Blockchain-Based Business Process Management (BPM) for Finance: The Case of Credit and Claim Requests

Abstract

:1. Introduction

- Blockchain records are secure and reliable,

- Blockchain are immutable, therefore one block/record cannot be changed,

- There is no need to validate the data by a third party.

- All the parties involved in the loan application, revision, and approval will have a single view of the data in a distributed ledger and blockchain platform;

- Manual processes can be automated, via checks of the data coded into blocks of blockchain and the use of “smart contracts”;

- The whole process is immutable, and everyone can see changes in status in the application; there is clear visibility of ownership, which makes it easy also to be a subject of audits, and the whole process is transparent.

2. Blockchain-Related Literature Overview

2.1. The Most Recent Developments in Blockchain Technologies on the Application in Insurance, Auditing, and Banking

2.2. Related Works

3. Research Methodology

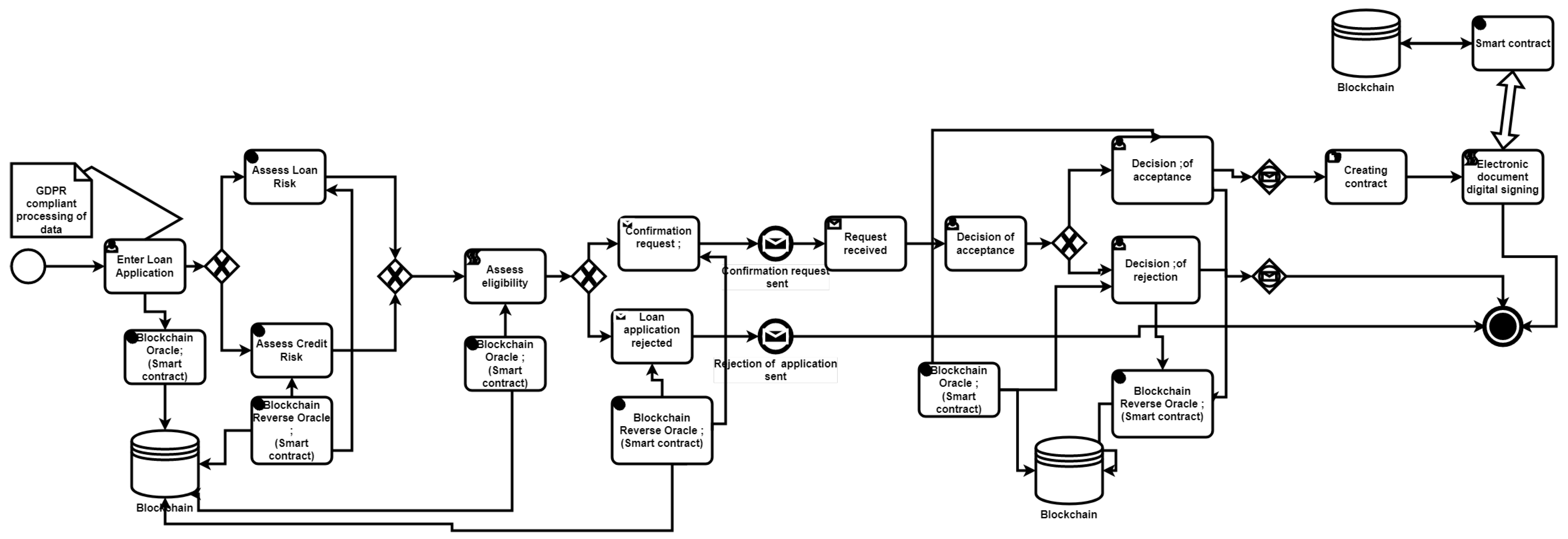

4. Loan Business Process

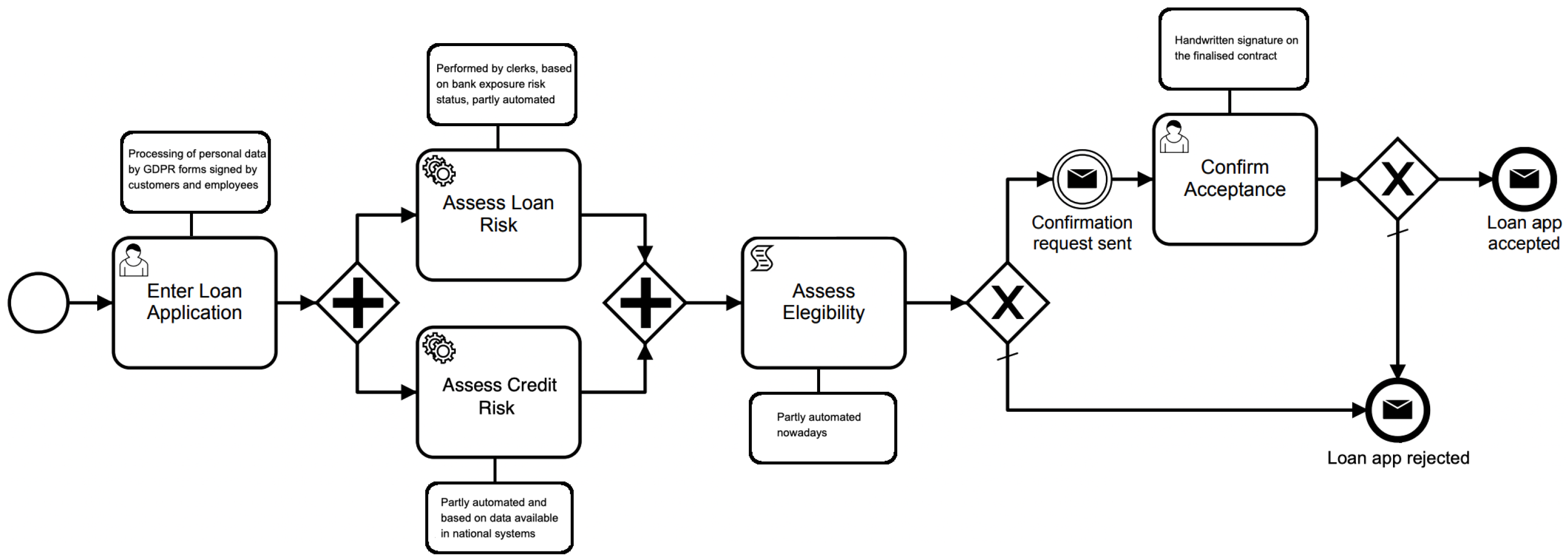

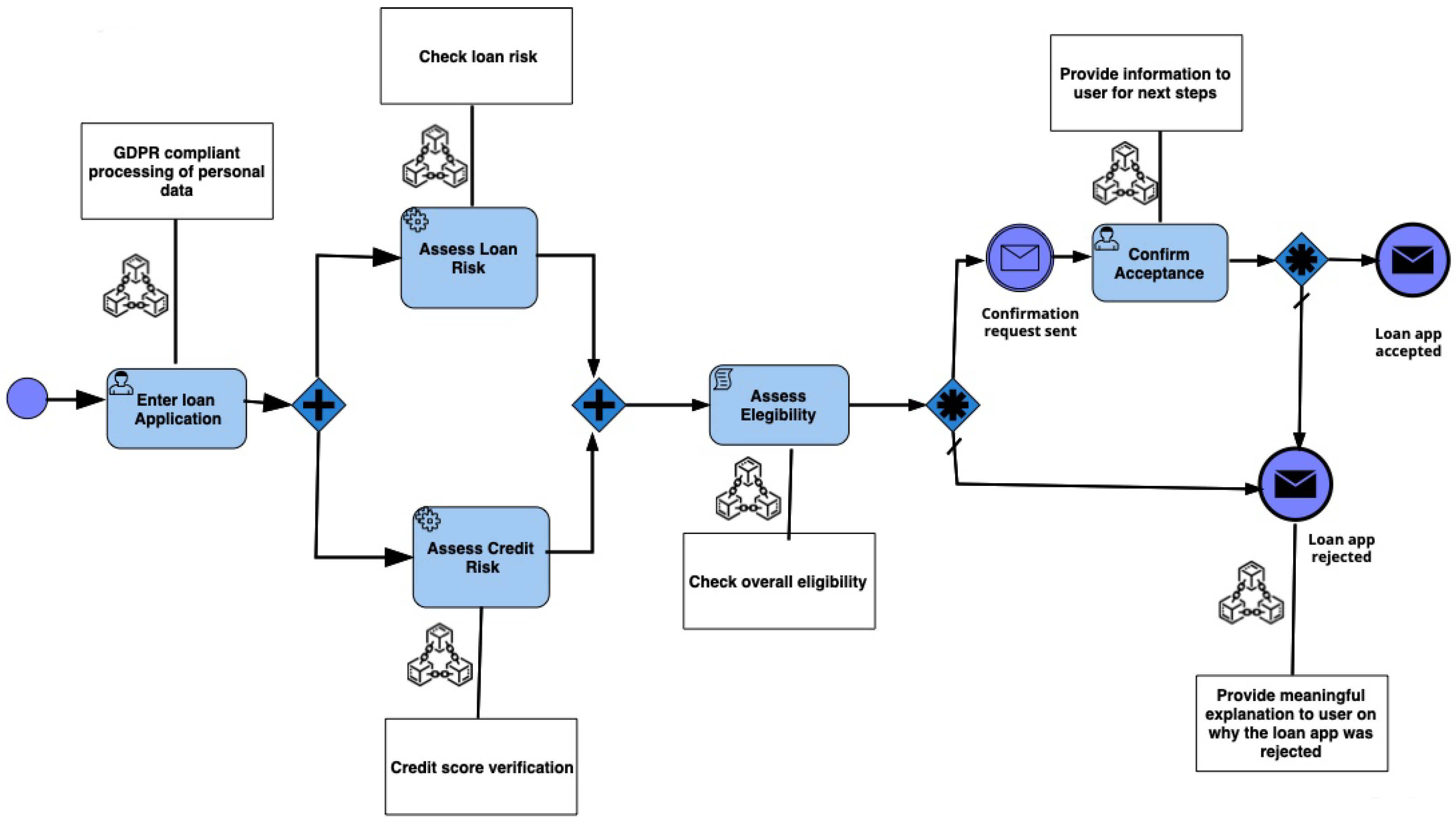

4.1. Loan Process Business Process Pattern with Blockchain

