Modeling and Analyzing a Multi-Objective Financial Planning Model Using Goal Programming

Abstract

:1. Introduction

2. Materials and Methods

2.1. Goal Programming Problem (GPP)

2.2. Nomenclature

2.3. General Mathematical Formulation as Goal Programming (GP) Model

2.4. Goal-Programming Types

- (i)

- The Lexicographic Goal Programming Model;

- (ii)

- The weighted goal programming model.

2.4.1. Lexicographic Goal Programming Model

2.4.2. Weighted Goal Programming Model

2.5. Formulation of Model

The Goals

- is the total quantity for each component of financial statements for 2010;

- is the total quantity for each component of financial statements for 2011;

- is the total quantity for each component of financial statements for 2012;

- is the total quantity for each component of financial statements for 2013;

- is the total quantity for each component of financial statements for 2014;

- is the total quantity for each component of financial statements for 2015;

- is the total quantity for each component of financial statements for 2016;

- is the total quantity for each component of financial statements for 2017;

- is the total quantity for each component of financial statements for 2018;

- is the total quantity for each component of financial statements for 2019;

- is the total quantity for each component of financial statements for 2020.

2.6. Goal Constraints

2.6.1. Total Asset Goal Constraint

2.6.2. Total Liability Goal Constraint

2.6.3. Total Equity Goal Constraint

2.6.4. Total Gross Profit Constraint

2.6.5. Total Operating Income Goal Constraint

2.6.6. Total Net Income Goal Constraint

2.6.7. Total Goal Achievement Constraint

2.7. Objective Function

2.8. GP Model

3. A Case Study

4. Results

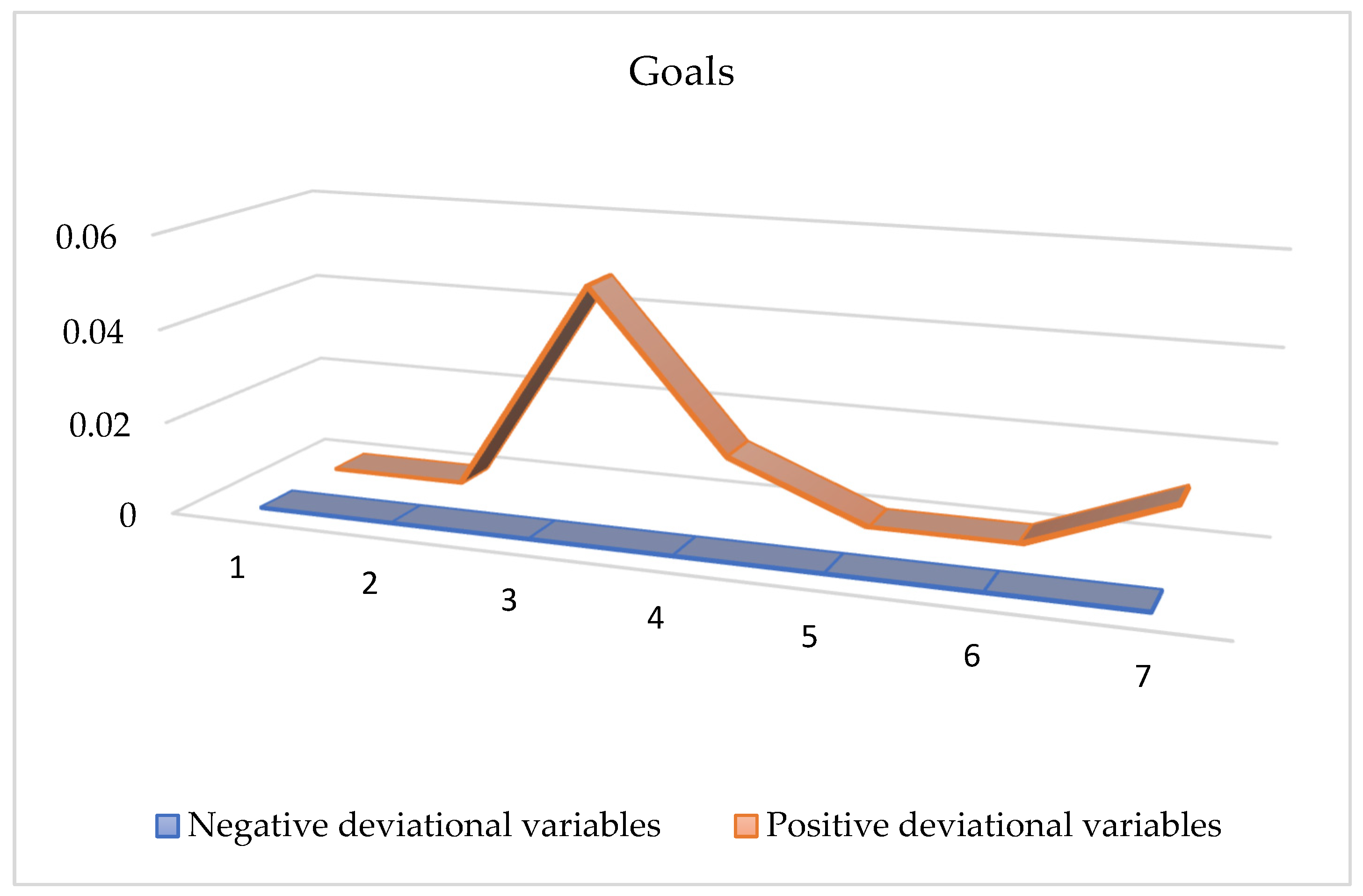

5. Discussion

- (i)

- The company’s first goal is totally attained as and are zero, and it concluded that the company’s total assets for eleven years remain the same;

- (ii)

- Similarly, since and are zero, second goal is also achieved;

- (iii)

- The value of for goal three is zero, whereas is . Thus, the company’s equity can increase by SAR 0.04694982 trillion annually after meeting the equity goal;

- (iv)

- For goal four, is zero, whereas is Therefore, the company’s gross profit goal was reached, resulting in a yearly increase of SAR 0.01220811 trillion in gross profit;

- (v)

