A Preconditioned Iterative Method for a Multi-State Time-Fractional Linear Complementary Problem in Option Pricing

Abstract

:1. Introduction

2. Numerical Scheme and Theoretical Analysis

2.1. Finite Difference Method

2.2. Matrix Form

2.3. Stability Analysis

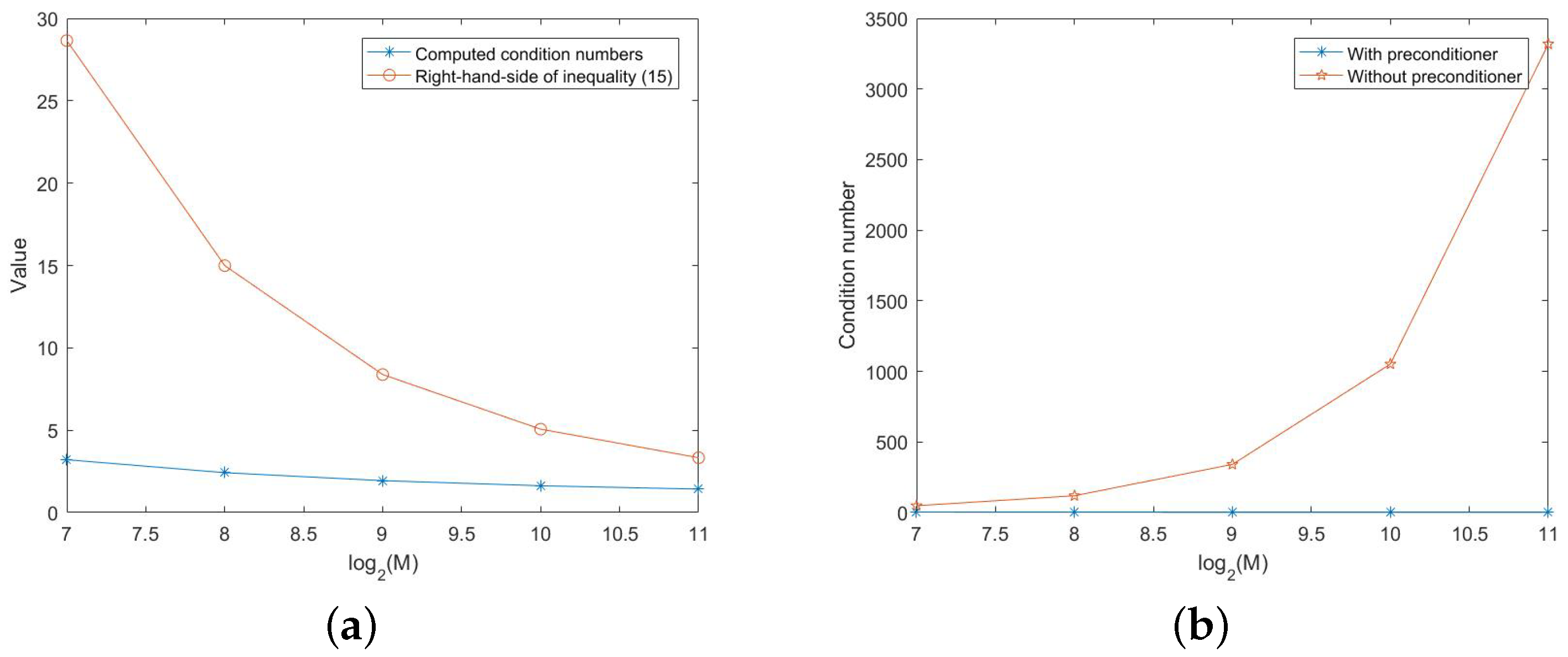

3. Preconditioned Policy-Krylov Subspace Method

3.1. Policy Iteration Method

| Algorithm 1 Framework of the policy iteration method |

Let be the k-th iteration of the policy iteration method for computing the solution . Let , , and . For , we have

