What We Know about Research on Life Insurance Lapse: A Bibliometric Analysis

Abstract

:1. Introduction

2. Life Insurance Lapsation

3. Materials and Methods

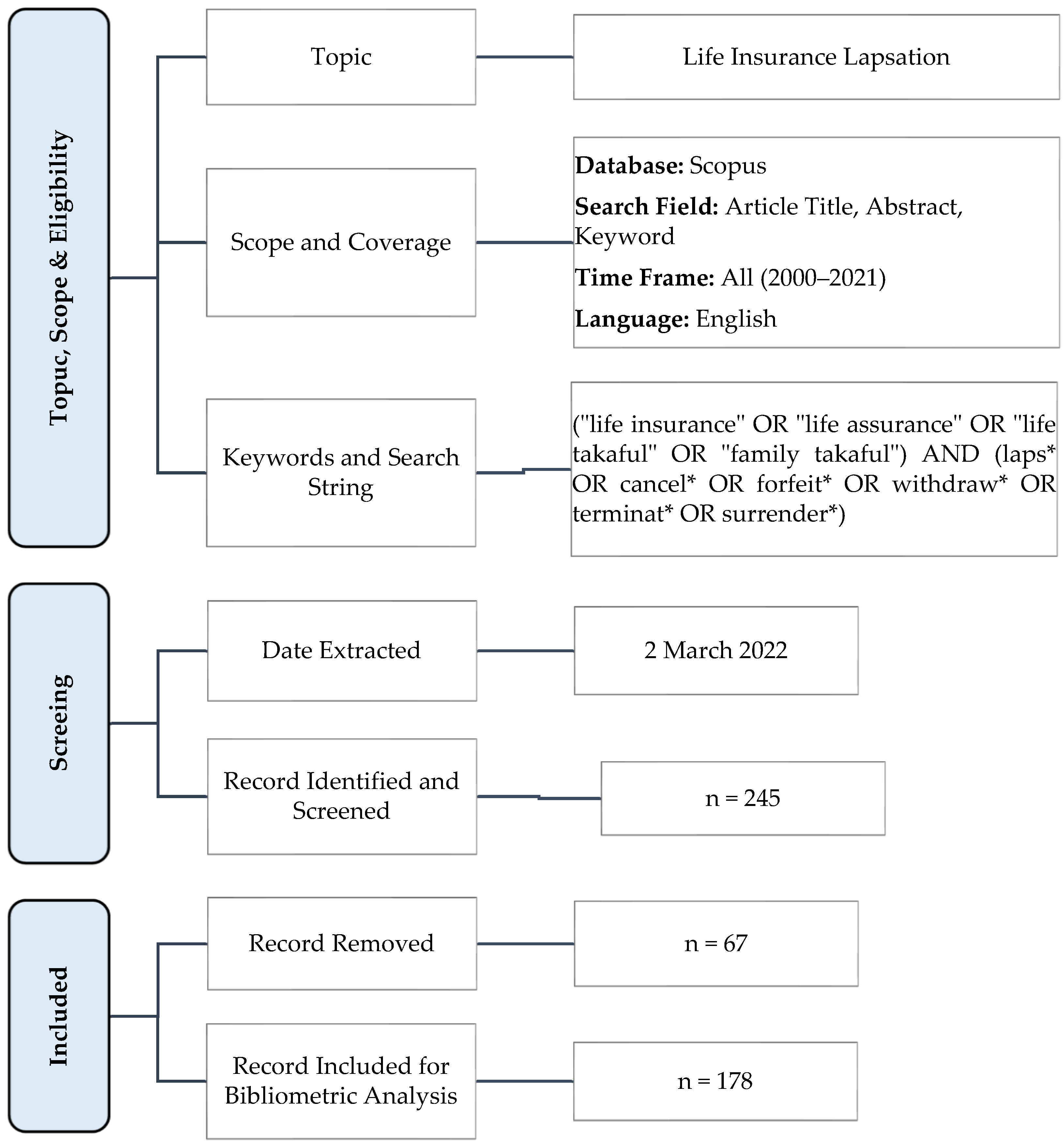

3.1. Bibliometric Analysis

3.2. Data Collection

4. Results and Discussion

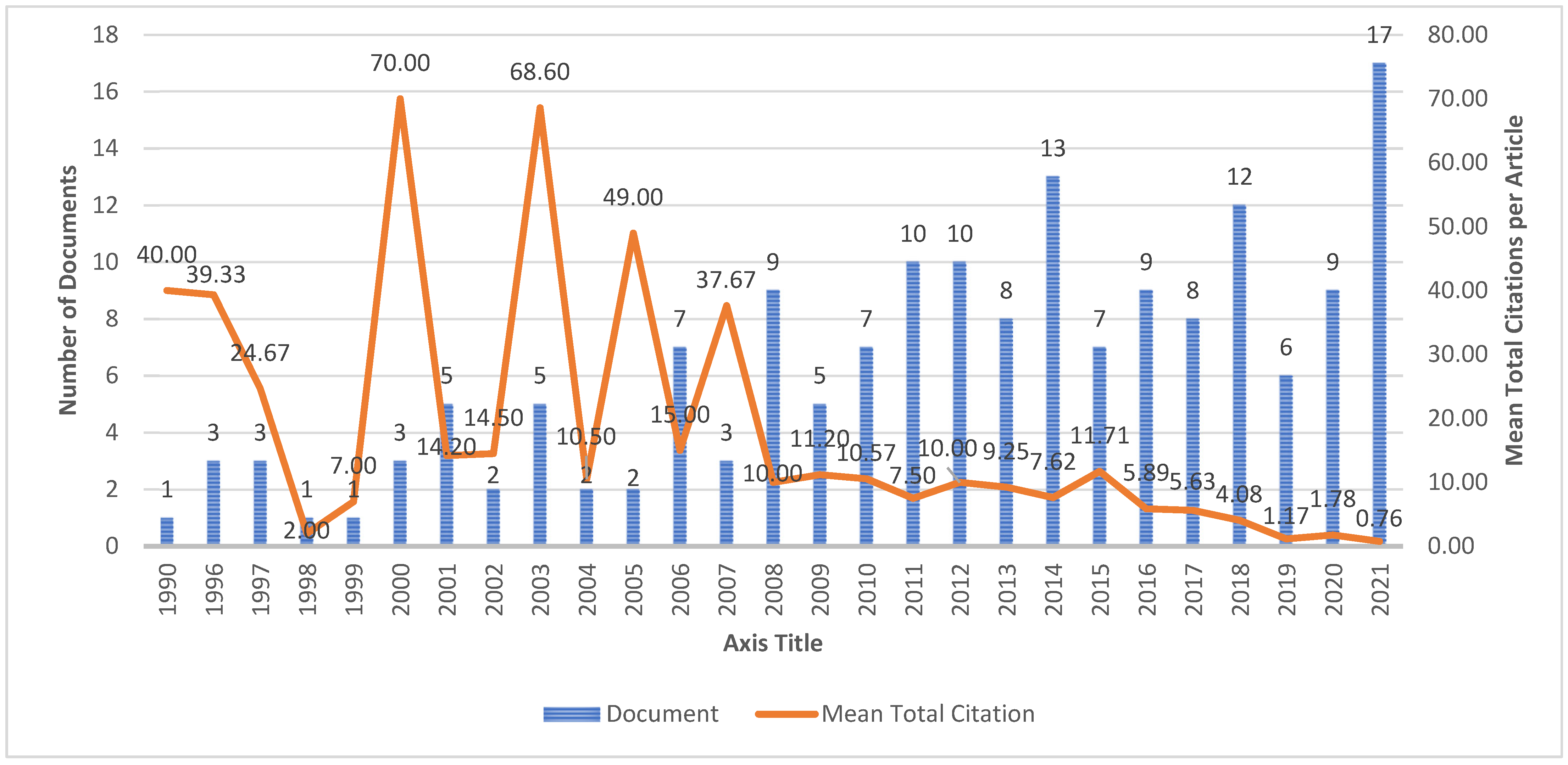

4.1. Publication Growth of Life Insurance Lapsation

