1. Introduction

Financial scandals in the U.S. and Europe (e.g., Enron, WorldCom, and Lehman and Brothers in the U.S.; Parmalat in Italy; Banco Português de Negócios, Banco Privado Português, and Banco Espírito Santo in Portugal) have demonstrated the relevance of the quality of financial reports (

Gaio and Raposo 2011). The lack of financial information quality can lead to a misunderstanding about the firms’ financial performance and sustainability (

Huynh 2019).

In moments of financial distress, managers tend to use earnings management or other practices to change financial reporting. Such behaviour aims to hide financial problems from stakeholders, meet financial investors’ expectations, reduce the cost of financial debt, access to new loans, maintain managers’ own bonuses, avoid the loss of reputation, and/or comply with legislation or other obligations (

Healy and Wahlen 1999;

Habib et al. 2013;

Dimitras et al. 2015). Therefore, this work intends to understand whether financial report quality impacts firms’ probabilities of default.

Beaver et al. (

2012) argue that financial reporting attributes are relevant to predicting a firm’s bankruptcy. Accounting-based models have been presented with a high predictive power of firms’ default and bankruptcy. However, if the indicators listed in the financial statements are not of high quality, this may compromise not only the financial informativeness but also may deteriorate the models’ predictive power. However, most studies on financial distress use accounting and market-based indicators (e.g.,

Altman 1968;

Lin 2009;

Mselmi et al. 2017;

Pacheco et al. 2019) without including financial reporting quality. In this work, this gap in the literature is filled as FRQ proxies are included to explain firms’ probabilities of default. The inclusion of FRQ proxies in the default prediction model allows us to consider the fluctuations between two reporting periods that can be masked in the financial statements that are annually reported. Financial ratios, which are included as determinants of firms’ probabilities of default, are determined at the end of the year with the available financial information which can lack quality. Therefore, financial ratios may not show all the relevant financial information of the company (

Du et al. 2020).

Studies which link financial reporting quality and probability of distress are limited but they are consensual on the impact of FRQ on financial distress. To the best of our knowledge, the few existing studies only address one of the FRQ characteristics—earnings management which is related to accruals quality (e.g.,

Beaver et al. 2012;

Diegues and Alves 2016;

Lin et al. 2016;

Nagar and Sen 2018;

Wu et al. 2018). Except for the above,

Ashraf et al. (

2020) analyse the impact of accruals quality and the earnings quality on firms’ probabilities of bankruptcy focusing on the listed firms. Nevertheless, financial information quality is not directly observable, and it is a multidimensional concept that can be evaluated using several proxies, such as accruals quality smoothness, value relevance, timeliness, and conservatism (

Gaio and Raposo 2011;

Perotti and Wagenhofer 2014;

Huynh 2019). The different proxies try to capture the desirable characteristics of financial information: relevance, faithful representation, understandability, comparability, verifiability, and timeliness. In this way, the different proxies end up capturing different characteristics and can affect different realities in different ways.

Despite the vast literature on financial distress, this study has four important contributions that will be explained: (i) it analyses various FRQ measures; (ii) it focuses on the SMEs; (iii) a specific country and sector are studied; and (iv) the methodology used presents particularities not previously applied.

Different financial information quality characteristics can impact SME’s default probability, namely accruals quality (related to earnings management), smoothing, and timeliness (the three proxies that can be analysed for SMEs). By including several proxies of financial information quality, this study aims not only to enlarge the literature review on this theme but also to give a deeper understanding of the impact of different characteristics of FRQ on firms’ probabilities of default. Managers can engage in earnings management practices, but can also smooth earnings, present less timely earnings, and not report information that is relevant to financial investors.

This paper intends to understand if FRQ helps to predict SMEs’ financial default. Previous works mostly focus on listed companies (e.g.,

Beaver et al. 2012;

Lin et al. 2016;

Wu et al. 2018;

Ashraf et al. 2020). The main reason for using listed companies is due to the easiest information availability. However, SMEs present a higher probability of default since their financial situation is less stable and they have more financial constraints (

Pacheco et al. 2019). Additionally, firms’ data quality depends on the type of firm (

Du et al. 2020). The regulation regarding the information quality of listed firms is different from unlisted ones (

Campa and Camacho-Miñamo 2014). Private firm financial reporting is of lower quality due to different market demands, regulation notwithstanding (

Ball and Shivakumar 2005). However, it is important to refer that the financial information of listed firms may suffer from information asymmetries and the need for managers to meet financial investors’ expectations (

Healy and Wahlen 1999). On the other hand, the users of financial information are also different (e.g., as listed firms are to financial investors, as SMEs are to banks). Such differences may compromise the generalization of the results obtained for large firms when applied to the SME unlisted firms. Nonetheless, SMEs are most firms all over the world and play an important role, as they have a relevant contribution not only to gross domestic product but also to job generation, which proves the need to understand this group of firms and gives support to this study.