Find , such that

|

3.2. Preconditioned Krylov Subspace Method

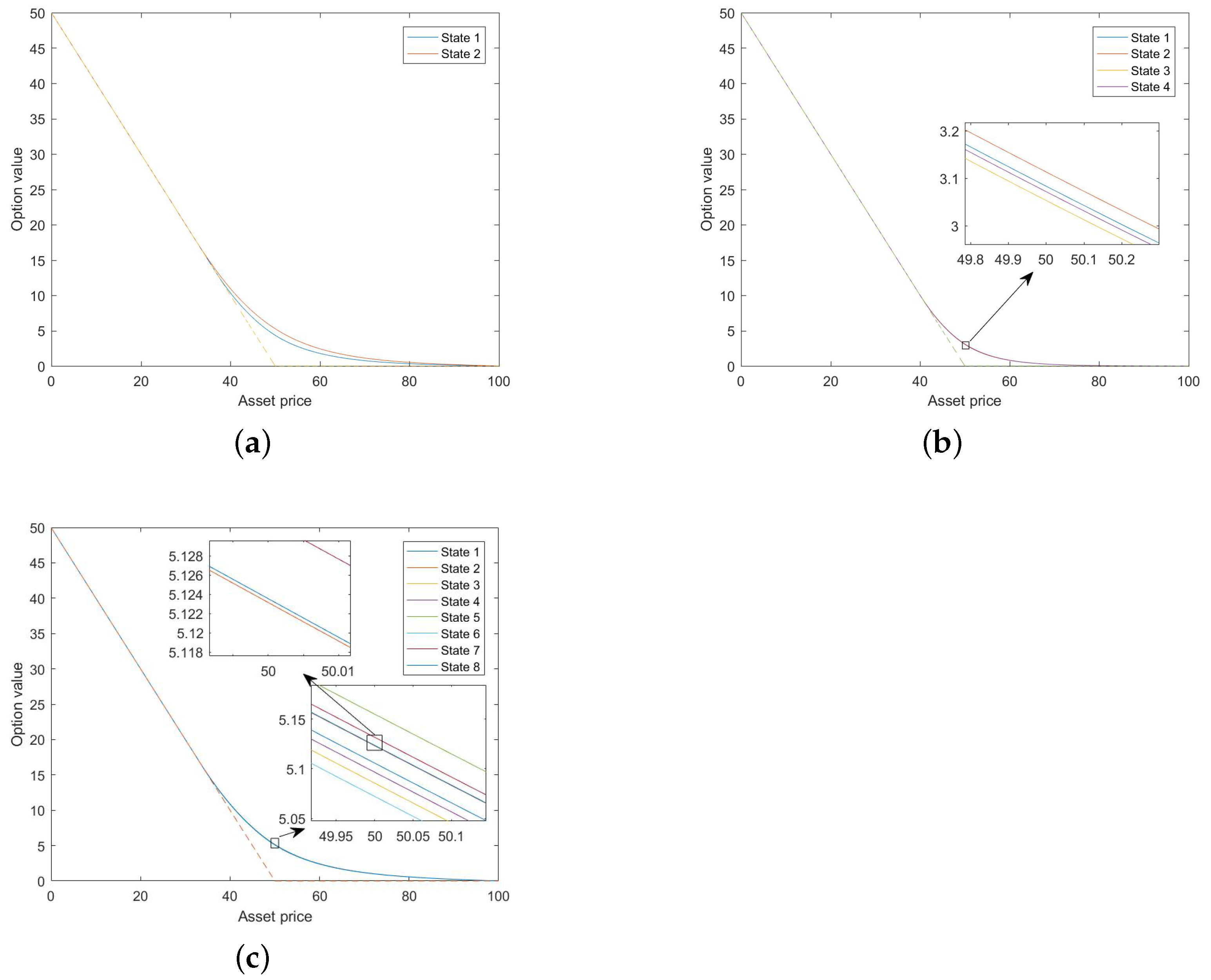

4. Numerical Experiment

- (a)

- , , ,

- (b)

- , , ,

- (c)

- , , ,

5. Concluding Remark

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Politics Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Stein, E.M.; Stein, J.C. Stock price distributions with stochastic volatility:an analytic approach. Rev. Financ. Stud. 1991, 4, 727–752. [Google Scholar] [CrossRef]

- Heston, S.L. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 1993, 6, 327–343. [Google Scholar] [CrossRef]

- Kou, S.G. A jump-diffusion model for option pricing. Manag. Sci. 2002, 48, 1086–1101. [Google Scholar] [CrossRef]

