FinTech in Latvia: Status Quo, Current Developments, and Challenges Ahead

Abstract

:1. Introduction

2. Data and Methodology

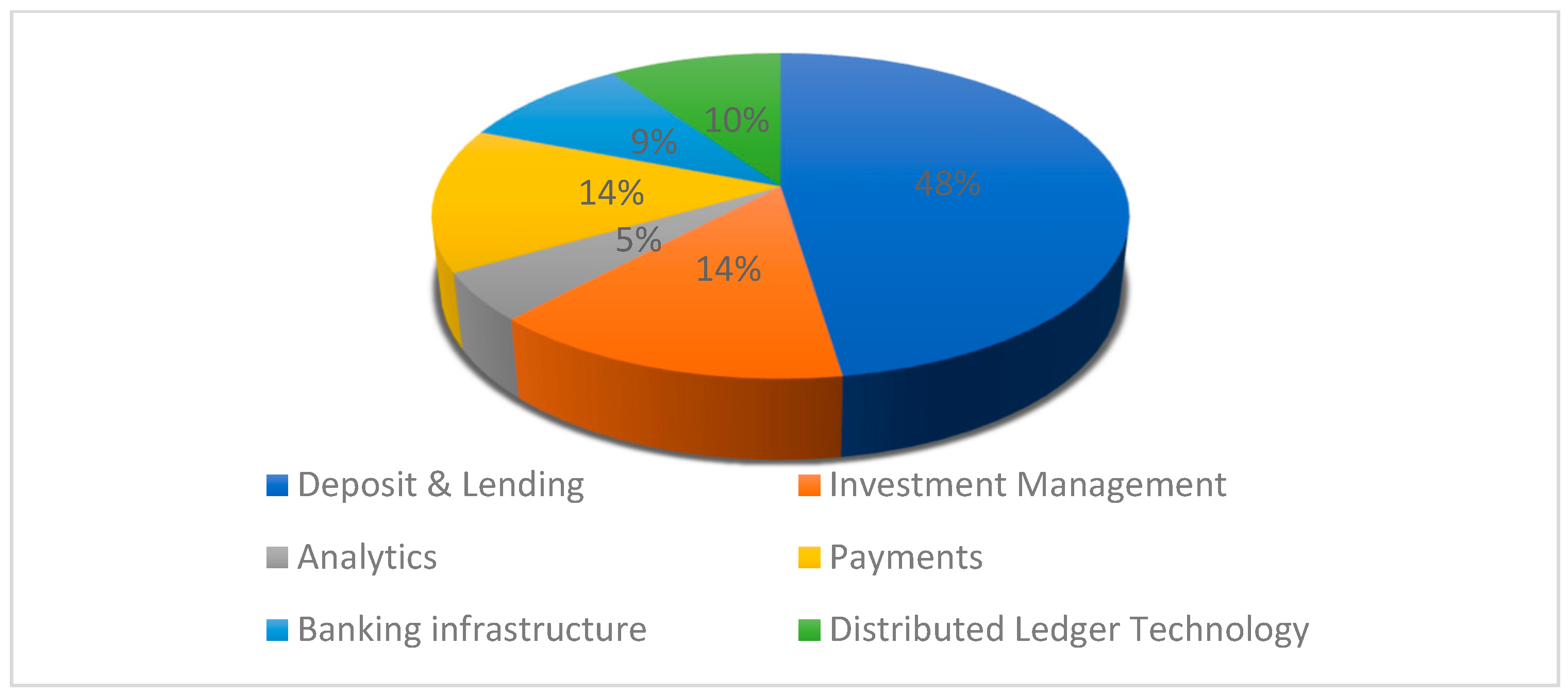

- Analytics—data mining, data (business) analytics, big data analysis, machine learning, artificial intelligence used for automated advice, chatbots, customer relations management, and data handling.

- Banking infrastructure—user interface, processing enhancement, technology infrastructure, various trading platforms, and software companies with a focus on the financial sector.

- Deposit and Lending—crowd investing, crowdlending, invoice trading, and other lending forms such as payday loans.

- Distributed Ledger Technology—cryptocurrency and everything encompassing blockchain technology, even from companies that are payment or crowdfunding companies at the same time.

- Insurance—insurance-related products and services and InsurTech.

- Payments—mobile payments, online payments, money transfers, and anything related to payments.

- Investment management—online investment processes based on algorithms and models, robo-advisors, and social trading.

3. The Latvian FinTech Environment

3.1. Political and Legal Environment

3.1.1. EU Regulatory Framework

3.1.2. Latvian Regulatory Framework

- increased competition, i.e., is the innovative financial service more advantageous, less costly and easier to use than traditional services;

- potential response from traditional market participants, either by improving their service or by adopting the innovative business model;

- access for consumers and non-professional customers to market segments that have traditionally not been available to them.

