Risk-Based Approach for Selecting Company Key Performance Indicator in an Example of Financial Services

Abstract

:1. Introduction

2. Materials and Methods

- Governance Risks—The risk that the company’s rules, processes, and mechanisms, important for oversighting and decision making, function improperly. Governance risks relate to the directors’ decisions regarding board leadership, composition, and structure. Governance risks are associated with the resourcefulness and robustness of the company’s procedures for compliance with the relevant framework of laws, including the quality of reporting lines [23].

- Human Resources Risks—The risks that human resources pose on the company’s operations [34].

- Health and Safety Risks—The risk of the company being exposed to a health and safety hazard that may result in harm, injury, death, or illness of an employee in a specific workplace [35].

- Financial Risks—The risk a company may face that results in the possibility of losing money on an investment or business project [36].

- Cyber Risks—This risk includes hardware and software failures, spam, viruses, malicious attacks, and other ICT matters [37].

- Capital Adequacy Risks—Risks arising from the firm’s capital position, the adequacy of capital to support the level of current and anticipated business activities, and the access to further capital [38].

- Environmental/External Risks—Risks arising from economic events that are out of the control of the corporate structure [39].

- Law and Regulation Risks—The risk that the firm suffers financial, reputational, or litigation damage through failure to monitor, control, and eliminate or substantially reduce regulatory compliance risk [40].

- Strategic Risks—The risk of loss arising from adverse business decisions that are poorly aligned to strategic goals, failed execution of policies and processes designed to meet those goals, and inability to respond to macroeconomic and industry dynamics. Strategic risks are also those risks associated with operating in a specific industry [41].

- Financial Crime Risks—The risks that arise from the failure to prevent financial crime, money laundering, and market abuse [42].

2.1. Risk, Threats and Vulnerabilities

2.2. Methods

- The respondent is a company registered in the European Union;

- The company is regulated or supervised by the financial company supervisor;

- The company has a risk management department or risk professionals;

- The company is involved in the payment business;

- Each risk event represents a threat or series of threats that exposes a company’s current vulnerabilities. The proper values of the vulnerabilities must be used to evaluate the threat impact or likelihood of the risk event.

2.2.1. Risk Calculation

- IR—inherent risk;

- Im—the impact of the risk;

- L—the likelihood of the risk.

- Im—the impact of the risk;

- Tii—threat impact per each of the threats within the risk group;

- Vi—vulnerabilities impact;

- m—number of vulnerabilities per risk group;

- n—number of threats per risk group.

- L—the likelihood of the risk;

- Tli—threat likelihood per each of the threats within the risk group;

- Vl—vulnerabilities likelihood;

- m—number of vulnerabilities per risk group;

- n—number of threats per risk group.

- Governance risk;

- ICT risk;

- Operational risk;

- Financial crime risk;

- Human resources risk.

2.2.2. Model Estimation Using the SmartPLS Software

- The validity of the outer paradigm or construct was assessed. The research included looking into the indicator loadings for the theoretically determined constructs and evaluating the model’s validity and dependability. Additionally, it was established how many iterations would be necessary for SmartPLS to finish the evaluation.

- The inner model (structural model) assessed how the categories related to one another. The coefficient of determination (R2), standardized path coefficients (B), and impact size (f2) were used to accomplish this.

- A broad evaluation of the model (overall model evaluation) was conducted to determine how well the model fits the data. This can be accomplished in SmartPLS by applying the SRM exact fit parameters.

3. Results

3.1. Preliminary Research

- Banks (credit institutions) pay the government for funds that serve as guarantees for the customer deposits that they take. The government will use these funds to reimburse the customer funds in case of the bank’s bankruptcy. As a result, the only factor affecting capital adequacy is the liquidity of bank funds [69].

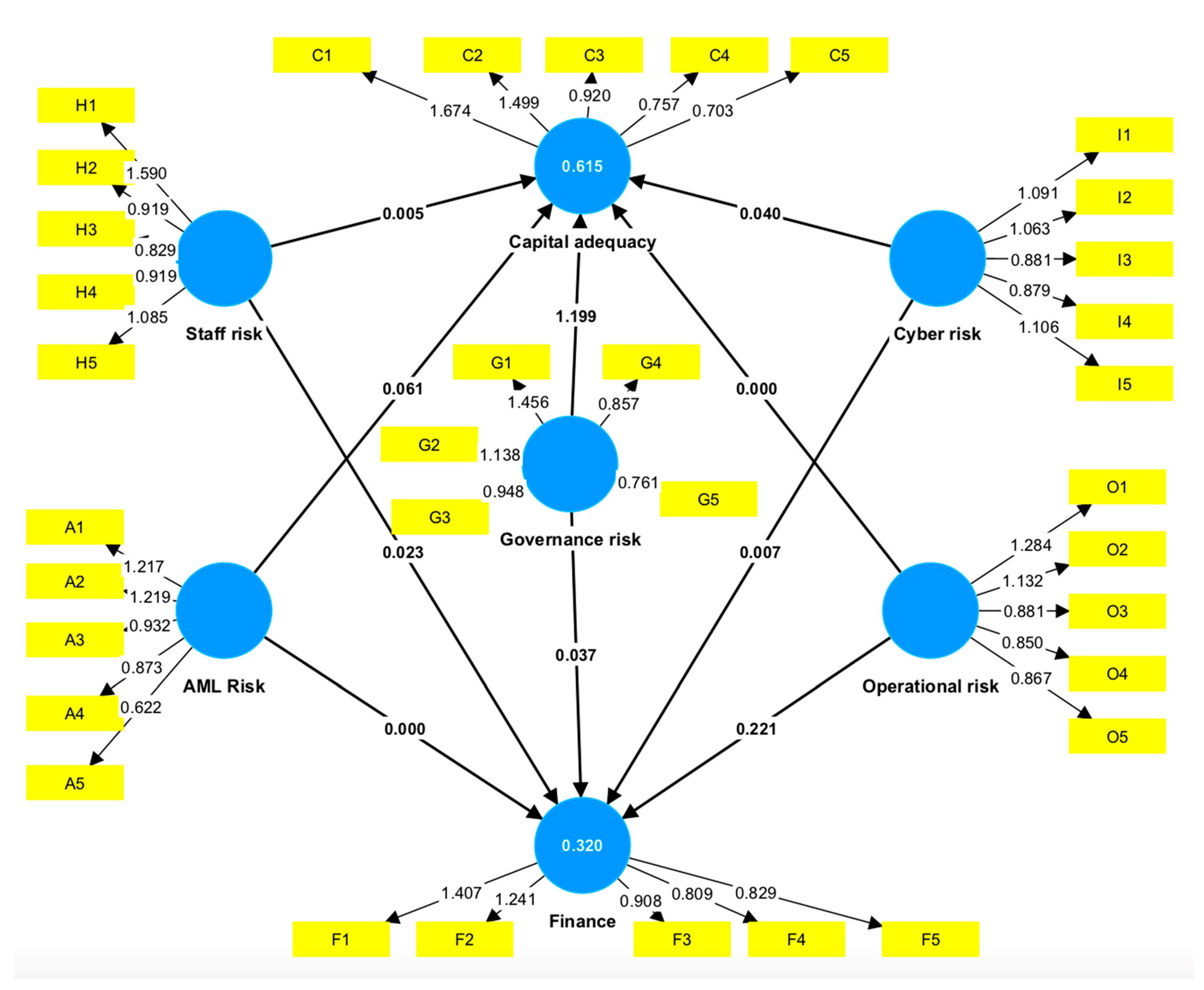

3.2. Outer Model Evaluation—Construct Validity

3.3. Evaluation of the Inner Model (Structural Model). Verifying the Hypotheses

3.4. Overall Model Assessment

4. Discussion

Research Limitations

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Threat Group | Threat | Governance Risks | Operational Risks | Human Resources Risks | Financial Risks | ICT Risks | Capital Adequacy Risks | Financial Crime Risks |

|---|---|---|---|---|---|---|---|---|

| 1 Ecosystem pollution | Air pollution | X | X | |||||

| 2 Ecosystem pollution | Environmental accidents | X | X | |||||

| 3 Extreme weather events | Earthquake | X | X | |||||

| 4 Extreme weather events | Flooding | X | X | |||||

| 5 Extreme weather events | Hurricane | X | X | |||||

| 6 Extreme weather events | Lightning | X | X | |||||

| 7 Extreme weather events | Heat waves | X | X | |||||

| 8 Extreme weather events | Fire | X | X | |||||

| 9 Ecosystem pollution | Water scarcity—Lack or insufficient supply of water | X | X | |||||

| 10 Market risk | Public policy change—Pollution control regulations | X | ||||||

| 11 Market risk | Shifting sentiment—Changes in consumer preference for certain products | X | ||||||

| 12 Remote work | Pandemic | X | X | X | X | X | ||

| 13 Company culture | Harassment | X | ||||||

| 14 Company culture | Discrimination | X | ||||||

| 15 Company culture | Eavesdropping | X | X | |||||

| 16 Humane resource | Illegal import/export of software | X | X | X | ||||

| 17 Humane resource | Illegal use of software | X | X | X | ||||

| 18 Humane resource | Maintenance error | X | X | X | ||||

| 19 Humane resource | Misuse of resources | X | X | X | ||||

| 20 Humane resource | Operational support staff error | X | X | X | X | |||

| 21 Humane resource | Staff shortage | X | X | X | X | |||

| 22 Humane resource | Staff mistakes | X | X | X | X | X | X | |

| 23 Manipulated data | Malware | X | X | X | ||||

| 24 Supply | Use of software in an unauthorized way | X | ||||||

| 25 Manipulated data | Communications infiltration | X | ||||||

| 26 Manipulated data | Misrouting or rerouting of messages | X | X | X | ||||

| 27 Manipulated data | Unauthorized use of software | X | ||||||

| 28 Manipulated data | Unauthorized use of storage media | X | ||||||

| 29 Manipulated data | Willful damage | X | X | X | X | X | ||

| 30 Remote work | Masquerading of user identity | X | X | |||||

| 31 Remote work | Network access by unauthorized persons | X | X | |||||

| 32 Remote work | Repudiation (e.g., of services, transactions, sending/receiving messages) | X | X | |||||

| 33 Remote work | Use of software by unauthorized users | X | ||||||

| 34 Communication | Damage to communication lines/cables | X | X | X | ||||

| 35 Communication | Failure of communications services | X | X | |||||

| 36 Communication | Failure of network components | X | ||||||

| 37 Communication | Traffic overloading | X | ||||||

| 38 Communication | Transmission errors | X | ||||||

| 39 Communication | Use of network facilities in an unauthorized way | X | ||||||