- Madan, D.B.; Carr, P.P.; Chang, E.C. The variance gamma process and option pricing. Eur. Financ. Rev. 1998, 2, 79–105. [Google Scholar] [CrossRef]

- Boyarchenko, S.; Levendorskii, S. Non-Gaussian Merton-Black-Scholes Theory; World Scientific: Singapore, 2002. [Google Scholar]

- Fulop, A.; Li, J.; Yu, J. Self-exciting jumps, learning, and asset pricing implications. Rev. Financ. Stud. 2015, 28, 876–912. [Google Scholar] [CrossRef]

- Hawkes, A.G. Hawkes jump-diffusions and finance: A brief history and review. Eur. J. Financ. 2022, 28, 627–641. [Google Scholar] [CrossRef]

- Cartea, A.; del Castillo-Negrete, D. Fractional diffusion models of option prices in markets with jumps. Physical A 2007, 374, 749–763. [Google Scholar] [CrossRef]

- Carr, P.; Wu, L. The finite moment log stable process and option pricing. J. Financ. 2003, 58, 753–777. [Google Scholar] [CrossRef]

- Carr, P.; Geman, H.; Madan, D.B.; Yor, M. The fine structure of asset returns: An empirical investigation. J. Bus. 2002, 75, 305–333. [Google Scholar] [CrossRef]

- Chen, W.; Wang, S. A penalty method for a fractional order parabolic variational inequality governing American put option valuation. Comput. Math. Appl. 2014, 67, 77–90. [Google Scholar] [CrossRef]

- Meng, Q.; Ding, D.; Sheng, Q. Preconditioned iterative methods for fractional diffusion models in finance. Numer. Meth. Part. Differ. Equ. 2014, 31, 1382–1395. [Google Scholar] [CrossRef]

- Zhang, H.; Liu, F.; Turner, I.; Chen, S. The numerical simulation of the tempered fractional Black–Scholes equation for European double barrier option. Appl. Math. Model. 2016, 40, 5819–5834. [Google Scholar] [CrossRef]

- Wyss, W. The fractional Black-Scholes equation. Fract. Calc. Appl. Anal. 2000, 3, 51–61. [Google Scholar]

- Jumarie, G. Derivation and solutions of some fractional Black–Scholes equations in coarse-grained space and time. Application to Merton’s optimal portfolio. Comput. Math. Appl. 2010, 59, 1142–1164. [Google Scholar] [CrossRef]

- Cartea, A. Derivation pricing with marked point processes using tick-by-tick data. Quant. Financ. 2013, 13, 111–123. [Google Scholar] [CrossRef]

- Zhang, H.; Liu, F.; Chen, S.; Anh, V.; Chen, J. Fast numerical simulation of a new time-space fractional option pricing model governing European call option. Appl. Math. Comput. 2018, 339, 186–198. [Google Scholar] [CrossRef]

- Yousur, M.; Khaliq, A.Q.M.; Liu, R.H. Pricing American options under multi-state regime switching with an efficient L-stable method. Int. J. Comput. Math. 2015, 92, 2530–2550. [Google Scholar]

- Hamilton, J.D. Analysis of time series subject to changes in regime. J. Econ. 1990, 45, 39–70. [Google Scholar] [CrossRef]

- He, X.; Chen, W. A Monte-Carlo based approach for pricing credit default swaps with regime switching. Comput. Math. Appl. 2018, 76, 1758–1766. [Google Scholar] [CrossRef]

- Koleva, M.N.; Vulkov, L.G. Fast positivity preserving numerical method for time-fractional regime-switching option pricing problem. In Advanced Computing in Industrial Mathematics; Georgiev, I., Kostadinov, H., Lilkova, E., Eds.; Springer: Cham, Switzerland, 2023; pp. 88–99. [Google Scholar]

- Lin, S.; He, X. A regime switching fractional Black–Scholes model and European option pricing. Commun. Nonlinear Sci. Numer. Simul. 2020, 85, 105222. [Google Scholar] [CrossRef]

- Saberi, E.; Hejazi, S.R.; Dastranj, E. A new method for option pricing via time-fractional PDE. Asian-Eur. J. Math. 2018, 11, 1850074. [Google Scholar] [CrossRef]

