The Effect of Business Legal Form on the Perception of COVID-19-Related Disruptions by Households Running a Business

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

2.1. Business Legal Form as a Factor of Vulnerability

- Personal capabilities of a business owner (e.g., Ayala and Manzano 2014; Bullough and Renko 2013; Bullough et al. 2014);

- Organizational characteristics of a venture (e.g., Smallbone et al. 2012);

- Institutional environment (Alinovi et al. 2009; Tan et al. 2020).

2.2. Risk Coping Mechanisms Influencing Households’ Perceptions of Risk

3. Research Design and Method

3.1. Survey Design

3.2. Sample Composition: Businesses Characteristics

3.3. Method

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Kolmogorov–Smirnov | Shapiro–Wilk | |||||

|---|---|---|---|---|---|---|

| Statistic | df | Sig. | Staitistc. | df | Istotność | |

| WORKERS | 0.192 | 538 | 0.000 | 0.917 | 538 | 0.000 |

| COSTS | 0.194 | 538 | 0.000 | 0.905 | 538 | 0.000 |

| PROD_CONT | 0.152 | 538 | 0.000 | 0.920 | 538 | 0.000 |

| SALES_CONT | 0.177 | 538 | 0.000 | 0.905 | 538 | 0.000 |

| SUPPLY CHAIN | 0.189 | 538 | 0.000 | 0.920 | 538 | 0.000 |

| LIQUIDITY | 0.167 | 538 | 0.000 | 0.925 | 538 | 0.000 |

| BANK LOANS | 0.168 | 538 | 0.000 | 0.936 | 538 | 0.000 |

| SURVIVAL | 0.193 | 538 | 0.000 | 0.929 | 538 | 0.000 |

| COVID-19 Interruptions | Legal Form of Business | Strongly Disagree | Disagree | Somewhat Disagree | Neither Agree Nor Disagree | Somewhat Agree | Agree | Strongly Agree | In Total |