A sample of Portuguese SMEs for the construction sector from 2012 to 2018 is analysed. Portugal is a small-size country almost unexplored, with singularities regarding large-size countries such as the U.S. (e.g.,

Charitou et al. 2007;

Nagar and Sen 2018) and China (e.g.,

Lin et al. 2016;

Wu et al. 2018;

Shen et al. 2020), where most works in the area were conducted. Moreover, it is a code-law country, with great financial asymmetries, which increases managers’ incentives to engage in earnings management practices (

Dimitras et al. 2015), reinforcing the need to understand the impact of these practices. Finally, in Portugal loans are the more relevant financial source of firms’ financing, so understanding firms’ probabilities of defaulting helps to promote the sustainability of the financial systems (

Bhimani et al. 2010). This work also focuses on a specific sector: the construction industry. Each sector has singularities regarding financial ratios and the quality of financial information differs by sector (

Kinnunen et al. 1995). Thus, analysing a unique sector avoids biased results. Regarding the importance of the construction industry, it is an industry with a fundamental role in the country’s development and citizens’ well-being. It drives productivity, employment, and wealth directly and indirectly through other subsectors (

Abdullahi and Bala 2018). According to

PORDATA (

2021), it is the fourth industry at the European level to create more wealth for the country. Additionally,

Choi et al. (

2018) argue that the construction sector is one of the more sensitive industries to economic cycles due to the long duration of the projects which causes liquidity problems and increases the financial risk (

Muscettola 2014). In fact, in Portugal, this sector not only has significant relevance to the economy (

Baganha et al. 2002) but it has also been characterized by high mortality rates in recent years (

Kapelko et al. 2015). The failure of a construction company is pressing for governments and economies because of the unfinished projects and covenants established (

Assaad and El-Adaway 2020). Therefore, understanding signs of default in advance in this industry allows to avoid (or at least reduce) situations of bankruptcy which can impact the whole country (directly or indirectly).

To analyse the impact of FRQ on the probability of default, firms are classified as compliant (firms with a healthy financial situation) or default (firms with a probability of not meeting debt responsibilities). For that, the ex-ante criteria proposed by

Lisboa et al. (

2021) are followed since they can be used for SMEs. Most studies about default’s probability and the impact of earnings management (a characteristic of FRQ) on default use an ex-post criterion or a mix classification (considering both in simultaneous: ex-post and ex-ante criterion) of default (e.g.,

García-Lara et al. 2009;

Diegues and Alves 2016;

Dutzi and Rausch 2016;

Ashraf et al. 2020). In both cases, firms are already in bankruptcy or insolvent, which is a severe financial situation that cannot be surpassed. Moreover, the legal criterion is country-specific which limits the comparison since laws, which are the base of ex-post classification, are singular, and can also depend on the macroeconomic environment (

Bhimani et al. 2010). An ex-ante criterion allows us not only to detect the warning signs of financial difficulties and solve them in time, but also facilitates generalization to other contexts. Considering the study’s aim, it will also be important to understand the signs of financial problems in advance.

Dutzi and Rausch (

2016), who analyse the impact of earnings management periods before bankruptcy, found that the impact of the quality of financial information is different depending on the level of default. Firms that seem healthier before bankruptcy engage more in earnings management practices than the ones that look unhealthier before bankruptcy. Therefore, when considering the ex-ante criterion, we will be analysing the impact of the FRQ before this motivation as defended by

Dutzi and Rausch (

2016).

Given the extensive list of predictive variables of default and the particularities of the sector studied the stepwise regression approach was used, following

Mselmi et al. (

2017), and

Ashraf et al. (

2020). Adopting a backward elimination method, we surpass the bias problem of including a large set of ratios. This methodology was also used by

Ashraf et al. (

2020), who also analysed the impact of earnings quality on the probability of default, but they applied it only to the accounting ratios. This work goes a step further by including simultaneously both accounting and FQR measures. In this way, we analysed the relevance of all the variables introduced, demonstrating the relevance of FQR measures, namely accruals quality and timeliness. The fact that more than one proxy is statistically relevant confirms the need to analyse more than one FQR characteristic beyond the impact of earnings management. These variables are included not only because the study aims to understand FRQ’s impact on default, but also because its significant relevance is confirmed a priori by the stepwise method.