- Zhou, Z.; Ma, J.; Gao, X. Convergence of iterative Laplace transform methods for a system of fractional PDEs and PIDEs arising in option pricing. East Asian J. Appl. Math. 2018, 8, 782–808. [Google Scholar] [CrossRef]

- Chen, X.; Deng, D.; Lei, S.; Wang, W. An implicit-explicit preconditioned direct method for pricing options under regime-switching tempered fractional partial differential models. Numer. Algorithms 2021, 87, 939–965. [Google Scholar] [CrossRef]

- Wang, M.; Wang, C.; Yin, J. A second-order ADI method for pricing options under fractional regime-switching models. Netw. Heterog. Media 2023, 18, 647–663. [Google Scholar] [CrossRef]

- Lei, S.; Wang, W.; Chen, X.; Ding, D. A fast preconditioned penalty method for American options pricing under regime-switching tempered fractional diffusion models. J. Sci. Comput. 2018, 75, 1633–1655. [Google Scholar] [CrossRef]

- Boyarchenko, S.; Levendorskii, S. American options in regime-switching models. SIAM J. Control Optim. 2009, 48, 1353–1376. [Google Scholar] [CrossRef]

- Khaliq, A.K.Q.; Voss, D.A.; Kazmi, S.H.K. A linearly implicit predictor-corrector scheme for pricing American options using a penalty method approach. J. Bank Financ. 2006, 30, 489–502. [Google Scholar] [CrossRef]

- Wang, W.; Chen, Y.; Fang, H. On the variable two-step IMEX BDF method for parabolic integro-differential equations with nonsmooth initial data arising in finance. SIAM J. Numer. Anal. 2019, 57, 1289–1317. [Google Scholar] [CrossRef]

- Shi, X.; Yang, L.; Huang, Z. A fixed point method for the linear complementarity problem arising from American option pricing. Acta Math. Appl. Sin. Engl. Ser. 2016, 32, 921–932. [Google Scholar] [CrossRef]

- Gan, X.; Yin, J. Pricing American options under regime-switching model with a Crank-Nicolson fitted finite volume method. East Asian Appl. Math. 2020, 10, 499–519. [Google Scholar]

- Bai, Z. Modulus-based matrix splitting iteration methods for linear complementarity problems. Numer. Linear Algebra Appl. 2010, 17, 917–933. [Google Scholar] [CrossRef]

- Zheng, H.; Vong, S. A modified modulus-based matrix splitting iteration method for solving implicit complementarity problems. Numer. Algorithms 2019, 82, 573–592. [Google Scholar] [CrossRef]

- Cryer, C.W. The solution of a quadratic programming problem using systematic overrelaxation. SIAM J. Control Optim. 1971, 9, 385–392. [Google Scholar] [CrossRef]

- Toivanen, J.; Oosterlee, C.W. A projected algebraic multigrid method for linear complementarity problems. Numer. Math. Theor. Meth. Appl. 2012, 5, 85–98. [Google Scholar] [CrossRef]

- Huang, Y.; Forsyth, P.A.; Labahn, G. Methods for pricing American options under regime switching. SIAM J. Sci. Comput. 2011, 33, 2144–2168. [Google Scholar] [CrossRef]

- Chen, C.; Wang, Z.; Yang, Y. A new operator splitting method for American options under fractional Black-Scholes models. Comput. Math. Appl. 2019, 77, 2130–2144. [Google Scholar] [CrossRef]

- Podlubny, I. Fractional Differential Equations; Academic Press: New York, NY, USA, 1999. [Google Scholar]

- Gao, G.; Sun, Z.; Zhang, H. A new fractional numerical differentiation formula to approximate the Caputo fractional derivative and its applications. J. Comput. Phys. 2014, 259, 33–50. [Google Scholar] [CrossRef]

- Reisinger, C.; Witte, J.H. On the use of policy iteration as an easy way of pricing American options. SIAM J. Financ. Math. 2012, 3, 459–478. [Google Scholar] [CrossRef]