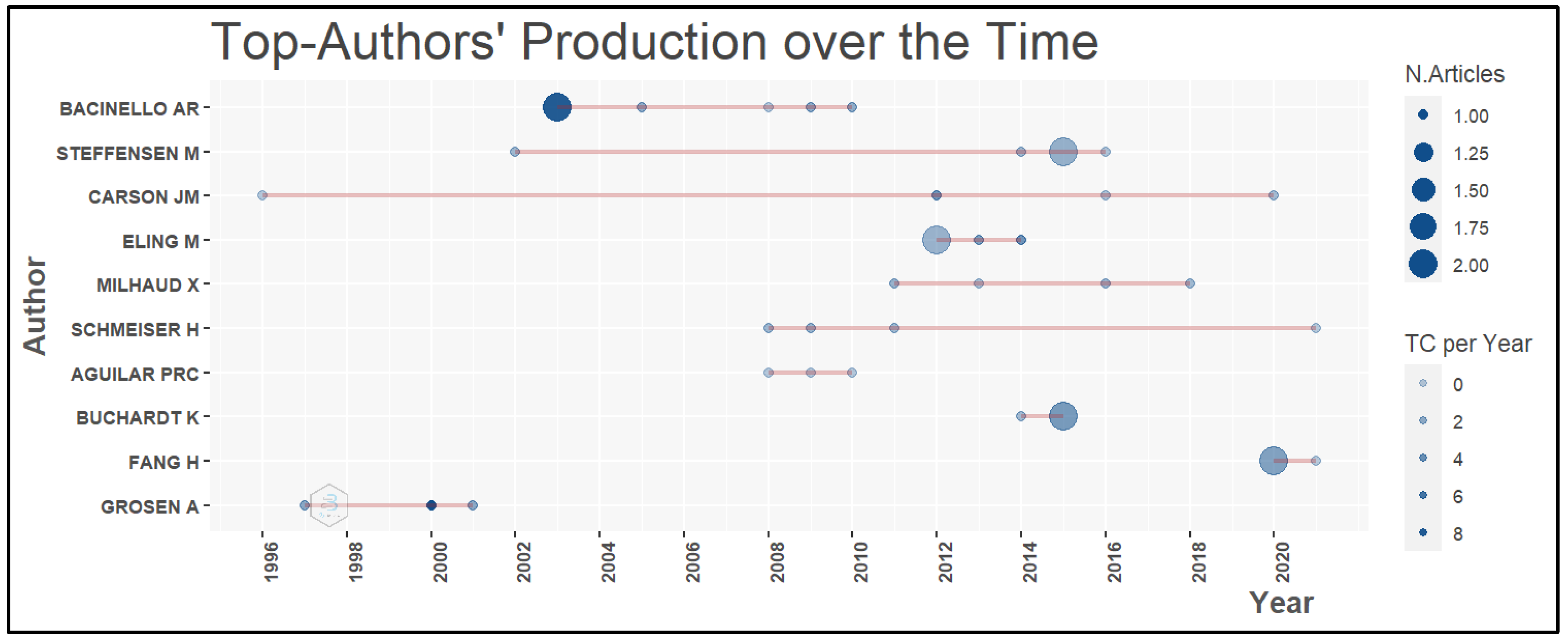

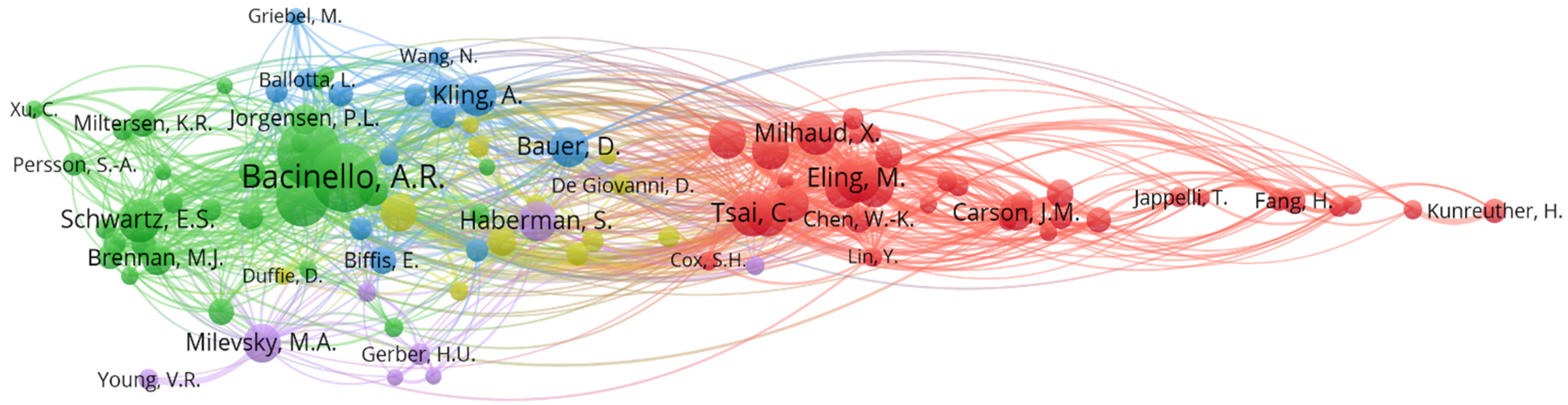

4.2. Productive Authors, Countries, and Journals

4.2.1. Author Network Analysis

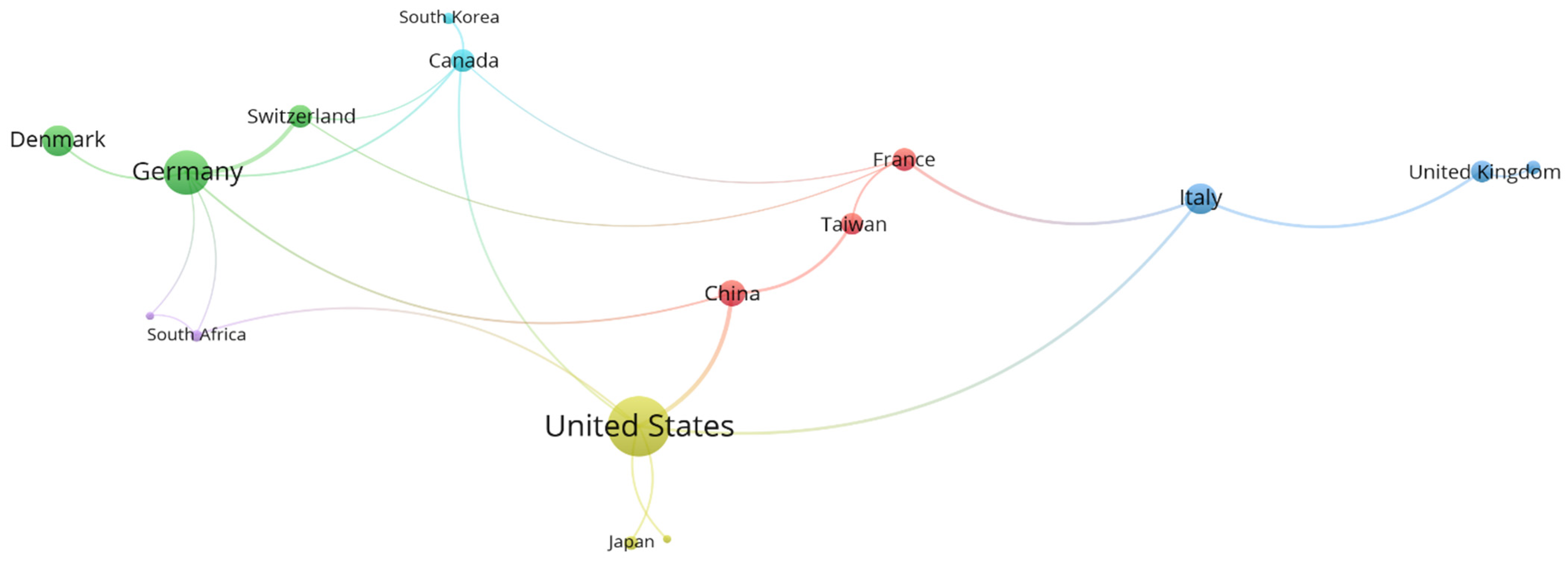

4.2.2. Country Network Analysis

4.2.3. Most Relevant Sources

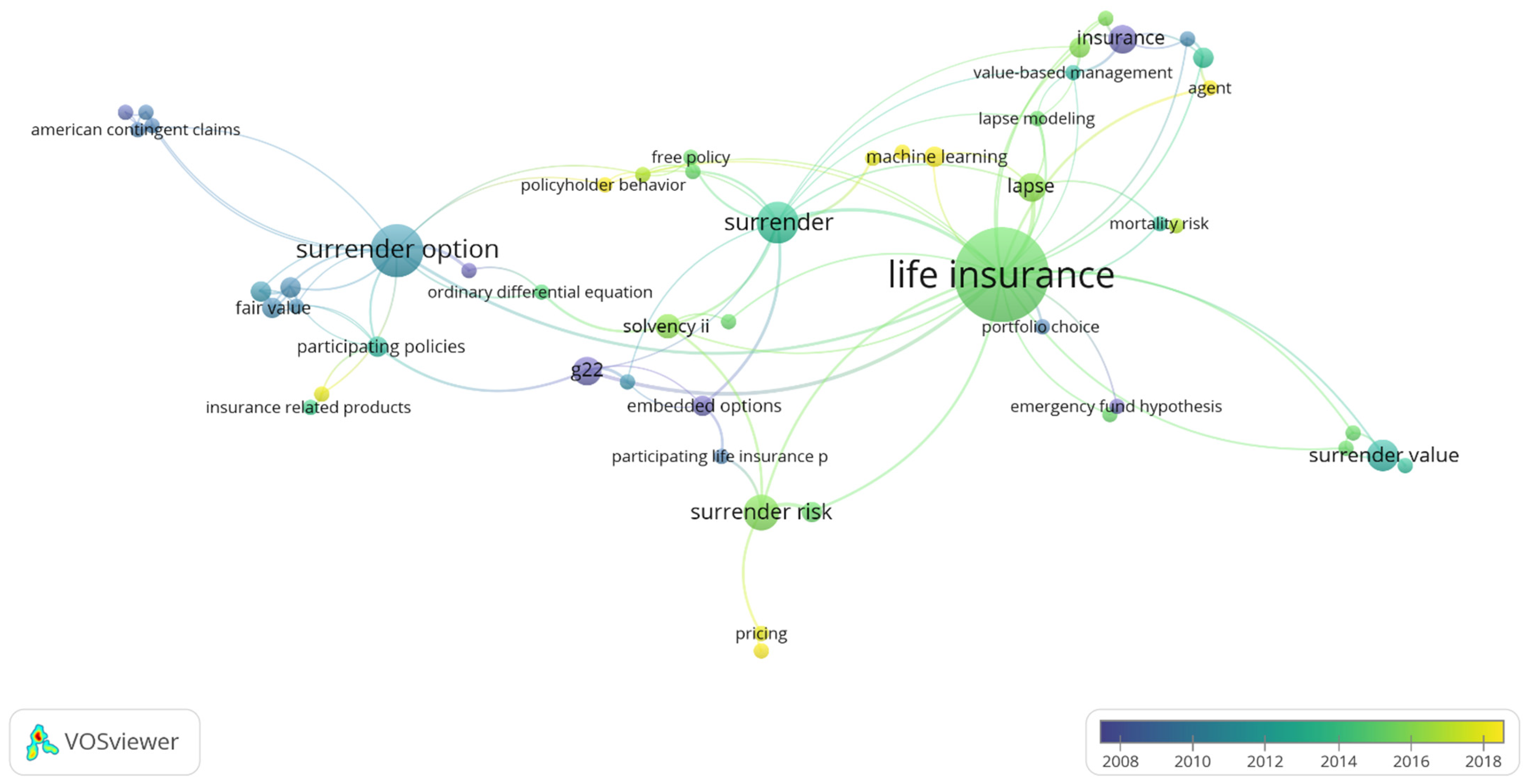

4.3. Co-Occurrence Analysis of Author Keywords

4.4. Document Analysis