3.2. Economic Environment

3.3. Social Environment

3.4. Technological Environment

4. Survey Results

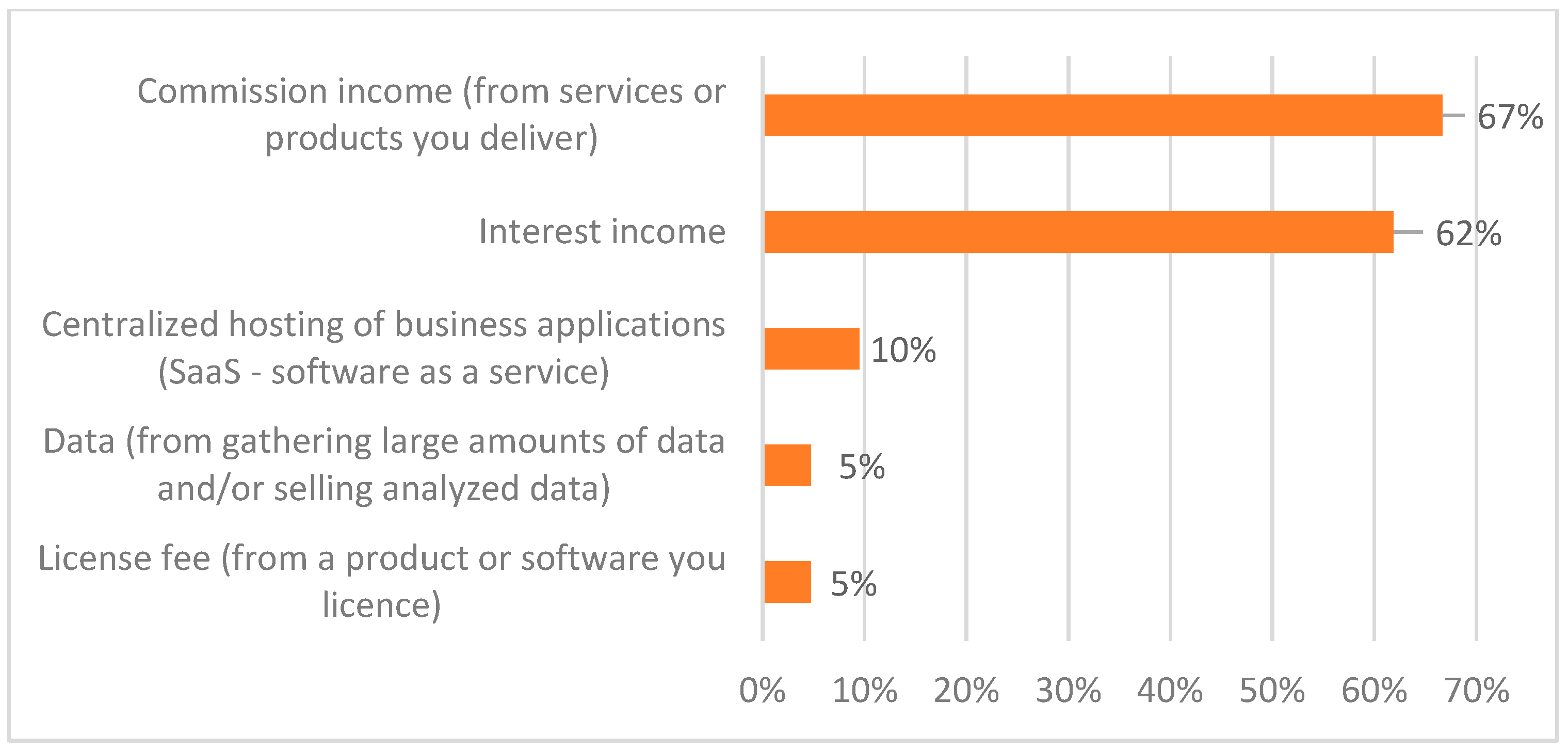

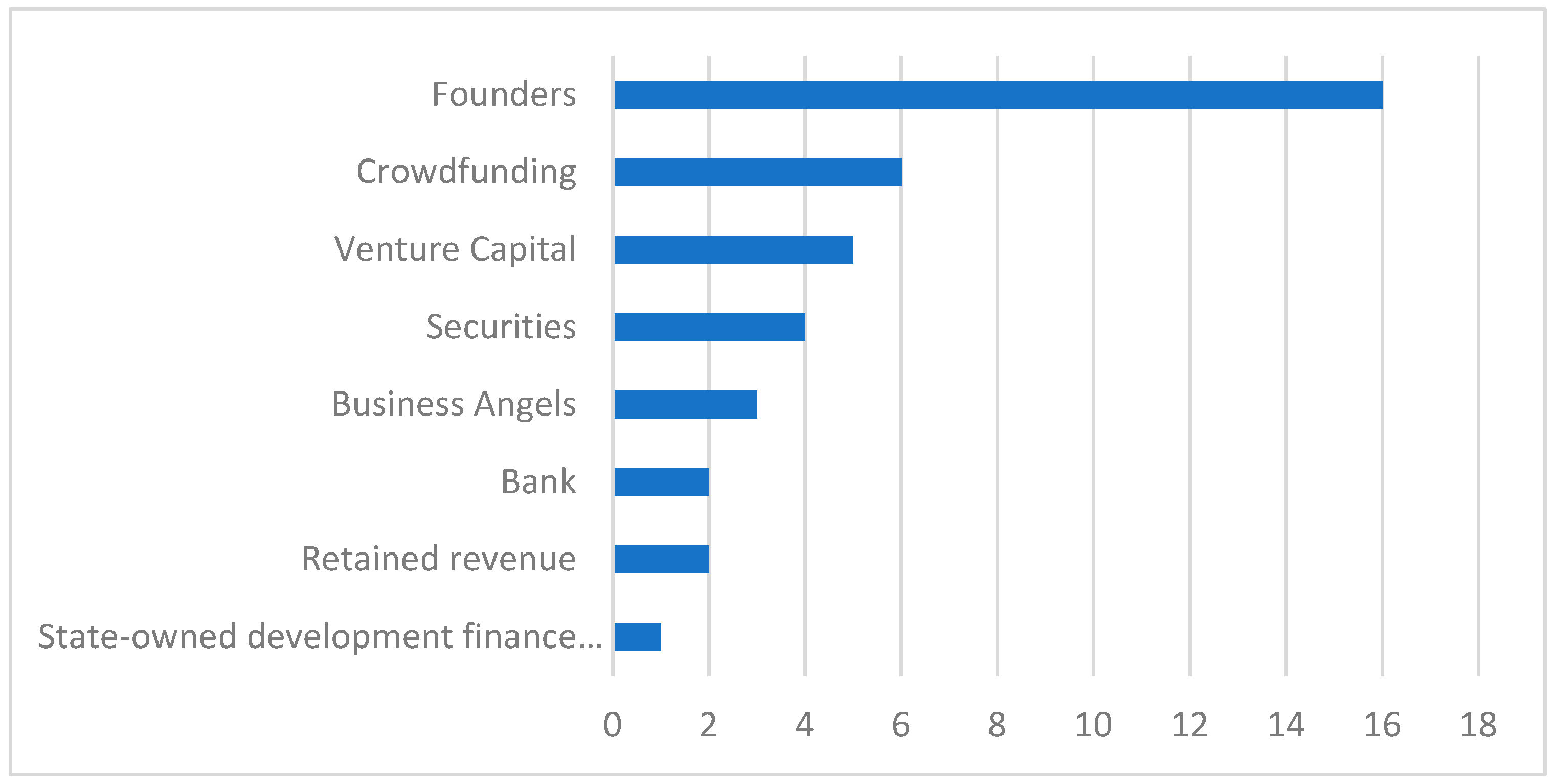

4.1. General Portrait of the Responding FinTech Companies

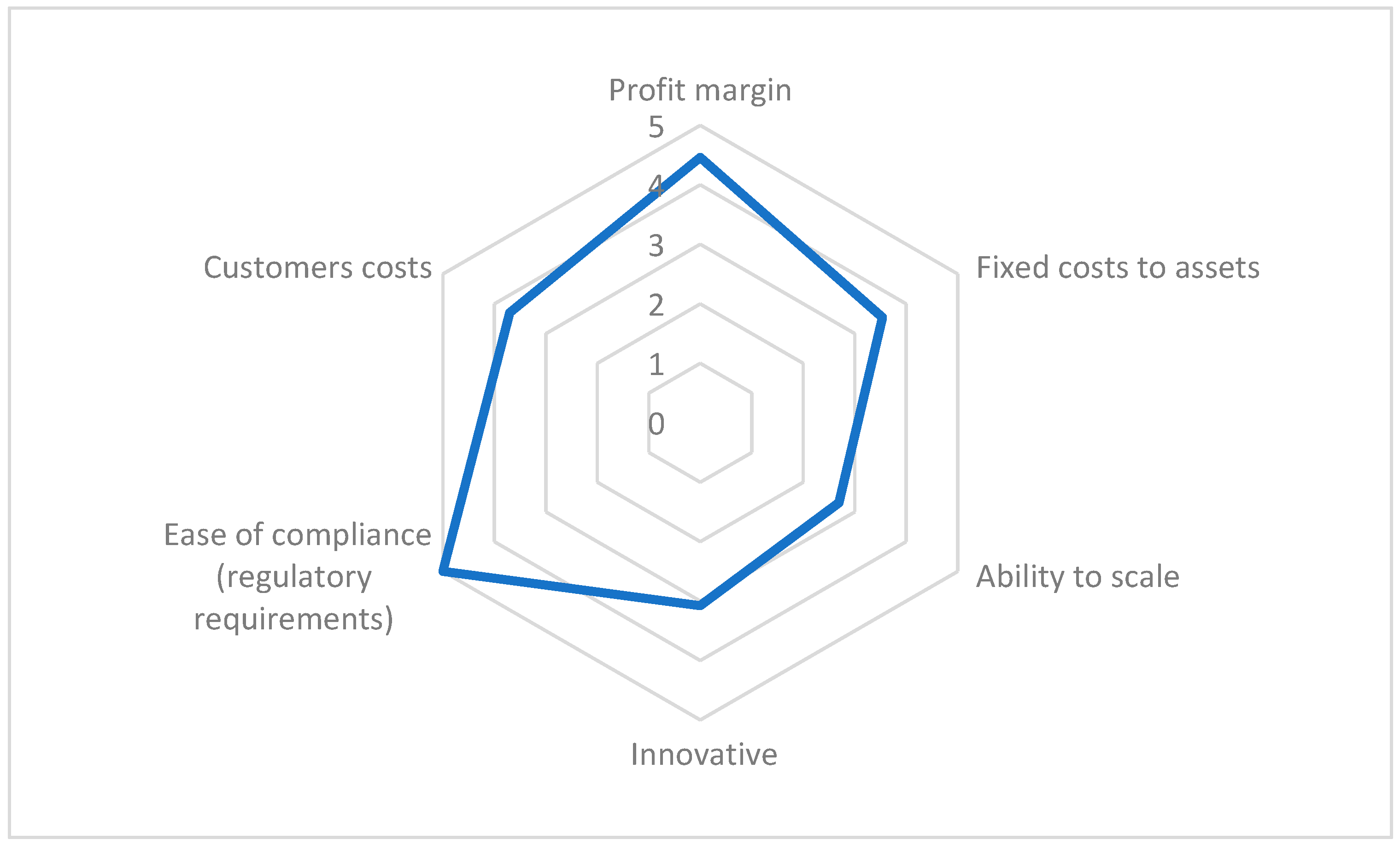

4.2. Assessment of Development Prospects for FinTech Companies

Fintech embraces inclusiveness of financial services within different areas and allows to create targeted solutions for customers to try out without changing their bank. Incumbents have failed in both innovation and communication, thus creating space for new players. As well—payment services directives are a significant trigger for increase of competition.

orThere is no 100% relevant regulation for our specific business.