- Varah, J.M. A lower bound for the smallest singular value of a matrix. Linear Algebra Appl. 1975, 11, 3–5. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| CG | PCG | |||||||

|---|---|---|---|---|---|---|---|---|

| N | M | Error | Rate | Ite-Out | Ite-In | Time | Ite-In | Time |

| Case (a) | ||||||||

| - | 2.86 | 77.46 | 0.37 s | 2.56 | 0.08 s | |||

| 1.0472 | 2.82 | 106.05 | 1.24 s | 2.08 | 0.21 s | |||

| 1.0746 | 2.86 | 141.44 | 4.96 s | 1.78 | 0.79 s | |||

| 1.1921 | 2.86 | 184.55 | 23.49 s | 1.54 | 4.40 s | |||

| Case (b) | ||||||||

| - | 2.73 | 62.25 | 0.38 s | 7.92 | 0.19 s | |||

| 0.9778 | 2.77 | 91.38 | 1.59 s | 5.79 | 0.51 s | |||

| 1.0634 | 2.71 | 138.52 | 8.79 s | 4.61 | 2.26 s | |||

| 1.2032 | 2.69 | 208.57 | 44.75 s | 3.70 | 9.30 s | |||

| Case (c) | ||||||||

| - | 3.33 | 427.40 | 4.83 s | 14.84 | 0.55 s | |||

| 1.0201 | 3.32 | 848.73 | 35.33 s | 11.46 | 2.04 s | |||

| 1.0099 | 3.26 | 1705.16 | 242.65 s | 9.43 | 7.15 s | |||

| 1.1648 | 3.24 | - | - | 7.41 | 30.50 s | |||

| GMRES | PGMRES | |||||||

|---|---|---|---|---|---|---|---|---|

| N | M | Error | Rate | Ite-Out | Ite-In | Time | Ite-In | Time |

| Case (a) | ||||||||

| - | 2.86 | 156.68 | 1.66 s | 5.04 | 0.11 s | |||

| 1.0474 | 2.82 | 242.87 | 6.81 s | 4.12 | 0.26 s | |||

| 1.0749 | 2.86 | 406.86 | 36.64 s | 3.33 | 0.90 s | |||

| 1.1929 | 2.86 | 692.43 | 392.76 s | 3.05 | 5.00 s | |||

| Case (b) | ||||||||

| - | 2.73 | 113.89 | 1.58 s | 13.86 | 0.30 s | |||

| 0.9778 | 2.77 | 191.73 | 8.20 s | 10.59 | 0.72 s | |||

| 1.0635 | 2.71 | 372.04 | 99.65 s | 8.29 | 3.07 s | |||

| 1.2032 | 2.69 | 760.57 | 637.37 s | 6.55 | 11.78 s | |||

| Case (c) | ||||||||

| - | 3.33 | 1411.11 | 36.60 s | 24.77 | 0.98 s | |||

| 1.0202 | 3.32 | 8428.32 | 1409.52 s | 18.56 | 4.21 s | |||

| 1.0099 | 3.26 | 32,658.12 | 17,206.00 s | 14.56 | 10.57 s | |||

| 1.1650 | 3.24 | - | - | 11.55 | 39.96 s | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, X.; Gong, X.; Lei, S.-L.; Sun, Y. A Preconditioned Iterative Method for a Multi-State Time-Fractional Linear Complementary Problem in Option Pricing. Fractal Fract. 2023, 7, 334. https://doi.org/10.3390/fractalfract7040334

Chen X, Gong X, Lei S-L, Sun Y. A Preconditioned Iterative Method for a Multi-State Time-Fractional Linear Complementary Problem in Option Pricing. Fractal and Fractional. 2023; 7(4):334. https://doi.org/10.3390/fractalfract7040334

Chicago/Turabian StyleChen, Xu, Xinxin Gong, Siu-Long Lei, and Youfa Sun. 2023. "A Preconditioned Iterative Method for a Multi-State Time-Fractional Linear Complementary Problem in Option Pricing" Fractal and Fractional 7, no. 4: 334. https://doi.org/10.3390/fractalfract7040334

APA StyleChen, X., Gong, X., Lei, S. -L., & Sun, Y. (2023). A Preconditioned Iterative Method for a Multi-State Time-Fractional Linear Complementary Problem in Option Pricing. Fractal and Fractional, 7(4), 334. https://doi.org/10.3390/fractalfract7040334