Global Collective Dynamics of Financial Market Efficiency Using Attention Entropy with Hierarchical Clustering

Abstract

:1. Introduction

2. Literature Review

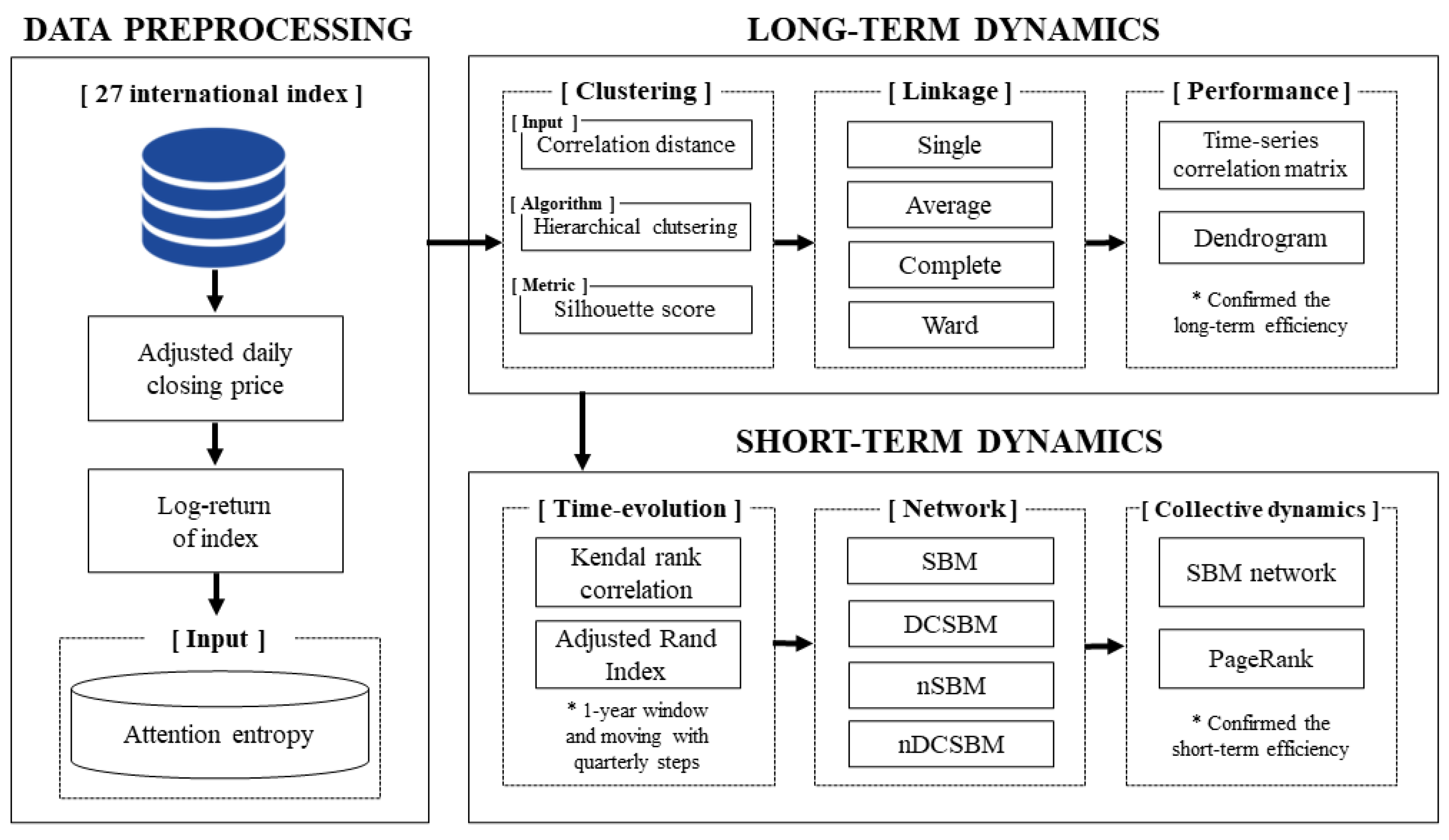

3. Methods

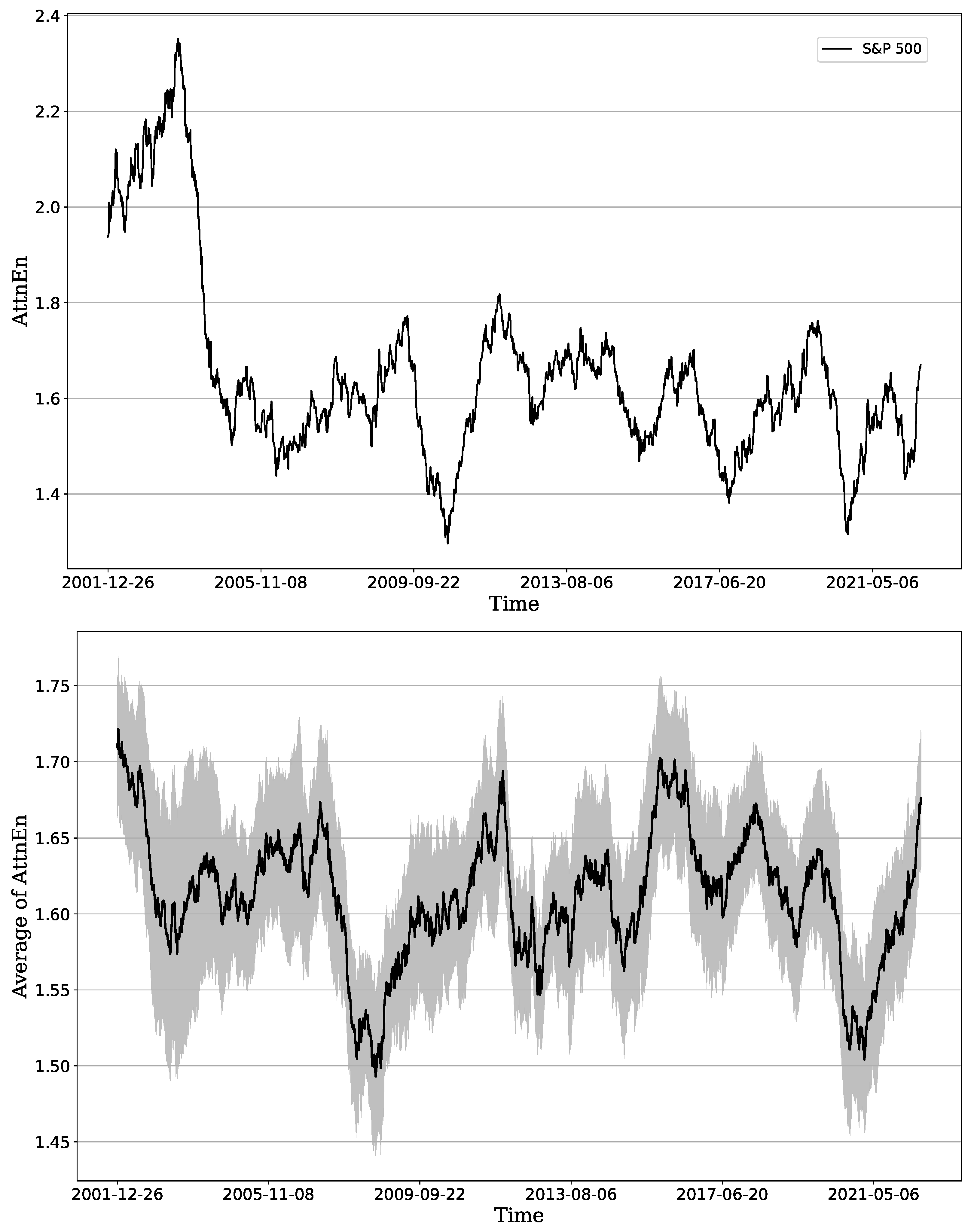