- Furthermore, because both and are equal to zero, maximizing total operating income for goal five is achieved. Therefore, total income remains the same for eleven years.;

- (vi)

- Furthermore, because and are equal to zero, goal six is also achieved by maximizing total net income. As a result, total net income remained constant for eleven years;

- (vii)

- As a final goal, the overall goal should be maximized. According to the results, is zero, while is 0.01185368, indicating that annual goal achievements can increase by SAR 0.01185368 trillion.

6. Conclusions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Available online: https://www.sabic.com/en/about/corporate-profile (accessed on 10 June 2022).

- Available online: https://brandfinance.com/insights/brand-spotlight-sabic (accessed on 10 June 2022).

- Dan, E.D.; Desmond, O.O. Goal programming: An application to budgetary allocation of an institution of higher learning. Res. J. Eng. Appl. Sci. 2013, 2, 95–105. [Google Scholar]

- Farahat, F.A.; ElSayed, M.A. Achievement Stability Set for Parametric Rough Linear Goal Programing Problem. Fuzzy Inf. Eng. 2019, 11, 279–294. [Google Scholar] [CrossRef]

- Chowdary, B.V.; Slomp, J. Production Planning under Dynamic Product Environment: A Multi-Objective Goal Programming Approach; Department of Production Systems Design, Faculty of Management & Organization, University of Groningen: Groningen, The Netherlands, 2002; pp. 1–48. [Google Scholar]

- Lin, T.W.; O’Leary, D.E. Goal programming applications in financial management. Adv. Math. Program. Financ. Plan. 1993, 3, 211–230. [Google Scholar]

- Hotvedt, J.E. Application of linear goal programming to forest harvest scheduling. J. Agric. Appl. Econ. 1983, 15, 103–108. [Google Scholar] [CrossRef] [Green Version]

- Tamiz, M.; Jones, D.; Romero, C. Goal programming for decision making: An overview of the current state-of-the-art. Eur. J. Oper. Res. 1998, 111, 569–581. [Google Scholar] [CrossRef]

- Lam, W.S.; Lam, W.H.; Lee, P.F. Decision Analysis on the Financial Management of Shipping Companies using Goal Programming Model. In Proceedings of the 2021 International Conference on Decision Aid Sciences and Application (DASA), Sakheer, Bahrain, 7–8 December 2021; pp. 591–595. [Google Scholar]

- Romero, C. Extended lexicographic goal programming: A unifying approach. Omega 2001, 29, 63–71. [Google Scholar] [CrossRef]