They try to box all new innovations in existing framework which mostly does not work.

5. Size and Financial Performance of FinTech Companies

6. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | The survey additionally included some questions on the financial situation of the companies and how they evaluate themselves vis à vis competitors. These questions were not considered for the further analysis though, because we decided to collect financial information on survey participants separately for a longer observation period. |

| 2 | Private pension funds are not further considered in the following descriptions due to relatively low relevance in the context of FinTech. |

| 3 | Beyond the regulatory situation described in this section, all financial service providers are subject to the Law on the Prevention of Money Laundering and Terrorism and Proliferation Financing (The Parliament of the Republic of Latvia 2008). The main institutions dedicated to combating money-laundering are the Financial Intelligence Unit of Latvia, FCMC, the State Revenue Service and CRPC. |

| 4 | Combined with potential free FCMC expert advice in PSD2, crowdfunding and/or virtual assets. |

| 5 | Application programming interface. |

References

- Ács, Zoltán J., Szerb László, Esteban Lafuente, and Markus Gábor. 2019. GEI_2019_Final-1. In Global Entrepreneurship Index. Washington, DC: Global Entrepreneurship and Development Institute, pp. 1–71. [Google Scholar] [CrossRef]

- Ankenbrand, Thomas, Andreas Dietrich, and Denis Bieri. 2019. IFZ FinTech Study 2019 An Overview of Swiss FinTech. IFZ FinTech Study. Luzern: Institute of Financial Services Zug IFZ, p. 144. [Google Scholar]

- Bank of Latvia. 2020. FINTECH Glossary. Available online: https://www.bank.lv/en/publications-r/other-publications/fintech-glossary (accessed on 15 June 2021).

- Bureau van Dijk. 2021. Private Company Information—Orbis. Available online: https://www.bvdinfo.com/en-gb/ (accessed on 17 June 2021).

- Cabinet of Ministers. 2011. Regulations Regarding the Special Permit (Licence) for the Provision of Consumer Credit Services; Riga: Cabinet of Ministers.

- Council of Europe. 2019. Anti-Money Laundering and Counter-Terrorist Financing Measures Latvia 1 St Enhanced Follow-Up Report (MONEYVAL). Strasbourg: Council of Europe. [Google Scholar]

- Crunchbase. 2020. Discover Innovative Companies and the People behind Them. Available online: https://www.crunchbase.com/ (accessed on 24 June 2021).

- European Union. 2009. Internet of Things: An Action Plan for Europe. In Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions. Maastricht: European Union. [Google Scholar]

- FCMC. 2021a. FinTech Monitoring. Available online: https://www.fktk.lv/en/licensing/innovation-and-fintech/fintech-monitoring/ (accessed on 27 May 2021).

- FCMC. 2021b. Regulatory Sandbox. Available online: https://www.fktk.lv/en/licensing/innovation-and-fintech/innovation-sandbox/ (accessed on 27 May 2021).

- Filimonova, Irina Viktorovna, Irina Viktorovna Provornaya, Anna V. Komarova, Ekaterina A. Zemnukhova, and Mikhail V. Mishenin. 2020. Influence of Economic Factors on the Environment in Countries with Different Levels of Development. Energy Reports 6: 27–31. [Google Scholar] [CrossRef]

- Financial Action Task Force. 2021. Countries—Latvia. Available online: https://www.fatf-gafi.org/countries/#Latvia (accessed on 22 June 2021).

- Financial Stability Board. 2019. FinTech and Market Structure in Financial Services: Market Developments and Potential Financial Stability Implications—Financial Stability Board. Basel: Financial Stability Board. [Google Scholar]

- Findexable. 2019. The Global Fintech Index 2020. London: Findexable. [Google Scholar]

- FinTech Baltic. 2020. First Ever Latvia Fintech Startup Map Draft Released—Fintech in Baltic. January 27. Available online: https://fintechbaltic.com/1575/fintechlatvia/latvia-fintech-startup-map-2020/ (accessed on 23 June 2021).

- FinTech Baltic. 2021. Latvia Named Top Country with Largest Growth Fintech Interest Since 2020—Fintech in Baltic. Available online: https://fintechbaltic.com/4707/fintechlatvia/latvia-named-top-country-with-largest-growth-fintech-interest-since-2020/ (accessed on 23 June 2021).

- Gomber, Peter, Robert J. Kauffman, Chris Parker, and Bruce W. Weber. 2018. On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services. Journal of Management Information Systems 35: 220–65. [Google Scholar] [CrossRef]

- Hoque, Zahirul. 2004. A Contingency Model of the Association between Strategy, Environmental Uncertainty and Performance Measurement: Impact on Organizational Performance. International Business Review 13: 485–502. [Google Scholar] [CrossRef]

- Horn, Matthias, Andreas Oehler, and Stefan Wendt. 2020. FinTech for Consumers and Retail Investors: Opportunities and Risks of Digital Payment and Investment Services. In Palgrave Studies in Sustainable Business in Association with Future Earth. Cham: Palgrave Macmillan, pp. 309–27. [Google Scholar] [CrossRef]

- IMF. 2019. Fintech: The Experience So Far. IMF Policy Paper 77. Washington, DC: IMF. [Google Scholar]

- Institute for Management Development. 2019. IMD World Talent Ranking 2019. Washington, DC: Institute for Management Development. [Google Scholar]

- Investment and Development Agency of Latvia. 2020. Areas of Activity. Available online: https://www.liaa.gov.lv/en/about-us/areas-activity (accessed on 19 June 2021).