3.1. Attention Entropy

3.2. Hierarchical Clustering

3.3. Stochastic Block Model (SBM)

4. Experiments and Data

4.1. Experiments

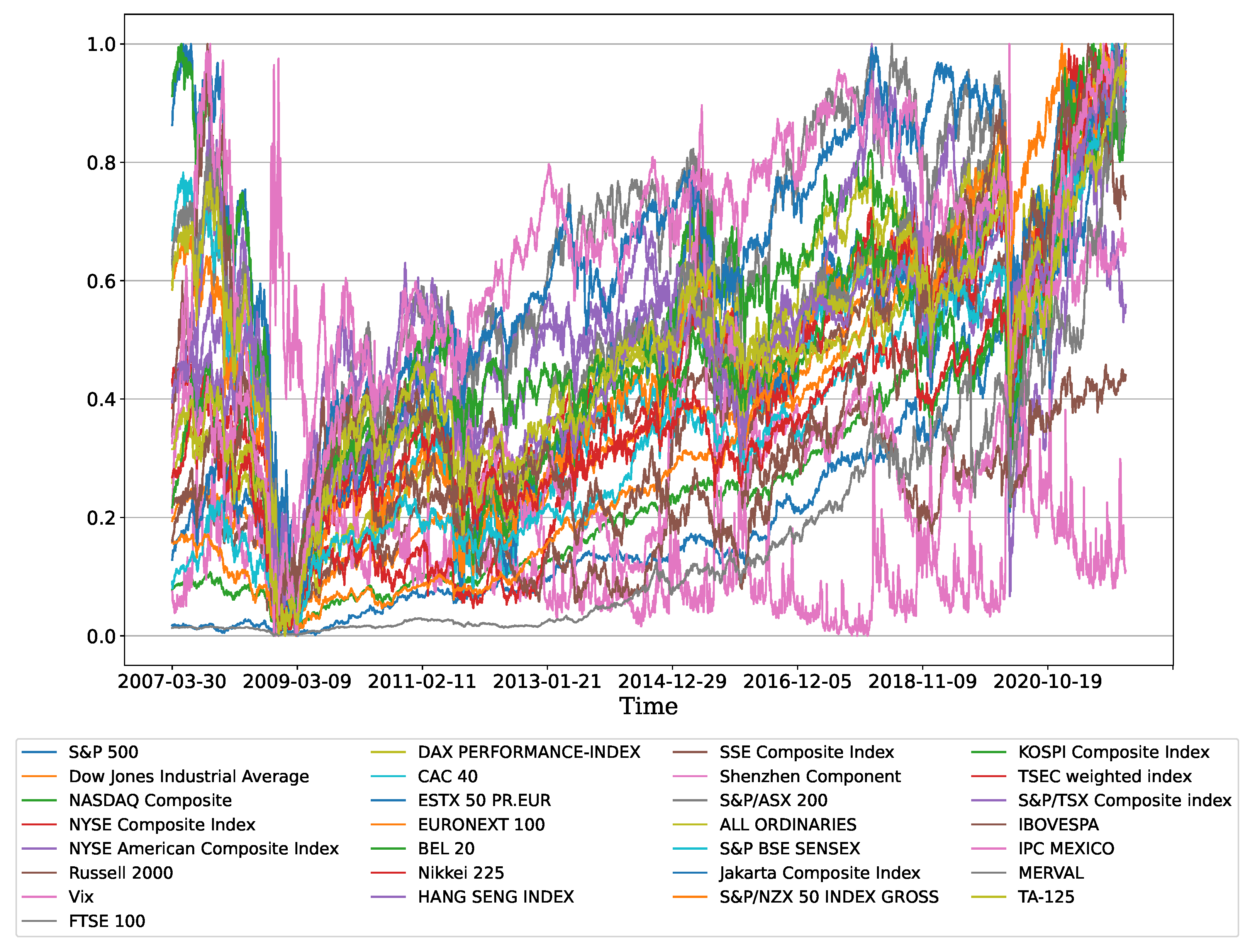

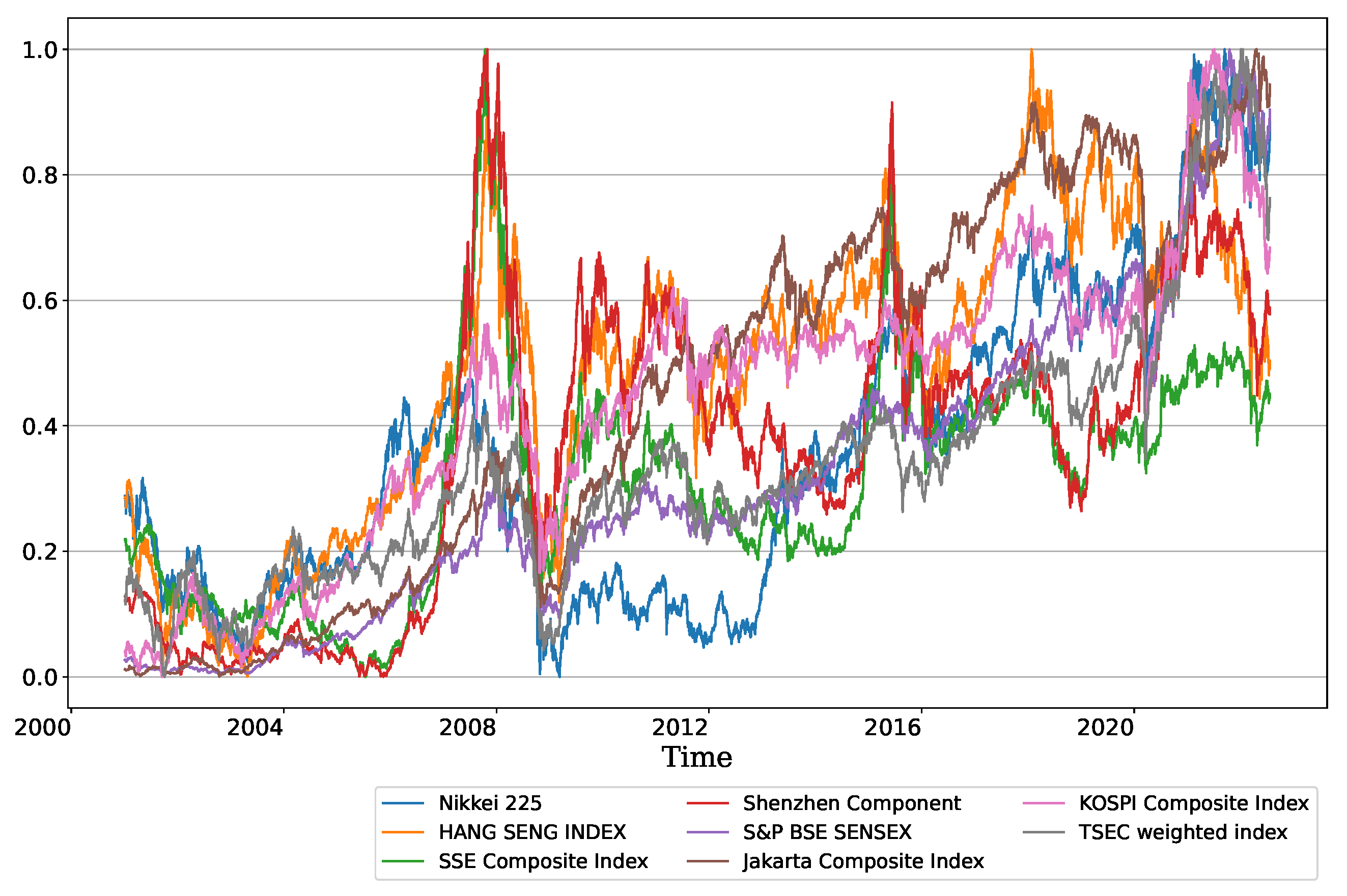

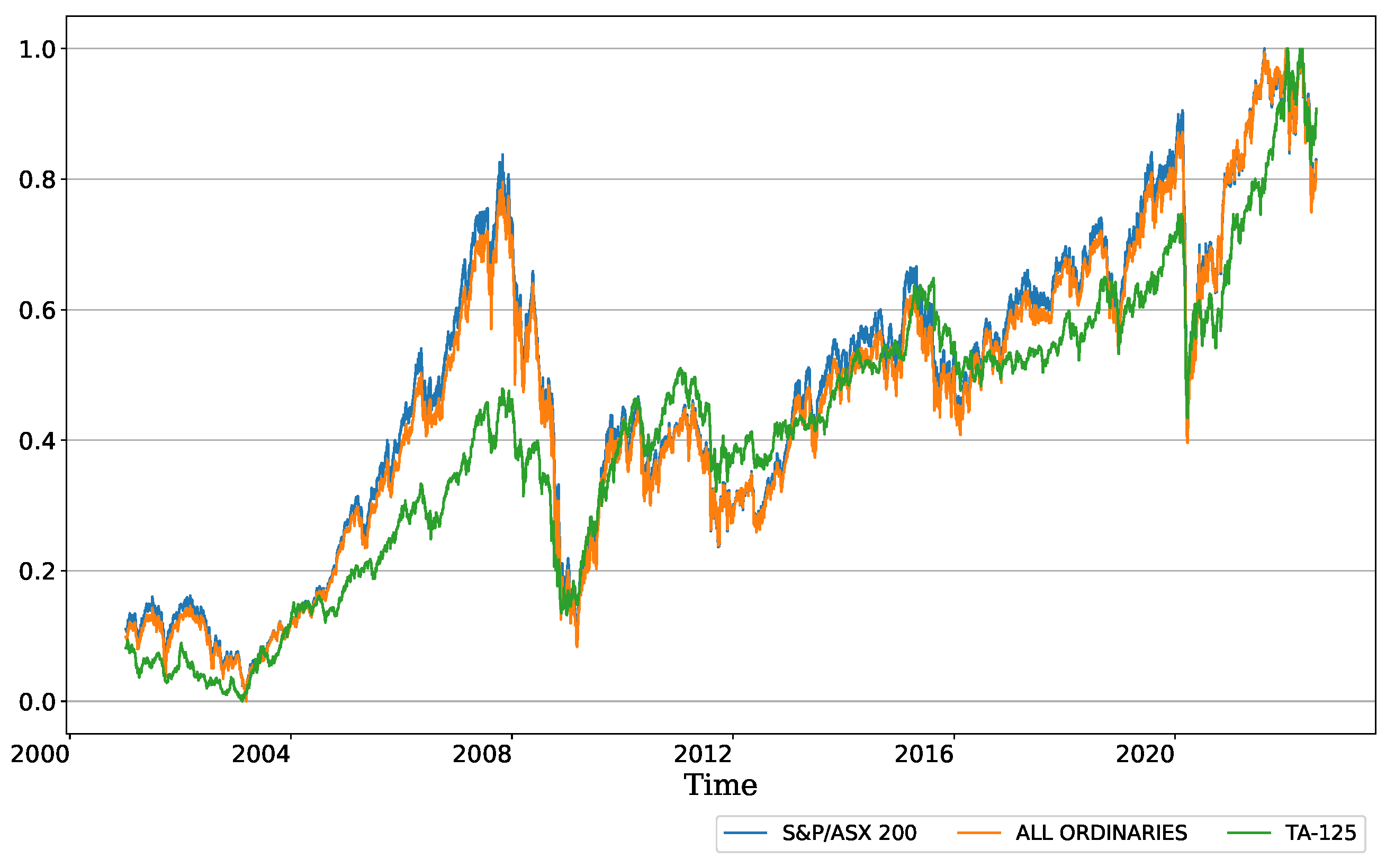