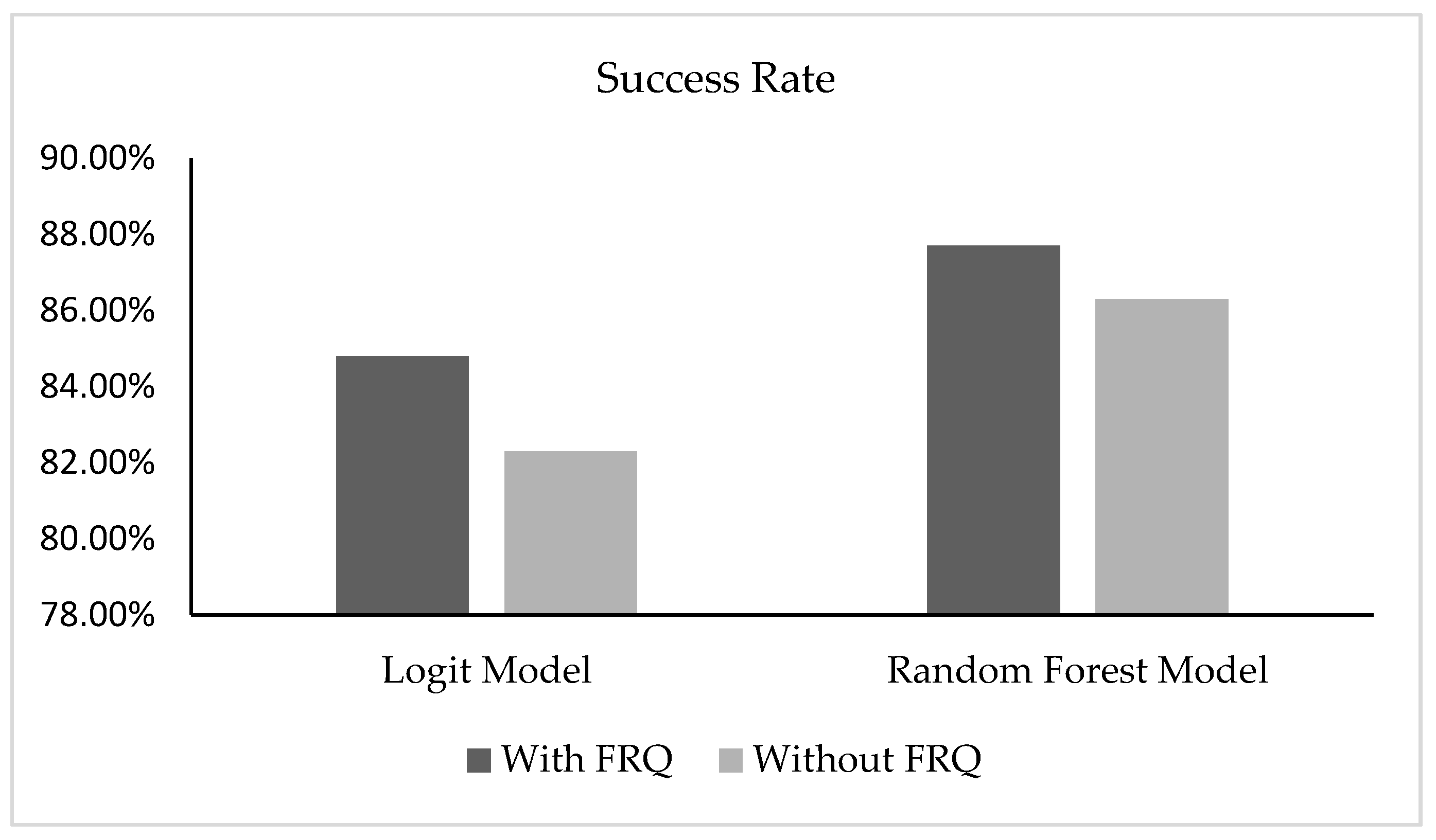

A logit model is then used to present a financial distress prediction model. This model presents an accuracy of 85% and is more efficient in the classification of compliant firms. Without FRQ, the accuracy of the model decreases, and error type I (classifying a firm as compliant when it is in default) is more evident. Additionally, a robustness analysis is done through the random forest methodology. New age classifier models were proposed (

Jones et al. 2015) to improve the predictive power of traditional models, such as logit. However, these techniques are still unexplored due to their complexity and time consumption (

Giriūniene et al. 2019). In both analyses, results confirm the relevance of FRQ proxies, especially in correctly classifying default firms. Few studies focus on the financial distress prediction of SMEs in the Portuguese context, and as far as we know, none used the random forest methodology.