| 40 Hardware | Air conditioning failure | X | X | X | X | |||

| 41 Hardware | Bomb attack | X | X | X | ||||

| 42 Hardware | Deterioration of storage media | X | X | X | ||||

| 43 Hardware | Hardware failure | X | ||||||

| 44 Hardware | Industrial action | X | ||||||

| 45 Hardware | Theft | X | X | X | X | X | X | |

| 46 Supply | Failure of power supply | X | ||||||

| 47 Supply | Power fluctuation | X | ||||||

| 48 Supply | Software failure | X | X | X | X | X | X | X |

| 49 Customer-related threats—Customer | Client works in high-risk sector | X | ||||||

| 50 Customer-related threats—Customer | UBO of the company works in high-risk sector | X | ||||||

| 51 Customer-related threats—Customer | Representative of the private individual works in high-risk sector | X | ||||||

| 52 Customer-related threats—Customer | Client family member of politically exposed person | X | ||||||

| 53 Customer-related threats—Customer | UBO family member of politically exposed person | X | ||||||

| 54 Customer-related threats—Customer | Client representative family member of politically exposed person | X | ||||||

| 55 Customer-related threats—Customer | Client representative associated to politically exposed person | X | ||||||

| 56 Customer-related threats—Customer | Client associated to politically exposed person | X | ||||||

| 57 Customer-related threats—Customer | Client representative politically exposed person | X | ||||||

| 58 Customer-related threats—Customer | Client foreign politically exposed person | X | ||||||

| 59 Customer-related threats—Customer | UBO foreign politically exposed person | X | ||||||

| 60 Customer-related threats—Customer | Client representative foreign politically exposed person | X | ||||||

| 61 Customer-related threats—Customer | Client domestical politically exposed person (PEP) | X | ||||||

| 62 Customer-related threats—Customer | UBO domestical politically exposed person (PEP) | X | ||||||

| 63 Customer-related threats—Customer | Client representative domestical politically exposed person (PEP) | X | ||||||

| 64 Customer-related threats—Customer | Company incorporation type | X | ||||||

| 65 Customer-related threats—Customer | Concealment of beneficial ownership | X | ||||||

| 66 Customer-related threats—Customer | Shell company | X | ||||||

| 67 Customer-related threats—Customer | Shell bank | X | ||||||

| 68 Customer-related threats—Transactions | High turnover | X | ||||||

| 69 Customer-related threats—Customer | Reliable bad adverse media | X | ||||||

| 70 Customer-related threats—Customer | Non-reliable bad adverse media | X | ||||||

| 71 Customer-related threats—Customer | Received request to freeze customer’s UBO (FIAU, MFSA, police, court, etc.) | X | X | X | X | |||

| 72 Customer-related threats—Customer | Received request to freeze customer’s UBO (FIAU, MFSA, police, court, etc.) | X | X | X | X | |||

| 73 Customer-related threats—Transactions | Received request to monitor customer’s transaction (FIAU); | X | X | X | X | |||

| 74 Customer-related threats—Transactions | Information request (FIAU, MFSA, police, court) | X | X | |||||

| 75 Customer-related threats—Transactions | STR/STA submitted regarding the customer or their UBO; | X | X | |||||

| 76 Customer-related threats—Transactions | STR/STA submitted regarding the customer’s UBO; | X | X | |||||

| 77 Customer-related threats—Customer | Customer in the terrorist list | X | X | X | X | |||

| 78 Customer-related threats—Customer | Customer UBO in the terrorist list | X | X | X | X | |||

| 79 Customer-related threats—Customer | Customer representative in the terrorist list | X | X | X | X | |||

| 80 Customer-related threats—Customer | Sanctions on the customer | X | X | X | ||||

| 81 Customer-related threats—Customer | Sanctions on the customer shareholders or UBOs | X | X | X | ||||

| 82 Customer-related threats—Customer | Sanctions on the customer representative | X | X | X | ||||

| 83 Customer-related threats—Customer | Identity fraud | X | X | X | ||||

| 84 Customer-related threats—Customer | Non-identified parties account usage | X | ||||||

| 85 Customer-related threats—Customer | False/incorrect personal data | X | ||||||

| 86 Customer-related threats—Customer | False/incorrect personal data of UBO, or authorized/representative persons. | X | ||||||

| 87 Customer-related threats—Customer | False/incorrect personal data of customer representative | X | ||||||

| 88 Customer-related threats—Customer | Customer issue bearer shares | X | ||||||

| 89 Customer-related threats—Customer | Complex ownership structure and opaque business structures (e.g., non-transparent, with several layers) | X | ||||||

| 90 Customer-related threats—Transactions | Tax evasion | X | ||||||

| 91 Customer-related threats—Transactions | Local criminal groups | X | ||||||

| 92 Customer-related threats—Transactions | Drug trafficking | X | ||||||

| 93 Customer-related threats—Transactions | Fraud and misappropriation | X | ||||||

| 94 Customer-related threats—Transactions | Corruption and bribery | X | ||||||

| 95 Customer-related threats—Transactions | Smuggling | X | ||||||

| 96 Customer-related threats—Transactions | Theft and receipt of stolen goods | X | ||||||

| 97 Customer-related threats—Transactions | Armed robbery | X | ||||||

| 98 Customer-related threats—Transactions | Living on the earnings of prostitution | X | ||||||

| 99 Customer-related threats—Transactions | Usury | X | ||||||

| 100 Customer-related threats—Transactions | Illegal gambling and violations of the Gaming Act | X | ||||||

| 101 Customer-related threats—Transactions | Human trafficking | X | ||||||

| 102 Customer-related threats—Transactions | Arms trafficking | X | ||||||

| 103 Customer-related threats—Transactions | Smuggling of persons | X | ||||||

| 104 Customer-related threats—Transactions | Unlicensed financial services | X | ||||||

| 105 Customer-related threats—Transactions | Terrorism and terrorist financing—Raising funds from criminal activities | X | ||||||

| 106 Customer-related threats—Transactions | Terrorism and terrorist financing—Raising funds from legal activity | X | ||||||

| 107 Customer-related threats—Transactions | Sexual exploitation, including sexual exploitation of children | X | ||||||

| 108 Customer-related threats—Transactions | Counterfeiting currency | X | ||||||

| 109 Customer-related threats—Transactions | Environmental crime (illegal fishing, logging, dumping, mining, constrictions) | X | ||||||

| 110 Customer-related threats—Transactions | Murder, grievous bodily injury | X | ||||||

| 111 Customer-related threats—Transactions | Counterfeiting and piracy of products | X | ||||||

| 112 Customer-related threats—Transactions | Kidnapping, illegal restraint, and hostage taking | X | ||||||

| 113 Customer-related threats—Transactions | Extortion | X | ||||||

| 114 Customer-related threats—Transactions | Forgery | X | ||||||

| 115 Customer-related threats—Transactions | Piracy (i.e., maritime) | X | ||||||

| 116 Customer-related threats—Transactions | Insider trading and market manipulation | X | ||||||

| 117 Customer-related threats—Transactions | Unauthorized (unlicensed) commercial activity | X | ||||||

| 118 Customer-related threats—Product | Product risk—SEPA payments | X | X | |||||

| 119 Customer-related threats—Product | Product risk—SWIFT payments | X | X | |||||

| 120 Customer-related threats—Product | Product risk—money send | X | X | |||||

| 121 Customer-related threats—Product | Product risk—payment cards | X | X | |||||

| 122 Customer-related threats—Product | Product risk—card purchases | X | X | |||||

| 123 Customer-related threats—Product | Product risk—card cash withdrawal | X | X | |||||

| 124 Customer-related threats—Product | Product risk—card credit voucher | X | X | |||||

| 125 Customer-related threats—Product | Product risk—cor. accounts payments | X | X | |||||

| 126 Customer-related threats—Product | Product risk—cash operations | X | X | |||||

| 127 Customer-related threats—Product | Product risk—transaction to cryptocurrency | X | X | |||||

| 128 Customer-related threats—Product | Product risk—transaction to gambling | X | X | |||||

| 129 Customer-related threats—Product | Product risk—transaction received from sanctioned country | X | X | X | ||||

| 130 Customer-related threats—Product | Product risk—transaction sent to sanctioned country | X | X | X | ||||

| 131 Customer-related threats—Product | Product risk—transaction sent/received to/from sanctioned entity. | X | X | X | X | |||

| 132 Customer-related threats—Product | Product risk—transactions sent to high-risk country (high AML, terrorism, criminal, corruption/bribery level) | X | X | X | ||||

| 133 Customer-related threats—Product | Product risk—transactions received from high-risk country (high AML, terrorism, criminal, corruption/bribery level) | X | X | X | ||||

| 134 Customer-related threats—Product | Product risk—transaction counteragent is included in terrorist list | X | X | X | X | |||

| 135 Customer-related threats—Geographic | Customer’s geographical location is in country with comprehensive sanctions | X | X | X | ||||

| 136 Customer-related threats—Geographic | UBO of the customer geographical location is in country with comprehensive sanctions | X | X | X | ||||

| 137 Customer-related threats—Geographic | Customer representative geographical location is in country with comprehensive sanctions | X | X | X | ||||

| 138 Customer-related threats—Geographic | Customer’s geographical location or their financial connections is in high-risk country (high AML, terrorism, criminal, corruption/bribery level) | X | X | X | ||||

| 139 Customer-related threats—Geographic | UBO of the customer’s geographical location or their financial connections is in high-risk country (high AML, terrorism, criminal, corruption/bribery level) | X | X | X | ||||

| 140 Customer-related threats—Geographic | Customer’s representative geographical location or their financial connections is in high-risk country (high AML, terrorism, criminal, corruption/bribery level) | X | X | X | ||||

| 141 Customer-related threats—Geographic | Geographical location of institution, branches | X | X | X | ||||

| 142 Customer-related threats—Customer | Face-to-face identification | X | X | |||||

| 143 Customer-related threats—Customer | Identification by distributor | X | X | |||||

| 144 Customer-related threats—Customer | Non-face-to-face identification | X | X | |||||

| 145 Customer-related threats—Transactions | Transaction initiated in the shop | X | ||||||

| 146 Customer-related threats—Transactions | Transaction initiated remotely | X | ||||||

| 147 Customer-related threats—Transactions | Transaction initiated by PISP | X | ||||||

| 148 Credit risk | Unallowed overdrafts | X | X | X | X | |||

| 149 Credit risk | Unallowed overdrafts with reserves | X | X | X | X | |||

| 150 Market risk | Recession | X | X | |||||

| 151 Market risk | Political turmoil | X | X | |||||

| 152 Market risk | Changes in interest rates | X | X | |||||

| 153 Market risk | Terrorist/pirates attacks | X | X | X | ||||

| 154 Market risk | War | X | X | X | X | X | X | X |

| 155 Market risk | Strikes | X | X | X | X | |||

| 156 Unsystematic risk | Regulators fines | X | X | X | X | X | ||

| 157 Unsystematic risk | Product supply suspension | X | X | X | X | X | ||

| 158 Unsystematic risk | Law cases | X | X | X | X | X | X | |

| 159 Market risk | Product price change on the market/product not competitive | X | X | X | X | |||