4.2. Data

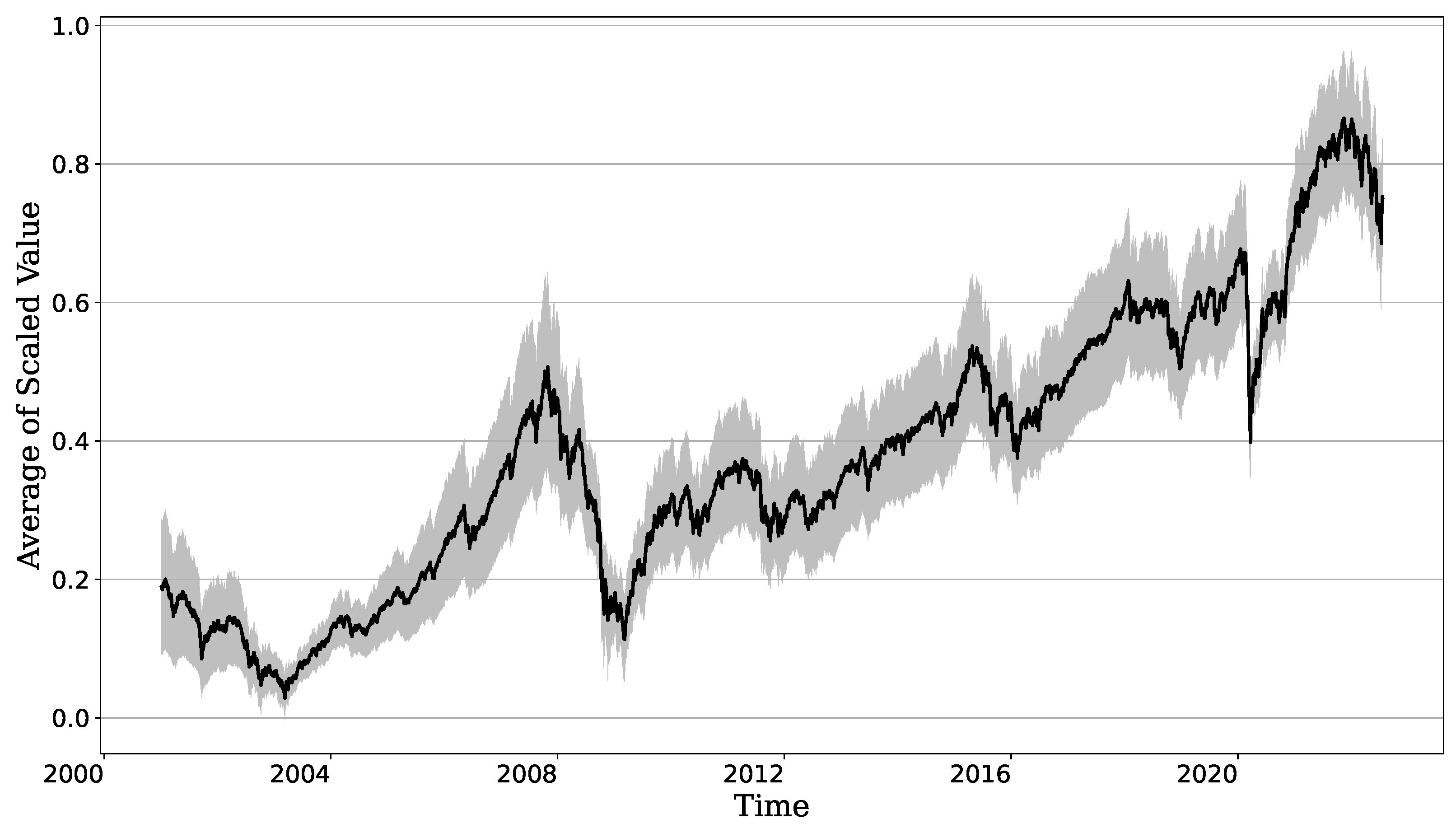

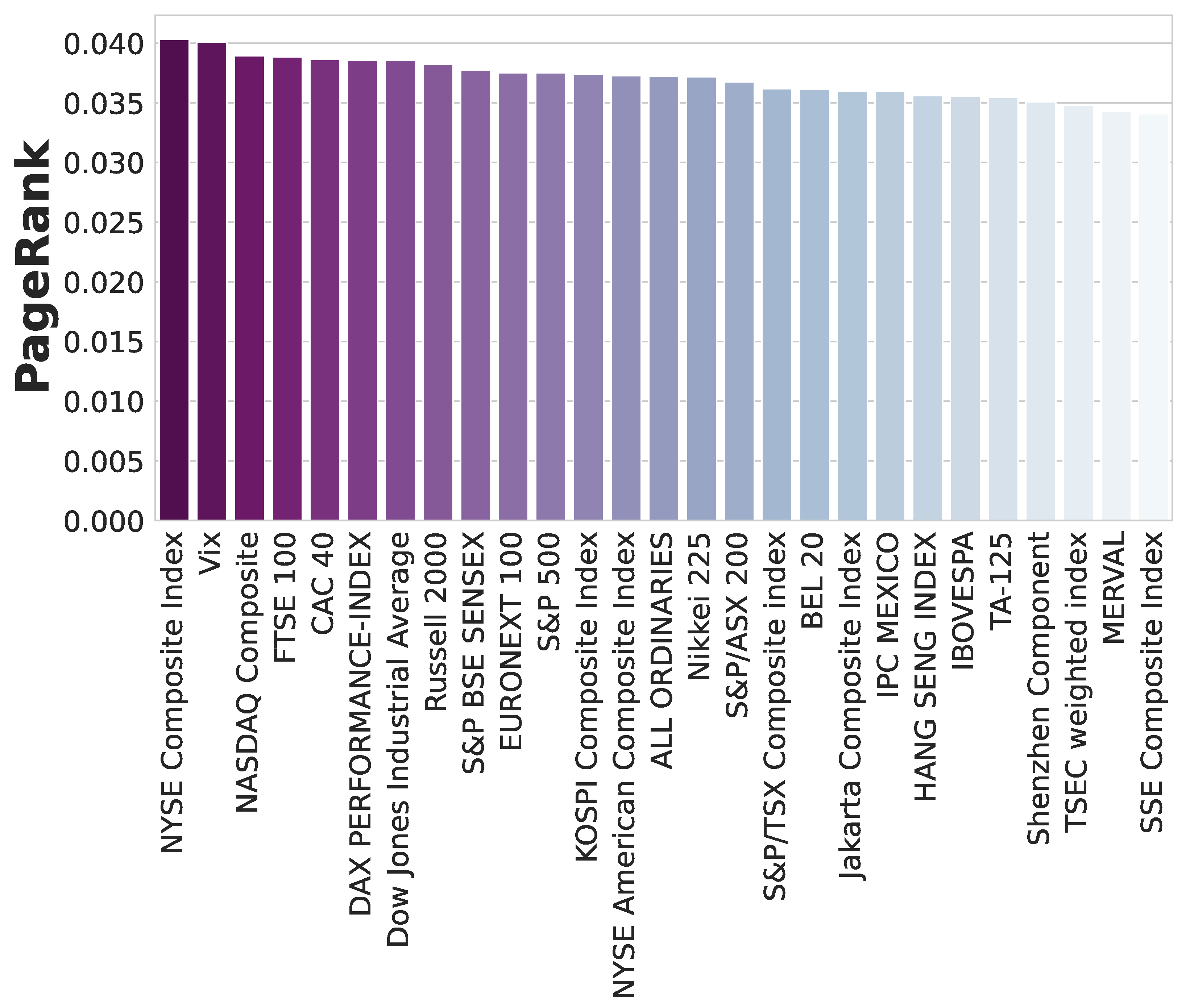

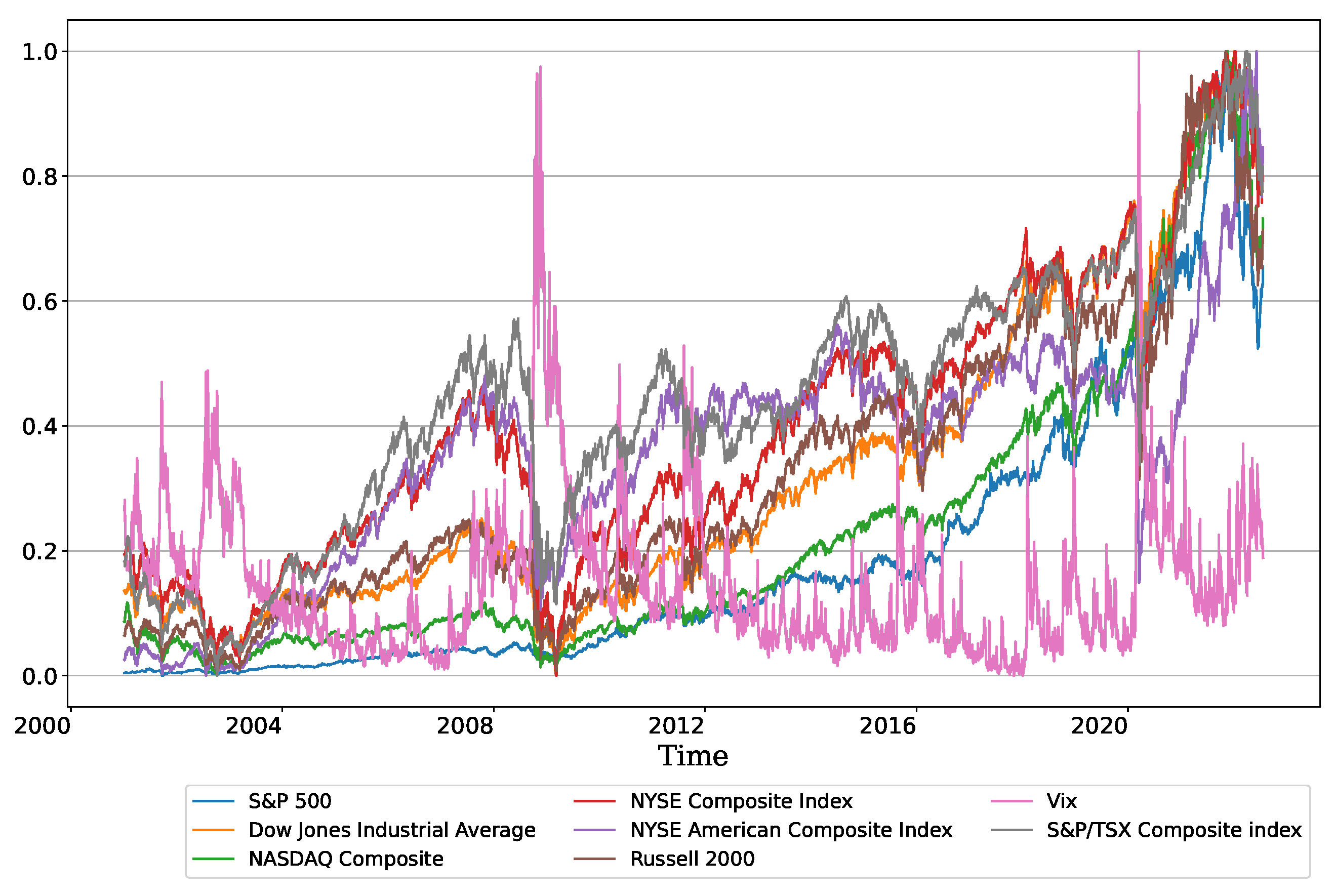

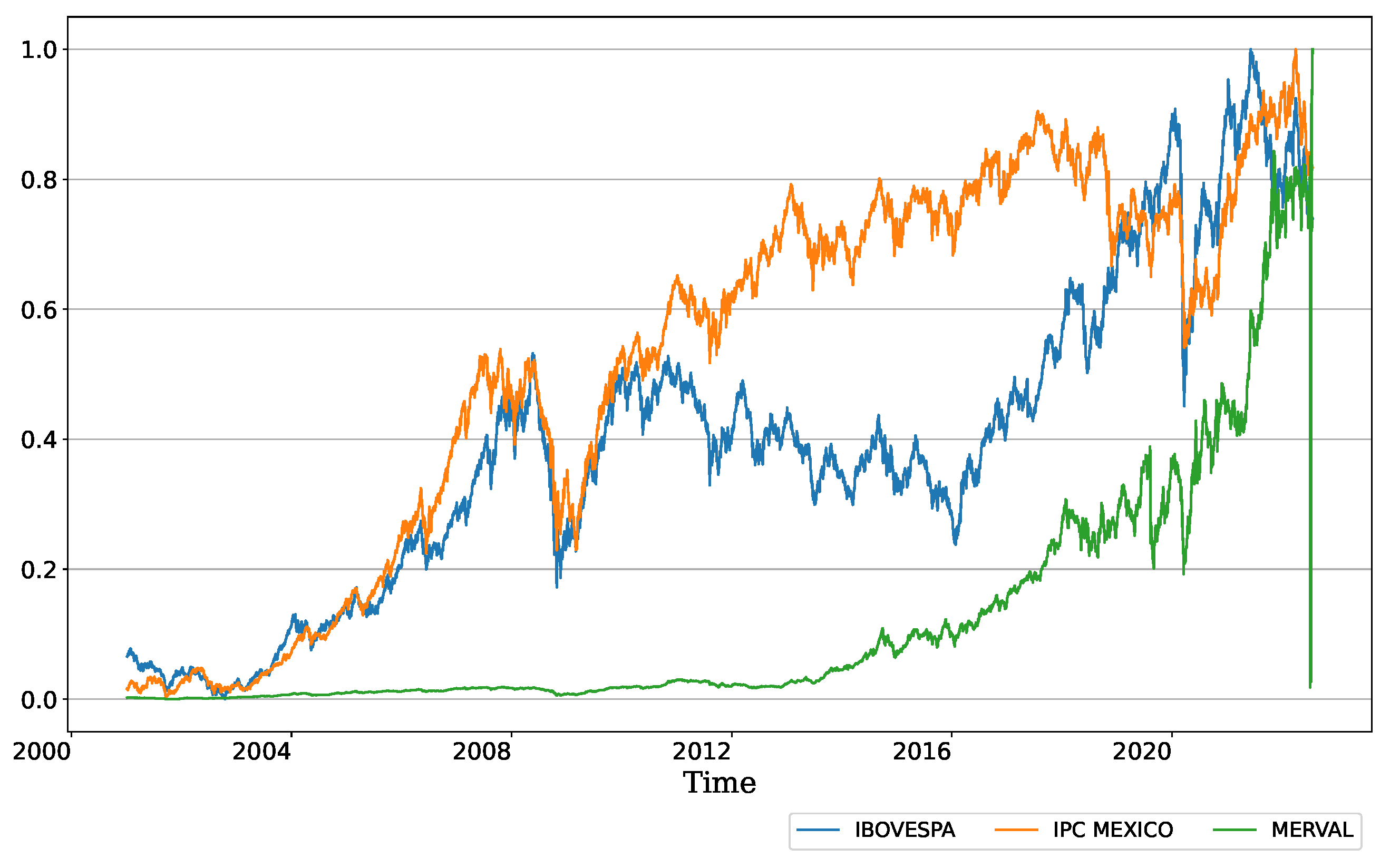

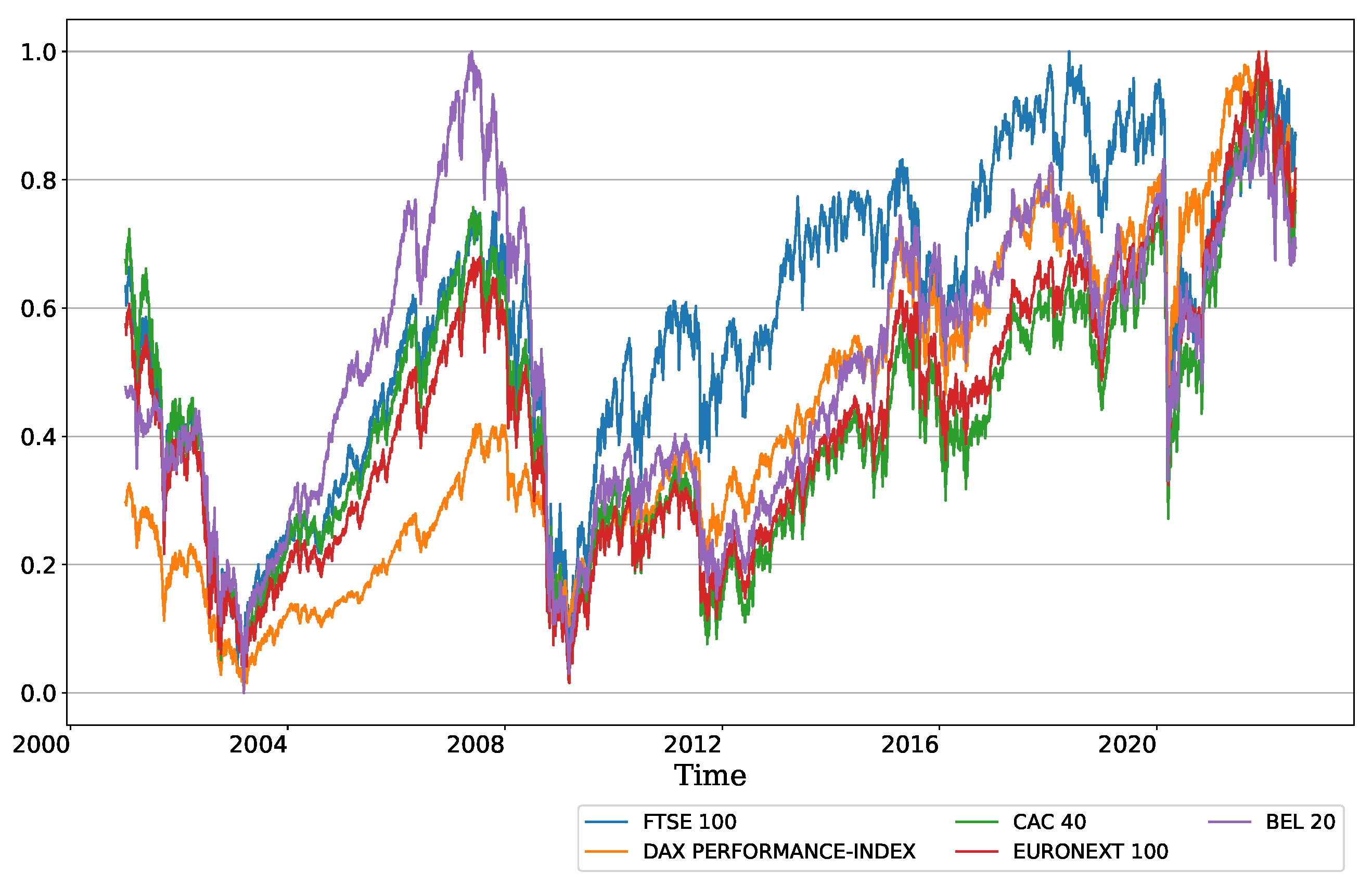

5. Results