- Ito, Takatoshi, Kenta Yamada, Misako Takayasu, and Hideki Takayasu. 2020. Execution Risk and Arbitrage Opportunities in the Foreign Exchange Markets. Working Paper 26706. Cambridge: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Key Capital. 2020. FinTech Companies in Latvia|Key Capital|Europe. Available online: https://www.keycapital.eu/fintechcompaniesinlatvia (accessed on 15 May 2021).

- Kliber, Agata, Barbara Będowska-Sójka, Aleksandra Rutkowska, and Katarzyna Świerczyńska. 2021. Triggers and Obstacles to the Development of the FinTech Sector in Poland. Risks 9: 30. [Google Scholar] [CrossRef]

- Kluza, Krzysztof, Magdalena Ziolo, and Anna Spoz. 2021. Innovation and Environmental, Social, and Governance Factors Influencing Sustainable Business Models—Meta-Analysis. Journal of Cleaner Production 303: 127015. [Google Scholar] [CrossRef]

- Laidroo, Laivi, Anneliis Tamre, Mari-Liis Kukk, Elina Tasa, and Mari Avarmaa. 2021a. FinTech Report Estonia 2021. Tallinn: Finance Estonia.EU. [Google Scholar] [CrossRef]

- Laidroo, Laivi, Ekaterina Koroleva, Agata Kliber, Ramona Rupeika-Apoga, and Zana Grigaliuniene. 2021b. Business Models of FinTechs—Difference in Similarity? Electronic Commerce Research and Applications 46: 101034. [Google Scholar] [CrossRef]

- Long Finance and Financial Centre Futures. 2020. The Global Financial Centres Index 28. London: Long Finance and Financial Centre Futures. [Google Scholar]

- OECD. 2018. Financial Markets, Insurance and Private Pensions: Digitalisation and Finance. Paris: OECD. [Google Scholar]

- Oehler, Andreas, and Stefan Wendt. 2018. Trust and Financial Services: The Impact of Increasing Digitalisation and the Financial Crisis. In The Return of Trust? Institutions and the Public after the Icelandic Financial Crisis. Bingley: Emerald Publishing Limited, pp. 195–211. [Google Scholar] [CrossRef]

- Oehler, Andreas, Matthias Horn, and Stefan Wendt. 2021. Investor Characteristics and Their Impact on the Decision to Use a Robo-Advisor. Journal of Financial Services Research. forthcoming. [Google Scholar]

- Olson, Eric M., and Stanley F. Slater. 2002. The Balanced Scorecard, Competitive Strategy, and Performance. Business Horizons 45: 11–16. [Google Scholar] [CrossRef]

- Rikhardsson, Pall, Stefan Wendt, Auður Arna Arnardóttir, and Throstur Olaf Sigurjónsson. 2020. Is More Really Better? Performance Measure Variety and Environmental Uncertainty. International Journal of Productivity and Performance Management 70: 1446–69. [Google Scholar] [CrossRef]

- Rupeika-Apoga, Ramona, and Eleftherios Thalassinos. 2020. Ideas for a Regulatory Definition of FinTech. International Journal of Economics and Business Administration 8: 136–54. [Google Scholar] [CrossRef] [Green Version]

- Rupeika-Apoga, Ramona, and Roberts Nedovis. 2016. The Foreign Exchange Exposure of Domestic Companies in Eurozone: Case of the Baltic States. European Research Studies Journal 19: 165–78. [Google Scholar] [CrossRef]

- Rupeika-Apoga, Ramona, and Svetlana Saksonova. 2018. SMEs’ Alternative Financing: The Case of Latvia. European Research Studies Journal 21: 43–52. [Google Scholar] [CrossRef]

- Saksonova, Svetlana, and Oksana Koļeda. 2017. Evaluating the Interrelationship between Actions of Latvian Commercial Banks and Latvian Economic Growth. Procedia Engineering 178: 123–30. [Google Scholar] [CrossRef]

- Saksonova, Svetlana. 2014. Foreign Direct Investment Attraction in the Baltic States. Journal: Business: Theory and Practice 15: 114–20. [Google Scholar] [CrossRef] [Green Version]

- Sammut-Bonnici, Tanya, and David Galea. 2015. PEST Analysis. In Wiley Encyclopedia of Management. Hoboken: John Wiley & Sons, Ltd. [Google Scholar] [CrossRef]

- Solovjova, Irina, Ramona Rupeika-Apoga, and Inna Romānova. 2018. Competitiveness Enhancement of International Financial Centres. European Research Studies Journal 21: 5–17. [Google Scholar] [CrossRef]

- Swedbank. 2020. Latvian Fintech Report 2020. Gothenburg: Swedbank. [Google Scholar]

- The Alternative Financial Services Association of Latvia. 2021. Members. Available online: https://www.lafpa.lv/en/about-us/members/ (accessed on 12 July 2021).

- The European Commission. 2018. FinTech Action Plan: For a more Competitive and Innovative European Financial Sector EN. Brussels: The European Commission. [Google Scholar]

- The European Commission. 2019. Commission Delegated Regulation (EU) 2019/980. Official Journal of the European Union L 166/26. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32019R0980 (accessed on 12 July 2021).

- The European Parliament and of the Council. 2014. Directive 2014/65/EU of the European Parliament and of the Council. Official Journal of the European Union L 173/349. Available online: http://data.europa.eu/eli/dir/2014/65/oj (accessed on 12 July 2021).

