Total Value Adjustment of Multi-Asset Derivatives under Multivariate CGMY Processes

Abstract

:1. Introduction

2. Preliminaries

2.1. The Structure of XVA and Exposure

2.2. Multivariate Lévy Processes and Stock Price Model

3. Numerical Method

- Simulate paths of underlying price under the multivariate CGMY model by the Monte Carlo method.

- Based on option types, applying the ADI method and cosine–cosine expansion method to find the exposure of each path in step 1.

3.1. Monte Carlo–ADI Method

3.1.1. The Derivation of 2D FPDE

3.1.2. ADI Method for 2D FPDE

3.1.3. Convergence Test

3.2. Monte Carlo–Cosine-Cosine Expansion Method

3.2.1. The Cosine–Cosine Expansion of Derivative Value

3.2.2. The Discrete Cosine Transforms Approximation

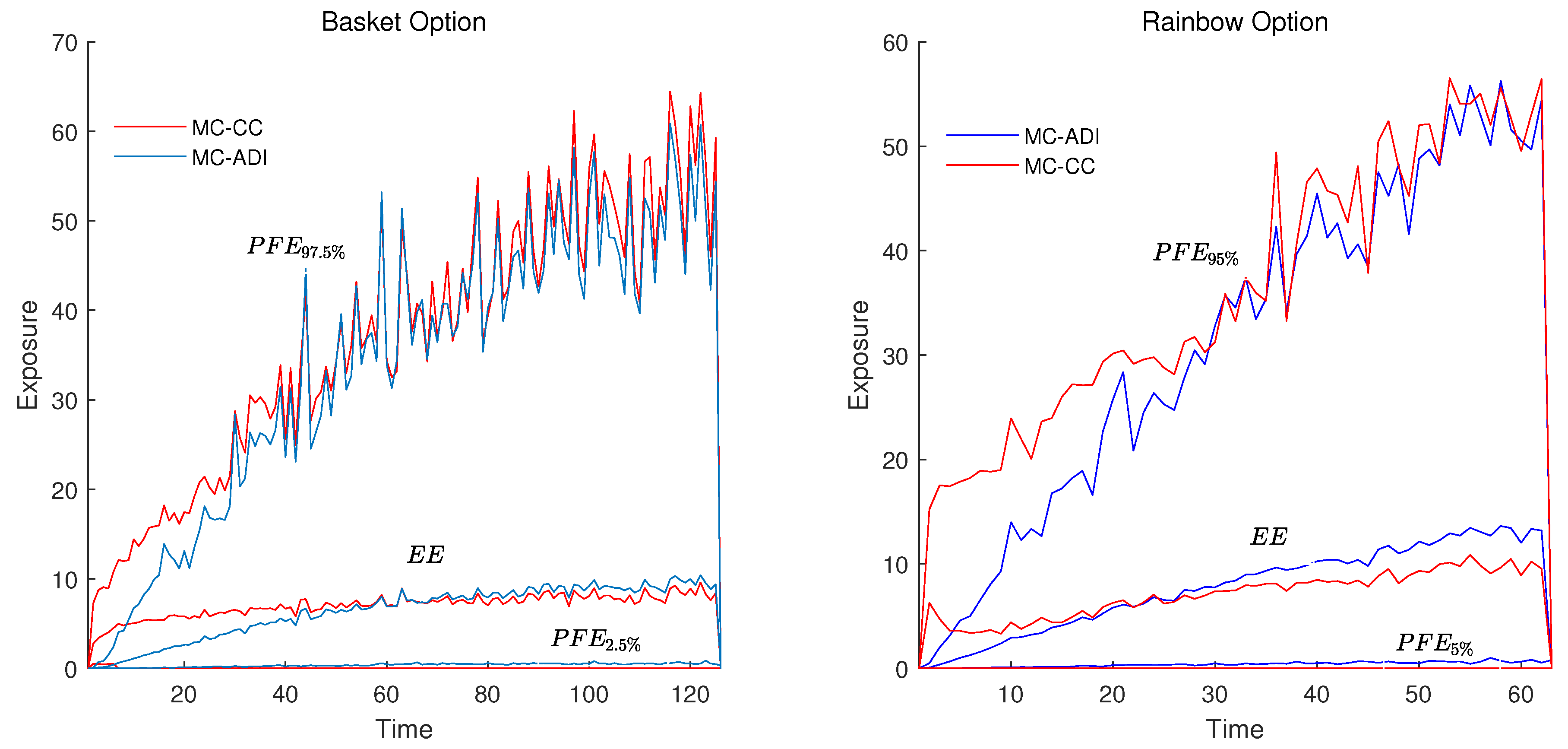

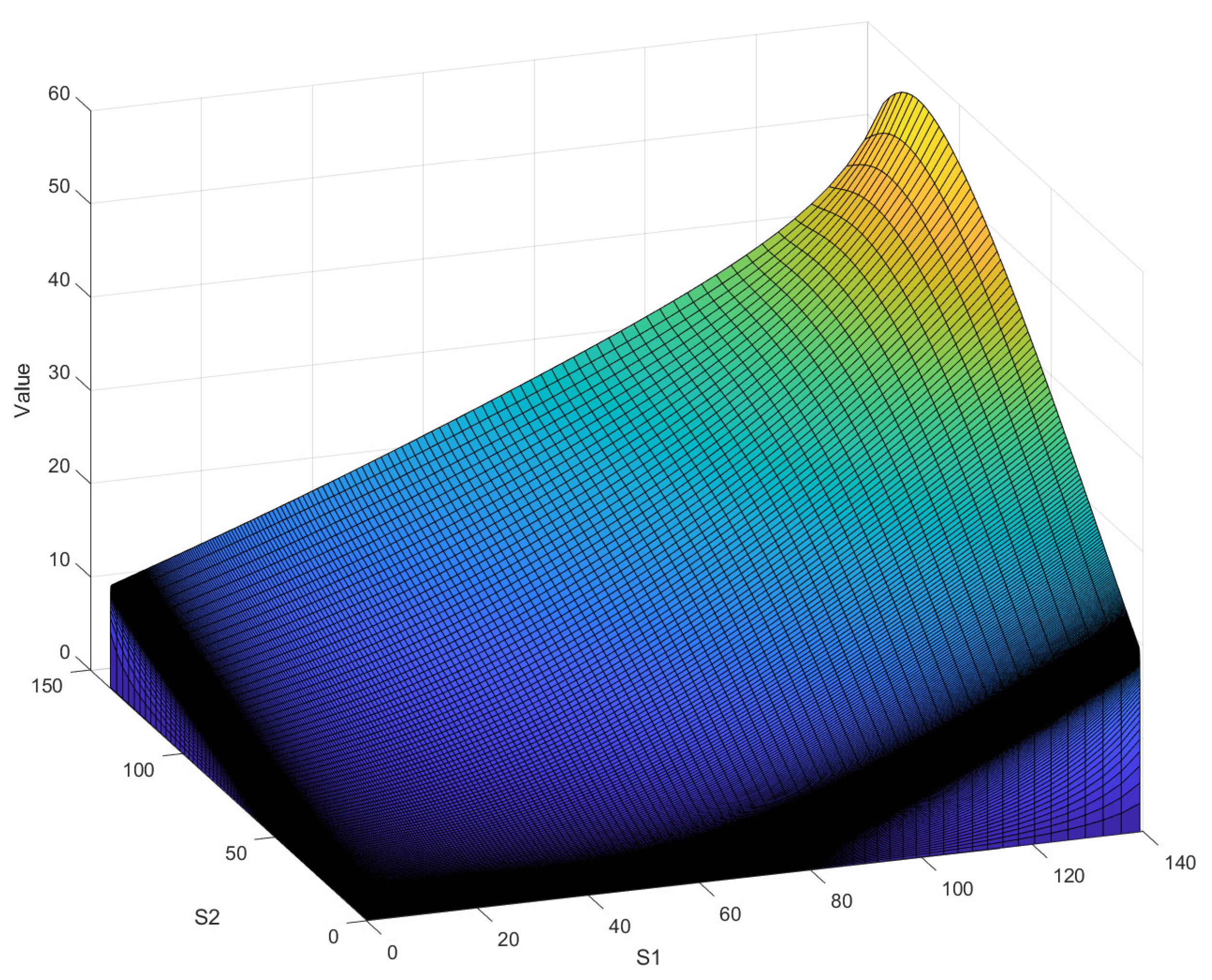

4. Numerical Results and Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Conflicts of Interest

References

- Gregory, J. Counterparty Credit Risk and Credit Value Adjustment: A Continuing Challenge for Global Financial Markets; John Wiley & Sons: Hoboken, NJ, USA, 2012. [Google Scholar]