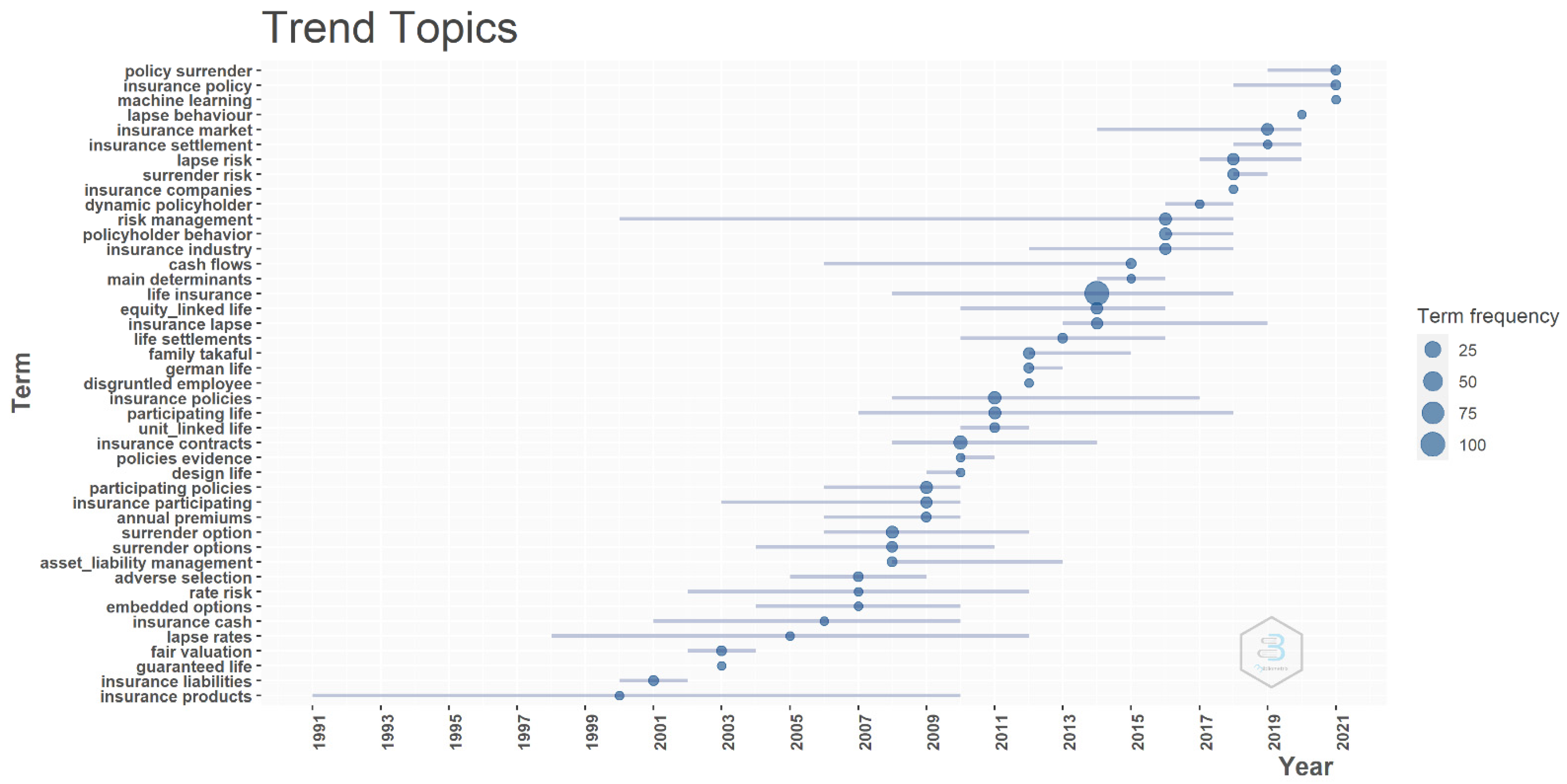

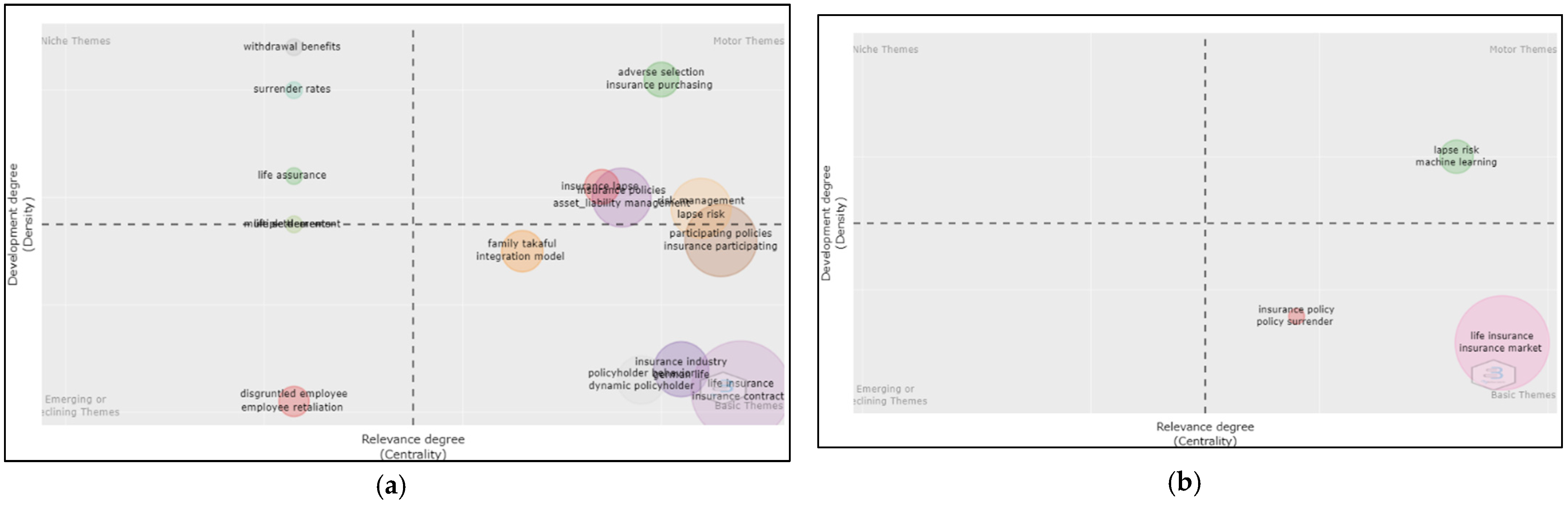

4.5. Trend Topics and Future Directions

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Adams, Mike, Lars-Fredrik Andersson, Magnus Lindmark, Liselotte Eriksson, and Elena Veprauskaite. 2020. Managing Policy Lapse Risk in Sweden’s Life Insurance Market between 1915 and 1947. Business History 62: 222–39. [Google Scholar] [CrossRef] [Green Version]

- Anandalakshmy, A., and K. Brindha. 2017. Policy Holders’ Awareness and Factors Influencing Purchase Decision towards Health Insurance in Coimbatore District. International Journal of Commerce and Management Research 3: 12–16. Available online: www.managejournal.com (accessed on 20 November 2021).