- Introduction and story of the business process case: the loan application is one of the most common operations banks perform. Banks face a demand for credit, so the primary role of their staff is to screen applicants and monitor outstanding loans. Loan officers perform an important strategic task in the process of a loan application, by evaluating loan risk and checking the previous credit scores of the applicant.

- Current situation faced: current loan applications are lengthy in time and require specialized personnel with lots of experience to process them. The current loan processes foresee the evaluation of eligibility by loan officers, and this analysis may often not be visible to other managers and departments within the bank. In addition, customers often complain about the lack of clarity and transparency in the processes of the bank, and the lack of a clear understanding of the steps and checks that the bank performs regarding their requests. It may not be understandable to the end customers why their loan was rejected. If this is the case, it is necessary to know what the reason was (due to low credit score in risk analysis, or does the risk seem too big for the bank to undertake?). Lastly, data must be treated in accordance with GDPR [57].

- Action taken: the underlying technological solution, such as the one that we propose in this paper, based on blockchain technology, can improve the execution of the process and make the process more transparent.

- Lessons learned: based on our previous works [58,59], we understood that financial companies are slow adaptors of new technologies. Technical teams, working on loan technology solutions, would need to perform mapping between their current solutions and the solution as described in our article, then critically analyze the feasibility of the transformation for their company from different points of view, namely technical and managerial viewpoints.

- It gives companies the ability to assemble teams around such developments freely, which can include “smart contracts”, and allow the company to automatize business processes.

- Identities are created for past and current events to be recognized, e.g., new employees of companies can also see past actions on blockchain and act in line with previous decisions made, helping pass knowledge in the company.

- Institutional memory: there are indelible extracts of all transactions and past actions of the company.