- Kenyon, C. Completing CVA and liquidity: Firm-level positions and collateralized trades. arXiv 2010, arXiv:1009.3361. [Google Scholar] [CrossRef] [Green Version]

- Gregory, J. The xVA Challenge: Counterparty Credit Risk, Funding, Collateral and Capital; John Wiley & Sons: Hoboken, NJ, USA, 2015. [Google Scholar]

- Burgard, C.; Kjaer, M. Partial differential equation representations of derivatives with bilateral counterparty risk and funding costs. J. Credit Risk 2011, 7, 1–19. [Google Scholar] [CrossRef]

- Arregui, I.; Salvador, B.; Vázquez, C. PDE models and numerical methods for total value adjustment in European and American options with counterparty risk. Appl. Math. Comput. 2017, 308, 31–53. [Google Scholar] [CrossRef]

- Borovykh, A.; Pascucci, A.; Oosterlee, C.W. Efficient computation of various valuation adjustments under local Lévy models. SIAM J. Financ. Math. 2018, 9, 251–273. [Google Scholar] [CrossRef] [Green Version]

- Salvador, B.; Oosterlee, C.W. Total value adjustment for a stochastic volatility model. A comparison with the Black–Scholes model. Appl. Math. Comput. 2020, 391, 125489. [Google Scholar] [CrossRef]

- de Graaf, C.; Kandhai, D.; Sloot, P. Efficient estimation of sensitivities for counterparty credit risk with the finite difference Monte Carlo method. J. Comput. Financ. 2016, 21, 83–113. [Google Scholar] [CrossRef] [Green Version]

- Goudenège, L.; Molent, A.; Zanette, A. Computing credit valuation adjustment solving coupled PIDEs in the Bates model. Comput. Manag. Sci. 2020, 17, 163–178. [Google Scholar] [CrossRef]

- Arregui, I.; Salvador, B.; Ševčovič, D.; Vázquez, C. Total value adjustment for European options with two stochastic factors. Mathematical model, analysis and numerical simulation. Comput. Math. Appl. 2018, 76, 725–740. [Google Scholar] [CrossRef]

- Arregui, I.; Salvador, B.; Ševčovič, D.; Vázquez, C. PDE models for American options with counterparty risk and two stochastic factors: Mathematical analysis and numerical solution. Comput. Math. Appl. 2020, 79, 1525–1542. [Google Scholar] [CrossRef]

- Yuan, G.; Ding, D.; Duan, J.; Lu, W.; Wu, F. Total value adjustment of Bermudan option valuation under pure jump Lévy fluctuations. Chaos Interdiscip. J. Nonlinear Sci. 2022, 32, 023127. [Google Scholar] [CrossRef]

- Elliott, R.J.; Osakwe, C.J.U. Option pricing for pure jump processes with Markov switching compensators. Financ. Stoch. 2006, 10, 250–275. [Google Scholar] [CrossRef]

- Geman, H. Pure jump Lévy processes for asset price modelling. J. Bank. Financ. 2002, 26, 1297–1316. [Google Scholar] [CrossRef] [Green Version]

- Shen, Y.; Anderluh, J.; Van Der Weide, J. Algorithmic counterparty credit exposure for multi-asset Bermudan options. Int. J. Theor. Appl. Financ. 2015, 18, 1550001. [Google Scholar] [CrossRef]

- Henderson, V.; Liang, G. A multidimensional exponential utility indifference pricing model with applications to counterparty risk. SIAM J. Control Optim. 2016, 54, 690–717. [Google Scholar] [CrossRef] [Green Version]

- Goudenege, L.; Molent, A.; Zanette, A. Computing XVA for American basket derivatives by Machine Learning techniques. arXiv 2022, arXiv:2209.06485. [Google Scholar]

- Deelstra, G.; Petkovic, A. How they can jump together: Multivariate Lévy processes and option pricing. Belg. Actuar. Bull. 2010, 9, 29–42. [Google Scholar]

- Tankov, P. Simulation and option pricing in Lévy copula models. In Mathematical Modelling of Financial Derivatives, IMA Volumes in Mathematics and Applications; Springer: Berlin/Heidelberg, Germany, 2006. [Google Scholar]

- Kawai, R. A multivariate Lévy process model with linear correlation. Quant. Financ. 2009, 9, 597–606. [Google Scholar] [CrossRef]

- Ballotta, L.; Bonfiglioli, E. Multivariate asset models using Lévy processes and applications. Eur. J. Financ. 2016, 22, 1320–1350. [Google Scholar] [CrossRef] [Green Version]