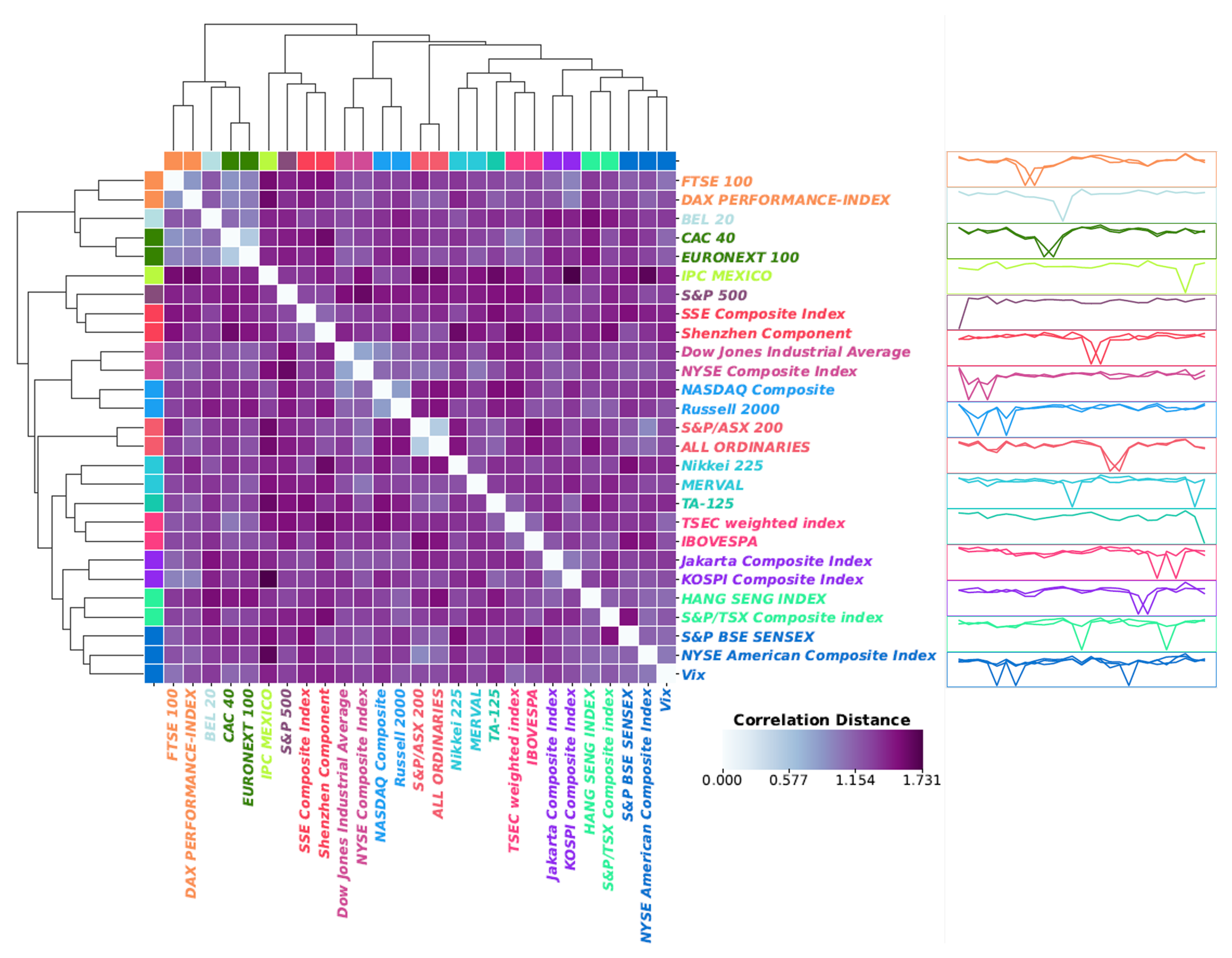

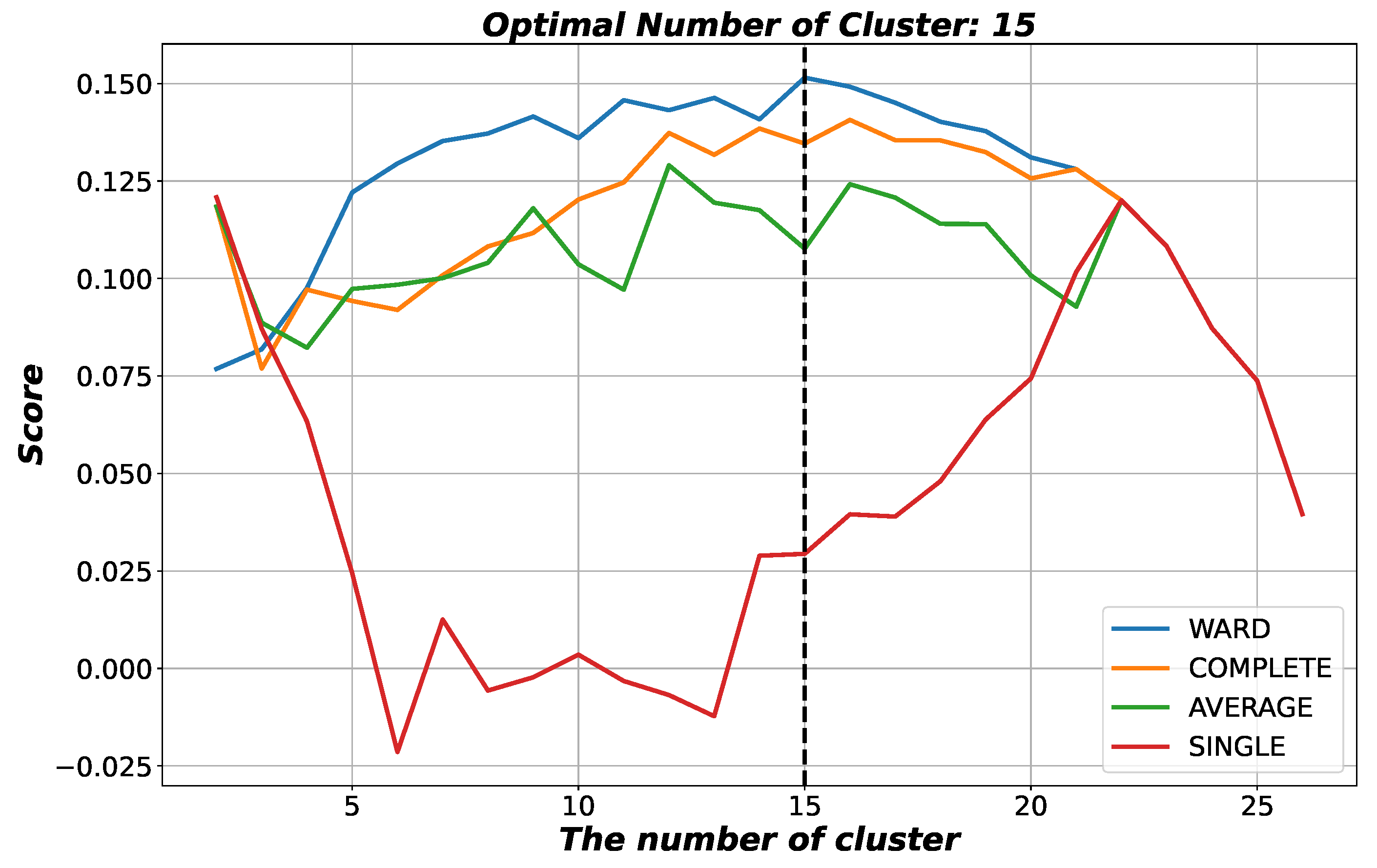

5.1. Long-Term Efficiency with Clustering

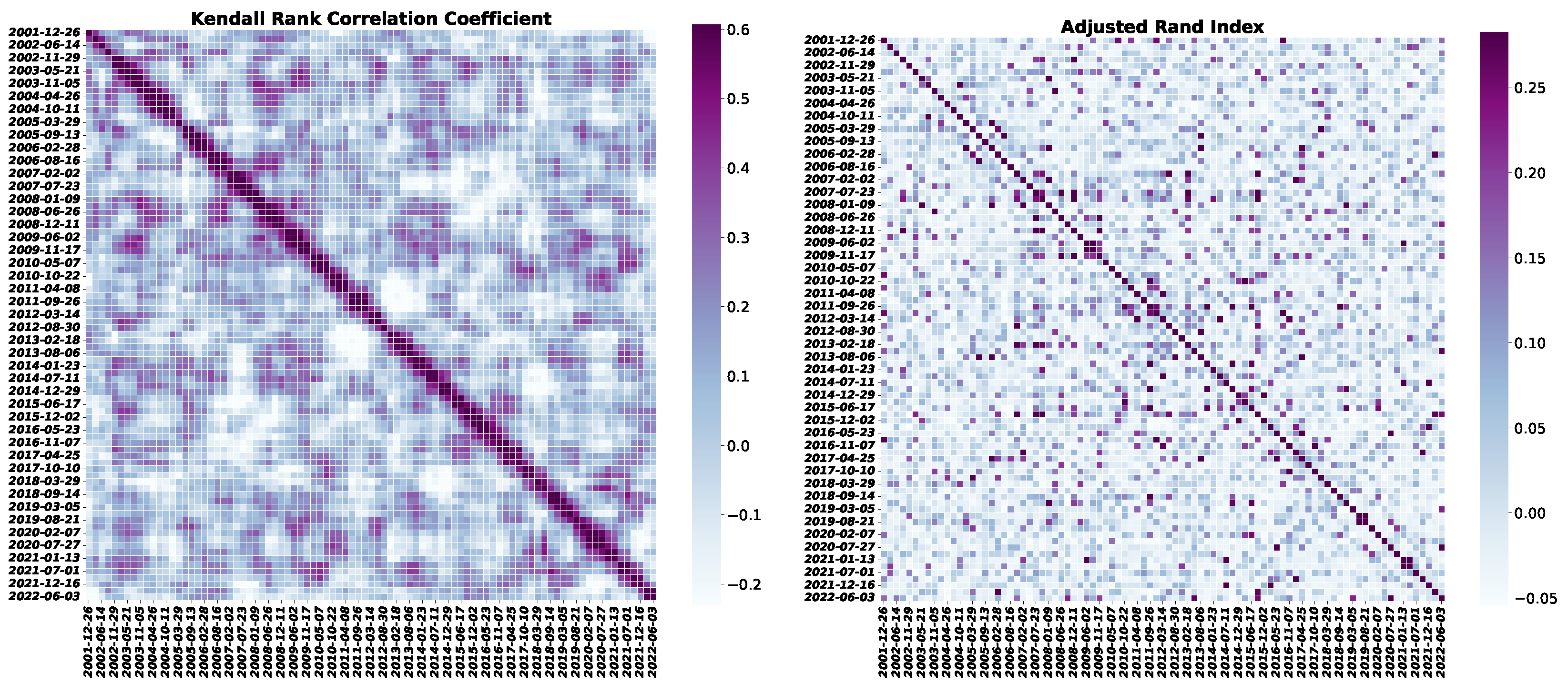

5.2. Short-Term Efficiency with Sliding Window

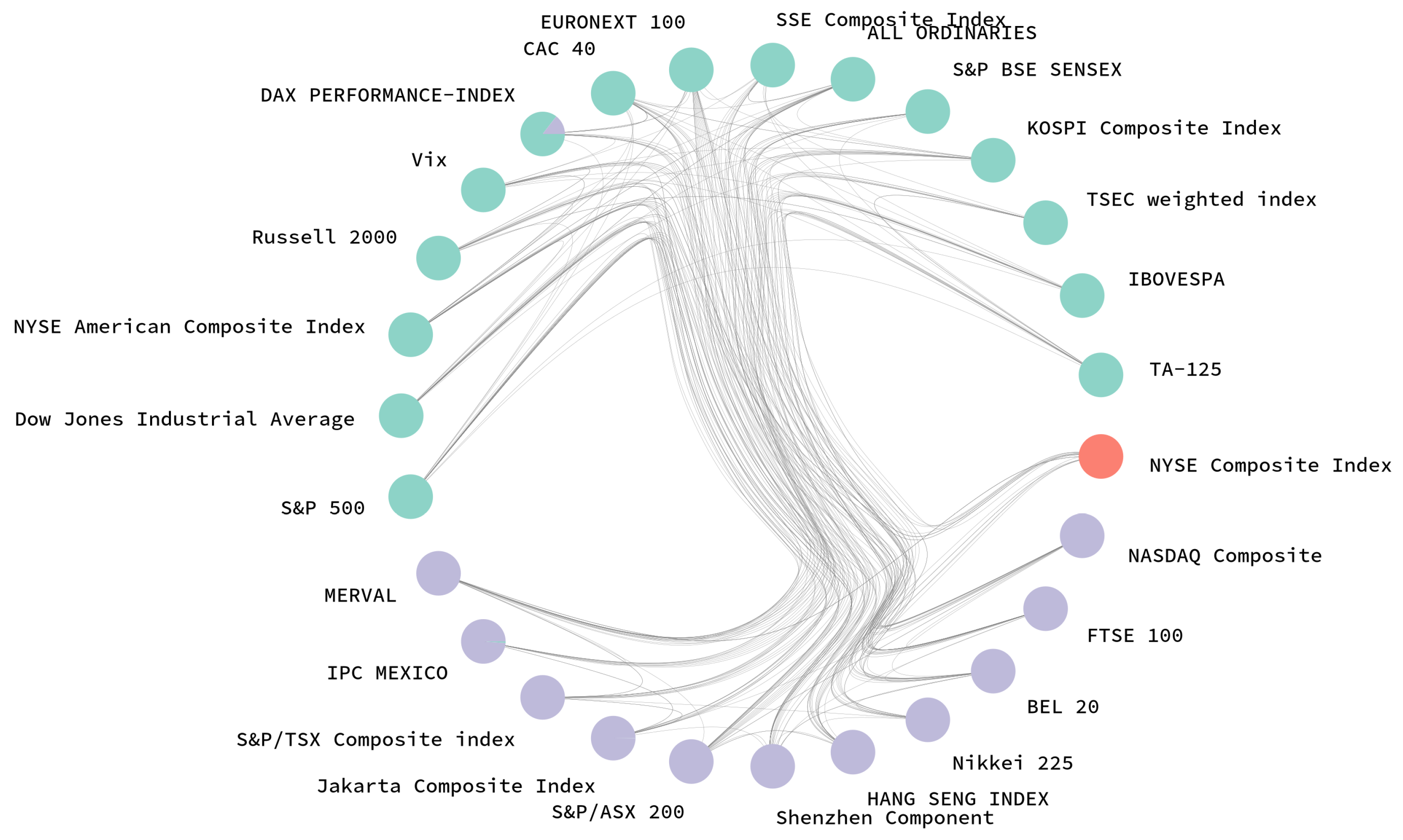

5.3. Short-Term Efficiency with SBM Network

6. Discussion and Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

References

- Cootner, P.H. The Random Character of Stock Market Prices; MIT Press: Cambridge, MA, USA, 1964. [Google Scholar]

- Fama, E.F. Efficient capital markets: A review of theory and empirical work. J. Financ. 1970, 25, 383–417. [Google Scholar] [CrossRef]

- Fama, E.F. The behavior of stock-market prices. J. Bus. 1965, 38, 34–105. [Google Scholar] [CrossRef] [Green Version]