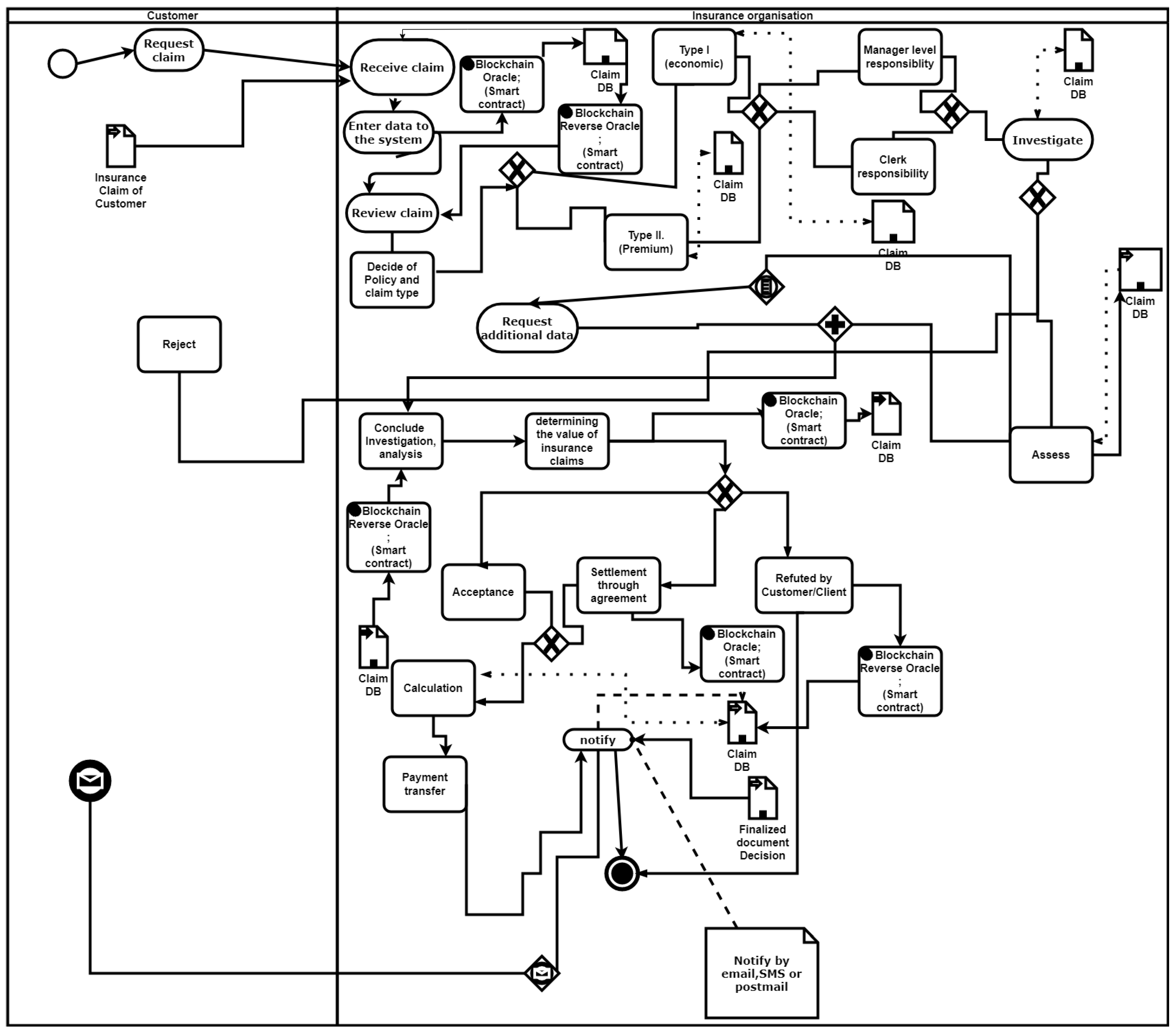

4.2. Insurance Claim Process

4.3. Loan BPM Implementation as a Web Service

- Conformance examination aims to test whether the behavior of the instance of a process model is in line with the prescribed requirements for the single process model;

- Compliance investigation contains techniques to audit whether the regulation, rules, prescriptions, and constraints are satisfied in the instance of the business process;

- XAI, explainable AI The AI (ML, machine learning, D.Sc., data science) algorithms give the foundation for decision-making. In a business process, some humans play active roles and there are some who play passive roles or only monitor the results. The AI algorithm should provide information that is interpretable to humans. This interpretable information might have been created through specific activities that might consist of web services invoking blockchain patterns, services that are a façade of AI algorithms, and conveying the basic information that can be translated into an interpretable format.