- Marfè, R. A multivariate pure-jump model with multi-factorial dependence structure. Int. J. Theor. Appl. Financ. 2012, 15, 1250028. [Google Scholar] [CrossRef]

- Gao, Y.; Song, H.; Wang, X.; Zhang, K. Primal-dual active set method for pricing American better-of option on two assets. Commun. Nonlinear Sci. Numer. Simul. 2020, 80, 104976. [Google Scholar] [CrossRef]

- Chen, W.; Wang, S. A 2nd-order ADI finite difference method for a 2D fractional Black–Scholes equation governing European two asset option pricing. Math. Comput. Simul. 2020, 171, 279–293. [Google Scholar] [CrossRef]

- Guo, X.; Li, Y.; Wang, H. A high order finite difference method for tempered fractional diffusion equations with applications to the CGMY model. SIAM J. Sci. Comput. 2018, 40, A3322–A3343. [Google Scholar] [CrossRef]

- Cartea, A.; del Castillo-Negrete, D. Fractional diffusion models of option prices in markets with jumps. Phys. A Stat. Mech. Appl. 2007, 374, 749–763. [Google Scholar] [CrossRef] [Green Version]

- Guo, X.; Li, Y.; Wang, H. Tempered fractional diffusion equations for pricing multi-asset options under CGMYe process. Comput. Math. Appl. 2018, 76, 1500–1514. [Google Scholar] [CrossRef]

- Liao, H.L.; Sun, Z.Z. Maximum norm error bounds of ADI and compact ADI methods for solving parabolic equations. Numer. Methods Partial Differ. Equ. Int. J. 2010, 26, 37–60. [Google Scholar] [CrossRef]

- Zhang, Q.; Zhang, C.; Deng, D. Compact alternating direction implicit method to solve two-dimensional nonlinear delay hyperbolic differential equations. Int. J. Comput. Math. 2014, 91, 964–982. [Google Scholar] [CrossRef]

- Wu, F.; Cheng, X.; Li, D.; Duan, J. A two-level linearized compact ADI scheme for two-dimensional nonlinear reaction–diffusion equations. Comput. Math. Appl. 2018, 75, 2835–2850. [Google Scholar] [CrossRef]

- Qin, H.; Wu, F.; Zhang, J.; Mu, C. A linearized compact ADI scheme for semilinear parabolic problems with distributed delay. J. Sci. Comput. 2021, 87, 1–19. [Google Scholar] [CrossRef]

- Qin, H.; Wu, F.; Ding, D. A linearized compact ADI numerical method for the two-dimensional nonlinear delayed Schrödinger equation. Appl. Math. Comput. 2022, 412, 126580. [Google Scholar] [CrossRef]

- Cheng, X.; Duan, J.; Li, D. A novel compact ADI scheme for two-dimensional Riesz space fractional nonlinear reaction–diffusion equations. Appl. Math. Comput. 2019, 346, 452–464. [Google Scholar] [CrossRef]

- Chen, X.; Di, Y.; Duan, J.; Li, D. Linearized compact ADI schemes for nonlinear time-fractional Schrödinger equations. Appl. Math. Lett. 2018, 84, 160–167. [Google Scholar] [CrossRef]

- Ruijter, M.J.; Oosterlee, C.W. Two-dimensional Fourier cosine series expansion method for pricing financial options. SIAM J. Sci. Comput. 2012, 34, B642–B671. [Google Scholar] [CrossRef] [Green Version]

- Fang, F.; Oosterlee, C.W. A novel pricing method for European options based on Fourier-cosine series expansions. SIAM J. Sci. Comput. 2009, 31, 826–848. [Google Scholar] [CrossRef] [Green Version]

- Meng, Q.J.; Ding, D. An efficient pricing method for rainbow options based on two-dimensional modified sine–sine series expansions. Int. J. Comput. Math. 2013, 90, 1096–1113. [Google Scholar] [CrossRef]

- Unal, H.; Madan, D.; Güntay, L. Pricing the risk of recovery in default with absolute priority rule violation. J. Bank. Financ. 2003, 27, 1001–1025. [Google Scholar] [CrossRef]

- Schläfer, T.; Uhrig-Homburg, M. Is recovery risk priced? J. Bank. Financ. 2014, 40, 257–270. [Google Scholar] [CrossRef]

- Hull, J.C. Options, Futures and Other Derivatives; Pearson: London, UK, 2019. [Google Scholar]