|---|---|---|---|---|---|---|---|---|---|

| WORKERS | SP | 11 | 22 | 35 | 27 | 52 | 22 | 26 | 195 |

| LLC | 11 | 49 | 43 | 8 | 56 | 82 | 17 | 266 | |

| GP | 3 | 16 | 17 | 7 | 13 | 15 | 6 | 77 | |

| In total | 25 | 87 | 95 | 42 | 121 | 119 | 49 | 538 | |

| COSTS | SP | 3 | 15 | 27 | 9 | 42 | 47 | 52 | 195 |

| LLC | 0 | 41 | 53 | 21 | 69 | 59 | 23 | 266 | |

| GP | 3 | 9 | 15 | 5 | 16 | 23 | 6 | 77 | |

| In total | 6 | 65 | 95 | 35 | 127 | 129 | 81 | 538 | |

| PROD_CONT | SP | 37 | 21 | 28 | 28 | 31 | 24 | 26 | 195 |

| LLC | 14 | 60 | 50 | 24 | 48 | 56 | 14 | 266 | |

| GP | 11 | 22 | 12 | 2 | 11 | 11 | 8 | 77 | |

| In total | 62 | 103 | 90 | 54 | 90 | 91 | 48 | 538 | |

| SALES_CONT | SP | 11 | 16 | 23 | 14 | 41 | 37 | 53 | 195 |

| LLC | 3 | 47 | 60 | 19 | 42 | 63 | 32 | 266 | |

| GP | 2 | 10 | 12 | 9 | 13 | 18 | 13 | 77 | |

| In total | 16 | 73 | 95 | 42 | 96 | 118 | 98 | 538 | |

| SUPPLY CHAIN | SP | 8 | 16 | 37 | 23 | 46 | 31 | 34 | 195 |

| LLC | 2 | 38 | 72 | 15 | 58 | 53 | 28 | 266 | |

| GP | 3 | 11 | 24 | 5 | 9 | 21 | 4 | 77 | |

| In total | 13 | 65 | 133 | 43 | 113 | 105 | 66 | 538 | |

| LIQUIDITY | SP | 5 | 13 | 35 | 24 | 30 | 34 | 54 | 195 |

| LLC | 6 | 60 | 59 | 35 | 56 | 35 | 15 | 266 | |

| GP | 2 | 9 | 21 | 11 | 15 | 14 | 5 | 77 | |

| In total | 13 | 82 | 115 | 70 | 101 | 83 | 74 | 538 | |

| BANK LOANS | SP | 6 | 21 | 23 | 82 | 29 | 22 | 12 | 195 |

| LLC | 7 | 72 | 70 | 64 | 33 | 13 | 7 | 266 | |

| GP | 3 | 16 | 13 | 28 | 12 | 5 | 0 | 77 | |

| In total | 16 | 109 | 106 | 174 | 74 | 40 | 19 | 538 | |

| SURVIVAL | SP | 6 | 15 | 39 | 22 | 44 | 36 | 33 | 195 |

| LLC | 4 | 58 | 83 | 38 | 42 | 30 | 11 | 266 | |

| GP | 4 | 14 | 19 | 10 | 19 | 9 | 2 | 77 | |

| In total | 14 | 87 | 141 | 70 | 105 | 75 | 46 | 538 |

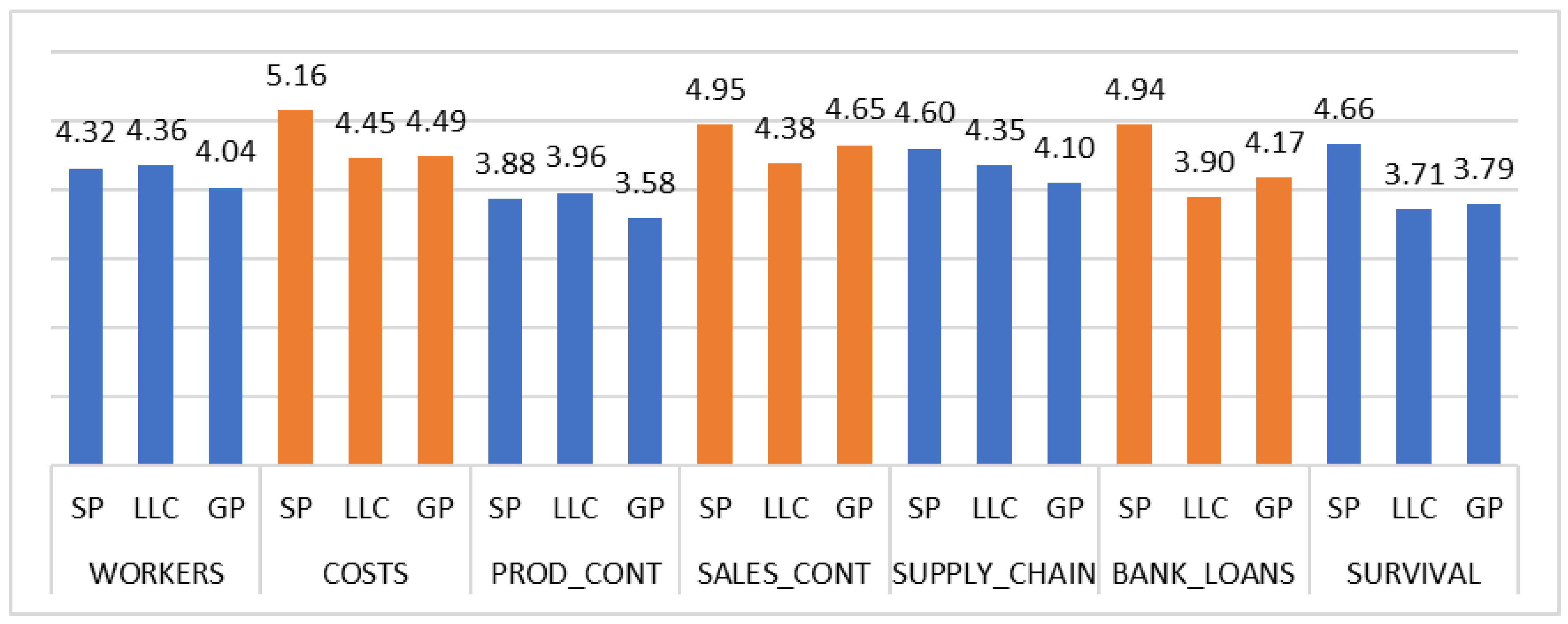

| SP | LCC | GP | ||||

|---|---|---|---|---|---|---|

| Mean | St.Dev. | Mean | St.Dev. | Mean | St.Dev. | |

| WORKERS | 4.318 | 1.724 | 4.365 | 1.780 | 4.039 | 1.758 |

| COSTS | 5.159 | 1.684 | 4.455 | 1.595 | 4.494 | 1.706 |

| PROD_CONT | 3.877 | 2.035 | 3.962 | 1.752 | 3.584 | 2.028 |

| SALES_CONT | 4.954 | 1.865 | 4.380 | 1.758 | 4.649 | 1.775 |

| SUPPLY CHAIN | 4.600 | 1.727 | 4.353 | 1.661 | 4.104 | 1.714 |

| LIQUIDITY | 4.944 | 1.774 | 3.902 | 1.604 | 4.169 | 1.576 |

| BANK LOANS | 4.133 | 1.404 | 3.417 | 1.344 | 3.584 | 1.271 |

| SURVIVAL | 4.656 | 1.690 | 3.714 | 1.492 | 3.792 | 1.542 |

References

- Abeler, Johannes, Armin Falk, Lorenz Goette, and David Huffman. 2011. Reference points and effort provision. American Economic Review 101: 470–92. [Google Scholar] [CrossRef] [Green Version]