- Malkiel, B.G. The efficient market hypothesis and its critics. J. Econ. Perspect. 2003, 17, 59–82. [Google Scholar] [CrossRef] [Green Version]

- Sornette, D. Why Stock Markets Crash: Critical Events in Complex Financial Systems; Princeton University Press: Princeton, NJ, USA, 2003. [Google Scholar]

- Stanley, H.E.; Amaral, L.A.; Gabaix, X.; Gopikrishnan, P.; Plerou, V. Similarities and differences between physics and economics. Phys. Stat. Mech. Appl. 2001, 299, 1–15. [Google Scholar] [CrossRef] [Green Version]

- Gopikrishnan, P.; Plerou, V.; Amaral, L.A.N.; Meyer, M.; Stanley, H.E. Scaling of the distribution of fluctuations of financial market indices. Phys. Rev. E 1999, 60, 5305. [Google Scholar] [CrossRef] [Green Version]

- Mantegna, R.N.; Stanley, H.E. Scaling behaviour in the dynamics of an economic index. Nature 1995, 376, 46–49. [Google Scholar] [CrossRef]

- Johansen, A.; Ledoit, O.; Sornette, D. Crashes as critical points. Int. J. Theor. Appl. Financ. 2000, 3, 219–255. [Google Scholar] [CrossRef]

- Preis, T.; Moat, H.S.; Stanley, H.E. Quantifying trading behavior in financial markets using Google Trends. Sci. Rep. 2013, 3, 1–6. [Google Scholar] [CrossRef] [Green Version]

- Preis, T.; Stanley, H.E. Bubble trouble. Phys. World 2011, 24, 29–32. [Google Scholar] [CrossRef]

- Sornette, D. Predictability of catastrophic events: Material rupture, earthquakes, turbulence, financial crashes, and human birth. Proc. Natl. Acad. Sci. USA 2002, 99, 2522–2529. [Google Scholar] [CrossRef]

- Lim, K.P.; Brooks, R. The evolution of stock market efficiency over time: A survey of the empirical literature. J. Econ. Surv. 2011, 25, 69–108. [Google Scholar] [CrossRef]

- Lo, A.W.; MacKinlay, A.C. The size and power of the variance ratio test in finite samples: A Monte Carlo investigation. J. Econom. 1989, 40, 203–238. [Google Scholar] [CrossRef]

- Lo, A.W. The adaptive markets hypothesis. J. Portf. Manag. 2004, 30, 15–29. [Google Scholar] [CrossRef]

- Urquhart, A.; McGroarty, F. Are stock markets really efficient? Evidence of the adaptive market hypothesis. Int. Rev. Financ. Anal. 2016, 47, 39–49. [Google Scholar] [CrossRef] [Green Version]

- Ito, M.; Noda, A.; Wada, T. The evolution of stock market efficiency in the US: A non-Bayesian time-varying model approach. Appl. Econ. 2016, 48, 621–635. [Google Scholar] [CrossRef] [Green Version]

- Noda, A. A test of the adaptive market hypothesis using a time-varying AR model in Japan. Financ. Res. Lett. 2016, 17, 66–71. [Google Scholar] [CrossRef] [Green Version]

- Zunino, L.; Tabak, B.M.; Pérez, D.G.; Garavaglia, M.; Rosso, O.A. Inefficiency in Latin-American market indices. Eur. Phys. J. B 2007, 60, 111–121. [Google Scholar] [CrossRef]

- Zunino, L.; Zanin, M.; Tabak, B.M.; Pérez, D.G.; Rosso, O.A. Forbidden patterns, permutation entropy and stock market inefficiency. Phys. Stat. Mech. Appl. 2009, 388, 2854–2864. [Google Scholar] [CrossRef]

- Zunino, L.; Bariviera, A.F.; Guercio, M.B.; Martinez, L.B.; Rosso, O.A. On the efficiency of sovereign bond markets. Phys. Stat. Mech. Appl. 2012, 391, 4342–4349. [Google Scholar] [CrossRef] [Green Version]

- Rocha Filho, T.M.; Rocha, P.M. Evidence of inefficiency of the Brazilian stock market: The IBOVESPA future contracts. Phys. Stat. Mech. Appl. 2020, 543, 123200. [Google Scholar] [CrossRef]

- Sánchez-Granero, M.; Balladares, K.; Ramos-Requena, J.; Trinidad-Segovia, J. Testing the efficient market hypothesis in Latin American stock markets. Phys. Stat. Mech. Appl. 2020, 540, 123082. [Google Scholar] [CrossRef]

- Szarek, D.; Bielak, Ł.; Wyłomańska, A. Long-term prediction of the metals’ prices using non-Gaussian time-inhomogeneous stochastic process. Phys. Stat. Mech. Appl. 2020, 555, 124659. [Google Scholar] [CrossRef]

- Yang, J.; Choudhary, G.I.; Rahardja, S.; Franti, P. Classification of interbeat interval time-series using attention entropy. IEEE Trans. Affect. Comput. 2020. [Google Scholar] [CrossRef]

- Pedregosa, F.; Varoquaux, G.; Gramfort, A.; Michel, V.; Thirion, B.; Grisel, O.; Blondel, M.; Prettenhofer, P.; Weiss, R.; Dubourg, V.; et al. Scikit-learn: Machine learning in Python. J. Mach. Learn. Res. 2011, 12, 2825–2830. [Google Scholar]

- Virtanen, P.; Gommers, R.; Oliphant, T.E.; Haberland, M.; Reddy, T.; Cournapeau, D.; Burovski, E.; Peterson, P.; Weckesser, W.; Bright, J.; et al. SciPy 1.0: Fundamental algorithms for scientific computing in Python. Nat. Methods 2020, 17, 261–272. [Google Scholar] [CrossRef] [Green Version]

- Gaio, L.E.; Stefanelli, N.O.; Pimenta, T.; Bonacim, C.A.G.; Gatsios, R.C. The impact of the Russia-Ukraine conflict on market efficiency: Evidence for the developed stock market. Financ. Res. Lett. 2022, 50, 103302. [Google Scholar] [CrossRef]

- Hkiri, B.; Béjaoui, A.; Gharib, C.; AlNemer, H.A. Revisiting efficiency in MENA stock markets during political shocks: Evidence from a multi-step approach. Heliyon 2021, 7, e08028. [Google Scholar] [CrossRef]

- Espinosa-Paredes, G.; Rodriguez, E.; Alvarez-Ramirez, J. A singular value decomposition entropy approach to assess the impact of COVID-19 on the informational efficiency of the WTI crude oil market. Chaos Solitons Fractals 2022, 160, 112238. [Google Scholar] [CrossRef]

- Wang, X. Efficient markets are more connected: An entropy-based analysis of the energy, industrial metal and financial markets. Energy Econ. 2022, 111, 106067. [Google Scholar] [CrossRef]

- Shternshis, A.; Mazzarisi, P.; Marmi, S. Measuring market efficiency: The Shannon entropy of high-frequency financial time series. Chaos Solitons Fractals 2022, 162, 112403. [Google Scholar] [CrossRef]

- Dinga, E.; Oprean-Stan, C.; Tănăsescu, C.R.; Brătian, V.; Ionescu, G.M. Entropy-Based Behavioural Efficiency of the Financial Market. Entropy 2021, 23, 1396. [Google Scholar] [CrossRef] [PubMed]

- Choi, S.Y. Analysis of stock market efficiency during crisis periods in the US stock market: Differences between the global financial crisis and COVID-19 pandemic. Phys. Stat. Mech. Appl. 2021, 574, 125988. [Google Scholar] [CrossRef]

- Mensi, W.; Hamdi, A.; Yoon, S.M. Modelling multifractality and efficiency of GCC stock markets using the MF-DFA approach: A comparative analysis of global, regional and Islamic markets. Phys. A Stat. Mech. Appl. 2018, 503, 1107–1116. [Google Scholar] [CrossRef]

- Han, C.; Wang, Y.; Ning, Y. Analysis and comparison of the multifractality and efficiency of Chinese stock market: Evidence from dynamics of major indexes in different boards. Phys. A Stat. Mech. Appl. 2019, 528, 121305. [Google Scholar] [CrossRef]

- Mensi, W.; Tiwari, A.K.; Al-Yahyaee, K.H. An analysis of the weak form efficiency, multifractality and long memory of global, regional and European stock markets. Q. Rev. Econ. Financ. 2019, 72, 168–177. [Google Scholar] [CrossRef]

- Cho, P.; Lee, M. Forecasting the Volatility of the Stock Index with Deep Learning Using Asymmetric Hurst Exponents. Fractal Fract. 2022, 6, 394. [Google Scholar] [CrossRef]

- Mensi, W.; Vo, X.V.; Kang, S.H. Upward/downward multifractality and efficiency in metals futures markets: The impacts of financial and oil crises. Resour. Policy 2022, 76, 102645. [Google Scholar] [CrossRef]

- Zhuang, X.; Wei, D. Asymmetric multifractality, comparative efficiency analysis of green finance markets: A dynamic study by index-based model. Phys. A Stat. Mech. Appl. 2022, 604, 127949. [Google Scholar] [CrossRef]

