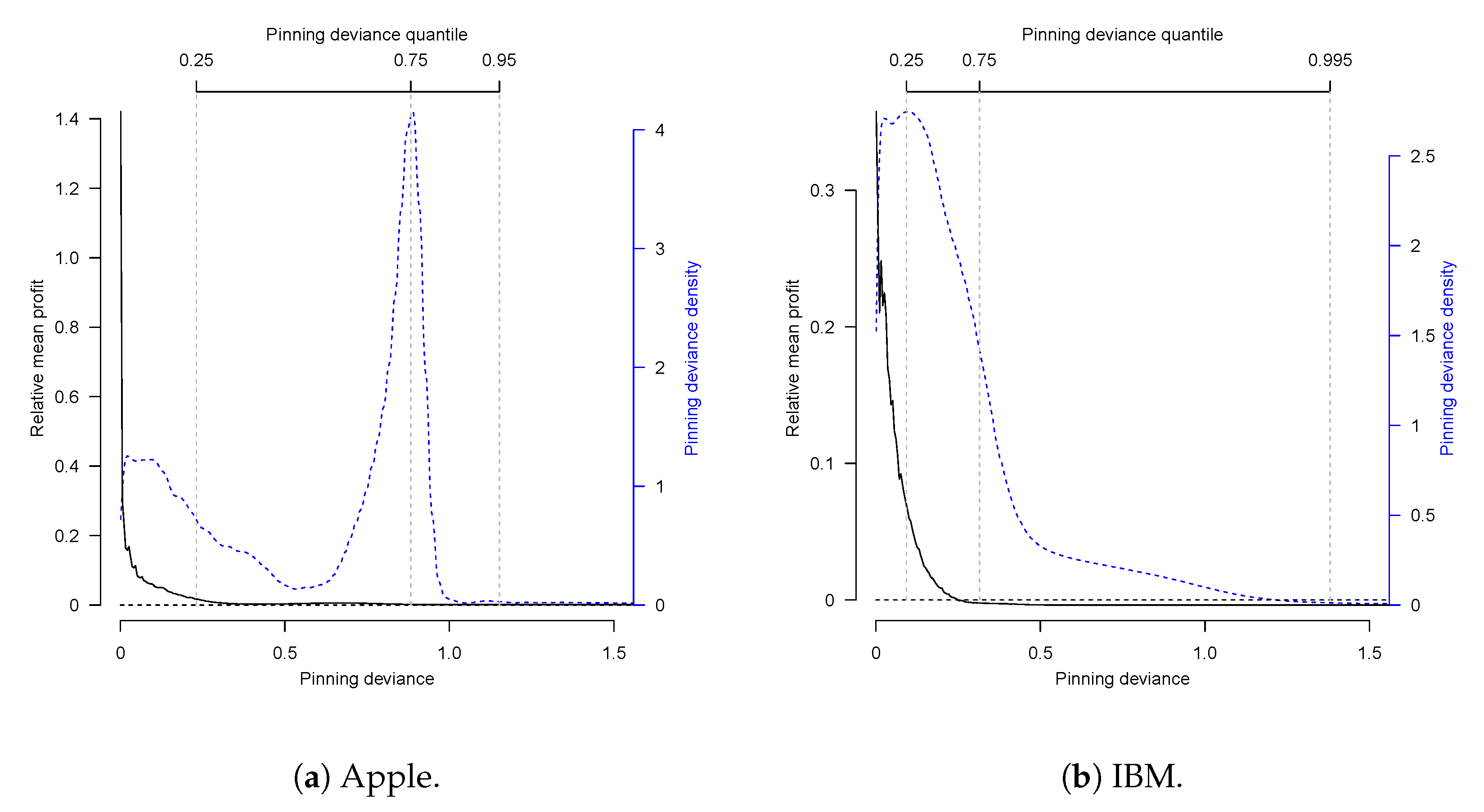

We plot the pinning deviances

p versus the relative mean profit (see

Figure 7).

The Brownian bridge model behaves better than the geometric Brownian motion for options with low pinning deviance. This advantage fades away as we take distance from an ideal pinning-at-the-strike scenario, that is, when the pinning deviance increases. While the Brownian bridge model outperforms the geometric Brownian motion when applied to the Apple options along the whole dataset, when we consider the IBM options, the advantage is only present in of the options with lower pinning deviances.

Remark 3. Besides using the OSB, we also considered in the analysis the confidence curves described in Section 4.3. However, since this is a high-frequency sampling scenario, both confidence curves provided almost indistinguishable results and were omitted to avoid redundancy. Remark 4. We did not consider the prices to buy the options when computing the profits in Figure 7, as we are interested in when it is optimal to exercise the option rather than in whether it is profitable to buy the option held. It is clear that an application of the Brownian bridge model is profitable in the presence of pinning-at-the-strike effect. However, it is far from being trivial to know beforehand if a stock will pin or not. Even if pinning forecasting is not the scope of this paper (for a systematic treatment, we refer to [

15,

16,

18]), we provide some basic evidence about the possibility to predict the appearance of the pinning effect by means of the trading volume of the options associated with a stock. For that, we study the association between the pinning deviances

and the number of open contracts for a given option that we call the

Open Interest (OI). In particular, we compute the

weighted OI for options expiring during the year 2017. Its definition is

, where

is the OI of the

j-th option at day

k after it was opened,

is the total number of days the option remained available, and the weights

,

, place more importance to OIs closer to the maturity date. We highlight that the

is an observable quantity. The Spearman’s rank correlation coefficient between the wOI and the pinning deviances scored

for Apple and

for IBM, thus revealing a significant (

p-values

) positive dependence between

and the pinning strength.