- Oracle and reverse-oracle pattern provides the communication channel between the closed blockchain environment and the execution of business process models;

- Off-chain data storage can be used since the representation of the instance of a business process and the documents that are involved in transactions may generate a volume of data that are hard to store in blocks and that are stored in external storage;

- Contract patterns. The smart contracts yield the tool and interface to describe the business rules that are realized in web services that are devoted to representing business entities and activities of business processes. The relevant smart contracts can interpret the business roles codified in web services.

4.4. Advantages and Challenges for Financial Companies in the Application of Blockchain Technology

- Agility gives companies the ability to assemble teams around such developments freely, which can include “smart contracts”, and allow the company to automatize business processes;

- Actions that were created in relation to past and current loan applications will be visible to all; e.g., new employees of companies can also see past actions on blockchain and act in line with previous decisions made, helping pass knowledge in the company;

- Institutional memory: that is, there are indelible extracts of all transactions and past actions of the company.

GDPR and Related Legal Issues of Privacy

- Requesting authentic documents. The financial institution (either bank, insurance company. or any other type) should access subject-specific authentic documents and information. In the case of a loan request, information should be collected about the requestor. In the recent FinTech framework, the financial institution may use credit bureaus. One of the credit bureaus can provide basic information about the requestor person, or the legal entity, to filter out potential customers with deceitful or unfavorable data. The other credit bureau can provide data that can be obtained from the banks that may have the requestor as a regular customer. Typical data that should be scored includes debt and loans of credit cards, performance of the payments, and how many bank accounts and credit/debit cards the potential customer may have. In recent cyberspace, data can be collected from telecommunication companies, retail chains, and utilities about invoice settlements.There are countries with central citizenship registration so that the existence of a person can be checked; in the case of companies, the company court serves as the validation of the existence of a firm. All interchange of data, electronic records, or documents can be based on blockchain technology to ensure the authenticity and validity of the communicated data. Although other technologies can be used, blockchain technology provides a seamless data interchange either in inter- or intra-organizational scenarios. In the case of an insurance claim, the customer’s data should be verified through retrieval from the database. Then, the insurance policy and the type should be checked after assessment of the damage assessment should be made. After the evaluation, a decision is made about disbursement, taking into account the claim and the actual damage. Blockchain technology and smart contracts can be employed for tracking documents, saving events and decisions, and furthermore controlling compliance to the various related regulations. The business rules for controlling whether the clerk who handles the customers’ data is authorized or the documents and data are authentic can be enforced and traced through smart contracts.

- Transparency through tracking. People are interested in the usage of their data, and they like to control their access. The industrialized nations have laws and regulations in force that oblige the firms to conform [80,81,82]. Blockchain technology offers trustworthy, reliable, and immutable solutions for audit trails. Such audit trails make the work of auditors more conducive, grounded, and dependable.

- Data protection of PII: The individuals who in either use case are concerned with sharing their data and want to give access only to those persons and institutions that are legally authorized. The usage of their PII is necessary for the actual business processes. Outside the business processes and authorized persons involved in the actual activities who should use the data, nobody else can access the data. Blockchain technology, smart contracts, web services, and controlled message-passing mechanisms can yield a solution that enforces and maintains compliance with the regulations [66].

- Integrity rules. In the smart contracts, the integrity rules can be codified in an operationalizational way that complies with GDPR, the Data and AI Act, and the business rules of the company [83,84,85,86]. Smart contracts can define business rules for both the inter- and intra-organizational relationships to enforce data and other governance rules automatically. In inter-organizational communication, those PIIs can be shared (only what is necessary for other organizations and conforming to the regulations of authorities that give and maintain permission for data handling).According to GDPR, the data can be gathered and retained only for the goals that are specified in the data handling policy. The policy and the related smart contracts should contain the following elements, however, the list is illustrative, non-complete, and not exhaustive: (a) information about the data-gathering methods and the utilization of PIIs, (b) constraints on the retention period of the collected data, (c) providing information to the new customers about the data privacy policy including the data handling, (d) the explicit goals of the data gathering, (e) how the security of data gathered is ensured, and (f) how the customers/consumers and the other users can obtain access rights to the gathered data and make use of it.