- The European Parliament and of the Council. 2015. Directive (EU) 2015/2366 of the European Parliament and of the Council of 25 November 2015 on Payment Services in the Internal Market, Amending Directives 2002/65/EC, 2009/110/EC and 2013/36/EU and Regulation (EU) No 1093/2010, and Repealing Directive 200. Official Journal of the European Union L 337/35. Available online: http://data.europa.eu/eli/dir/2015/2366/oj (accessed on 12 July 2021).

- The European Parliament and of the Council. 2018. Directive (EU) 2018/843 of the European Parliament and of the Council. Official Journal of the European Union L 156/43. Available online: http://data.europa.eu/eli/dir/2018/843/oj (accessed on 12 July 2021).

- The European Parliament and of the Council. 2019a. DIRECTIVE (EU) 2019/2034 on the Prudential Supervision of Investment Firms and Amending Directives 2002/87/EC, 2009/65/EC, 2011/61/EU, 2013/36/EU, 2014/59/EU and 2014/65/EU. Official Journal of the European Union. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32019L2034 (accessed on 19 July 2021).

- The European Parliament and of the Council. 2019b. EUR-Lex—32019L2034—EN—EUR-Lex. Official Journal of the European Union L 314/64. Available online: http://data.europa.eu/eli/dir/2019/2034/oj (accessed on 12 July 2021).

- The European Parliament and of the Council. 2019c. REGULATION (EU) 2019/2033 on the Prudential Requirements of Investment Firms and Amending Regulations (EU) No 1093/2010, (EU) No 575/2013, (EU) No 600/2014 and (EU) No 806/2014. Official Journal of the European Union L 314/1. Available online: http://data.europa.eu/eli/reg/2019/2033/oj (accessed on 15 July 2021).

- The European Parliament and of the Council. 2020. REGULATION (EU) 2020/1503 of The European Parliament and of The Council of 7 October 2020 on European Crowdfunding Service Providers for Business. Official Journal of the European Union L 347/1. Available online: http://data.europa.eu/eli/reg/2020/1503/oj (accessed on 19 July 2021).

- The European Parliament. 2017. Report on FinTech: The Influence of Technology on the Future of the Financial Sector (2016/2243(INI)). A8-0176/2017. Brussels: The European Parliament. [Google Scholar] [CrossRef]

- The Financial and Capital Market Commission. 2002. Regulations on the Issue of Credit Institution and Credit Union Operating Licences. Riga: The Financial and Capital Market Commission. [Google Scholar]

- The Parliament of the Republic of Latvia. 1997. Law on the Investment Management Companies; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 1999. Consumer Rights Protection Law; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 2000. Commercial Law; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 2001a. Credit Union Law; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 2001b. Investor Protection Law; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 2003. Law on the Financial Instruments Market; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 2004. Compulsory Civil Liability Insurance of Owners of Motor Vehicles Law; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 2008. The Law on the Prevention of Money Laundering and Terrorism and Proliferation Financing. Riga: Latvijas Vestnesis. [Google Scholar]

- The Parliament of the Republic of Latvia. 2010. The Law on Payment Services and Electronic Money; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 2013. Law on Alternative Investment Funds and Their Managers; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 2015a. Deposit Guarantee Law; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 2015b. Law on Insurance and Reinsurance; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 2017. Law on the Recovery and Resolution of Credit Institutions and Investment Firms; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 2018. The Insurance Contract Law; Riga: The Parliament of the Republic of Latvia.

- The Parliament of the Republic of Latvia. 2019. The Insurance and Reinsurance Distribution Law; Riga: The Parliament of the Republic of Latvia.

- Tirmaste, Kersti, Liina Voolma, Laivi Laidroo, Mari-Liis Kukk, and Mari Avarmaa. 2019. FinTech Report Estonia 2019. Tallinn: Finance Estonia.EU. [Google Scholar] [CrossRef]

- World Bank Group. 2020. Doing Business 2020: Comparing Business Regulation in 190 Economies. Washington, DC: World Bank Group. [Google Scholar] [CrossRef] [Green Version]

- World Economic Forum. 2019. The Global Competitiveness Report 2019. Cologny: World Economic Forum. [Google Scholar] [CrossRef]

- World Economic Forum. 2020. The Europe 2020 Competitiveness Report: Building a More Competitive Europe. Cologny: World Economic Forum. [Google Scholar]

- Yeandle, Mark, and Michael Mainelli. 2015. The Global Financial Centres Index 17. The Global Finance Centres Index (GFCI)—Long Finance, 2015. Available online: https://ssrn.com/abstract=3671501 (accessed on 9 July 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Response Items | Number of Responses |

|---|---|

| Pre-defined items | |

| Traditional banks will adopt new technologies, modernize and digitalize. | 16 |

| Traditional banks will not survive and will be replaced by new technology-driven banks. | 3 |

| FinTech companies will be partners of traditional banks. | 19 |

| Traditional banks will become commoditized service providers, leaving customer ownership to FinTech companies. | 9 |

| Traditional banks will become irrelevant as customers interact directly with individual financial services providers (FinTech). | 1 |

| Other responses | |

| Traditional banks will not save retail and SME business. | 1 |

| Situation will vary from market to market, thus so many scenarios are selected. | 1 |

| Level of How Pressing | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | N | Median |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Number of responses to predefined items | ||||||||||||