| 160 Compliance | Product area of use violence | X | X | X | X | |||

| 161 Compliance | Product licensor regulation violation | X | X | X | X | |||

| 162 Compliance | Current product does not correspond to new regulators norms | X | X | X | X | X | ||

| 163 Compliance | Payment systems regulation violence | X | X | X | X | |||

| 164 Compliance | Partner due diligence absence | X | X | X | X | X | ||

| 165 Compliance | Sign agreement with the out-source without prior approval from regulator | X | X | X | X | |||

| 166 Compliance | Use of cloud solutions, rendered services not in accordance with EBA regulation | X | X | X | X | |||

| 167 Compliance | Do not support PISP, AISP | X | X | X | X | X | ||

| 168 Compliance | Do not apply SCA in accordance with norms | X | X | X | X | X | ||

| 169 Compliance | Financial institution operates below the minimum regulatory capital ratios or with negative own funds | X | X | X | X | |||

| 170 Compliance | Correspondent bank deducts funds without approval from customer funds segregation account | X | X | X | ||||

| 171 Compliance | The customer “Right to Be Forgotten” was not realized | X | X | X | X | X | X | |

| 172 Compliance | The customers data were shared with GDPR violation | X | X | X | X | X | X | |

| 173 Compliance | Breach of payment card data | X | X | X | X | X | ||

| 174 Compliance | Disclosure of protected health information | X | X | X | X | X | X | |

| 175 Compliance | Not appointed or trained data protection officer | X | X | X | X | X | X | |

| 176 Compliance | Not easy to identify and/or no data upon customer request available | X | X | X | ||||

| 177 Compliance | The business continuity plan not tested | X | X | X | ||||

| 178 Compliance | The ICT risk not assessed and/or reported | X | X | |||||

| 179 Compliance | Governance risk not assessed and/or reported | X | ||||||

| 180 Compliance | Operational risk not assessed and/or reported | X | X | |||||

| 181 Compliance | Human resource risk not assessed and/or reported | X | X | |||||

| 182 Compliance | Health and safety risk not assessed and/or reported | X | ||||||

| 183 Compliance | Financial risk not assessed and/or reported | X | X | |||||

| 184 Compliance | Capital adequacy risk not assessed and/or reported | X | X | |||||

| 185 Compliance | Environmental/external risk not assessed and/or reported | X | ||||||

| 186 Compliance | Law/compliance risk not assessed and/or reported | X | ||||||

| 187 Compliance | Strategic risk not assessed and/or reported | X | ||||||

| 188 Compliance | Financial crime risk not assessed and/or reported | X | X | |||||

| 189 Compliance | The compliance officer was not assigned | X | X | |||||

| 190 Compliance | The MLRO was not assigned | X | X | X | ||||

| 191 Compliance | The risk officer was not assigned | X | X | |||||

| 192 Compliance | The internal auditor was not assigned | X | X | X | X | X | X | X |

| 193 Compliance | Board director shortage | X | X | X | X | X | ||

| 194 Compliance | Board directors not approved by regulators | X | X | X | X | X | ||

| 195 Compliance | Senior management not approved by regulators (if applicable) | X | X | X | X | X | ||

| 196 Compliance | Unresolved/unassessed conflict of interests | X | X | X | X | X | X | X |

| 197 Change risk | Implementation of the new distribution channels without POG approval | X | X | X | X | X | X | X |

| 198 Change risk | Implementing new requirements to customers without POG approval | X | X | X | X | X | X | |

| 199 Change risk | Implementing new product/service or their changes without POG approval | X | X | X | X | X | X | |

| 200 Change risk | Implementing new/variation of tariffs before prior customer approval | X | X | X | X | |||

| 201 Change risk | Implementing new/variation of tariffs without POG approval | X | X | X | X | |||

| 202 Change risk | Elimination of the product/services before prior customer’s approval | X | X | X | X | X | ||

| 203 Change risk | Elimination of the product/services without POG approval | X | X | X | X | X | ||

| 204 Change risk | Country/audience change without POG approval | X | X | X | X | X | X | |

| 205 Change risk | Country/audience elimination before prior customer’s notification | X | X | X | X | X | X | |

| 206 Change risk | No execution of the regulatory changes in the requested time period | X | X | X | X | X | X | |

| 207 Reputational risk | Poor customer support service | X | X | |||||

| 208 Reputational risk | Lack of secure e/m banking platform | X | X | X | X | X | ||

| 209 Reputational risk | Fraud and corruption related to the financial institution | X | X | X | X | X | ||

| 210 Reputational risk | Unreasonable account block or product unavailability | X | X | X | X | |||

| 211 Reputational risk | Unclear/incorrect information to the customers (tariffs, extracts) | X | X | X | ||||

| 212 Reputational risk | Hosting country reputation | |||||||

| 213 Reputational risk | Negative review on social media | X | X | |||||

| 214 Reputational risk | Unreasonably long customer onboard | X | X | X | X | X | X | |

| 215 Reputational risk | Unreasonably long customer request processing | X | X | X | X | X | ||

| 216 Reputational risk | Low shareholders trust | X | ||||||

| 217 Reputational risk | Product functioning errors | X | X | X | X | X |

| Vulnerability | Governance Risks | Operational Risks | Human Resources Risks | Financial Risks | ICT Risks | Capital Adequacy Risks | Financial Crime Risks |

|---|---|---|---|---|---|---|---|

| Absence of clear and comprehensive governance policy | X | ||||||

| Lack of information exchange between departments | X | X | X | ||||

| Lack of strategy plan or its actualization | X | ||||||

| Lack of record keeping of the board decision | X | ||||||

| Lack of board decision notification to the staff | X | X | |||||

| Lack/improper policies/procedures describing internal processes | X | X | X | X | X | X | X |

| Lack of the procedure/policies/reports approval procedure by the board | X | ||||||

| Lack of financial reporting | X | X | X | X | X | ||

| Lack of job descriptions | X | X | X | X | X | ||

| Absence of the critical skills management procedure | X | X | X | ||||

| Critical skills shortage | X | X | X | X | |||

| Lack of/insufficient staff training | X | X | X | X | |||

| Lack of the product oversign and governance/change control | X | X | |||||

| Failure to adhere to the company’s policies or procedures | X | X | X | X | X | X | X |

| Failure to enforce policies | X | X | X | X | X | X | X |

| Failure to stack to the distributors/out-source company approval procedure | X | X | |||||

| Lack of an exit strategy for co-operation with distributors/out-source companies | X | X | |||||

| Failure to protect prices with the distributor/out-source company | X | X | X | ||||

| Failure of distributor/out-source company/supplier to supply service | X | X | X | X | |||

| Lack of a business continuity plan or its insufficiency | X | X | X | X | X | ||

| Failure to diversify | X | X | X | X | X | X | X |

| Unsupervised work by suppliers or cleaning staff | X | X | |||||

| Lack of security awareness | X | X | X | ||||

| Poorly documented software | X | X | |||||

| Lack of monitoring mechanisms | X | X | X | X | X | X | |

| Inadequate or careless use of physical access control to buildings, rooms, and offices | X | X | |||||

| Lack of physical protection for the building, doors, and windows | X | ||||||

| Location in an area susceptible to flood and fire | X | X | |||||

| Unprotected storage | X | X | X | X | |||

| Insufficient maintenance/faulty installation of storage media | X | ||||||

| Lack of periodic equipment replacement schemes | X | ||||||

| Susceptibility to humidity, dust, and soiling | X | X | |||||

| Susceptibility to temperature variations | X | X | |||||

| Susceptibility to voltage variations | X | ||||||

| Unprotected communication lines | X | ||||||

| Poor joint cabling | X | ||||||

| Lack of identification and authentication mechanisms | X | X | X | ||||

| Unprotected sensitive traffic | X | X | X | X | X | ||

| Inadequate network management | X | ||||||

| Lack of care at disposal | X | X | |||||

| Complicated user interface | X | X | |||||

| Lack of audit trail | X | X | X | X | X | ||

| No or insufficient product/software/process testing | X | X | X | X | |||

| Poor password management | X | ||||||

| Unclear or incomplete specification for developers | X | X | X | X | X | ||

| Uncontrolled downloading and using software | X | X | |||||

| Well-known gap in the software/process still in covering | X | X | X | X | X | ||

| Wrong allocation of access rights | X | X | X | X | |||

| Insufficient or irregular water supply | X | X | |||||

| Inappropriate CDD/EDD procedure | X | X | |||||

| Inappropriate cash management | X | X | X | X | X | ||

| Failure to identify risk-related events | X | X | X | X | X | X | X |

| Failure to identify beneficiary/customer | X | X | X | ||||

| Failure to report to supervising organizations | X | X | X | X | X | X | X |

| Failure to respond/communicate with the regulators | X | X | X | X | X | X | X |

| Lack of incident-reporting mechanism | X | X | X | X | X | X | X |

| Lack of staff stress relief possibilities and trainings | X | ||||||

| Bad ergonomics of the work place | |||||||

| Bad or absent noise control | |||||||

| Poor housekeeping | X | ||||||

| Missing or insufficient lighting | |||||||

| Missing or expired or not verified extinguishers/fire-extinguishing mechanisms | X | ||||||

| Correspondent bank stability risk | X | X | X | ||||

| Failure to define product prices in accordance with the market | X | ||||||

| Failure to manage assets volatility risk | X | ||||||

| Lack of liquidity | X | X | X | ||||

| Staff fraud | X | X | |||||

| Staff mistakes | X | X | X | X | |||

| Incorrect accounting/business model application | X | X | X | ||||

| Internal processes incompliant with current legal norms and regulations | X | X | X | X | X | X | X |

| Lack of or improper customer funds segregation/capital rate calculation mechanism | X | X | |||||

| Failure of the management to review and evaluate capital adequacy/customer funds segregation assessments and strategies | X | X | X | X | |||

| Failure to define and control segregated funds access from the side of the correspondent bank | X | X | X | X | |||

| Poorly described and managed suppliers’ invoices payments procedure | X | X | X | ||||

| Lack of or improper overdraft management procedure | X | X | X | ||||

| Lack of or improper company liabilities management procedure | X | X | X | ||||