- Aria, Massimo, and Corrado Cuccurullo. 2017. Bibliometrix: An R-Tool for Comprehensive Science Mapping Analysis. Journal of Informetrics 11: 959–75. [Google Scholar] [CrossRef]

- Arici, Faruk, Pelin Yildirim, Şeyma Caliklar, and Rabia M. Yilmaz. 2019. Research Trends in the Use of Augmented Reality in Science Education: Content and Bibliometric Mapping Analysis. Computers & Education 142: 103647. [Google Scholar]

- Bacinello, Anna Rita. 2003a. Pricing Guaranteed Life Insurance Participating Policies with Annual Premiums and Surrender Option. North American Actuarial Journal 7: 1–17. [Google Scholar] [CrossRef]

- Bacinello, Anna Rita. 2003b. Fair Valuation of a Guaranteed Life Insurance Participating Contract Embedding a Surrender Option. Journal of Risk and Insurance 70: 461–87. [Google Scholar] [CrossRef]

- Bacinello, Anna Rita. 2005. Endogenous Model of Surrender Conditions in Equity-Linked Life Insurance. Insurance: Mathematics and Economics 37: 270–96. [Google Scholar] [CrossRef]

- Barucci, Emilio, Tommaso Colozza, Daniele Marazzina, and Edit Rroji. 2020. The Determinants of Lapse Rates in the Italian Life Insurance Market. European Actuarial Journal 10: 149–78. [Google Scholar] [CrossRef] [Green Version]

- Bayer, Alan E., John Carson Smart, and Gerald W. McLaughlin. 1990. Mapping Intellectual Structure of a Scientific Subfield through Author Cocitations. Journal of the American Society for Information Science 41: 444–52. [Google Scholar] [CrossRef]

- Bernama. 2020. Allianz Sees More Payment Defaults in October When Moratorium Ends. Available online: https://www.Thestar.Com.My/Business/Business-News/2020/05/19/Allianz-See-More-Payment-Defaults-in-October-When-Moratorium-Ends (accessed on 16 February 2022).

- Biagini, Francesca, Tobias Huber, Johannes G. Jaspersen, and Andrea Mazzon. 2021. Estimating Extreme Cancellation Rates in Life Insurance. Journal of Risk and Insurance 88: 971–1000. [Google Scholar] [CrossRef]

- Brum, Matias, and Mauricio De Rosa. 2021. Too Little but Not Too Late: Nowcasting Poverty and Cash Transfers’ Incidence during COVID-19’s Crisis. World Development 140: 105227. [Google Scholar] [CrossRef] [PubMed]

- Buchardt, Kristian, and Thomas Møller. 2015. Life Insurance Cash Flows with Policyholder Behavior. Risks 3: 290–317. [Google Scholar] [CrossRef] [Green Version]

- Campbell, Jason, Michael Chan, Kate Li, Louise Lombardi, Lucian Lombardi, Marianne Purushotham, and Anand Rao. 2014. Modeling of Policyholder Behavior for Life Insurance and Annuity Products. Report. Schaumburg: Society of Actuaries. [Google Scholar]

- Carson, James M., Cameron McNeill Ellis, Robert E. Hoyt, and Krzysztof Ostaszewski. 2020. Sunk Costs and Screening: Two-Part Tariffs in Life Insurance. Journal of Risk and Insurance 87: 689–718. [Google Scholar] [CrossRef]

- Cheng, Chunli, and Jing Li. 2018. Early Default Risk and Surrender Risk: Impacts on Participating Life Insurance Policies. Insurance: Mathematics and Economics 78: 30–43. [Google Scholar] [CrossRef]

- Cole, Cassandra, and Stephen G. Fier. 2021. An Examination of Life Insurance Policy Surrender and Loan Activity. Journal of Risk and Insurance 88: 483–516. [Google Scholar] [CrossRef]

- Cox, Samuel Hanson, and Yijia Lin. 2006. Annuity Lapse Rate Modeling: Tobit or Not Tobit? Working Paper. Schaumburg: Society of Actuaries. [Google Scholar]

- Ćurak, Marijana, Doris Podrug, and Klime Poposki. 2015. Policyholder and Insurance Policy Features as Determinants of Life Insurance Lapse-Evidence from Croatia. Economics and Business Review 1: 58–77. [Google Scholar] [CrossRef]

- Della Corte, Valentina, Giovanna Del Gaudio, Fabiana Sepe, and Fabiana Sciarelli. 2019. Sustainable Tourism in the Open Innovation Realm: A Bibliometric Analysis. Sustainability 11: 6114. [Google Scholar] [CrossRef] [Green Version]

- De Giovanni, Domenico. 2010. Lapse Rate Modeling: A Rational Expectation Approach. Scandinavian Actuarial Journal 2010: 56–67. [Google Scholar] [CrossRef]

- Driver, Tania, Mark Brimble, Brett Freudenberg, and Katherine Hunt. 2018. Insurance Literacy in Australia: Not Knowing the Value of Personal Insurance. Financial Planning Research Journal 1: 53. [Google Scholar]

- Eling, Martin, and Dieter Kiesenbauer. 2014. What Policy Features Determine Life Insurance Lapse? An Analysis of the German Market. Journal of Risk and Insurance 81: 241–69. [Google Scholar] [CrossRef]

- Eling, Martin, and Michael Kochanski. 2013. Research on Lapse in Life Insurance—What Has Been Done and What Needs to Be Done? The Journal of Risk Finance 14: 392–413. [Google Scholar] [CrossRef] [Green Version]

- Elsevier B.V. 2020. Scopus Preview-Scopus-Welcome to Scopus. Amsterdam: Elsevier B.V. [Google Scholar]

- Falden, Debbie Kusch, and Anna Kamille Nyegaard. 2021. Retrospective Reserves and Bonus with Policyholder Behavior. Risks 9: 15. [Google Scholar] [CrossRef]

- Fang, Hangmin, and Edward Kung. 2020a. Life Insurance and Life Settlements: The Case for Health-Contingent Cash Surrender Values. Journal of Risk and Insurance 87: 7–39. [Google Scholar] [CrossRef]

- Fang, Hangmin, and Edward Kung. 2020b. Why Do Life Insurance Policyholders Lapse? The Roles of Income, Health, and Bequest Motive Shocks. Journal of Risk and Insurance 88: 937–70. [Google Scholar] [CrossRef]

- Fang, Hanming, and Zenan Wu. 2020. Life Insurance and Life Settlement Markets with Overconfident Policyholders. Journal of Economic Theory 189: 105093. [Google Scholar] [CrossRef]

- Garfield, Eugene, Irving H. Sher, and Ricahrd J. Torpie. 1964. The Use of Citation Data in Writing the History of Science. Philadelphia: Institute for Scientific Information. [Google Scholar]

- Gemmo, Irina, and Martin Götz. 2016. Life Insurance and Demographic Change: An Empirical Analysis of Surrender Decisions Based on Panel Data. 240. SAFE Sustainable Architecture for Finance in Europe. Available online: https://ssrn.com/abstract=3230274Electroniccopyavailableat:https://ssrn.com/abstract=3230274Electroniccopyavailableat:https://ssrn.com/abstract=3230274Electroniccopyavailableat:https://ssrn.com/abstract=3230274 (accessed on 2 March 2022).