- Agarwal, Reena, and Andrew W. Horowitz. 2002. Are international remittances altruism or insurance? Evidence from Guyana using multiple-migrant households. World Development 30: 2033–44. [Google Scholar] [CrossRef]

- Albacete, Nicolas, Pirmin Fessler, Fabian Kalleitner, and Peter Lindner. 2021. How has COVID-19 affected the financial situation of households in Austria? Monetary Policy and the Economy Q 4: 111–30. [Google Scholar]

- Alderman, Harold, Pierre-Andre Chiappori, Lawrence Haddad, John Hoddinott, and Ravi Kanbur. 1995. Unitary versus collective models of the household: Is it time to shift the burden of proof? The World Bank Research Observer 10: 1–19. [Google Scholar] [CrossRef]

- Alinovi, Luca, Erdgin Mane, and Donato Romano. 2009. Measuring Household Resilience to Food Insecurity: Application to Palestinian Households. Rome: EC-FAO Food Security Programme Rom, pp. 1–39. [Google Scholar]

- Armantier, Oliver, Gizem Koşar, Rachel Pomerantz, Daphne Skandalis, Kyle Smith, Giorgio Topa, and Wilbert Van der Klaauw. 2020. Coronavirus Outbreak Sends Consumer Expectations Plummeting. (No. 20200406b). New York: Federal Reserve Bank of New York. [Google Scholar]

- Armstrong, Richard A., and Anthony C. Hilton. 2011. Statistical Analysis in Microbiology: Statnotes. Hoboken: Wiley-Blackwell. [Google Scholar]

- Asdrubali, Pierfederico, Simone Tedeschi, and Luigi Ventura. 2020. Household risk-sharing channels. Quantitative Economics 11: 1109–42. [Google Scholar] [CrossRef]

- Attanasio, Orazio, Abigail Barr, Juan Camilo Cardenas, Garance Genicot, and Costas Meghir. 2012. Risk pooling, risk preferences, and social networks. American Economic Journal: Applied Economics 4: 134–67. [Google Scholar] [CrossRef] [Green Version]

- Ayala, Juan-Carlos, and Guadalupe Manzano. 2014. The resilience of the entrepreneur. Influence on the success of the business. A longitudinal analysis. Journal of Economic Psychology 42: 126–35. [Google Scholar] [CrossRef]

- Baker, Scott R., Robert A. Farrokhnia, Steffen Meyer, Michaela Pagel, and Constantine Yannelis. 2020. How does household spending respond to an epidemic? Consumption during the 2020 COVID-19 pandemic. The Review of Asset Pricing Studies 10: 834–62. [Google Scholar] [CrossRef]

- Barrafrem, Kinga, Daniel Västfjäll, and Gustav Tinghög. 2020. Financial well-being, COVID-19, and the financial better-than-average-effect. Journal of Behavioral and Experimental Finance 28: 100410. [Google Scholar] [CrossRef]

- Becker, Gary. 1965. A theory of the allocation of time. Economic Journal 75: 493–517. [Google Scholar] [CrossRef] [Green Version]