| Lack of or improper data privacy procedure | X | X | X | X | X | ||

| Lack of a data protection officer or role | X | X | X | X | X | X |

| Governance Risks | Operational Risks | Human Resources Risks | Financial Risks | ICT Risks | Capital Adequacy Risks | Financial Crime Risks | Governance Risks | Operational Risks | Human Resources Risks | Financial Risks | ICT Risks | Capital Adequacy Risks | Financial Crime Risks | Governance Risks | Operational Risks | Human Resources Risks | Financial Risks | ICT Risks | Capital Adequacy Risks | Financial Crime Risks | Governance Risks | Operational Risks | Human Resources Risks | Financial Risks | ICT Risks | Capital Adequacy Risks | Financial Crime Risks | Governance Risks | Operational Risks | Human Resources Risks | Financial Risks | ICT Risks | Capital Adequacy Risks | Financial Crime Risks | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Respondent 1 | Respondent 2 | Respondent 3 | Respondent 4 | Respondent 5 | |||||||||||||||||||||||||||||||

| 1 | 0 | 0 | 0 | 3 | 4 | 0 | 0 | 0 | 0 | 0 | 2 | 3 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 3 | 4 | 0 | 0 |

| 2 | 0 | 0 | 0 | 3 | 4 | 0 | 0 | 0 | 0 | 0 | 2 | 3 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 3 | 4 | 0 | 0 |

| 3 | 0 | 0 | 0 | 4 | 4 | 0 | 0 | 0 | 0 | 0 | 4 | 4 | 0 | 0 | 0 | 0 | 0 | 4 | 4 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 4 | 4 | 0 | 0 |

| 4 | 0 | 0 | 0 | 4 | 4 | 0 | 0 | 0 | 0 | 0 | 4 | 4 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 4 | 4 | 0 | 0 |

| 5 | 0 | 0 | 0 | 3 | 4 | 0 | 0 | 0 | 0 | 0 | 3 | 4 | 0 | 0 | 0 | 0 | 0 | 3 | 2 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 4 | 0 | 0 |

| 6 | 0 | 0 | 0 | 2 | 4 | 0 | 0 | 0 | 0 | 0 | 2 | 4 | 0 | 0 | 0 | 0 | 0 | 2 | 3 | 0 | 0 | 0 | 0 | 0 | 2 | 3 | 0 | 0 | 0 | 0 | 0 | 2 | 4 | 0 | 0 |

| 7 | 0 | 0 | 0 | 4 | 3 | 0 | 0 | 0 | 0 | 0 | 4 | 3 | 0 | 0 | 0 | 0 | 0 | 4 | 3 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 4 | 3 | 0 | 0 |

| 8 | 0 | 0 | 0 | 5 | 5 | 0 | 0 | 0 | 0 | 0 | 5 | 5 | 0 | 0 | 0 | 0 | 0 | 5 | 5 | 0 | 0 | 0 | 0 | 0 | 5 | 5 | 0 | 0 | 0 | 0 | 0 | 5 | 5 | 0 | 0 |

| 9 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 |

| 10 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 |

| 11 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 |

| 12 | 4 | 3 | 4 | 3 | 4 | 0 | 0 | 5 | 4 | 4 | 3 | 4 | 0 | 0 | 4 | 4 | 4 | 3 | 4 | 0 | 0 | 4 | 4 | 4 | 3 | 4 | 0 | 0 | 4 | 3 | 4 | 3 | 4 | 0 | 0 |

| 13 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 |

| 14 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 |

| 15 | 0 | 0 | 3 | 0 | 4 | 0 | 0 | 0 | 0 | 2 | 0 | 3 | 0 | 0 | 0 | 0 | 2 | 0 | 2 | 0 | 0 | 0 | 0 | 3 | 0 | 2 | 0 | 0 | 0 | 0 | 3 | 0 | 4 | 0 | 0 |

| 16 | 0 | 0 | 1 | 3 | 4 | 0 | 0 | 0 | 0 | 1 | 3 | 4 | 0 | 0 | 0 | 0 | 1 | 2 | 4 | 0 | 0 | 0 | 0 | 2 | 2 | 4 | 0 | 0 | 0 | 0 | 1 | 3 | 4 | 0 | 0 |

| 17 | 0 | 0 | 4 | 3 | 4 | 0 | 0 | 0 | 0 | 4 | 3 | 4 | 0 | 0 | 0 | 0 | 4 | 3 | 4 | 0 | 0 | 0 | 0 | 3 | 3 | 4 | 0 | 0 | 0 | 0 | 4 | 3 | 4 | 0 | 0 |

| 18 | 0 | 4 | 1 | 0 | 4 | 0 | 0 | 0 | 4 | 1 | 0 | 4 | 0 | 0 | 0 | 3 | 1 | 0 | 4 | 0 | 0 | 0 | 4 | 2 | 0 | 4 | 0 | 0 | 0 | 4 | 1 | 0 | 4 | 0 | 0 |

| 19 | 0 | 3 | 1 | 0 | 5 | 0 | 0 | 0 | 2 | 1 | 0 | 3 | 0 | 0 | 0 | 2 | 1 | 0 | 3 | 0 | 0 | 0 | 3 | 3 | 0 | 3 | 0 | 0 | 0 | 3 | 1 | 0 | 5 | 0 | 0 |

| 20 | 0 | 5 | 2 | 5 | 4 | 0 | 0 | 0 | 5 | 2 | 5 | 4 | 0 | 0 | 0 | 4 | 2 | 4 | 4 | 0 | 0 | 0 | 4 | 3 | 4 | 4 | 0 | 0 | 0 | 5 | 2 | 5 | 4 | 0 | 0 |

| 21 | 0 | 4 | 4 | 3 | 4 | 0 | 0 | 0 | 3 | 4 | 3 | 4 | 0 | 0 | 0 | 3 | 3 | 3 | 3 | 0 | 0 | 0 | 4 | 3 | 4 | 3 | 0 | 0 | 0 | 4 | 4 | 3 | 4 | 0 | 0 |

| 22 | 0 | 5 | 4 | 5 | 3 | 5 | 4 | 0 | 5 | 4 | 5 | 3 | 5 | 4 | 0 | 4 | 3 | 4 | 3 | 4 | 3 | 0 | 4 | 3 | 4 | 3 | 4 | 3 | 0 | 5 | 4 | 5 | 3 | 5 | 4 |

| 23 | 0 | 3 | 0 | 3 | 4 | 0 | 0 | 0 | 3 | 0 | 3 | 4 | 0 | 0 | 0 | 3 | 0 | 3 | 4 | 0 | 0 | 0 | 4 | 0 | 4 | 4 | 0 | 0 | 0 | 3 | 0 | 3 | 4 | 0 | 0 |

| 24 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 |

| 25 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 |

| 26 | 0 | 3 | 0 | 0 | 4 | 0 | 4 | 0 | 2 | 0 | 0 | 3 | 0 | 3 | 0 | 2 | 0 | 0 | 3 | 0 | 3 | 0 | 3 | 0 | 0 | 3 | 0 | 3 | 0 | 3 | 0 | 0 | 4 | 0 | 4 |

| 27 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 |

| 28 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 |

| 29 | 0 | 5 | 0 | 4 | 4 | 4 | 4 | 0 | 4 | 0 | 4 | 4 | 4 | 4 | 0 | 4 | 0 | 4 | 4 | 4 | 4 | 0 | 4 | 0 | 4 | 4 | 4 | 4 | 0 | 5 | 0 | 4 | 4 | 4 | 4 |

| 30 | 0 | 1 | 0 | 0 | 4 | 0 | 0 | 0 | 1 | 0 | 0 | 4 | 0 | 0 | 0 | 1 | 0 | 0 | 3 | 0 | 0 | 0 | 2 | 0 | 0 | 3 | 0 | 0 | 0 | 1 | 0 | 0 | 4 | 0 | 0 |

| 31 | 0 | 5 | 0 | 0 | 5 | 0 | 0 | 0 | 4 | 0 | 0 | 4 | 0 | 0 | 0 | 4 | 0 | 0 | 4 | 0 | 0 | 0 | 4 | 0 | 0 | 4 | 0 | 0 | 0 | 5 | 0 | 0 | 5 | 0 | 0 |

| 32 | 0 | 4 | 0 | 0 | 4 | 0 | 0 | 0 | 4 | 0 | 0 | 4 | 0 | 0 | 0 | 4 | 0 | 0 | 4 | 0 | 0 | 0 | 4 | 0 | 0 | 4 | 0 | 0 | 0 | 4 | 0 | 0 | 4 | 0 | 0 |

| 33 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 |

| 34 | 0 | 3 | 0 | 3 | 4 | 0 | 0 | 0 | 3 | 0 | 3 | 4 | 0 | 0 | 0 | 3 | 0 | 3 | 4 | 0 | 0 | 0 | 3 | 0 | 3 | 4 | 0 | 0 | 0 | 3 | 0 | 3 | 4 | 0 | 0 |

| 35 | 0 | 4 | 0 | 0 | 4 | 0 | 0 | 0 | 5 | 0 | 0 | 4 | 0 | 0 | 0 | 5 | 0 | 0 | 4 | 0 | 0 | 0 | 5 | 0 | 0 | 4 | 0 | 0 | 0 | 4 | 0 | 0 | 4 | 0 | 0 |

| 36 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 |

| 37 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 |

| 38 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 |

| 39 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 |

| 40 | 0 | 3 | 0 | 4 | 5 | 3 | 0 | 0 | 3 | 0 | 4 | 4 | 3 | 0 | 0 | 3 | 0 | 2 | 4 | 2 | 0 | 0 | 2 | 0 | 2 | 3 | 2 | 0 | 0 | 3 | 0 | 4 | 5 | 3 | 0 |

| 41 | 0 | 0 | 0 | 5 | 5 | 5 | 0 | 0 | 0 | 0 | 5 | 5 | 5 | 0 | 0 | 0 | 0 | 5 | 5 | 5 | 0 | 0 | 0 | 0 | 5 | 5 | 5 | 0 | 0 | 0 | 0 | 5 | 5 | 5 | 0 |

| 42 | 0 | 0 | 0 | 5 | 5 | 5 | 0 | 0 | 0 | 0 | 5 | 5 | 5 | 0 | 0 | 0 | 0 | 4 | 4 | 4 | 0 | 0 | 0 | 0 | 4 | 4 | 4 | 0 | 0 | 0 | 0 | 5 | 5 | 5 | 0 |

| 43 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 |

| 44 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 |

| 45 | 2 | 4 | 1 | 4 | 4 | 4 | 0 | 3 | 3 | 1 | 4 | 4 | 4 | 0 | 2 | 3 | 1 | 3 | 4 | 3 | 0 | 2 | 3 | 1 | 3 | 4 | 3 | 0 | 2 | 4 | 1 | 4 | 4 | 4 | 0 |