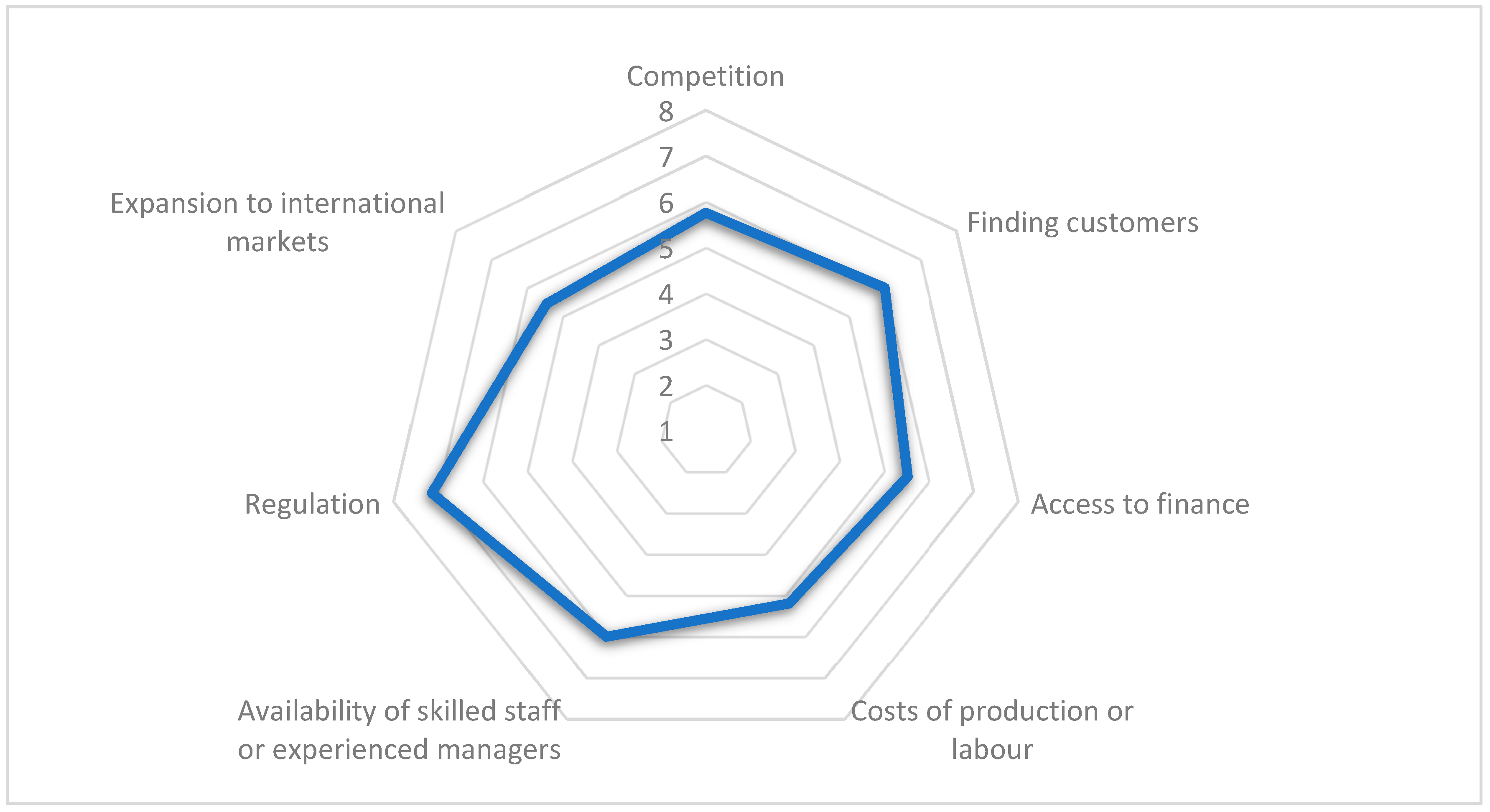

| Competition | 2 | 0 | 1 | 2 | 2 | 6 | 5 | 1 | 1 | 1 | 21 | 6 |

| Finding customers | 0 | 1 | 3 | 1 | 2 | 4 | 5 | 3 | 2 | 0 | 21 | 6 |

| Access to finance | 2 | 2 | 3 | 1 | 1 | 2 | 5 | 2 | 1 | 2 | 21 | 6 |

| Cost of production or labour | 0 | 0 | 6 | 2 | 4 | 4 | 2 | 2 | 1 | 0 | 21 | 5 |

| Availability of skilled staff or experienced managers | 0 | 0 | 5 | 1 | 2 | 2 | 4 | 6 | 1 | 0 | 21 | 7 |

| Regulation | 0 | 1 | 3 | 0 | 2 | 1 | 0 | 6 | 5 | 3 | 21 | 8 |

| Expansion to international markets | 0 | 1 | 3 | 4 | 3 | 2 | 3 | 3 | 0 | 1 | 20 | 5 |

| Other | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 |

| Response Items | Number of Responses |

|---|---|

| Predefined items | |

| Special regulations. | 16 |

| Regulatory sandboxes. | 11 |

| Tax relief. | 7 |

| Other responses | |

| Mostly none. | 1 |

| Response Items | Number of Responses |

|---|---|

| Predefined items | |

| State Revenue Service | 12 |

| Financial and Capital Market Commission | 11 |

| Bank of Latvia | 1 |

| Other responses | |

| PTAC/Consumer Rights Protection Center | 9 |

| VARAM (Ministry of Environmental Protection and Regional Development) | 1 |

| Ministry of Economics | 1 |

| LIAA (Investment and Development Agency) | 1 |

| Municipalities | 1 |

| None | 1 |

| “We are trying to avoid communication with state authorities without necessity. Usually officials in Latvia are very conservative and they are not ready to help young entrepreneurs” | 1 |