- Block, Joen H., Christian Fisch, and Mirko Hirschmann. 2021. The determinants of bootstrap financing in crises: Evidence from entrepreneurial ventures in the COVID-19 pandemic. Small Business Economics 58: 867–85. [Google Scholar] [CrossRef]

- Bourlès, Renaud, Yann Bramoullé, and Eduardo Perez-Richet. 2021. Altruism and risk sharing in networks. Journal of the European Economic Association 19: 1488–521. [Google Scholar] [CrossRef]

- Brewer, Mike, and Laura Gardiner. 2020. The initial impact of COVID-19 and policy responses on household incomes. Oxford Review of Economic Policy 36: S187–99. [Google Scholar] [CrossRef]

- Bullough, Amanda, and Maija Renko. 2013. Entrepreneurial resilience during challenging times. Business Horizons 56: 343–50. [Google Scholar] [CrossRef]

- Bullough, Amanda, Maija Renko, and Tamara Myatt. 2014. Danger zone entrepreneurs: The importance of resilience anmandad self–efficacy for entrepreneurial intentions. Entrepreneurship Theory and Practice 38: 473–99. [Google Scholar] [CrossRef]

- Burchardi, Konrad B., and Tarek A. Hassan. 2013. The economic impact of social ties: Evidence from German reunification. The Quarterly Journal of Economics 128: 1219–71. [Google Scholar] [CrossRef] [Green Version]

- Cacciotti, Gabriella, James C. Hayton, J. Robert Mitchell, and Andres Giazitzoglu. 2016. A reconceptualization of fear of failure in entrepreneurship. Journal of Business Venturing 31: 302–25. [Google Scholar] [CrossRef] [Green Version]

- Carlson, Stacy, Ms Era Dabla-Norris, Mika Saito, and Yu Shi. 2015. Household Financial Access and Risk Sharing in Nigeria. Washington, DC: International Monetary Fund. [Google Scholar]

- Carter, Craig R., Lisa M. Ellram, and Wendy Tate. 2007. The use of social network analysis in logistics research. Journal of Business Logistics 28: 137–68. [Google Scholar] [CrossRef]

- Chiappori, Pierre-Andre A., and Arthur Lewbel. 2015. Gary Becker’s a theory of the allocation of time. The Economic Journal 125: 410–42. [Google Scholar] [CrossRef] [Green Version]

- Chronopoulos, Dimitris K., Marcel Lukas, and John O. Wilson. 2020. Consumer Spending Responses to the COVID-19 Pandemic: An Assessment of Great Britain. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3586723 (accessed on 10 December 2021).

- Corbet, Shaen, Yang Hou, Yang Hu, and Les Oxley. 2020. The influence of the COVID-19 pandemic on asset-price discovery: Testing the case of Chinese informational asymmetry. International Review of Financial Analysis 72: 101560. [Google Scholar] [CrossRef]

- Crawford, Vincent P., and Juanjuan Meng. 2011. New York city cab drivers’ labor supply revisited: Reference-dependent preferences with rational-expectations targets for hours and income. American Economic Review 101: 1912–32. [Google Scholar] [CrossRef] [Green Version]

- Davis, H. James, Kameda Tatsuya, and Stasson Mark. 1992. Group Risk Taking: Selected Topics. In Risk-Taking Behavior. Edited by Frank Yates. Chichester: Wiley, pp. 163–99. [Google Scholar]

- Deloitte. 2020. Deloitte Global Cost and Enterprise Transformation Survey. Available online: https://www2.deloitte.com/us/en/pages/about-deloitte/articles/press-releases/deloitte-covid-19-survey-shifts-cost-strategies.html (accessed on 5 October 2020).

- De Weerdt, Joachim, and Stefan Dercon. 2006. Risk-sharing networks and insurance against illness. Journal of Development Economics 81: 337–56. [Google Scholar] [CrossRef] [Green Version]

- Demertzis, Maria, Marta Domínguez-Jiménez, and Annamaria Lusardi. 2020. The Financial Fragility of European Households in the Time of COVID-19. Brussels: Bruegel. [Google Scholar]

- Dierkes, Maik, Carsten Erner, Thomas Langer, and Lars Norden. 2013. Business credit information sharing and default risk of private firms. Journal of Banking and Finance 37: 2867–78. [Google Scholar] [CrossRef]

- Dost, Florian, Ulrike Phieler, Michael Haenlein, and Barak Libai. 2019. Seeding as part of the marketing mix: Word-of-mouth program interactions for fast-moving consumer goods. Journal of Marketing 83: 62–81. [Google Scholar] [CrossRef]

- European Commission. 2019. 219 SBA Fact Sheet Poland. Available online: https://ec.europa.eu/docsroom/documents/38662/attachments/22/translations/en/renditions/native (accessed on 1 July 2021).