| 46 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 |

| 47 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 |

| 48 | 2 | 5 | 1 | 5 | 5 | 5 | 5 | 2 | 5 | 1 | 5 | 5 | 5 | 5 | 2 | 5 | 1 | 3 | 5 | 3 | 5 | 2 | 5 | 1 | 3 | 5 | 3 | 5 | 2 | 5 | 1 | 5 | 5 | 5 | 5 |

| 49 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 50 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 51 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 52 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 53 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 54 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 55 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 56 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 57 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 58 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 59 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 60 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 61 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 62 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 63 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 64 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 65 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 66 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 67 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 68 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 69 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 70 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 71 | 2 | 0 | 0 | 3 | 0 | 3 | 5 | 3 | 0 | 0 | 4 | 0 | 4 | 5 | 3 | 0 | 0 | 3 | 0 | 3 | 5 | 3 | 0 | 0 | 3 | 0 | 3 | 5 | 2 | 0 | 0 | 3 | 0 | 3 | 5 |

| 72 | 2 | 0 | 0 | 3 | 0 | 3 | 5 | 3 | 0 | 0 | 4 | 0 | 4 | 5 | 3 | 0 | 0 | 3 | 0 | 3 | 5 | 3 | 0 | 0 | 3 | 0 | 3 | 5 | 2 | 0 | 0 | 3 | 0 | 3 | 5 |

| 73 | 2 | 0 | 0 | 3 | 0 | 3 | 4 | 3 | 0 | 0 | 4 | 0 | 4 | 4 | 3 | 0 | 0 | 3 | 0 | 3 | 4 | 3 | 0 | 0 | 3 | 0 | 3 | 4 | 2 | 0 | 0 | 3 | 0 | 3 | 4 |

| 74 | 2 | 0 | 0 | 0 | 0 | 0 | 4 | 2 | 0 | 0 | 0 | 0 | 0 | 4 | 2 | 0 | 0 | 0 | 0 | 0 | 4 | 2 | 0 | 0 | 0 | 0 | 0 | 4 | 2 | 0 | 0 | 0 | 0 | 0 | 4 |

| 75 | 2 | 0 | 0 | 0 | 0 | 0 | 5 | 3 | 0 | 0 | 0 | 0 | 0 | 5 | 3 | 0 | 0 | 0 | 0 | 0 | 5 | 3 | 0 | 0 | 0 | 0 | 0 | 5 | 2 | 0 | 0 | 0 | 0 | 0 | 5 |

| 76 | 2 | 0 | 0 | 0 | 0 | 0 | 5 | 3 | 0 | 0 | 0 | 0 | 0 | 5 | 3 | 0 | 0 | 0 | 0 | 0 | 5 | 3 | 0 | 0 | 0 | 0 | 0 | 5 | 2 | 0 | 0 | 0 | 0 | 0 | 5 |

| 77 | 2 | 0 | 0 | 3 | 0 | 3 | 5 | 4 | 0 | 0 | 3 | 0 | 3 | 5 | 2 | 0 | 0 | 3 | 0 | 3 | 5 | 2 | 0 | 0 | 3 | 0 | 3 | 5 | 2 | 0 | 0 | 3 | 0 | 3 | 5 |

| 78 | 2 | 0 | 0 | 3 | 0 | 3 | 5 | 4 | 0 | 0 | 3 | 0 | 3 | 5 | 2 | 0 | 0 | 3 | 0 | 3 | 5 | 2 | 0 | 0 | 3 | 0 | 3 | 5 | 2 | 0 | 0 | 3 | 0 | 3 | 5 |

| 79 | 2 | 0 | 0 | 3 | 0 | 3 | 5 | 4 | 0 | 0 | 3 | 0 | 3 | 5 | 2 | 0 | 0 | 3 | 0 | 3 | 5 | 2 | 0 | 0 | 3 | 0 | 3 | 5 | 2 | 0 | 0 | 3 | 0 | 3 | 5 |

| 80 | 0 | 0 | 0 | 3 | 0 | 3 | 5 | 0 | 0 | 0 | 3 | 0 | 3 | 5 | 0 | 0 | 0 | 2 | 0 | 2 | 5 | 0 | 0 | 0 | 2 | 0 | 2 | 5 | 0 | 0 | 0 | 3 | 0 | 3 | 5 |

| 81 | 0 | 0 | 0 | 3 | 0 | 3 | 5 | 0 | 0 | 0 | 3 | 0 | 3 | 5 | 0 | 0 | 0 | 3 | 0 | 3 | 5 | 0 | 0 | 0 | 3 | 0 | 3 | 5 | 0 | 0 | 0 | 3 | 0 | 3 | 5 |

| 82 | 0 | 0 | 0 | 3 | 0 | 3 | 5 | 0 | 0 | 0 | 3 | 0 | 3 | 5 | 0 | 0 | 0 | 3 | 0 | 3 | 5 | 0 | 0 | 0 | 3 | 0 | 3 | 5 | 0 | 0 | 0 | 3 | 0 | 3 | 5 |

| 83 | 0 | 0 | 0 | 2 | 0 | 2 | 3 | 0 | 0 | 0 | 2 | 0 | 2 | 4 | 0 | 0 | 0 | 2 | 0 | 2 | 4 | 0 | 0 | 0 | 2 | 0 | 2 | 4 | 0 | 0 | 0 | 2 | 0 | 2 | 3 |

| 84 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 85 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 86 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 87 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 88 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 89 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 90 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 |

| 91 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 |

| 92 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 93 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 94 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 95 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 96 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 97 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 98 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 99 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 100 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 101 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 102 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 103 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 104 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 105 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 |

| 106 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 5 |

| 107 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 108 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 109 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 110 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 111 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 112 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 113 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 114 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 115 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 116 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 117 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 118 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 3 | 0 | 0 | 0 | 0 | 3 |

| 119 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 2 | 0 | 0 | 0 | 0 | 2 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 3 | 0 | 0 | 0 | 0 | 3 |

| 120 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 5 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 4 | 0 | 0 | 0 | 0 | 4 |

| 121 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 4 | 0 | 0 | 0 | 0 | 4 |

| 122 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 3 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 4 | 0 | 0 | 0 | 0 | 4 |

| 123 | 0 | 5 | 0 | 0 | 0 | 0 | 5 | 0 | 4 | 0 | 0 | 0 | 0 | 5 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 5 | 0 | 0 | 0 | 0 | 5 |

| 124 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 3 | 0 | 0 | 0 | 0 | 3 |

| 125 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 |

| 126 | 0 | 5 | 0 | 0 | 0 | 0 | 5 | 0 | 5 | 0 | 0 | 0 | 0 | 5 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 5 | 0 | 0 | 0 | 0 | 5 |

| 127 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 3 | 0 | 0 | 0 | 0 | 3 |

| 128 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 5 | 0 | 0 | 0 | 0 | 5 | 0 | 5 | 0 | 0 | 0 | 0 | 5 | 0 | 5 | 0 | 0 | 0 | 0 | 5 | 0 | 3 | 0 | 0 | 0 | 0 | 3 |

| 129 | 0 | 5 | 0 | 5 | 0 | 0 | 5 | 0 | 5 | 0 | 5 | 0 | 0 | 5 | 0 | 5 | 0 | 5 | 0 | 0 | 5 | 0 | 5 | 0 | 5 | 0 | 0 | 5 | 0 | 5 | 0 | 5 | 0 | 0 | 5 |

| 130 | 0 | 5 | 0 | 5 | 0 | 0 | 5 | 0 | 5 | 0 | 5 | 0 | 0 | 5 | 0 | 5 | 0 | 5 | 0 | 0 | 5 | 0 | 5 | 0 | 5 | 0 | 0 | 5 | 0 | 5 | 0 | 5 | 0 | 0 | 5 |

| 131 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 |

| 132 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 |

| 133 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 |

| 134 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 | 0 | 5 | 0 | 3 | 0 | 3 | 5 |

| 135 | 0 | 4 | 0 | 4 | 0 | 0 | 5 | 0 | 4 | 0 | 4 | 0 | 0 | 5 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 5 |

| 136 | 0 | 4 | 0 | 4 | 0 | 0 | 5 | 0 | 4 | 0 | 4 | 0 | 0 | 5 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 5 |

| 137 | 0 | 4 | 0 | 4 | 0 | 0 | 5 | 0 | 4 | 0 | 4 | 0 | 0 | 5 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 5 |

| 138 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 |

| 139 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 |

| 140 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 |

| 141 | 0 | 3 | 0 | 1 | 0 | 0 | 3 | 0 | 3 | 0 | 1 | 0 | 0 | 3 | 0 | 3 | 0 | 1 | 0 | 0 | 3 | 0 | 3 | 0 | 1 | 0 | 0 | 3 | 0 | 3 | 0 | 1 | 0 | 0 | 3 |

| 142 | 0 | 4 | 0 | 0 | 0 | 0 | 2 | 0 | 4 | 0 | 0 | 0 | 0 | 3 | 0 | 4 | 0 | 0 | 0 | 0 | 3 | 0 | 4 | 0 | 0 | 0 | 0 | 3 | 0 | 4 | 0 | 0 | 0 | 0 | 2 |

| 143 | 0 | 5 | 0 | 0 | 0 | 0 | 4 | 0 | 5 | 0 | 0 | 0 | 0 | 4 | 0 | 5 | 0 | 0 | 0 | 0 | 4 | 0 | 5 | 0 | 0 | 0 | 0 | 4 | 0 | 5 | 0 | 0 | 0 | 0 | 4 |

| 144 | 0 | 5 | 0 | 0 | 0 | 0 | 4 | 0 | 5 | 0 | 0 | 0 | 0 | 4 | 0 | 5 | 0 | 0 | 0 | 0 | 4 | 0 | 5 | 0 | 0 | 0 | 0 | 4 | 0 | 5 | 0 | 0 | 0 | 0 | 4 |

| 145 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 146 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 |

| 147 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 4 |

| 148 | 4 | 4 | 0 | 4 | 0 | 4 | 0 | 3 | 3 | 0 | 3 | 0 | 3 | 0 | 1 | 1 | 0 | 1 | 0 | 1 | 0 | 1 | 1 | 0 | 1 | 0 | 1 | 0 | 4 | 4 | 0 | 4 | 0 | 4 | 0 |

| 149 | 4 | 4 | 0 | 4 | 0 | 4 | 0 | 3 | 3 | 0 | 4 | 0 | 4 | 0 | 1 | 1 | 0 | 1 | 0 | 1 | 0 | 1 | 1 | 0 | 1 | 0 | 1 | 0 | 4 | 4 | 0 | 4 | 0 | 4 | 0 |

| 150 | 0 | 1 | 0 | 4 | 0 | 0 | 0 | 0 | 3 | 0 | 3 | 0 | 0 | 0 | 0 | 2 | 0 | 2 | 0 | 0 | 0 | 0 | 2 | 0 | 2 | 0 | 0 | 0 | 0 | 1 | 0 | 4 | 0 | 0 | 0 |