Besides the several contributions in the literature, this work also contributes to practice. Firms’ bankruptcy affects stakeholders’ welfare such as shareholders, employees, creditors, and the government, among others (

Beaver et al. 2011). The results also give insights to managers, especially construction sector managers, to understand how they can detect financial problems in advance to avoid default. Moreover, it helps to understand the impact of financial reporting quality to prevent additional risks, and which factors can lead to financial distress.

This paper is organized into six sections. After this first introductory section,

Section 2 presents a theoretical context, followed by the sample characterization and the description of the methodology and variables to be used in the analysis of default risk. In

Section 4, the results are discussed. The next section presents a discussion. Finally, the main conclusions, as well as limitations and suggestions for future research, are presented in the last section.

5. Discussion

Accruals’ quality negatively impacts firms’ probabilities of default. This fact proposes that firms who tend to mislead investors know their financial situation and want to meet stakeholders’ interests or continue to access bank loans at lower costs to survive in the future. However, based on

Rosner (

2003), this conclusion does not mean that later these firms go into bankruptcy. When the probability of financial distress increases, firms show their real situation, increasing financial report quality. Results are singular when compared with the literature that analyses listed companies (e.g.,

Beaver et al. 2012;

Lin et al. 2016;

Nagar and Sen 2018;

Wu et al. 2018;

Ashraf et al. 2020). SMEs’ financial reporting quality is different compared to listed companies as well as the users of this information which can support the results obtained (

Campa and Camacho-Miñamo 2014). SMEs have different motivations to engage in earnings management practices (usually to have benefits in their relationship with banks).

Diegues and Alves (

2016), who analysed Portuguese firms (with total assets higher than one million euros) already in bankruptcy (ex-post criterion), found that one year before bankruptcy, firms’ earnings management increases (less FRQ). These conclusions suggest that this situation is common to SMEs and/or to Portuguese firms with financial problems.

Timeliness also contributes to explaining firms’ probabilities of default. Firms’ financial information should be rapidly available to users, but sometimes managers delay or advance information to influence stakeholders’ perceptions. Firms with previous losses (bad news) tend to change earnings due to the need to access bank loans or to meet their covenants, as suggested by

García-Lara et al. (

2009). Results show that when net income has a significant variation from one year to the other, firms’ probabilities of default increase. This is also related to predictability as less constant earnings are less predictable, which is not desirable for stakeholders who prefer more stable firms. Therefore, when financial information is of quality and is reported in a timely fashion, firms’ probabilities of default decrease.

This work also aimed to develop a model with an optimal set of variables to predict the probability of default. To fulfil this, the stepwise method was used following

Mselmi et al. (

2017) and

Ashraf et al. (

2020). FRQ and accounting measures were simultaneously included, and the results show the relevance of FRQ. Nevertheless, three FRQ proxies were included, and only two were significant for this specific sample, necessitating replication of this approach in different countries and/or sectors.

Additionally, to FRQ variables, results show that smaller, less profitable, and less efficient more indebted firms, with more working capital, are more likely to present financial problems. Less efficient firms usually do less profitable investments and so are less profitable. Therefore, self-funding is not sufficient to cover financial needs and firms tend to increase debt, especially when working capital needs to increase. With the increase of liabilities, firms’ obligations also increase, which can lead to financial problems. This situation is more common for smaller firms as these firms usually do not have the financial capacity to surpass financial difficulties. The conclusions are mainly in line with research on default (e.g.,

Altman 1968;

Lin 2009;

Mselmi et al. 2017;

Pacheco et al. 2019). The exception is regarding the CL/L impact, which can be justified by the specificities of this sector. The greater the weight of current liabilities over total liabilities, the lower the probability of default. The construction sector is characterized by a long duration of projects that cause liquidity problems and increase its financial risk (

Muscettola 2014). Therefore, firms that are able to negotiate higher credits with suppliers will need less financial debt and thus face fewer financial difficulties. This conclusion highlights the need to explore each sector separately due to its specificities.