- Evans, Alison. 1991. Evans, Alison. 1991. Gender issues in rural household economics. ids Bulletin 22: 51–59. [Google Scholar] [CrossRef] [Green Version]

- Fafchamps, Marcel, and Susan Lund. 2003. Risk-sharing networks in rural Philippines. Journal of Development Economics 71: 261–87. [Google Scholar]

- Fafchamps, Marcel. 2011. Risk Sharing between Households. Handbook of Social Economics 1: 1255–79. [Google Scholar]

- Gertler, Paul, and Jonathan Gruber. 2002. Insuring consumption against illness. American Economic Review 92: 51–70. [Google Scholar]

- Guerini, Mattia, Nesta Lionel, Xavier Ragot, and Stefano Schiavo. 2020. Firm liquidity and solvency under the Covid-19 lockdown in France. OFCE Policy Brief 76: 1–20. [Google Scholar]

- GUS. 2021a. Information Regarding the Labour Market in the Second Quarter of 2021. Warsaw: GUS. [Google Scholar]

- GUS. 2021b. Informacja o Podmiotach Gospodarki Narodowej Wpisanych do Rejestru REGON-Styczeń 2021. Warsaw: GUS. [Google Scholar]

- Haan, Peter, and Prowse Victoria. 2017. Optimal Social Assistance and Umemployment Insurance in a Life-Cycle Model of Family Labor Supply and Savings. In Purdue University Economics Working Papers 1294. West Lafayette: Department of Economics, Purdue University. [Google Scholar]

- Hallegatte, Stephane. 2014. Economic resilience: Definition and measurement. In World Bank Policy Research Working Paper (6852). Washington, DC: World Bank. [Google Scholar]

- Hanspal, Tobin, Annika Weber, and Johannes Wohlfart. 2020a. Exposure to the COVID-19 stock market crash and its effect on household expectations. The Review of Economics and Statistics 103: 994–1010. [Google Scholar]

- Hanspal, Tobin, Annika Weber, and Johannes Wohlfart. 2020b. Income and Wealth Shocks and Expectations during the COVID-19 Pandemic. (No. 8244). CESifo Working Paper. Munich: Center for Economic Studies and ifo Institute (CESifo). [Google Scholar]

- Harhoff, Dietmar, Konrad Stahl, and Michael Woywode. 1998. Legal form, growth and exit of West German firms—empirical results for manufacturing, construction, trade and service industries. The Journal of Industrial Economics 46: 453–88. [Google Scholar] [CrossRef]

- Van Hecke, Tanja. 2012. Power study of anova versus Kruskal-Wallis test. Journal of Statistics and Management Systems 15: 241–47. [Google Scholar] [CrossRef]

- Horvath, Akos, Benjamin S. Kay, and Carlo Wix. 2021. The COVID-19 Shock and Consumer Credit: Evidence from Credit Card Data. Available at SSRN 3613408. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3613408 (accessed on 15 November 2021).

- Hurst, Erik, and Annamaria Lusardi. 2004. Liquidity constraints, household wealth, and entrepreneurship. Journal of Political Economy 112: 319–47. [Google Scholar] [CrossRef] [Green Version]

- Jack, William, and Tawneet Suri. 2014. Risk sharing and transactions costs: Evidence from Kenya’s mobile money revolution. American Economic Review 104: 183–223. [Google Scholar] [CrossRef]

- Kansiime, Monika K., Justice A. Tambo, Idah Mugambi, Mary Bundi, Augustine Kara, and Charles Owuor. 2021. COVID-19 implications on household income and food security in Kenya and Uganda: Findings from a rapid assessment. World Development 137: 105199. [Google Scholar] [CrossRef]

- Kay, Benjamin S. 2021. The COVID-19 Shock and Consumer Credit: Evidence from Credit Card Data; (No. 2021-008). Washington, DC: Board of Governors of the Federal Reserve System (US).