5. Contribution

- Model: A meta-model for AD was developed that made it possible that model-checking relational logical predicates could be formulated. The checking of the soundness of the model through the logical predicates uses the AD meta-model and Alloy. A set of logical rules as a representation of model checking was elaborated. Using the meta-model and before-mentioned patterns, a method is defined for detecting the dubious or defective components of business problems.

- Architecture: The facilities for the meta-modeling of YAWL were utilized for UML AD [90,91]. Acceleo is a plug-in for the Eclipse modeling framework that supports model-driven architecture [92,93,94,95,96,97]. Alloy supports relational logic for the model-checking of software systems [39,40]. Papyrus is a Java plug-in and a graphical editor that helps manipulate and transform diagrams, according to model-to-text (M2T) paradigms [98,99,100].

- Method: We used the design science research and software case study research method to assess the results of the research work [47,48,101]. During the research work, we employed disciplined software-engineering methods in the form of object-oriented analysis and design. For program code generation, we exploited the above-mentioned toolset (Eclipse, Acceleo, and Papyrus). We utilized the capability of YAWL and Papyrus to define the meta-model and fit the meta-model to the purpose. To obtain the requirements for two case study-level experiments, we consulted the partners at companies with structured interviews.

- Implementation: Acceleo and Papyrus were used for software model transformation. YAWL was applied to interpret the XML representation of business processes and the workflows; moreover, the meta-modeling and model-checking capability of YAWL was utilized for the workflows. The YAWL model-checking ability focuses on the structure of the workflows, so we inserted a step for model-checking other properties of the specified business processes, for example, the correct application of SOA and blockchain patterns.

6. Summary

Future Work

7. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| Article specific | |

| AD | UML Activity Diagram |

| M2T | Model-to-Text |

| M2P | Model-to-Program |

| SOA | Service Oriented Architecture |

| PII | Personal Identifying Information |

| IS | Information System |

| IT | Information Technology |

| IT/IS | Information Technology and Information System |

| ERP | Enterprise Resource-Planning System |

| ITIL | Information Technology Infrastructure Library |

| TOGAF | The Open Group Architecture Framework |

| XML | Extensible Markup Language |

| JSON | JavaScript Object Notation |

| DBMS | Database Management System |

| BPMN | Business Process modeling Notation standard version 2.0 |

| DOM | Document Object Model |

References

- Van Der Aalst, W.M.; La Rosa, M.; Santoro, F.M. Business process management. Bus. Inf. Syst. Eng. 2016, 58, 1–6. [Google Scholar] [CrossRef]

- Du, W.D.; Pan, S.L.; Leidner, D.E.; Ying, W. Affordances, experimentation and actualization of FinTech: A blockchain implementation study. J. Strateg. Inf. Syst. 2019, 28, 50–65. [Google Scholar] [CrossRef]

- Thomas, D. Blockchain as a Backbone to Asset and Wealth Creation. In The WealthTech Book: The FinTech Handbook for Investors, Entrepreneurs and Finance Visionaries; Wiley: Hoboken, NJ, USA, 2018; pp. 170–172. [Google Scholar]

- Brown, R.G.; Carlyle, J.; Grigg, I.; Hearn, M. Corda: An introduction. In R3 CEV, August; R3 CEV: New York, NY, USA, 2016; Volume 1, p. 14. [Google Scholar]

- Thuvarakan, M. Regulatory changes for redesigned securities markets with distributed ledger technology. Knowl. Eng. Rev. 2020, 35, e14. [Google Scholar] [CrossRef]

- Cho, S.; Lee, K.; Cheong, A.; No, W.G.; Vasarhelyi, M.A. Chain of values: Examining the economic impacts of blockchain on the value-added tax system. J. Manag. Inf. Syst. 2021, 38, 288–313. [Google Scholar] [CrossRef]

- Chavez-Dreyfuss, G. Sweden tests blockchain technology for land registry. Reuters. 16 June 2016. Available online: https://www.reuters.com/article/us-sweden-blockchain-idUSKCN0Z22KV (accessed on 3 March 2023).