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Panel A: Number of employees | ||||||||||

| Mean | 6 | 14 | 18 | 32 | 33 | 39 | 43 | 46 | 47 | 46 |

| St. Dev. | 6 | 17 | 25 | 57 | 67 | 70 | 80 | 74 | 70 | 64 |

| Median | 5 | 8 | 9 | 14 | 11 | 14 | 20 | 24 | 24 | 26 |

| Min | 1 | 0 | 1 | 1 | 1 | 3 | 3 | 1 | 3 | 2 |

| Max | 18 | 56 | 86 | 200 | 243 | 260 | 322 | 311 | 295 | 266 |

| N | 6 | 8 | 9 | 10 | 11 | 12 | 14 | 15 | 15 | 16 |

| Panel B: Turnover in thousand USD | ||||||||||

| Mean | 528 | 3953 | 7710 | 12,571 | 9773 | 9623 | 8306 | 8852 | 10,589 | 9213 |

| St. Dev. | 266 | 6978 | 15,712 | 28,498 | 22,360 | 22,037 | 11,798 | 11,417 | 13,233 | 10,733 |

| Median | 703 | 787 | 926 | 2698 | 1822 | 3078 | 1910 | 2586 | 5121 | 4069 |

| Min | 105 | 103 | 82 | 89 | 247 | 3 | 1 | 8 | 32 | 101 |

| Max | 761 | 20,920 | 48,959 | 92,909 | 76,504 | 85,168 | 39,230 | 36,770 | 42,509 | 30,354 |

| N | 5 | 7 | 8 | 9 | 10 | 13 | 16 | 17 | 17 | 18 |

| Panel C: Total assets in thousand USD | ||||||||||

| Mean | 776 | 4622 | 16,548 | 30,970 | 27,527 | 21,734 | 21,029 | 24,150 | 21,153 | 19,252 |

| St. Dev. | 605 | 8122 | 40,316 | 76,071 | 78,379 | 51,725 | 42,655 | 46,834 | 36,511 | 30,893 |

| Median | 585 | 1736 | 2141 | 2980 | 1675 | 3201 | 3450 | 4093 | 2549 | 3677 |

| Min | 181 | 270 | 374 | 861 | 55 | 162 | 43 | 141 | 368 | 595 |

| Max | 2050 | 25,912 | 130,451 | 245,895 | 297,402 | 204,791 | 176,417 | 195,143 | 149,172 | 124,631 |

| N | 6 | 8 | 9 | 9 | 13 | 14 | 16 | 17 | 18 | 19 |

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Panel A: Return on Equity in percent | ||||||||||

| Mean | 77.8 | 51.9 | 2.1 | 20.0 | 2.8 | −11.2 | 20.2 | 2.2 | 9.9 | 26.6 |

| St. Dev. | 65.6 | 24.6 | 83.7 | 38.5 | 36.7 | 64.4 | 77.5 | 107.5 | 180.8 | 38.3 |

| Median | 77.8 | 58.7 | 15.6 | 14.3 | 13.5 | −4.9 | 3.7 | 38.7 | 26.6 | 25.5 |

| Min | 12.2 | 12.6 | −177.7 | −36.6 | −60.3 | −128.7 | −123.4 | −330.7 | −555.1 | −72.4 |

| Max | 143.4 | 81.7 | 107.8 | 74.8 | 48.6 | 100.0 | 199.0 | 93.8 | 410.5 | 99.4 |

| N | 2 | 5 | 8 | 8 | 11 | 11 | 11 | 12 | 15 | 14 |

| Panel B: Profit margin in percent | ||||||||||

| Mean | 2.7 | 36.1 | 15.4 | 2.1 | 3.8 | 11.3 | 9.4 | 4.4 | 19.9 | 8.5 |

| St. Dev. | 43.9 | 16.4 | 22.7 | 27.9 | 29.0 | 20.8 | 42.3 | 25.3 | 25.6 | 40.9 |

| Median | 22.6 | 42.0 | 12.4 | 2.1 | 9.3 | 5.5 | 2.1 | 0.8 | 15.2 | 13.2 |

| Min | −71.7 | 3.3 | −28.4 | −41.6 | −59.5 | −15.3 | −79.4 | −40.6 | −25.4 | −71.4 |

| Max | 37.2 | 56.2 | 53.1 | 45.9 | 38.5 | 44.4 | 93.1 | 50.2 | 91.5 | 95.4 |

| N | 4 | 7 | 7 | 9 | 8 | 10 | 12 | 13 | 14 | 16 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rupeika-Apoga, R.; Wendt, S. FinTech in Latvia: Status Quo, Current Developments, and Challenges Ahead. Risks 2021, 9, 181. https://doi.org/10.3390/risks9100181

Rupeika-Apoga R, Wendt S. FinTech in Latvia: Status Quo, Current Developments, and Challenges Ahead. Risks. 2021; 9(10):181. https://doi.org/10.3390/risks9100181

Chicago/Turabian StyleRupeika-Apoga, Ramona, and Stefan Wendt. 2021. "FinTech in Latvia: Status Quo, Current Developments, and Challenges Ahead" Risks 9, no. 10: 181. https://doi.org/10.3390/risks9100181

APA StyleRupeika-Apoga, R., & Wendt, S. (2021). FinTech in Latvia: Status Quo, Current Developments, and Challenges Ahead. Risks, 9(10), 181. https://doi.org/10.3390/risks9100181