- Kruger, M. A Goal Programming Approach to Strategic Bank Balance Sheet Management. In SAS Global Forum 2011 Banking; Financial Services and Insurance, Centre for BMI, North-West University: Potchefstroom, South Africa, 2011; pp. 1–11. [Google Scholar]

- Díaz-Balteiro, L.; Romero, C. Forest management optimization models when carbon captured is considered: A goal programming approach. For. Ecol. Manag. 2003, 174, 447–457. [Google Scholar] [CrossRef]

- Jamalnia, A.; Soukhakian, M.A. A hybrid fuzzy goal programming approach with different goal priorities to aggregate production planning. Comput. Ind. Eng. 2009, 56, 1474–1486. [Google Scholar] [CrossRef]

- Chen, J.W.; Lam, W.S.; Lam, W.H. Optimization on the financial management of the bank with goal programming model. J. Fundam. Appl. Sci. 2017, 9, 442–451. [Google Scholar] [CrossRef] [Green Version]

- Dyer, J.S. Interactive goal programming. Manag. Sci. 1972, 19, 62–70. [Google Scholar] [CrossRef]

- Kvanli, A.H. Financial planning using goal programming. Omega 1980, 8, 207–218. [Google Scholar] [CrossRef]

- ChiangLin, C.-Y. A Personal Financial Planning Model Based on Fuzzy Multiple Goal Programming Method. In Proceedings of the 9th Joint International Conference on Information Sciences (JCIS-06), Kaohsiung, Taiwan, 8–11 October 2006; pp. 129–132. [Google Scholar]

- Shafer, S.M.; Rogers, D.F. A goal programming approach to the cell formation problem. J. Oper. Manag. 1991, 10, 28–43. [Google Scholar] [CrossRef]

- Arewa, A.; Owoputi, J.A.; Torbira, L.L. Financial statement management, liability reduction and asset accumulation: An application of goal programming model to a Nigerian Bank. Int. J. Financ. Res. 2013, 4, 83. [Google Scholar] [CrossRef] [Green Version]

- Romero, C.; Rehman, T. Multiple Criteria Analysis for Agricultural Decisions; Elsevier: Amsterdam, The Netherlands, 2003; Volume 11, pp. 23–45. [Google Scholar]

- Schniederjans, M.J.; Hoffman, J.J.; Sirmans, G.S. Using goal programming and the analytic hierarchy process in house selection. J. Real Estate Financ. Econ. 1995, 11, 167–176. [Google Scholar] [CrossRef]

- Mirzaee, H.; Naderi, B.; Pasandideh, S.H.R. A preemptive fuzzy goal programming model for generalized supplier selection and order allocation with incremental discount. Comput. Ind. Eng. 2018, 122, 292–302. [Google Scholar] [CrossRef]

- Hoe, L.W.; Siew, L.W.; Fun, L.P. Optimizing the Financial Management of Electronic Companies using Goal Programming Model. J. Phys. Conf. Ser. 2021, 2070, 012046. [Google Scholar] [CrossRef]

- Choudhary, D.; Shankar, R. A goal programming model for joint decision making of inventory lot-size, supplier selection and carrier selection. Comput. Ind. Eng. 2014, 71, 1–9. [Google Scholar] [CrossRef]

- Schniederjans, M.J.; Wilson, R.L. Using the analytic hierarchy process and goal programming for information system project selection. Inf. Manag. 1991, 20, 333–342. [Google Scholar] [CrossRef]

- Lakshmi, K. Vasantha, Harish Babu GA, and Uday Kumar KN. Application of Goal Programming Model for Optimization of Financial Planning: Case Study of a Distribution Company. Palest. J. Math. 2021, 10, 144–150. [Google Scholar]

- Schniederjans, M.J.; Schniederjans, D.; Cao, Q. Value analysis planning with goal programming. Ann. Oper. Res. 2017, 251, 367–382. [Google Scholar] [CrossRef]

- AlArjani, A.; Alam, T. Lexicographic Goal Programming Model for Bank’s Performance Management. J. Appl. Math. 2021, 2021, 8011578. [Google Scholar] [CrossRef]

- Fechete, F.; Nedelcu, A. Multi-Objective Optimization of the Organization’s Performance for Sustainable Development. Sustainability 2022, 14, 9179. [Google Scholar] [CrossRef]