- Giri, Manohar. 2018. A Behavioral Study of Life Insurance Purchase Decisions. Indian Institute of Technology Kanpur. Ph.D. thesis, Industrial and Management Engineering, Kanpur, India. [Google Scholar]

- Grant, Jonathan, Robert Cottrell, Françoise Cluzeau, and Gail Fawcett. 2000. Evaluating ‘Payback’ on Biomedical Research from Papers Cited in Clinical Guidelines: Applied Bibliometric Study. BMJ 320: 1107–11. [Google Scholar] [CrossRef] [Green Version]

- Grosen, Anders, and Peter Lochte Jorgensen. 1997. Valuation of Early Exercisable Interest Rate Guarantees. The Journal of Risk and Insurance 64: 481. [Google Scholar] [CrossRef]

- Grosen, Anders, and Peter Løchte Jørgensen. 2000. Fair Valuation of Life Insurance Liabilities: The Impact of Interest Rate Guarantees, Surrender Options, and Bonus Policies. Insurance: Mathematics and Economics 26: 221–53. [Google Scholar] [CrossRef]

- Hong, Jimin. 2020. The Effect of Life Insurance Settlement on Insurance Market and Consumer Welfare. Communications for Statistical Applications and Methods 27: 689–99. [Google Scholar] [CrossRef]

- Hu, Sen, Adrian O’Hagan, James Sweeney, and Mohammadhossein Ghahramani. 2021. A Spatial Machine Learning Model for Analysing Customers’ Lapse Behaviour in Life Insurance. Annals of Actuarial Science 15: 367–93. [Google Scholar] [CrossRef]

- Insurance Barometer Study. 2021. Insurance Barometer Study, LIMRA and Life Happens. COVID-19 Drives Interest in Life Insurance. Available online: https://www.limra.com/siteassets/newsroom/help-protect-our-families/2022_covid-drives-li-awareness_infographic.pdf (accessed on 2 March 2022).

- Janik, Agnieszka, Adam Ryszko, and Marek Szafraniec. 2020. Scientific Landscape of Smart and Sustainable Cities Literature: A Bibliometric Analysis. Sustainability 12: 799. [Google Scholar] [CrossRef] [Green Version]

- Jensen, Bjarke, Peter Løchte Jørgensen, and Anders Grosen. 2001. A Finite Difference Approach to the Valuation of Path Dependent Life Insurance Liabilities. The Geneva Papers on Risk and Insurance Theory 26: 57–84. [Google Scholar] [CrossRef]

- Kagraoka, Yusho. 2005. Modeling Insurance Surrenders by the Negative Binomial Model. Working Paper. Amsterdam: Elsevier Science, Available online: http://www.musashi.jp/ (accessed on 10 November 2020).

- Khan, Ashraf, Mohammad Kabir Hassan, Andrea Paltrinieri, Alberto Dreassi, and Salman Bahoo. 2020. A Bibliometric Review of Takaful Literature. International Review of Economics and Finance 69: 389–405. [Google Scholar] [CrossRef]

- Kiesenbauer, Dieter. 2012. Main Determinants of Lapse in the German Life Insurance Industry. North American Actuarial Journal 16: 52–73. [Google Scholar] [CrossRef]

- Kuo, Weiyu, Chenghsien Tsai, and Wei-Kuang Chen. 2003. An Empirical Study on the Lapse Rate: The Cointegration Approach. Journal of Risk and Insurance 70: 489–508. [Google Scholar] [CrossRef]

- Li, Zongyun, Panteha Farmanesh, Dervis Kirikkaleli, and Rania Itani. 2021. A Comparative Analysis of COVID-19 and Global Financial Crises: Evidence from US Economy. Economic Research-Ekonomska Istraživanja 2021: 1–15. [Google Scholar] [CrossRef]

- Milhaud, Xavier, Stéphane Loisel, and Véronique Maume-Deschamps. 2011. Surrender Triggers in Life Insurance: What Main Features Affect the Surrender Behavior in a Classical Economic Context? Institut Des Actuaires 11: 5–48. [Google Scholar]

- Nobanee, Haitham, Maryam Alhajjar, Ghada Abushairah, and Safaa Al Harbi. 2021a. Reputational Risk and Sustainability: A Bibliometric Analysis of Relevant Literature. Risks 9: 134. [Google Scholar] [CrossRef]

- Nobanee, Haitham, Maryam Alhajjar, Mohammed Ahmed Alkaabi, Majed Musabah Almemari, Mohamed Abdulla Alhassani, Naema Khamis Alkaabi, Saeed Abdulla Alshamsi, and Hanan Hamed AlBlooshi. 2021b. A Bibliometric Analysis of Objective and Subjective Risk. Risks 9: 128. [Google Scholar] [CrossRef]

- Nolte, Sven, and Judith C. Schneider. 2017. Don’t Lapse into Temptation: A Behavioral Explanation for Policy Surrender. Journal of Banking and Finance 79: 12–27. [Google Scholar] [CrossRef]

- Outreville, Jean-Francois. 1990. Whole-Life Insurance Lapse Rates and the Emergency Fund Hypothesis. Insurance Mathematics and Economics 9: 249–55. [Google Scholar] [CrossRef]

- Poufinas, Thomas, and Gina Michaelide. 2018. Determinants of Life Insurance Policy Surrenders. Modern Economy 9: 1400–22. [Google Scholar] [CrossRef] [Green Version]

- Pranckutė, Raminta. 2021. Web of Science (Wos) and Scopus: The Titans of Bibliographic Information in Today’s Academic World. Publications 9: 12. [Google Scholar] [CrossRef]

- Russell, David T., Stephen G. Fier, James M. Carson, and Randy E. Dumm. 2013. An Empirical Analysis of Life Insurance Policy Surrender Activity. Journal of Insurance Issues 36: 35–57. [Google Scholar]

- Russo, Vincenzo, Rosella Giacometti, and Frank J. Fabozzi. 2017. Intensity-Based Framework for Surrender Modeling in Life Insurance. Insurance: Mathematics and Economics 72: 189–96. [Google Scholar] [CrossRef]

- Sanjeewa, Weedige Sampath, Hongbing Ouyang, Yao Gao, and Yaqing Liu. 2019. Decision Making in Personal Insurance: Impact of Insurance Literacy. Sustainability 11: 6795. [Google Scholar] [CrossRef] [Green Version]

- Sirak, Adjmal S. 2015. Income and Unemployment Effects on Life Insurance Lapse. Working Paper. Available online: https://www.researchgate.net/publication/299455763 (accessed on 22 November 2021).