- Bonanno, G.; Caldarelli, G.; Lillo, F.; Micciche, S.; Vandewalle, N.; Mantegna, R.N. Networks of equities in financial markets. Eur. Phys. J. B 2004, 38, 363–371. [Google Scholar] [CrossRef] [Green Version]

- Kuang, P.C. Measuring information flow among international stock markets: An approach of entropy-based networks on multi time-scales. Phys. A Stat. Mech. Appl. 2021, 577, 126068. [Google Scholar] [CrossRef]

- Shin, K.H.; Lim, G.; Min, S. Dynamics of the Global Stock Market Networks Generated by DCCA Methodology. Appl. Sci. 2020, 10, 2171. [Google Scholar] [CrossRef]

- Balcı, M.A.; Batrancea, L.M.; Akgüller, O.; Nichita, A. Coarse Graining on Financial Correlation Networks. Mathematics 2022, 10, 2118. [Google Scholar] [CrossRef]

- Alves, L.G.; Sigaki, H.Y.; Perc, M.; Ribeiro, H.V. Collective dynamics of stock market efficiency. Sci. Rep. 2020, 10, 1–10. [Google Scholar] [CrossRef]

- Shannon, C.E. A mathematical theory of communication. Bell Syst. Tech. J. 1948, 27, 379–423. [Google Scholar] [CrossRef] [Green Version]

- Aranganayagi, S.; Thangavel, K. Clustering Categorical Data Using Silhouette Coefficient as a Relocating Measure. In Proceedings of the International Conference on Computational Intelligence and Multimedia Applications (ICCIMA 2007), Sivakasi, India, 13–15 December 2007; Volume 2, pp. 13–17. [Google Scholar]

- Page, L.; Brin, S.; Motwani, R.; Winograd, T. The PageRank Citation Ranking: Bringing Order to the Web; Technical Report 1999-66; Stanford InfoLab: Stanford, CA, USA, 1999. [Google Scholar]

- Kendall, M.G. A new measure of rank correlation. Biometrika 1938, 30, 81–93. [Google Scholar] [CrossRef]

- Rand, W.M. Objective criteria for the evaluation of clustering methods. J. Am. Stat. Assoc. 1971, 66, 846–850. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mean | Stdev | Skewness | Kurtosis | ARCH (10) | ARCH (20) | Augmented Dickey–Fuller | |

|---|---|---|---|---|---|---|---|

| S&P 500 | 0.07 | 1.55 | 0.16 | 3.53 | 230.1 *** | 250.07 *** | −29.91 *** |

| Dow Jones Industrial Average | 0.03 | 1.22 | −0.49 | 16.05 | 1262.23 *** | 1311.84 *** | −15.14 *** |

| NASDAQ Composite | 0.05 | 1.38 | −0.50 | 9.24 | 998.5 *** | 1045.3 *** | −14.49 *** |

| NYSE Composite Index | 0.02 | 1.32 | −0.68 | 13.41 | 1225.34 *** | 1295.24 *** | −14.79 *** |

| NYSE American Composite Index | 0.01 | 1.31 | −1.00 | 16.49 | 984.88 *** | 1161.64 *** | −15.2 *** |

| Russell 2000 | 0.03 | 1.62 | −0.66 | 8.60 | 1146.88 *** | 1214.77 *** | −14.73 *** |

| Vix | 0.00 | 7.70 | 1.05 | 6.14 | 192.18 *** | 195.78 *** | −25.58 *** |

| FTSE 100 | 0.00 | 1.20 | −0.41 | 10.03 | 788.14 *** | 834.46 *** | −23.79 *** |

| DAX PERFORMANCE-INDEX | 0.02 | 1.39 | −0.23 | 8.39 | 583.26 *** | 674.27 *** | −22.63 *** |

| CAC 40 | 0.01 | 1.42 | −0.28 | 8.25 | 628.1 *** | 688.32 *** | −23.59 *** |

| ESTX 50 PR.EUR | 0.00 | 1.43 | −0.32 | 7.99 | 589.85 *** | 613.74 *** | −29.08 *** |

| EURONEXT 100 | 0.01 | 1.30 | −0.38 | 9.10 | 692.21 *** | 759.31 *** | −23.48 *** |

| BEL 20 | −0.00 | 1.30 | −0.65 | 10.77 | 584.09 *** | 614.49 *** | −12.24 *** |

| Nikkei 225 | 0.01 | 1.47 | −0.45 | 8.38 | 1054.16 *** | 1098.86 *** | −63.39 *** |

| HANG SENG INDEX | 0.00 | 1.48 | −0.03 | 8.96 | 997.94 *** | 1106.29 *** | −10.72 *** |

| SSE Composite Index | 0.00 | 1.53 | −0.61 | 5.44 | 408.67 *** | 472.35 *** | −12.97 *** |

| Shenzhen Component | 0.02 | 1.78 | −0.55 | 3.45 | 364.1 *** | 426.68 *** | −14.66 *** |

| S&P/ASX 200 | 0.01 | 1.12 | −0.69 | 7.80 | 1129.81 *** | 1175.54 *** | −14.4 *** |

| ALL ORDINARIES | 0.01 | 1.07 | −0.66 | 9.66 | 768.79 *** | 817.83 *** | −37.55 *** |

| S&P BSE SENSEX | 0.04 | 1.37 | −0.21 | 13.61 | 543.65 *** | 561.24 *** | −11.96 *** |

| Jakarta Composite Index | 0.03 | 1.27 | −0.58 | 9.61 | 508.49 *** | 614.77 *** | −18.47 *** |

| S&P/NZX 50 INDEX GROSS | 0.03 | 0.74 | −0.65 | 8.21 | 886.56 *** | 947.68 *** | −21.0 *** |

| KOSPI Composite Index | 0.02 | 1.23 | −0.55 | 10.44 | 966.23 *** | 990.46 *** | −12.24 *** |

| TSEC weighted index | 0.02 | 1.14 | −0.42 | 5.11 | 488.16 *** | 541.14 *** | −14.08 *** |

| S&P/TSX Composite index | 0.01 | 1.15 | −1.08 | 20.75 | 1126.95 *** | 1262.88 *** | −11.45 *** |

| IBOVESPA | 0.02 | 1.74 | −0.44 | 10.17 | 1174.02 *** | 1267.65 *** | −26.78 *** |

| IPC MEXICO | 0.02 | 1.18 | −0.02 | 7.29 | 724.97 *** | 843.78 *** | −27.88 *** |

| MERVAL | 0.10 | 2.32 | −2.67 | 50.22 | 37.67 *** | 58.42 *** | −61.87 *** |

| TA-125 | 0.02 | 1.09 | −1.17 | 12.07 | 466.91 *** | 527.72 *** | −18.56 *** |

| Average | 0.02 | 1.58 | −0.52 | 11.01 | - | - | - |

| Cluster | Market | Country |

|---|---|---|

| 1 | FTSE 100 | United Kingdom |

| DAX PERFORMANCE-INDEX | Germany | |

| 2 | BEL 20 | Belgium |

| 3 | CAC 40 | France |

| EURONEXT 100 | France | |

| 4 | IPC MEXICO | Mexico |

| 5 | S&P 500 | United States |

| 6 | SSE Composite Index | China |

| Shenzhen Component | China | |

| 7 | Dow Jones Industrial Average | United States |

| NYSE Composite Index | United States | |

| 8 | NASDAQ Composite | United States |

| Russell 2000 | United States | |

| 9 | S&P/ASX 200 | Australia |

| ALL ORDINARIES | Australia | |

| 10 | Nikkei 225 | Japan |

| MERVAL | Argentina | |

| 11 | TA-125 | Israel |

| 12 | TSEC weighted index | Taiwan |

| IBOVESPA | Brazil | |

| 13 | Jakarta Composite Index | Indonesia |

| KOSPI Composite Index | Republic of Korea | |

| 14 | HANG SENG INDEX | Hong Kong |

| S&P/TSX Composite index | Canada | |

| 15 | S&P BSE SENSEX | India |

| NYSE American Composite Index | United States | |

| Vix | United States |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cho, P.; Kim, K. Global Collective Dynamics of Financial Market Efficiency Using Attention Entropy with Hierarchical Clustering. Fractal Fract. 2022, 6, 562. https://doi.org/10.3390/fractalfract6100562

Cho P, Kim K. Global Collective Dynamics of Financial Market Efficiency Using Attention Entropy with Hierarchical Clustering. Fractal and Fractional. 2022; 6(10):562. https://doi.org/10.3390/fractalfract6100562

Chicago/Turabian StyleCho, Poongjin, and Kyungwon Kim. 2022. "Global Collective Dynamics of Financial Market Efficiency Using Attention Entropy with Hierarchical Clustering" Fractal and Fractional 6, no. 10: 562. https://doi.org/10.3390/fractalfract6100562

APA StyleCho, P., & Kim, K. (2022). Global Collective Dynamics of Financial Market Efficiency Using Attention Entropy with Hierarchical Clustering. Fractal and Fractional, 6(10), 562. https://doi.org/10.3390/fractalfract6100562