- Aouni, B.; McGillis, S.; Abdulkarim, M.E. Goal programming model for management accounting and auditing: A new typology. Ann. Oper. Res. 2017, 251, 41–54. [Google Scholar] [CrossRef]

{kind=link}

| Notation | Description |

|---|---|

| m | Number of goals |

| p | Constraints of the system |

| n | Number of decision variables |

| Z | Objective function (Summation of all deviations) |

| Coefficient associated with variable j in the ith goal | |

| Variable that represents the jth decision | |

| bi | Value associated with the right-hand side |

| Negative deviation from the ith goal (underachievement) | |

| Positive deviation from the target (overachievement) | |

| Preemptive importance factors of the ith goal. | |

| Non-negative constants that represent relative weights for positive deviations | |

| Non-negative constants that represent relative weights for negative deviations | |

| Target levels of ith goal |

| Minimize | Goal | If Goal Is Achieved |

|---|---|---|

| Minimize the underachievement | . | |

| Minimize the overachievement | . | |

| Minimize both underachievement and overachievement | . |

| Goals | Priority |

|---|---|

| Evaluating the Maximized total assets | |

| Evaluating the Minimized total liabilities | |

| Evaluating the Maximized total equity | |

| Evaluating the Maximized Gross profit | |

| Evaluating the Maximized operating income | |

| Evaluating the Maximized net income | |

| Evaluating the Maximized total goal achievements |

| Target | Fiscal Year Is January–December (All Values in SAR Trillion) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | Total | |

| Total assets | 0.3176 | 0.3328 | 0.3384 | 0.3391 | 0.34 | 0.3279 | 0.3169 | 0.3225 | 0.3197 | 0.3104 | 0.2955 | 3.5607 |

| Total liabilities | 0.1514 | 0.1436 | 0.1402 | 0.1324 | 0.1286 | 0.118 | 0.1066 | 0.1123 | 0.0983 | 0.0991 | 0.1012 | 1.3318 |

| Total equity | 0.1661 | 0.1892 | 0.1982 | 0.2067 | 0.2114 | 0.2099 | 0.2103 | 0.2101 | 0.2214 | 0.2113 | 0.1942 | 2.2289 |

| Gross profit | 0.0485 | 0.0621 | 0.0543 | 0.0553 | 0.0517 | 0.043 | 0.0409 | 0.05 | 0.0576 | 0.0355 | 0.0229 | 0.5219 |

| Total operating income | 0.0296 | 0.0421 | 0.0409 | 0.0426 | 0.038 | 0.0533 | 0.0397 | 0.0387 | 0.0447 | 0.0356 | 0.022 | 0.4272 |

| Net income | 0.0215 | 0.0292 | 0.0248 | 0.0253 | 0.0233 | 0.0188 | 0.0178 | 0.0184 | 0.0215 | 0.0085 | 0.0013 | 0.2105 |

| Total | 0.7349 | 0.7991 | 0.7969 | 0.8013 | 0.793 | 0.7709 | 0.7322 | 0.752 | 0.7633 | 0.7003 | 0.6371 | 8.2811 |

| Goal | Outcomes | Target |

|---|---|---|

| Accomplished | ||

| Accomplished | ||

| Accomplished | ||

| Accomplished | ||

| Accomplished | ||

| Accomplished | ||

| Accomplished |

| Goal | ||

|---|---|---|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Alam, T. Modeling and Analyzing a Multi-Objective Financial Planning Model Using Goal Programming. Appl. Syst. Innov. 2022, 5, 128. https://doi.org/10.3390/asi5060128

Alam T. Modeling and Analyzing a Multi-Objective Financial Planning Model Using Goal Programming. Applied System Innovation. 2022; 5(6):128. https://doi.org/10.3390/asi5060128

Chicago/Turabian StyleAlam, Teg. 2022. "Modeling and Analyzing a Multi-Objective Financial Planning Model Using Goal Programming" Applied System Innovation 5, no. 6: 128. https://doi.org/10.3390/asi5060128

APA StyleAlam, T. (2022). Modeling and Analyzing a Multi-Objective Financial Planning Model Using Goal Programming. Applied System Innovation, 5(6), 128. https://doi.org/10.3390/asi5060128