- de Graaf, C. Efficient PDE Based Numerical Estimation of Credit and Liquidity Risk Measures for Realistic Derivative Portfolios. Ph.D. Thesis, University of Amsterdam, Amsterdam, The Netherlands, 2016. [Google Scholar]

- Ruiz, I. A Complete XVA Valuation Framework: Why the “law of one price” is dead. IRuiz Consult 2015, 12, 1–23. [Google Scholar]

- Tankov, P. Financial Modelling with Jump Processes; Chapman and Hall/CRC: Boca Raton, FL, USA, 2003. [Google Scholar]

- Duan, J. An Introduction to Stochastic Dynamics; Cambridge University Press: New York, NY, USA, 2015. [Google Scholar]

- Carr, P.; Geman, H.; Madan, D.B.; Yor, M. The fine structure of asset returns: An empirical investigation. J. Bus. 2002, 75, 305–332. [Google Scholar] [CrossRef] [Green Version]

- Oosterlee, C.W.; Grzelak, L.A. Mathematical Modeling and Computation in Finance: With Exercises and Python and Matlab Computer Codes; World Scientific: Singapore, 2019. [Google Scholar]

- Madan, D.; Yor, M. CGMY and Meixner subordinators are absolutely continuous with respect to one sided stable subordinators. arXiv 2006, arXiv:math/0601173. [Google Scholar]

- Sioutis, S.J. Calibration and Filtering of Exponential Lévy Option Pricing Models. arXiv 2017, arXiv:1705.04780. [Google Scholar]

- Rosiński, J. Series representations of Lévy processes from the perspective of point processes. In Lévy Processes; Springer: Berlin/Heidelberg, Germany, 2001; pp. 401–415. [Google Scholar]

- Li, C.; Deng, W. High order schemes for the tempered fractional diffusion equations. Adv. Comput. Math. 2016, 42, 543–572. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Order | Order | |||

|---|---|---|---|---|

| 3.5624 | — | 8.6670 | — | |

| 8.9622 | 1.9909 | 2.0971 | 2.0471 | |

| 2.2375 | 2.0020 | 5.1710 | 2.0199 | |

| 5.5945 | 1.9998 | 1.2809 | 2.0133 |

| C | G | M | Y | |||

|---|---|---|---|---|---|---|

| Basket | Process | 1 | 5 | 6 | 1.5 | 40 |

| Process | 1 | 10 | 12 | 1.2 | 40 | |

| Rainbow | Process | 0.5 | 25 | 26 | 1.5 | 40 |

| Process | 0.5 | 20 | 22 | 1.2 | 45 |

| MC-ADI | MC-CC | Difference | |

|---|---|---|---|

| CVA | −9.5826% | −10.0421% | 0.4595% |

| FVA | −3.1944% | −3.3514% | 0.1570% |

| XVA | −12.7770% | −13.3935% | 0.6165% |

| MC-ADI | MC-CC | Difference | |

|---|---|---|---|

| CVA | −11.1571% | −10.6143% | 0.5428% |

| FVA | −3.7185% | −3.5462% | 0.1723% |

| XVA | −14.8753% | −14.1605% | 0.7151% |

| MC-ADI | MC-CC | |

|---|---|---|

| Basket | 1.8798 | 4.6667 |

| Rainbow | 1.9943 | 4.7001 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, F.; Ding, D.; Yin, J.; Lu, W.; Yuan, G. Total Value Adjustment of Multi-Asset Derivatives under Multivariate CGMY Processes. Fractal Fract. 2023, 7, 308. https://doi.org/10.3390/fractalfract7040308

Wu F, Ding D, Yin J, Lu W, Yuan G. Total Value Adjustment of Multi-Asset Derivatives under Multivariate CGMY Processes. Fractal and Fractional. 2023; 7(4):308. https://doi.org/10.3390/fractalfract7040308

Chicago/Turabian StyleWu, Fengyan, Deng Ding, Juliang Yin, Weiguo Lu, and Gangnan Yuan. 2023. "Total Value Adjustment of Multi-Asset Derivatives under Multivariate CGMY Processes" Fractal and Fractional 7, no. 4: 308. https://doi.org/10.3390/fractalfract7040308

APA StyleWu, F., Ding, D., Yin, J., Lu, W., & Yuan, G. (2023). Total Value Adjustment of Multi-Asset Derivatives under Multivariate CGMY Processes. Fractal and Fractional, 7(4), 308. https://doi.org/10.3390/fractalfract7040308