- Korosteleva, Julia, and Paulina Stępień-Baig. 2020. Climbing the poverty ladder: The role of entrepreneurship and gender in alleviating poverty in transition economies. Entrepreneurship and Regional Development 32: 197–220. [Google Scholar] [CrossRef]

- Kozubíková, Ludmila, Jaroslav Belás, Yuriy Bilan, and Premysl Bartoš. 2015. Personal characteristics of entrepreneurs in the context of perception and management of business risk in the SME segment. Economics and Sociology 8: 41–54. [Google Scholar] [CrossRef]

- Krueger, Dirk. 1999. Risk Sharing in Economies with Incomplete Markets. Ph.D. thesis, University of Minnesota, Minneapolis, MS, USA. [Google Scholar]

- Krukowski, Kipp A., and Dawn R. DeTienne. 2021. Selling a business after the pandemic? Crisis and information asymmetry impact on deal terms. Business Horizons, in press. [Google Scholar]

- Łasak, Piotr. 2020. Wyzwania dla polskiego sektora bankowego jako skutek pandemii COVID-19. In Polityka Gospodarcza w Niestabilnym Otoczeniu–Dylematy i Wyzwania. Toruń: Wyższa Szkoła Kultury Społecznej i Medialnej, pp. 80–93. [Google Scholar]

- Lee, Soon J., Soon I. Kwon, and Seok Y. Chung. 2010. Determinants of household demand for insurance: The case of Korea. The Geneva Papers on Risk and Insurance-Issues and Practice 35: S82–S91. [Google Scholar] [CrossRef] [Green Version]

- Li, Jie, Quanlun Song, Changyan Peng, and Yu Wu. 2020. COVID-19 pandemic and household liquidity constraints: Evidence from micro data. Emerging Markets Finance and Trade 56: 3626–34. [Google Scholar] [CrossRef]

- Lin, Mingfeng, Nagpurnanand R. Prabhala, and Siva Viswanathan. 2009. Can Social Networks Help Mitigate Information Asymmetry in Online Markets? ICIS 2009 Proceedings. p. 202. Available online: https://aisel.aisnet.org/icis2009/202 (accessed on 20 November 2021).

- Mankart, Jochen, and Rigas Oikonomou. 2017. Household search and the aggregate labour market. The Review of Economic Studies 84: 1735–88. [Google Scholar] [CrossRef]

- Marsh, Dorota, and Pete Thomas. 2017. The Governance of Welfare and the Expropriation of the Common: Polish Tales of Entrepreneurship. In Critical Perspectives on Entrepreneurship. London: Routledge, pp. 225–44. [Google Scholar]

- Martin, Amory, Maryia Markhvida, Stéphane Hallegatte, and Brian Walsh. 2020. Socio-economic impacts of COVID-19 on household consumption and poverty. Economics of Disasters And Climate Change 4: 453–79. [Google Scholar] [CrossRef]

- Midões, Catarina, and Mateo Seré. 2021. Living with Reduced Income: An Analysis of Household Financial Vulnerability under COVID-19. Social Indicators Research 8: 1–25. [Google Scholar] [CrossRef]

- Ministerstwo Rozwoju. 2020. Podstawowe Wskaźniki Makroekonomiczne, Polska, Wrzesień 2020. Available online: https://www.gov.pl/attachment/bc0e9744-1fdf-475c-a137-d141df473769 (accessed on 1 July 2021).

- Munshi, Kaivan. 2003. Networks in the modern economy: Mexican migrants in the US labor market. The Quarterly Journal of Economics 118: 549–99. [Google Scholar] [CrossRef] [Green Version]

- Neumeyer, Xaver, and Susana C. Santos. 2018. Sustainable business models, venture typologies, and entrepreneurial ecosystems: A social network perspective. Journal of Cleaner Production 172: 4565–79. [Google Scholar] [CrossRef]

- Paci, Pirella, Marcin J. Sasin, and Jos Verbeek. 2004. Economic growth, income distribution, and poverty in Poland during transition. In Policy Research Working Paper. No. 3467. Washington, DC: World Bank. [Google Scholar]

- PwC. 2020. PwC Global COVID-19 CFO Pulse Report. June. Available online: https://www.pwc.com/gx/en/issues/crisis-solutions/covid-19/global-cfo-pulse.html (accessed on 2 October 2020).