| 151 | 0 | 1 | 0 | 4 | 0 | 0 | 0 | 0 | 1 | 0 | 3 | 0 | 0 | 0 | 0 | 1 | 0 | 3 | 0 | 0 | 0 | 0 | 1 | 0 | 3 | 0 | 0 | 0 | 0 | 1 | 0 | 4 | 0 | 0 | 0 |

| 152 | 0 | 1 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 4 | 0 | 0 | 0 | 0 | 2 | 0 | 2 | 0 | 0 | 0 | 0 | 2 | 0 | 2 | 0 | 0 | 0 | 0 | 1 | 0 | 3 | 0 | 0 | 0 |

| 153 | 0 | 5 | 0 | 5 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 2 | 0 | 2 | 0 | 0 | 3 | 0 | 2 | 0 | 2 | 0 | 0 | 3 | 0 | 5 | 0 | 5 | 0 | 0 | 4 |

| 154 | 5 | 4 | 5 | 5 | 5 | 5 | 4 | 5 | 4 | 5 | 5 | 5 | 5 | 4 | 5 | 4 | 5 | 5 | 5 | 5 | 4 | 5 | 4 | 5 | 5 | 5 | 5 | 4 | 5 | 4 | 5 | 5 | 5 | 5 | 4 |

| 155 | 0 | 4 | 5 | 3 | 0 | 3 | 0 | 0 | 1 | 1 | 1 | 0 | 1 | 0 | 0 | 1 | 1 | 1 | 0 | 1 | 0 | 0 | 1 | 1 | 1 | 0 | 1 | 0 | 0 | 4 | 5 | 3 | 0 | 3 | 0 |

| 156 | 5 | 5 | 0 | 5 | 0 | 5 | 5 | 5 | 5 | 0 | 5 | 0 | 5 | 5 | 5 | 5 | 0 | 5 | 0 | 5 | 5 | 5 | 5 | 0 | 5 | 0 | 5 | 5 | 5 | 5 | 0 | 5 | 0 | 5 | 5 |

| 157 | 3 | 5 | 0 | 3 | 0 | 3 | 4 | 3 | 4 | 0 | 3 | 0 | 3 | 4 | 4 | 5 | 0 | 4 | 0 | 4 | 4 | 4 | 5 | 0 | 4 | 0 | 4 | 4 | 3 | 5 | 0 | 3 | 0 | 3 | 4 |

| 158 | 3 | 4 | 3 | 5 | 0 | 5 | 4 | 3 | 3 | 3 | 5 | 0 | 5 | 4 | 3 | 3 | 3 | 5 | 0 | 5 | 4 | 3 | 3 | 3 | 5 | 0 | 5 | 4 | 3 | 4 | 3 | 5 | 0 | 5 | 4 |

| 159 | 4 | 2 | 0 | 4 | 0 | 4 | 0 | 3 | 2 | 0 | 4 | 0 | 4 | 0 | 3 | 2 | 0 | 4 | 0 | 4 | 0 | 3 | 2 | 0 | 4 | 0 | 4 | 0 | 4 | 2 | 0 | 4 | 0 | 4 | 0 |

| 160 | 5 | 4 | 0 | 5 | 0 | 5 | 0 | 2 | 2 | 0 | 3 | 0 | 3 | 0 | 3 | 3 | 0 | 3 | 0 | 3 | 0 | 3 | 3 | 0 | 3 | 0 | 3 | 0 | 5 | 4 | 0 | 5 | 0 | 5 | 0 |

| 161 | 5 | 4 | 0 | 5 | 0 | 5 | 0 | 3 | 3 | 0 | 4 | 0 | 4 | 0 | 3 | 3 | 0 | 4 | 0 | 4 | 0 | 3 | 3 | 0 | 4 | 0 | 4 | 0 | 5 | 4 | 0 | 5 | 0 | 5 | 0 |

| 162 | 3 | 3 | 0 | 5 | 0 | 5 | 4 | 3 | 4 | 0 | 5 | 0 | 5 | 4 | 3 | 4 | 0 | 5 | 0 | 5 | 4 | 3 | 4 | 0 | 5 | 0 | 5 | 4 | 3 | 3 | 0 | 5 | 0 | 5 | 4 |

| 163 | 3 | 4 | 0 | 4 | 0 | 4 | 0 | 3 | 4 | 0 | 4 | 0 | 4 | 0 | 3 | 4 | 0 | 4 | 0 | 4 | 0 | 3 | 4 | 0 | 4 | 0 | 4 | 0 | 3 | 4 | 0 | 4 | 0 | 4 | 0 |

| 164 | 4 | 2 | 0 | 3 | 0 | 3 | 4 | 3 | 2 | 0 | 3 | 0 | 3 | 4 | 3 | 2 | 0 | 3 | 0 | 3 | 4 | 3 | 2 | 0 | 3 | 0 | 3 | 4 | 4 | 2 | 0 | 3 | 0 | 3 | 4 |

| 165 | 4 | 2 | 0 | 3 | 0 | 3 | 0 | 4 | 2 | 0 | 3 | 0 | 3 | 0 | 4 | 2 | 0 | 3 | 0 | 3 | 0 | 4 | 2 | 0 | 3 | 0 | 3 | 0 | 4 | 2 | 0 | 3 | 0 | 3 | 0 |

| 166 | 0 | 2 | 0 | 3 | 5 | 3 | 0 | 0 | 2 | 0 | 3 | 5 | 3 | 0 | 0 | 3 | 0 | 3 | 5 | 3 | 0 | 0 | 3 | 0 | 3 | 5 | 3 | 0 | 0 | 2 | 0 | 3 | 5 | 3 | 0 |

| 167 | 3 | 2 | 0 | 4 | 4 | 4 | 0 | 4 | 3 | 0 | 4 | 4 | 4 | 0 | 1 | 1 | 0 | 1 | 1 | 1 | 0 | 1 | 1 | 0 | 1 | 1 | 1 | 0 | 3 | 2 | 0 | 4 | 4 | 4 | 0 |

| 168 | 3 | 2 | 0 | 4 | 4 | 4 | 0 | 4 | 3 | 0 | 4 | 4 | 4 | 0 | 2 | 2 | 0 | 2 | 2 | 2 | 0 | 2 | 2 | 0 | 2 | 2 | 2 | 0 | 3 | 2 | 0 | 4 | 4 | 4 | 0 |

| 169 | 5 | 3 | 0 | 5 | 0 | 5 | 0 | 4 | 3 | 0 | 5 | 0 | 5 | 0 | 2 | 2 | 0 | 2 | 0 | 2 | 0 | 2 | 2 | 0 | 2 | 0 | 2 | 0 | 5 | 3 | 0 | 5 | 0 | 5 | 0 |

| 170 | 0 | 5 | 0 | 3 | 0 | 3 | 0 | 0 | 1 | 0 | 3 | 0 | 3 | 0 | 0 | 1 | 0 | 1 | 0 | 1 | 0 | 0 | 1 | 0 | 1 | 0 | 1 | 0 | 0 | 5 | 0 | 3 | 0 | 3 | 0 |

| 171 | 4 | 2 | 4 | 4 | 3 | 4 | 0 | 3 | 1 | 4 | 4 | 3 | 4 | 0 | 3 | 1 | 4 | 4 | 3 | 4 | 0 | 3 | 1 | 4 | 4 | 3 | 4 | 0 | 4 | 2 | 4 | 4 | 3 | 4 | 0 |

| 172 | 4 | 2 | 4 | 4 | 4 | 4 | 0 | 3 | 2 | 4 | 4 | 4 | 4 | 0 | 3 | 2 | 4 | 4 | 4 | 4 | 0 | 3 | 2 | 4 | 4 | 4 | 4 | 0 | 4 | 2 | 4 | 4 | 4 | 4 | 0 |

| 173 | 4 | 4 | 0 | 4 | 4 | 4 | 0 | 4 | 4 | 0 | 4 | 4 | 4 | 0 | 1 | 1 | 0 | 1 | 1 | 1 | 0 | 1 | 1 | 0 | 1 | 1 | 1 | 0 | 4 | 4 | 0 | 4 | 4 | 4 | 0 |

| 174 | 3 | 3 | 5 | 4 | 0 | 4 | 3 | 2 | 2 | 3 | 4 | 0 | 4 | 3 | 2 | 2 | 3 | 4 | 0 | 4 | 3 | 2 | 2 | 3 | 4 | 0 | 4 | 3 | 3 | 3 | 5 | 4 | 0 | 4 | 3 |

| 175 | 4 | 2 | 1 | 3 | 5 | 3 | 0 | 4 | 2 | 1 | 3 | 5 | 3 | 0 | 4 | 2 | 1 | 3 | 5 | 3 | 0 | 4 | 2 | 1 | 3 | 5 | 3 | 0 | 4 | 2 | 1 | 3 | 5 | 3 | 0 |

| 176 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 | 0 | 4 | 0 | 0 | 4 | 0 | 4 |

| 177 | 4 | 2 | 0 | 0 | 3 | 0 | 0 | 3 | 1 | 0 | 0 | 3 | 0 | 0 | 3 | 1 | 0 | 0 | 3 | 0 | 0 | 3 | 1 | 0 | 0 | 3 | 0 | 0 | 4 | 2 | 0 | 0 | 3 | 0 | 0 |

| 178 | 4 | 0 | 0 | 0 | 5 | 0 | 0 | 4 | 0 | 0 | 0 | 5 | 0 | 0 | 4 | 0 | 0 | 0 | 5 | 0 | 0 | 4 | 0 | 0 | 0 | 5 | 0 | 0 | 4 | 0 | 0 | 0 | 5 | 0 | 0 |

| 179 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 |

| 180 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 4 | 0 | 0 | 0 | 0 | 0 | 3 | 4 | 0 | 0 | 0 | 0 | 0 | 3 | 4 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 |

| 181 | 3 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 3 | 0 | 0 | 0 | 0 |

| 182 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 |

| 183 | 3 | 0 | 0 | 3 | 0 | 0 | 0 | 3 | 0 | 0 | 4 | 0 | 0 | 0 | 3 | 0 | 0 | 4 | 0 | 0 | 0 | 3 | 0 | 0 | 4 | 0 | 0 | 0 | 3 | 0 | 0 | 3 | 0 | 0 | 0 |

| 184 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 3 | 0 | 0 | 0 | 0 | 4 | 0 | 3 | 0 | 0 | 0 | 0 | 4 | 0 | 3 | 0 | 0 | 0 | 0 | 4 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 |