The results also show that the construction sector highly depends on macroeconomic factors, mainly on the inflation rate. When inflation decreases, the firms’ probabilities of default increase. This conclusion contradicts the expectations and results of

Antunes and Mucharreira (

2015) who analysed Portuguese SMEs. Therefore, this result can be specific to this sample.

The proposed model presents an accuracy of 85%, which is higher than those of

Ashraf et al. (

2020). The model classifies better compliant firms. Moreover, results are confirmed through the random forest methodology, which is a new age classifier less used due to its complexity and time-consuming. In both analyses, the results confirm the relevance of FRQ proxies, especially in correctly classifying default firms.

Besides the several contributions in the literature, the conclusions necessitate that firms make efficient investments that promote more sales and profits, which will decrease external financial needs and increase financial wealth. Moreover, firms should present high-quality earnings and financial reports in a timely manner.

6. Conclusions

A firm’s probability of default is not a new research theme but is gaining prominence in recent years since it helps to avoid firms’ bankruptcy. Several sets of variables, models, and methodologies have been discussed in the literature to define a more accurate way to predict distress. However, few studies have analysed the impact of financial reporting quality in this relation, and the ones which take it into account focus mainly on earnings management (or accruals quality), which is only one characteristic. This study aims to understand if FRQ proxies impact firms’ probabilities of default. Three measures of FRQ that can be used by SMEs are included: accruals quality (related to earnings management), earnings timeliness, and earnings smoothness.

A panel of data of Portuguese SMEs in the construction sector from 2012 to 2018 was analysed for this purpose. First, we classify firms in default or compliant using an ex-ante classification. Using signs to predict firms’ financial problems in advance will allow a firm to make timely decisions to avoid bankruptcy. This is of greater relevance, especially in the construction sector which is characterized by a long duration of projects that last more than one year. The results show the prevalence of compliant firms over the period analysed.

Second, we use the stepwise methodology to identify the most accurate set of variables, both financial reporting quality and accounting variables, to predict firms’ probabilities of default. Findings show the relevance of FRQ proxies, namely accruals quality and earnings timeliness to financial distress. This finding shows not only that FRQ should be included to predict default, but also that earnings management (proxy of accruals quality) is not sufficient to explain it. Moreover, the variables group of leverage, liquidity, size, profitability, efficiency, and cash flow are also relevant to discriminate between default and compliant firms.

Third, using a logit model to predict financial distress, our results prove that by including FRQ proxies, the success prediction rate of the model increases, suggesting that financial information quality is relevant to explaining firms’ default and especially to correctly classifying distress firms (avoiding error type I, which is more costly to firms). Finally, results were confirmed using a new age classifier model: the random forest.

This study makes several contributions to the literature, practice, and society. First, the literature about financial distress is enlarged since results prove the relevance of FRQ to predict default. Studies analysing this relation are scarce and the existing ones focus on earnings management, one characteristic of FRQ (accruals quality), and/or on listed firms. By including more proxies of FRQ, which are relevant to predicting distress, we add new knowledge to the literature. Moreover, when using the stepwise methodology to understand the best set of variables to predict the financial distress of the specific sample, we have included FRQ proxies as well as financial determinants and the results prove the relevance of both types of variables. Previous studies such as

Ashraf et al. (

2020) use the stepwise methodology only for financial determinants and then include FRQ proxies in the final model. Finally, not only traditional models of financial distress are used, such as the logit model, but also a new age classifier, the random forest methodology, which, to our knowledge, has not been used in a Portuguese sample before.

Moreover, in practice, managers of the construction sector can understand the firms’ financial situation in advance by understanding the signs of financial problems and which variables help to predict default situations. The impact of financial information quality to prevent additional risks is also explained. This helps managers to make timely decisions to avoid firms’ bankruptcy. Stakeholders of the construction firms can understand firms’ financial sustainability and whether to believe (or not) in the financial information provided by firms. Finally, the government can understand how regulations can be adapted or created to both promote financial information quality and transparency and help firms to recover from financial constraints. This will help to promote the well-being of society as SMEs are an important driver of economic development.

The work fulfilled the proposed aims. However, all works have some limitations. First, the analysis is based on construction firms of a single country, which does not allow for the generalization of results. Future research could be done using different samples to validate results. This work only takes into account accruals quality of the year, although it can have medium-term effects as earnings management usually have reputational impacts one or more years after, so this lag effect could be also addressed in future analysis. Ex-ante and ex-post classifications of default may also be addressed to verify the potential differences.

{kind=link}