- Rowland, Zuzana, Veronika Machova, Jakub Horak, and Jan Hejda. 2019. Determining the market value of the enterprise using the modified method of capitalized net incomes and Metfessel allocation of input data. AD ALTA: Journal of Interdisciplinary Research 9: 305–10. [Google Scholar]

- Schneider, Daniel, Peter Tufano, and Annamaria Lusardi. 2020. Household Financial Fragility during COVID-19: Rising Inequality and Unemployment Insurance Benefit Reductions. GFLEC WP, 4. Available online: https://www.sbs.ox.ac.uk/sites/default/files/2020-10/finfrag_workingpaper_103020%20%281%29.pdf (accessed on 18 December 2021).

- Shen, Huayu, Mengyao Fu, Hongyu Pan, Zhongfu Yu, and Yongquan Chen. 2020. The impact of the COVID-19 pandemic on firm performance. Emerging Markets Finance and Trade 56: 2213–30. [Google Scholar] [CrossRef]

- Smallbone, David, David Deakins, and Martina Battisti. 2012. Small business responses to a major economic downturn: Empirical perspectives from New Zealand and the United Kingdom. International Small Business Journal 30: 754–77. [Google Scholar] [CrossRef]

- Smith, Lisa C., and Timothy R. Frankenberger. 2018. Does resilience capacity reduce the negative impact of shocks on household food security? Evidence from the 2014 floods in Northern Bangladesh. World Development 102: 358–76. [Google Scholar] [CrossRef]

- Tan, Jin, Li Peng, and Shili Guo. 2020. Measuring Household Resilience in Hazard-Prone Mountain Areas: A Capacity-Based Approach. Social Indicators Research 152: 1153–76. [Google Scholar] [CrossRef]

- Tchamyou, Vanessa S. 2019. The role of information sharing in modulating the effect of financial access on inequality. Journal of African Business 20: 317–38. [Google Scholar] [CrossRef] [Green Version]

- Thomas, Duncan. 1990. Intra-household resource allocation: An inferential approach. Journal of Human Resources 25: 635–64. [Google Scholar] [CrossRef]

- TMF Group. 2021. Global Business Complexity Index 2021. Available online: https://www.tmf-group.com/en/news-insights/publications/2021/global-business-complexity-index/ (accessed on 20 November 2021).

- Wang, Haomin. 2019. Intra-household risk sharing and job search over the business cycle. Review of Economic Dynamics 34: 165–82. [Google Scholar] [CrossRef] [Green Version]

- Winnicka-Popczyk, Alicja. 2014. Finansowe uwarunkowania wyboru formy prawnej biznesu w firmach rodzinnych. Przedsiębiorczość i Zarządzanie 15: 249–59. [Google Scholar]

- Yang, Dean, and Hwajung Choi. 2007. Are remittances insurance? Evidence from rainfall shocks in the Philippines. The World Bank Economic Review 21: 219–48. [Google Scholar] [CrossRef]

- Yue, Pengpeng, Aslihang G. Korkmaz, Zhichao Yin, and Haigang Zhou. 2021. Household-owned Businesses’ Vulnerability to the COVID-19 Pandemic. Emerging Markets Finance and Trade 57: 1662–74. [Google Scholar] [CrossRef]

- Yue, Pengpeng, Aslihang Gizem Korkmaz, and Haigang Zhou. 2020. Household financial decision making amidst the COVID-19 pandemic. Emerging Markets Finance and Trade 56: 2363–77. [Google Scholar] [CrossRef]

- Zhang, Huanhuan, Gang Kou, and Yi Peng. 2019. Soft consensus cost models for group decision making and economic interpretations. European Journal of Operational Research 277: 964–80. [Google Scholar] [CrossRef]

| Level of Analysis | Variables | Question |

|---|---|---|

| Did the COVID-19 Pandemic Result in Difficulties in the Following Aspects of Firm’s Performance: | ||

| Operating risk factors | WORKERS | limited accessibility of workers |

| COSTS | additional costs of the implementation of required safety measures | |

| PROD_CONT | inability to continue production | |

| SALES_CONT | inability to continue sales | |

| SUPPLY CHAIN | delayed delivery of production components/materials etc., or produced goods to the customers | |

| Financial risk factors | LIQUIDITY | worsening of financial liquidity |

| BANK LOANS | limited accessibility of bank loans | |

| SURVIVAL | the overall impact of COVID-19 threatened the survival of our company |