- Song, Yu, Xieling Chen, Tianyong Hao, Zhinan Liu, and Zixin Lan. 2019. Exploring Two Decades of Research on Classroom Dialogue by Using Bibliometric Analysis. Computers & Education 137: 12–31. [Google Scholar] [CrossRef]

- Steffensen, Mogens. 2002. Intervention Options in Life Insurance. Insurance: Mathematics and Economics 31: 71–85. [Google Scholar] [CrossRef]

- Subashini, S., and Ramaswamy Velmurugan. 2015. Lapsation in Life Insurance Policies. International Journal of Advance Research in Computer Science and Management Studies 3: 41–45. Available online: www.ijarcsms.com (accessed on 22 November 2021).

- Tennyson, Sharon. 2011. Consumers’ Insurance Literacy: Evidence from Survey Data. Financial Services Review 20: 165–79. Available online: https://www.researchgate.net/publication/267094407 (accessed on 1 March 2022).

- Vasudev, Mohnish, Raheja Bajaj, and Antonio Alegre Escolano. 2016. On the Drivers of Lapse Rates in Life Insurance. Sarjana thesis, University of Barcelona, Barcelona, Spain. [Google Scholar]

- Waheed, Hajra, Saeed-Ul Hassan, Naif Radi Aljohani, and Muhammad Wasif. 2018. A Bibliometric Perspective of Learning Analytics Research Landscape. Behaviour & Information Technology 37: 10–11. [Google Scholar] [CrossRef]

- Wang, Fanyi, Ruobing Zhang, Faraz Ahmed, and Syed Mir Muhammed Shah. 2021. Impact of Investment Behaviour on Financial Markets during COVID-19: A Case of UK. Economic Research-Ekonomska Istraživanja 2021: 1–19. [Google Scholar] [CrossRef]

- White, H. D., and K. W McCain. 1989. Bibliometrics. Annual Review of Information Science and Technology 24: 119–86. [Google Scholar]

- Xong, Lim Jin, Lim Jin Xong, and Ho Ming Kang. 2019. A Comparison of Classification Models for Life Insurance Lapse Risk. International Journal of Recent Technology and Engineering 7: 245–50. [Google Scholar]

- Yacob, Rubayah, Mohd Hafizuddin Bangaan Abdullah, and Norasykeen Mohd Baharom. 2018. Analisis Polisi Luput Pelan Takaful Keluarga. Journal of Muamalat and Islamic Finance Research 15: 109–24. [Google Scholar] [CrossRef]

- Yakob, Rubayah, B.A.M. Hafizuddin-Syah, and Nurfarhana Hani Badrul Hisham. 2019. Demographic Analysis towards the Understanding of Education Takaful (Islamic Insurance) Plan. Malaysian Journal of Society and Space 15: 92–105. [Google Scholar] [CrossRef]

- Yong, Jeffery. 2020. Insurance Regulatory Measures in Response to COVID-19. FSI Briefs No. 4. Financial Stability Institute. Available online: www.bis.org/emailalerts.htm (accessed on 30 December 2021).

- Yu, Lu, Jiang Cheng, and Tzuting Lin. 2019. Life Insurance Lapse Behaviour: Evidence from China. Geneva Papers on Risk and Insurance: Issues and Practice 44: 653–78. [Google Scholar] [CrossRef]

- Zakaria, Rahimah, Aidi Ahmi, Asma Hayati Ahmad, and Zahiruddin Othman. 2021. Worldwide Melatonin Research: A Bibliometric Analysis of the Published Literature between 2015 and 2019. Chronobiology International 38: 1–11. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Document Type | Frequency | Percentage (n = 373) |

|---|---|---|

| Article | 151 | 84.40 |

| Conference paper | 13 | 7.30 |

| Review | 7 | 3.90 |

| Book | 4 | 2.20 |

| Book chapter | 3 | 1.70 |

| Total | 178 | 100.00 |

| Author | TLS | NL | Citations | Cluster |

|---|---|---|---|---|

| Anna Rita Bacinello | 87.50 | 89 | 95 | 2 |

| Anders Grosen | 84.93 | 90 | 90 | 2 |

| Peter Lohte Jørgensen | 59.14 | 86 | 65 | 2 |

| Martin Eling | 48.56 | 87 | 51 | 1 |

| Chenghsien Tsai | 47.58 | 89 | 49 | 1 |

| Weiyu Kuo | 44.33 | 89 | 45 | 1 |

| Eduardo Schwartz | 43.83 | 72 | 47 | 2 |

| Nadine Gatzert | 40.67 | 87 | 43 | 1 |

| Xavier Milhaud | 40.13 | 72 | 44 | 1 |

| Alexander Kling | 39.74 | 87 | 41 | 3 |

| Country | TLS | NL | Documents | Citations | Cluster |

|---|---|---|---|---|---|

| United States | 10 | 6 | 39 | 473 | 4 |

| Germany | 8 | 6 | 24 | 245 | 2 |

| China | 7 | 3 | 11 | 17 | 1 |

| Italy | 6 | 3 | 14 | 289 | 3 |

| Switzerland | 5 | 3 | 9 | 185 | 2 |

| Canada | 4 | 5 | 9 | 116 | 6 |

| France | 4 | 4 | 9 | 72 | 1 |

| Taiwan | 3 | 2 | 8 | 31 | 1 |

| United Kingdom | 3 | 2 | 8 | 234 | 3 |

| South Africa | 2 | 3 | 3 | 10 | 5 |

| Journal | Country | TC | TP | CS | SJR | Quartile |

|---|---|---|---|---|---|---|

| Insurance: Mathematics and Economics | Netherlands | 493 | 20 | 2.7 | 1.139 | Q1 |

| Journal of Risk and Insurance | United Kingdom | 366 | 16 | 3.6 | 1.055 | Q1 |

| North American Actuarial Journal | United Kingdom | 129 | 8 | 1.6 | 0.936 | Q2 |

| Scandinavian Actuarial Journal | United Kingdom | 78 | 6 | 2.7 | 1.061 | Q1 |

| Journal of Banking and Finance | Netherlands | 106 | 3 | 4.4 | 1.58 | Q1 |

| Journal of Risk Finance | United Kingdom | 45 | 4 | 2.1 | 0.295 | Q3 |

| Risks | Switzerland | 27 | 5 | 1.4 | 0.403 | Q2 |

| Astin Bulletin | United Kingdom | 8 | 2 | 2.1 | 1.113 | Q1 |

| European Actuarial Journal | Switzerland | 18 | 3 | 1.4 | 0.661 | Q2 |

| Geneva Papers on Risk and Insurance: Issues and Practice | United States | 10 | 3 | 2.0 | 0.535 | Q2 |

| No. | Author(s) | Document Title | Source | LC | GC | NLC |

|---|---|---|---|---|---|---|

| 1 | Grosen and Løchte Jørgensen (2000) | Fair valuation of life insurance liabilities: The impact of interest rate guarantees, surrender options, and bonus policies | Insurance: Mathematics and Economics | 39 | 206 | 18.93 |

| 2 | Bacinello (2003b) | Fair valuation of a guaranteed life insurance participating contract embedding a surrender option | Journal of Risk and Insurance | 27 | 98 | 27.55 |