| 185 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 |

| 186 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 |

| 187 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 |

| 188 | 4 | 0 | 0 | 0 | 0 | 0 | 4 | 4 | 0 | 0 | 0 | 0 | 0 | 4 | 4 | 0 | 0 | 0 | 0 | 0 | 4 | 4 | 0 | 0 | 0 | 0 | 0 | 4 | 4 | 0 | 0 | 0 | 0 | 0 | 4 |

| 189 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 |

| 190 | 5 | 0 | 4 | 0 | 0 | 0 | 5 | 5 | 0 | 4 | 0 | 0 | 0 | 5 | 5 | 0 | 4 | 0 | 0 | 0 | 5 | 5 | 0 | 4 | 0 | 0 | 0 | 5 | 5 | 0 | 4 | 0 | 0 | 0 | 5 |

| 191 | 4 | 0 | 4 | 0 | 0 | 0 | 0 | 3 | 0 | 4 | 0 | 0 | 0 | 0 | 3 | 0 | 4 | 0 | 0 | 0 | 0 | 3 | 0 | 4 | 0 | 0 | 0 | 0 | 4 | 0 | 4 | 0 | 0 | 0 | 0 |

| 192 | 4 | 4 | 4 | 4 | 3 | 4 | 4 | 4 | 4 | 4 | 4 | 3 | 4 | 4 | 4 | 4 | 4 | 4 | 3 | 4 | 4 | 4 | 4 | 4 | 4 | 3 | 4 | 4 | 4 | 4 | 4 | 4 | 3 | 4 | 4 |

| 193 | 3 | 3 | 3 | 2 | 0 | 2 | 0 | 3 | 3 | 3 | 2 | 0 | 2 | 0 | 3 | 3 | 3 | 2 | 0 | 2 | 0 | 3 | 3 | 3 | 2 | 0 | 2 | 0 | 3 | 3 | 3 | 2 | 0 | 2 | 0 |

| 194 | 3 | 2 | 3 | 1 | 0 | 1 | 0 | 2 | 2 | 3 | 1 | 0 | 1 | 0 | 2 | 2 | 3 | 1 | 0 | 1 | 0 | 2 | 2 | 3 | 1 | 0 | 1 | 0 | 3 | 2 | 3 | 1 | 0 | 1 | 0 |

| 195 | 3 | 2 | 3 | 1 | 0 | 1 | 0 | 1 | 1 | 1 | 1 | 0 | 1 | 0 | 1 | 1 | 1 | 1 | 0 | 1 | 0 | 1 | 1 | 1 | 1 | 0 | 1 | 0 | 3 | 2 | 3 | 1 | 0 | 1 | 0 |

| 196 | 4 | 2 | 5 | 4 | 4 | 4 | 3 | 3 | 2 | 5 | 4 | 4 | 4 | 3 | 3 | 2 | 5 | 4 | 4 | 4 | 3 | 3 | 2 | 5 | 4 | 4 | 4 | 3 | 4 | 2 | 5 | 4 | 4 | 4 | 3 |

| 197 | 3 | 4 | 3 | 4 | 3 | 4 | 4 | 2 | 3 | 2 | 4 | 3 | 4 | 4 | 2 | 3 | 2 | 3 | 3 | 3 | 4 | 2 | 3 | 2 | 3 | 3 | 3 | 4 | 3 | 4 | 3 | 4 | 3 | 4 | 4 |

| 198 | 3 | 3 | 0 | 3 | 2 | 3 | 4 | 2 | 3 | 0 | 3 | 2 | 3 | 4 | 2 | 3 | 0 | 3 | 2 | 3 | 4 | 2 | 3 | 0 | 3 | 2 | 3 | 4 | 3 | 3 | 0 | 3 | 2 | 3 | 4 |

| 199 | 3 | 3 | 0 | 3 | 2 | 3 | 4 | 3 | 3 | 0 | 3 | 2 | 3 | 4 | 3 | 3 | 0 | 3 | 2 | 3 | 4 | 3 | 3 | 0 | 3 | 2 | 3 | 4 | 3 | 3 | 0 | 3 | 2 | 3 | 4 |

| 200 | 3 | 3 | 0 | 3 | 0 | 3 | 0 | 3 | 3 | 0 | 3 | 0 | 3 | 0 | 3 | 3 | 0 | 3 | 0 | 3 | 0 | 3 | 3 | 0 | 3 | 0 | 3 | 0 | 3 | 3 | 0 | 3 | 0 | 3 | 0 |

| 201 | 3 | 3 | 0 | 4 | 0 | 4 | 0 | 4 | 4 | 0 | 4 | 0 | 4 | 0 | 4 | 4 | 0 | 4 | 0 | 4 | 0 | 4 | 4 | 0 | 4 | 0 | 4 | 0 | 3 | 3 | 0 | 4 | 0 | 4 | 0 |

| 202 | 3 | 3 | 0 | 3 | 0 | 3 | 4 | 2 | 3 | 0 | 3 | 0 | 3 | 4 | 2 | 3 | 0 | 3 | 0 | 3 | 4 | 2 | 3 | 0 | 3 | 0 | 3 | 4 | 3 | 3 | 0 | 3 | 0 | 3 | 4 |

| 203 | 3 | 3 | 0 | 3 | 0 | 3 | 4 | 2 | 3 | 0 | 3 | 0 | 3 | 4 | 2 | 3 | 0 | 3 | 0 | 3 | 4 | 2 | 3 | 0 | 3 | 0 | 3 | 4 | 3 | 3 | 0 | 3 | 0 | 3 | 4 |

| 204 | 3 | 3 | 0 | 3 | 2 | 3 | 4 | 1 | 3 | 0 | 3 | 2 | 3 | 4 | 1 | 3 | 0 | 3 | 2 | 3 | 4 | 1 | 3 | 0 | 3 | 2 | 3 | 4 | 3 | 3 | 0 | 3 | 2 | 3 | 4 |

| 205 | 3 | 3 | 0 | 3 | 2 | 3 | 4 | 1 | 3 | 0 | 3 | 2 | 3 | 4 | 1 | 3 | 0 | 3 | 2 | 3 | 4 | 1 | 3 | 0 | 3 | 2 | 3 | 4 | 3 | 3 | 0 | 3 | 2 | 3 | 4 |

| 206 | 4 | 3 | 0 | 5 | 4 | 5 | 4 | 4 | 4 | 0 | 5 | 4 | 5 | 4 | 4 | 4 | 0 | 5 | 4 | 5 | 4 | 4 | 4 | 0 | 5 | 4 | 5 | 4 | 4 | 3 | 0 | 5 | 4 | 5 | 4 |

| 207 | 4 | 5 | 0 | 0 | 0 | 0 | 0 | 3 | 5 | 0 | 0 | 0 | 0 | 0 | 3 | 5 | 0 | 0 | 0 | 0 | 0 | 3 | 5 | 0 | 0 | 0 | 0 | 0 | 4 | 5 | 0 | 0 | 0 | 0 | 0 |

| 208 | 4 | 2 | 0 | 3 | 4 | 3 | 0 | 3 | 2 | 0 | 3 | 4 | 3 | 0 | 4 | 4 | 0 | 4 | 4 | 4 | 0 | 4 | 4 | 0 | 4 | 4 | 4 | 0 | 4 | 2 | 0 | 3 | 4 | 3 | 0 |

| 209 | 3 | 4 | 3 | 5 | 0 | 5 | 0 | 2 | 2 | 2 | 3 | 0 | 3 | 0 | 2 | 2 | 2 | 3 | 0 | 3 | 0 | 2 | 2 | 2 | 3 | 0 | 3 | 0 | 3 | 4 | 3 | 5 | 0 | 5 | 0 |

| 210 | 2 | 4 | 0 | 0 | 4 | 0 | 4 | 1 | 2 | 0 | 0 | 3 | 0 | 3 | 1 | 2 | 0 | 0 | 3 | 0 | 3 | 1 | 2 | 0 | 0 | 3 | 0 | 3 | 2 | 4 | 0 | 0 | 4 | 0 | 4 |

| 211 | 4 | 3 | 0 | 0 | 0 | 0 | 4 | 3 | 3 | 0 | 0 | 0 | 0 | 3 | 3 | 3 | 0 | 0 | 0 | 0 | 3 | 3 | 3 | 0 | 0 | 0 | 0 | 3 | 4 | 3 | 0 | 0 | 0 | 0 | 4 |

| 212 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 213 | 2 | 3 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 2 | 3 | 0 | 0 | 0 | 0 | 0 |

| 214 | 2 | 4 | 0 | 4 | 3 | 4 | 4 | 2 | 1 | 0 | 1 | 2 | 1 | 1 | 2 | 1 | 0 | 1 | 2 | 1 | 1 | 2 | 1 | 0 | 1 | 2 | 1 | 1 | 2 | 4 | 0 | 4 | 3 | 4 | 4 |

| 215 | 4 | 4 | 0 | 3 | 0 | 3 | 4 | 3 | 4 | 0 | 3 | 0 | 3 | 4 | 3 | 4 | 0 | 3 | 0 | 3 | 4 | 3 | 4 | 0 | 3 | 0 | 3 | 4 | 4 | 4 | 0 | 3 | 0 | 3 | 4 |

| 216 | 2 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 2 | 1 | 0 | 0 | 0 | 0 | 0 |

| 217 | 4 | 4 | 0 | 4 | 5 | 4 | 0 | 4 | 3 | 0 | 4 | 5 | 4 | 0 | 4 | 3 | 0 | 4 | 5 | 4 | 0 | 4 | 3 | 0 | 4 | 5 | 4 | 0 | 4 | 4 | 0 | 4 | 5 | 4 | 0 |

| Governance Risks | Operational Risks | Human Resources Risks | Financial Risks | ICT Risks | Capital Adequacy Risks | Financial Crime Risks | Governance Risks | Operational Risks | Human Resources Risks | Financial Risks | ICT Risks | Capital Adequacy Risks | Financial Crime Risks | Governance Risks | Operational Risks | Human Resources Risks | Financial Risks | ICT Risks | Capital Adequacy Risks | Financial Crime Risks | Governance Risks | Operational Risks | Human Resources Risks | Financial Risks | ICT Risks | Capital Adequacy Risks | Financial Crime Risks | Governance Risks | Operational Risks | Human Resources Risks | Financial Risks | ICT Risks | Capital Adequacy Risks | Financial Crime Risks | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Respondent 1 | Respondent 2 | Respondent 3 | Respondent 4 | Respondent 5 | |||||||||||||||||||||||||||||||

| 1 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 |

| 2 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 |

| 3 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 |

| 4 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 |

| 5 | 0 | 0 | 0 | 4 | 5 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 |

| 6 | 0 | 0 | 0 | 3 | 4 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 |

| 7 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 |

| 8 | 0 | 0 | 0 | 3 | 2 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 |

| 9 | 0 | 0 | 0 | 2 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 |

| 10 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 |

| 11 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 |

| 12 | 4 | 4 | 4 | 4 | 4 | 0 | 0 | 4 | 4 | 4 | 4 | 4 | 0 | 0 | 4 | 4 | 4 | 4 | 4 | 0 | 0 | 4 | 4 | 4 | 4 | 4 | 0 | 0 | 4 | 4 | 4 | 4 | 4 | 0 | 0 |