| Variable | N | % | |

|---|---|---|---|

| OWN_2 (owners’ responsibility, three categories) | |||

| LLC | limited, perform as limited liability companies | 195 | 36.2 |

| SP | unlimited, perform as sole proprietorship | 266 | 49.4 |

| GP | unlimited, perform as general partnerships | 77 | 14.3 |

| total | 538 | 100 | |

| SIZE (by the number of employees) | |||

| micro | up to 9 persons | 182 | 33.8 |

| small | 10–49 persons | 208 | 38.7 |

| medium | 50–249 persons | 148 | 27.5 |

| total | 538 | 100 | |

| AGE_1 (by the years of performance, four categories of business’ age) | |||

| infant | (up to 5 years) | 86 | 16.0 |

| young | (6–10 years) | 137 | 25.5 |

| intermediate | (11–20 years) | 187 | 34.8 |

| mature | (21 years or more) | 128 | 23.8 |

| total | 538 | 100 | |

| WORK | COSTS | PROD _CONT | SALES _CONT | SUPPLY CHAIN | LIQUIDITY | BANK LOANS | SURVIVAL | |

|---|---|---|---|---|---|---|---|---|

| Chi-squared statistic | 52.375 *** | 48.685 *** | 55.344 *** | 41.794 *** | 35.558 *** | 68.974 *** | 53.349 *** | 57.328 *** |

| Phi | 0.312 *** | 0.301 *** | 0.321 *** | 0.279 *** | 0.257 *** | 0.358 *** | 0.315 *** | 0.326 *** |

| Cramer’s V | 0.221 *** | 0.213 *** | 0.227 *** | 0.197 *** | 0.182 *** | 0.253 *** | 0.223 *** | 0.231 *** |

| Contingency ratio | 0.298 *** | 0.288 *** | 0.305 *** | 0.268 *** | 0.249 *** | 0.337 *** | 0.300 *** | 0.310 *** |

| Variables | WORK | COSTS | PROD _CONT | SALES _CONT | SUPPLY CHAIN | LIQUIDITY | BANK LOANS | SURVIVAL |

|---|---|---|---|---|---|---|---|---|

| Kruskal–Wallis statistics | 2.224 | 24.623 *** | 2.646 | 12.629 ** | 5.137 | 41.779 *** | 32.177 *** | 39.205 *** |

| pair-vise comparisons | ||||||||

| LLC-GP | −7.866 | −23.017 | −24.993 | −26.159 | −9.715 | |||

| LLC-SP | 69.405 *** | 51.261 *** | 92.732 *** | 81.334 *** | 87.661 *** | |||

| GP-SP | 61.539 ** | 28.244 | 67.738 ** | 55.175 ** | 77.945 *** |

| Legal Form of Business | COSTS | SALES _CONT | LIQUIDITY | BANK LOANS | SURVIVAL |

|---|---|---|---|---|---|

| SP | 312.62 | 298.89 | 325.04 | 317.61 | 324.00 |

| LLC | 243.22 | 247.63 | 232.31 | 236.28 | 236.34 |

| GP | 251.08 | 270.64 | 257.31 | 262.44 | 246.05 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Doś, A.; Wieczorek-Kosmala, M.; Błach, J. The Effect of Business Legal Form on the Perception of COVID-19-Related Disruptions by Households Running a Business. Risks 2022, 10, 82. https://doi.org/10.3390/risks10040082

Doś A, Wieczorek-Kosmala M, Błach J. The Effect of Business Legal Form on the Perception of COVID-19-Related Disruptions by Households Running a Business. Risks. 2022; 10(4):82. https://doi.org/10.3390/risks10040082

Chicago/Turabian StyleDoś, Anna, Monika Wieczorek-Kosmala, and Joanna Błach. 2022. "The Effect of Business Legal Form on the Perception of COVID-19-Related Disruptions by Households Running a Business" Risks 10, no. 4: 82. https://doi.org/10.3390/risks10040082

APA StyleDoś, A., Wieczorek-Kosmala, M., & Błach, J. (2022). The Effect of Business Legal Form on the Perception of COVID-19-Related Disruptions by Households Running a Business. Risks, 10(4), 82. https://doi.org/10.3390/risks10040082