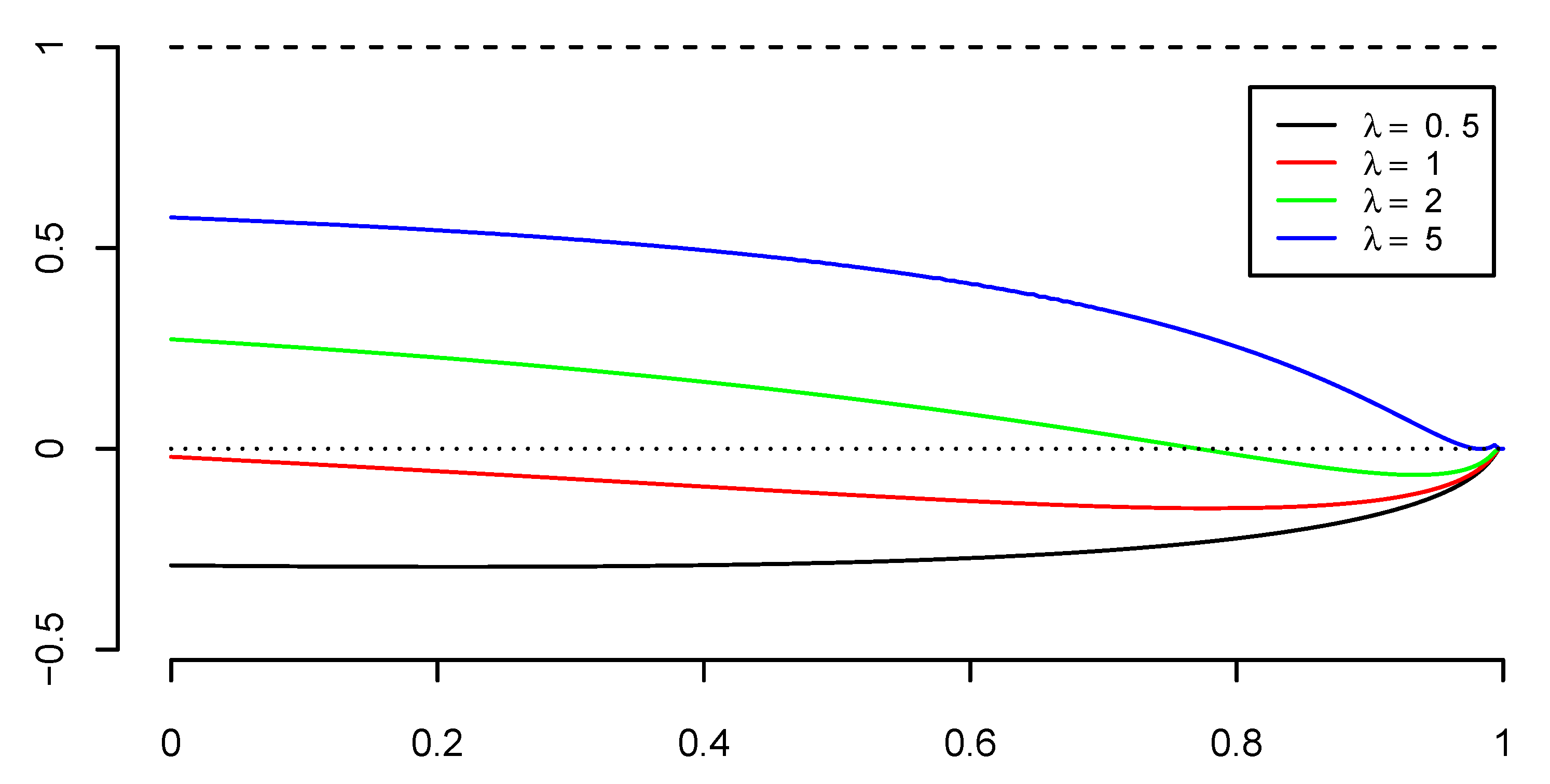

6. Pinning at Any Point

A recurring assumption in our work is that the pinning point coincides with the strike price of the option. We address next on what should be expected when relaxing this assumption.

A pinning point different from the strike prices would be desirable as it would increase the adaptability of the model to fit specific real situations. However, this extra flexibility makes the problem substantially more complex. For instance, the arguments used to state that the OSB is monotone in Proposition 1 do not work anymore. Actually, empirical evidence suggests that this property does not hold anymore. Assuming that all regularity conditions still hold and that is possible to apply the extended version of the Itô’s formula, then following the same arguments of

Section 3 one would obtain the integral equation

where

A and

S are the pinning point and the strike price respectively, and where

Figure 8 shows the optimal stopping boundary numerically obtained from (

20) for different discounting rates, suggesting that the OSB is not monotone.

Without monotonicity, it is much harder to prove other properties like the continuity of the boundary and the smooth fit condition. Some continuity results for the boundary for time homogeneous and non-homogeneous diffusions are proved in [

31,

32], respectively, while [

33] addresses the smooth fit condition for a broad range of cases.

Some works go a step forward and try to solve a similar problem with a random pinning point, but in such cases different kinds of simplifications are required. For example, in [

21], the authors work in a non-discounted scenario with the identity as the gain function and gives bounds for the value function with a general pinning point distribution. Another good example is [

25], where gain functions of class

are considered.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}