| 13 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 |

| 14 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 |

| 15 | 0 | 0 | 3 | 0 | 3 | 0 | 0 | 0 | 0 | 3 | 0 | 3 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 3 | 0 | 3 | 0 | 0 |

| 16 | 0 | 0 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 0 |

| 17 | 0 | 0 | 2 | 2 | 2 | 0 | 0 | 0 | 0 | 2 | 2 | 2 | 0 | 0 | 0 | 0 | 2 | 2 | 2 | 0 | 0 | 0 | 0 | 2 | 2 | 2 | 0 | 0 | 0 | 0 | 3 | 3 | 3 | 0 | 0 |

| 18 | 0 | 3 | 3 | 0 | 3 | 0 | 0 | 0 | 3 | 3 | 0 | 3 | 0 | 0 | 0 | 2 | 2 | 0 | 2 | 0 | 0 | 0 | 2 | 2 | 0 | 2 | 0 | 0 | 0 | 3 | 3 | 0 | 3 | 0 | 0 |

| 19 | 0 | 3 | 3 | 0 | 3 | 0 | 0 | 0 | 3 | 3 | 0 | 4 | 0 | 0 | 0 | 2 | 2 | 0 | 2 | 0 | 0 | 0 | 2 | 2 | 0 | 2 | 0 | 0 | 0 | 3 | 3 | 0 | 3 | 0 | 0 |

| 20 | 0 | 3 | 3 | 3 | 3 | 0 | 0 | 0 | 4 | 2 | 4 | 3 | 0 | 0 | 0 | 3 | 2 | 3 | 3 | 0 | 0 | 0 | 2 | 2 | 3 | 2 | 0 | 0 | 0 | 3 | 3 | 3 | 3 | 0 | 0 |

| 21 | 0 | 4 | 4 | 4 | 4 | 0 | 0 | 0 | 2 | 2 | 1 | 2 | 0 | 0 | 0 | 1 | 1 | 1 | 1 | 0 | 0 | 0 | 1 | 1 | 1 | 1 | 0 | 0 | 0 | 2 | 2 | 2 | 2 | 0 | 0 |

| 22 | 0 | 3 | 3 | 3 | 3 | 3 | 4 | 0 | 3 | 1 | 2 | 2 | 2 | 2 | 0 | 3 | 2 | 2 | 2 | 2 | 2 | 0 | 3 | 2 | 2 | 2 | 2 | 2 | 0 | 3 | 3 | 3 | 3 | 3 | 2 |

| 23 | 0 | 3 | 0 | 3 | 3 | 0 | 0 | 0 | 2 | 0 | 3 | 3 | 0 | 0 | 0 | 2 | 0 | 2 | 2 | 0 | 0 | 0 | 2 | 0 | 2 | 2 | 0 | 0 | 0 | 3 | 0 | 3 | 3 | 0 | 0 |

| 24 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 |

| 25 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 |

| 26 | 0 | 1 | 0 | 0 | 1 | 0 | 1 | 0 | 1 | 0 | 0 | 1 | 0 | 1 | 0 | 1 | 0 | 0 | 1 | 0 | 1 | 0 | 1 | 0 | 0 | 1 | 0 | 1 | 0 | 2 | 0 | 0 | 2 | 0 | 2 |

| 27 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 |

| 28 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 |

| 29 | 0 | 3 | 0 | 3 | 3 | 3 | 3 | 0 | 2 | 0 | 3 | 3 | 3 | 2 | 0 | 2 | 0 | 2 | 2 | 2 | 2 | 0 | 2 | 0 | 2 | 2 | 2 | 2 | 0 | 2 | 0 | 2 | 2 | 2 | 2 |

| 30 | 0 | 4 | 0 | 0 | 4 | 0 | 0 | 0 | 3 | 0 | 0 | 3 | 0 | 0 | 0 | 2 | 0 | 0 | 2 | 0 | 0 | 0 | 2 | 0 | 0 | 2 | 0 | 0 | 0 | 3 | 0 | 0 | 3 | 0 | 0 |

| 31 | 0 | 3 | 0 | 0 | 3 | 0 | 0 | 0 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 2 | 0 | 0 | 2 | 0 | 0 |

| 32 | 0 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 3 | 0 | 0 | 3 | 0 | 0 | 0 | 2 | 0 | 0 | 2 | 0 | 0 | 0 | 2 | 0 | 0 | 2 | 0 | 0 | 0 | 3 | 0 | 0 | 3 | 0 | 0 |

| 33 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 |

| 34 | 0 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 2 | 0 | 0 | 0 | 1 | 0 | 1 | 2 | 0 | 0 | 0 | 1 | 0 | 1 | 2 | 0 | 0 | 0 | 2 | 0 | 2 | 2 | 0 | 0 |

| 35 | 0 | 4 | 1 | 0 | 1 | 0 | 0 | 0 | 3 | 2 | 0 | 2 | 0 | 0 | 0 | 2 | 2 | 0 | 2 | 0 | 0 | 0 | 2 | 2 | 0 | 2 | 0 | 0 | 0 | 3 | 3 | 0 | 3 | 0 | 0 |

| 36 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 |

| 37 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 |

| 38 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 |

| 39 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 |

| 40 | 0 | 1 | 0 | 1 | 1 | 1 | 0 | 0 | 2 | 0 | 2 | 3 | 2 | 0 | 0 | 2 | 0 | 2 | 2 | 2 | 0 | 0 | 2 | 0 | 2 | 2 | 2 | 0 | 0 | 2 | 0 | 2 | 2 | 2 | 0 |

| 41 | 0 | 0 | 0 | 2 | 2 | 2 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 |

| 42 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 |

| 43 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 |

| 44 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 |

| 45 | 3 | 3 | 3 | 3 | 3 | 3 | 0 | 2 | 3 | 2 | 2 | 2 | 2 | 0 | 1 | 1 | 1 | 2 | 2 | 2 | 0 | 1 | 1 | 1 | 2 | 2 | 2 | 0 | 2 | 2 | 2 | 2 | 2 | 2 | 0 |

| 46 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 |

| 47 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 |

| 48 | 4 | 4 | 4 | 4 | 4 | 4 | 4 | 3 | 4 | 2 | 4 | 4 | 4 | 4 | 3 | 3 | 2 | 3 | 3 | 3 | 4 | 3 | 3 | 2 | 3 | 3 | 3 | 4 | 3 | 3 | 1 | 3 | 3 | 3 | 4 |

| 49 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 50 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 51 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 52 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 53 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 54 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 55 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 56 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 57 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 58 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 59 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 60 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 61 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 62 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 63 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 64 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 65 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 66 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 67 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 68 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 69 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 70 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| 71 | 5 | 0 | 0 | 5 | 0 | 5 | 5 | 2 | 0 | 0 | 2 | 0 | 2 | 2 | 2 | 0 | 0 | 2 | 0 | 2 | 2 | 2 | 0 | 0 | 2 | 0 | 2 | 2 | 2 | 0 | 0 | 2 | 0 | 2 | 2 |

| 72 | 5 | 0 | 0 | 5 | 0 | 5 | 5 | 2 | 0 | 0 | 2 | 0 | 2 | 2 | 2 | 0 | 0 | 2 | 0 | 2 | 2 | 2 | 0 | 0 | 2 | 0 | 2 | 2 | 2 | 0 | 0 | 2 | 0 | 2 | 2 |

| 73 | 3 | 0 | 0 | 3 | 0 | 3 | 3 | 2 | 0 | 0 | 2 | 0 | 2 | 2 | 2 | 0 | 0 | 2 | 0 | 2 | 2 | 2 | 0 | 0 | 2 | 0 | 2 | 2 | 2 | 0 | 0 | 2 | 0 | 2 | 2 |

| 74 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 4 | 0 | 0 | 0 | 0 | 0 | 4 | 4 | 0 | 0 | 0 | 0 | 0 | 4 | 4 | 0 | 0 | 0 | 0 | 0 | 4 | 2 | 0 | 0 | 0 | 0 | 0 | 2 |

| 75 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 1 | 0 | 0 | 0 | 0 | 0 | 1 |

| 76 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 3 | 0 | 0 | 0 | 0 | 0 | 3 | 1 | 0 | 0 | 0 | 0 | 0 | 1 |

| 77 | 5 | 0 | 0 | 5 | 0 | 5 | 5 | 3 | 0 | 0 | 3 | 0 | 3 | 3 | 3 | 0 | 0 | 3 | 0 | 3 | 3 | 3 | 0 | 0 | 3 | 0 | 3 | 3 | 1 | 0 | 0 | 1 | 0 | 1 | 1 |

| 78 | 5 | 0 | 0 | 5 | 0 | 5 | 5 | 3 | 0 | 0 | 3 | 0 | 3 | 3 | 3 | 0 | 0 | 3 | 0 | 3 | 3 | 3 | 0 | 0 | 3 | 0 | 3 | 3 | 1 | 0 | 0 | 1 | 0 | 1 | 1 |

| 79 | 1 | 0 | 0 | 1 | 0 | 1 | 1 | 1 | 0 | 0 | 1 | 0 | 1 | 1 | 1 | 0 | 0 | 1 | 0 | 1 | 1 | 1 | 0 | 0 | 1 | 0 | 1 | 1 | 1 | 0 | 0 | 1 | 0 | 1 | 1 |

| 80 | 0 | 0 | 0 | 5 | 0 | 5 | 5 | 0 | 0 | 0 | 4 | 0 | 4 | 4 | 0 | 0 | 0 | 4 | 0 | 4 | 4 | 0 | 0 | 0 | 4 | 0 | 4 | 4 | 0 | 0 | 0 | 4 | 0 | 4 | 4 |

| 81 | 0 | 0 | 0 | 5 | 0 | 5 | 5 | 0 | 0 | 0 | 4 | 0 | 4 | 4 | 0 | 0 | 0 | 4 | 0 | 4 | 4 | 0 | 0 | 0 | 4 | 0 | 4 | 4 | 0 | 0 | 0 | 4 | 0 | 4 | 4 |

| 82 | 0 | 0 | 0 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 1 |

| 83 | 0 | 0 | 0 | 3 | 0 | 3 | 3 | 0 | 0 | 0 | 3 | 0 | 3 | 3 | 0 | 0 | 0 | 3 | 0 | 3 | 3 | 0 | 0 | 0 | 3 | 0 | 3 | 3 | 0 | 0 | 0 | 3 | 0 | 3 | 3 |