| 3 | Bacinello (2003a) | Pricing guaranteed life insurance participating policies with annual premiums and surrender option | North American Actuarial Journal | 22 | 61 | 36.07 |

| 4 | Grosen and Jorgensen (1997) | Valuation of early exercisable interest rate guarantees | Journal of Risk and Insurance | 20 | 62 | 32.26 |

| 5 | De Giovanni (2010) | Lapse rate modelling: a rational expectation approach | Scandinavian Actuarial Journal | 18 | 31 | 58.06 |

| 6 | Outreville (1990) | Whole-life insurance lapse rates and the emergency fund hypothesis | Insurance: Mathematics and Economics | 17 | 40 | 42.50 |

| 7 | Bacinello (2005) | Endogenous model of surrender conditions in equity-linked life insurance | Insurance: Mathematics and Economics | 15 | 36 | 41.67 |

| 8 | Steffensen (2002) | Intervention options in life insurance | Insurance: Mathematics and Economics | 13 | 28 | 46.43 |

| 9 | Jensen et al. (2001) | A finite-difference approach to the valuation of path-dependent life insurance liabilities | The Geneva Papers on Risk and Insurance Theory | 13 | 51 | 25.49 |

| 10 | Eling and Kiesenbauer (2014) | What policy features determine life insurance lapse? An analysis of the German market | Journal of Risk and Insurance | 12 | 34 | 35.29 |

| Author(s) | TC | Title | Method(s) | Variable(s) | Main Result(s) | Recommendation(s) |

|---|---|---|---|---|---|---|

| Hu et al. (2021) | 5 | A spatial machine learning model for analysing customers’ lapse behaviour in life insurance | Spatial analysis and logistic regression | Sum assured, age, duration, gender, total number of policies, number of lapsed policies, household composition, education level, employment status | Adding census clustering at the local population level to the company’s current internal data does not improve lapse prediction. | Use a larger dataset such as an all-Ireland dataset to understand the relationship between cluster characteristics and policyholder lapse behaviour. |

| Falden and Nyegaard (2021) | 4 | Retrospective reserves and bonus with policyholder behaviour | Markov model | Age of policyholder, age of retirement, termination, premium, annuity, term insurance | The study derives accurate differential equations for the state-wise projections of the savings account and surplus with the optimal free-policy factor where all benefits are governed by bonus. However, it fails to predict the savings account and surplus with an optimal free-policy factor when policyholder behaviour is considered. | Adding a more complex dividend strategy to the model and allowing for dependencies on assets and market values. Another research topic is, How to determine the best dividend approach in a multi-state setting? |

| Fang and Wu (2020) | 4 | Life insurance and life settlement markets with overconfident policyholders | Utility function | Income, health status, bequest motives, preference, timing, commitment, and contracts | When overconfident consumers are sufficiently susceptible to strong intertemporal consumption substitution elasticity, a life settlement market may raise their equilibrium welfare. | Should experimentally test the existence of policyholder overconfidence based on the predictions in this study. Study the settlement market’s welfare consequences in a unified framework where lapsation is driven by both bequest motive and negative income shocks. |

| Fang and Kung (2020a) | 4 | Life insurance and life settlements: The case for health-contingent cash surrender values | Utility function | Income, health status, bequest motives, timing, commitment, and contracts | The consumer welfare loss induced by the settlement market can be partially mitigated by optimally determining cash surrender values, but only if the cash surrender values are allowed to be conditional on health status. | - |

| Cole and Fier (2021) | 3 | An examination of life insurance policy surrender and loan activity | Logistic regression | Major expenses, income drop, expenditure, unemployment, late loan, credit status, net worth, inflation, marital status, age, number of children | While some overlaps in the circumstances cause families to use their cash value policies to attain some goal(s), households perceive surrenders and loans as separate activities. | - |

| Carson et al. (2020) | 3 | Sunk costs and screening: Two-part tariffs in life insurance | Cox proportional hazard model | Backdate, days after birthday, lapse, face amount, annual premium, days in force | Even when correcting for arbitrary nonlinearity in premium effects on lapse proclivity, life insurance clients demonstrate behaviour consistent with the sunk cost fallacy in their lapsing behaviour. | Further studies on the optimal menu of contracts. |

| Adams et al. (2020) | 2 | Managing policy lapse risk in Sweden’s life insurance market between 1915 and 1947 | Panel data | Unemployment, wage growth, interest rate, pension, regulation, new policies, firm size, organisation form, policy size, age, death rate, lapse total, cash surrender, surrender, expense cash, dividends, bonus | The findings support previous emergency fund tests and interest rate explanations for voluntary life insurance policy cancellations. | - |

| Biagini et al. (2021) | 1 | Estimating extreme cancellation rates in life insurance | Dynamic peaks-over-threshold (POT) | Direct written premium, policies lapsed, policies surrendered, policies lost, policies issued, policies revived, policies assumed, term life in force, permanent life in force, total in force, share of term policies, share of issued policies, interest rate changes, cancellation rates | There is a positive relationship between new company activity and high cancellation rates. There is no correlation between interest rate changes and high cancellation rates. | Future research should use the dynamic POT approach on a larger dataset to examine the mass cancellation scenario in the German market by product category. Further research using different periods. |

| Barucci et al. (2020) | 1 | The determinants of lapse rates in the Italian life insurance market | Generalised linear modelling and survival analysis | Age, contract age, contract size, product type, gender, premium frequency, region, profession, inflation rate, growth rate of disposable income, growth rate of the European stock index | There is modest evidence supporting the Interest Rate Hypothesis, a positive link between interest and lapse rates, for contracts signed a few years ago. Instead, some data suggest that lapse rates are linked to personal financial/economic issues (the emergency fund hypothesis). | - |

| Hong (2020) | 1 | The effect of life insurance settlement on insurance market and consumer welfare | Utility function | The introduction of settlement can enhance insurance demand and customer welfare even when the trading cost is higher than the liquidity cost. The monopolistic insurer can either boost or decrease insurance demand depending on the population distribution and policyholders’ liquidity risk. | - |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shamsuddin, S.N.; Ismail, N.; Roslan, N.F. What We Know about Research on Life Insurance Lapse: A Bibliometric Analysis. Risks 2022, 10, 97. https://doi.org/10.3390/risks10050097

Shamsuddin SN, Ismail N, Roslan NF. What We Know about Research on Life Insurance Lapse: A Bibliometric Analysis. Risks. 2022; 10(5):97. https://doi.org/10.3390/risks10050097

Chicago/Turabian StyleShamsuddin, Siti Nurasyikin, Noriszura Ismail, and Nur Firyal Roslan. 2022. "What We Know about Research on Life Insurance Lapse: A Bibliometric Analysis" Risks 10, no. 5: 97. https://doi.org/10.3390/risks10050097

APA StyleShamsuddin, S. N., Ismail, N., & Roslan, N. F. (2022). What We Know about Research on Life Insurance Lapse: A Bibliometric Analysis. Risks, 10(5), 97. https://doi.org/10.3390/risks10050097