- Lu, Y. Blockchain and the related issues: A review of current research topics. J. Manag. Anal. 2018, 5, 231–255. [Google Scholar] [CrossRef]

- Gorkhali, A.; Li, L.; Shrestha, A. Blockchain: A literature review. J. Manag. Anal. 2020, 7, 321–343. [Google Scholar] [CrossRef]

- Casino, F.; Dasaklis, T.K.; Patsakis, C. A systematic literature review of blockchain-based applications: Current status, classification and open issues. Telemat. Inform. 2019, 36, 55–81. [Google Scholar] [CrossRef]

- Eyal, I. Blockchain technology: Transforming libertarian cryptocurrency dreams to finance and banking realities. Computer 2017, 50, 38–49. [Google Scholar] [CrossRef]

- Dai, J.; Wang, Y.; Vasarhelyi, M.A. Blockchain: An emerging solution for fraud prevention. CPA J. 2017, 87, 12–14. [Google Scholar]

- Laroiya, C.; Saxena, D.; Komalavalli, C. Applications of blockchain technology. In Handbook of Research on Blockchain Technology; Elsevier: Amsterdam, The Netherlands, 2020; pp. 213–243. [Google Scholar]

- Wang, S.; Ouyang, L.; Yuan, Y.; Ni, X.; Han, X.; Wang, F.Y. Blockchain-enabled smart contracts: Architecture, applications, and future trends. IEEE Trans. Syst. Man Cybern. Syst. 2019, 49, 2266–2277. [Google Scholar] [CrossRef]

- Hewa, T.; Ylianttila, M.; Liyanage, M. Survey on blockchain based smart contracts: Applications, opportunities and challenges. J. Netw. Comput. Appl. 2021, 177, 102857. [Google Scholar] [CrossRef]

- Kassab, M.H.; DeFranco, J.; Malas, T.; Laplante, P.; Neto, V.V.G. Exploring Research in Blockchain for Healthcare and a Roadmap for the Future. IEEE Trans. Emerg. Top. Comput. 2019, 9, 1835–1852. [Google Scholar] [CrossRef]

- Cai, W.; Wang, Z.; Ernst, J.B.; Hong, Z.; Feng, C.; Leung, V.C. Decentralized applications: The blockchain-empowered software system. IEEE Access 2018, 6, 53019–53033. [Google Scholar] [CrossRef]

- López-Pintado, O.; García-Bañuelos, L.; Dumas, M.; Weber, I. Caterpillar: A Blockchain-Based Business Process Management System. In Proceedings of the Business Process Management, Barcelona, Spain, 10–15 September 2017. [Google Scholar]

- Edrud, P. Improving BPM with Blockchain Technology: Benefits, Costs, Criteria & Barriers. Master’s Thesis, Mid Sweden University, Sundsvall, Sweden, 2021. [Google Scholar]

- Viriyasitavat, W.; Da Xu, L.; Bi, Z.; Sapsomboon, A. Blockchain-based business process management (BPM) framework for service composition in industry 4.0. J. Intell. Manuf. 2020, 31, 1737–1748. [Google Scholar] [CrossRef]

- Al-Rakhami, M.S.; Al-Mashari, M. Blockchain and internet of things for business process management: Theory, challenges, and key success factors. Int. J. Adv. Comput. Sci. Appl. 2020, 11, 552–562. [Google Scholar] [CrossRef]

- Viriyasitavat, W.; Bi, Z.; Hoonsopon, D. Blockchain technologies for interoperation of business processes in smart supply chains. J. Ind. Inf. Integr. 2022, 26, 100326. [Google Scholar] [CrossRef]

- Di Ciccio, C.; Meroni, G.; Plebani, P. On the adoption of blockchain for business process monitoring. Softw. Syst. Model. 2022, 21, 915–937. [Google Scholar] [CrossRef]

- Belchior, R.; Guerreiro, S.; Vasconcelos, A.; Correia, M. A survey on business process view integration: Past, present and future applications to blockchain. Bus. Process. Manag. J. 2022, 28, 713–739. [Google Scholar] [CrossRef]

- Kherbouche, M.; Molnár, B. Modelling to Program in the case of Workflow Systems Theoretical background and literature review. In Proceedings of the 13th Joint Conference on Mathematics and Informatics, Budapest, Hungary, 1–3 October 2020; pp. 1–3. [Google Scholar]

- Kherbouche, M.; Molnár, B. Formal Model Checking and Transformations of Models Represented in UML with Alloy. In Proceedings of the International Workshop on Modelling to Program, Lappeenranta, Finland, 10–12 March 2020; Springer: Berlin/Heidelberg, Germany, 2020; pp. 127–136. [Google Scholar]

- Molnár, B.; Benczúr, A. The Application of Directed Hyper-Graphs for Analysis of Models of Information Systems. Mathematics 2022, 10, 759. [Google Scholar] [CrossRef]

- Molnár, B.; Benczúr, A.; Béleczki, A. A Model for Analysis and Design of Information Systems based on a Document Centric Approach. In Intelligent Information and Database Systems IIDS; Springer: Berlin/Heidelberg, Germany, 2016; pp. 290–299. [Google Scholar]

- Kherbouche, M.; Pisoni, G.; Molnár, B. Model to Program and Blockchain Approaches for Business Processes and Workflows in Finance. Appl. Syst. Innov. 2022, 5, 10. [Google Scholar] [CrossRef]

- Lauster, C.; Klinger, P.; Schwab, N.; Bodendorf, F. Literature Review Linking Blockchain and Business Process Mangement. In Proceedings of the 15th International Conference on Wirtschaftsinformatik Band-1, Potsdam, Germany, 8–11 March 2020. [Google Scholar]

- Mendling, J.; Weber, I.; Aalst, W.V.D.; Brocke, J.V.; Cabanillas, C.; Daniel, F.; Debois, S.; Ciccio, C.D.; Dumas, M.; Dustdar, S.; et al. Blockchains for business process management-challenges and opportunities. ACM Trans. Manag. Inf. Syst. (TMIS) 2018, 9, 1–16. [Google Scholar] [CrossRef]

- Atik, A.; Kelten, G. Blockchain Technology and Its Potential Effects on Accounting: A Systematic Literature Review. Istanb. Bus. Res. 2021, 50, 495–515. [Google Scholar] [CrossRef]

- Badhwar, A.; Islam, S.; Tan, C.S.L. Exploring the potential of blockchain technology within the fashion and textile supply chain with a focus on traceability, transparency, and product authenticity: A systematic review. Front. Blockchain 2023, 6, 1044723. [Google Scholar] [CrossRef]

- Indriasari, E.; Prabowo, H.; Gaol, F.L.; Purwandari, B. Digital Banking. Int. J. E-Bus. Res. 2022, 18, 1–20. [Google Scholar] [CrossRef]

- Tyagi, A.K.; Dananjayan, S.; Agarwal, D.; Ahmed, H.F.T. Blockchain—Internet of Things Applications: Opportunities and Challenges for Industry 4.0 and Society 5.0. Sensors 2023, 23, 947. [Google Scholar] [CrossRef]

- Thalheim, B. From Models_For_Programming to Modelling_To_Program and Towards Models_As_A_Program. In Modelling to Program; Springer: Berlin/Heidelberg, Germany, 2021; pp. 3–44. [Google Scholar] [CrossRef]

- Laurent, Y.; Bendraou, R.; Baarir, S.; Gervais, M.P. Alloy4SPV: A Formal Framework for Software Process Verification. In Modelling Foundations and Applications; Springer: Berlin/Heidelberg, Germany, 2014; pp. 83–100. [Google Scholar] [CrossRef]

- Ringert, J.O.; Sullivan, A. Abstract Alloy Instances. In Formal Methods; Springer: Berlin/Heidelberg, Germany, 2023; pp. 364–382. [Google Scholar] [CrossRef]

- AlloyTools. 2023. Available online: https://github.com/AlloyTools (accessed on 15 April 2023).

- Rivadeh, M.; Mirian-Hosseinabadi, S.H. Formal translation of YAWL workflow models to the Alloy formal specifications: A testing application. Softw. Syst. Model. 2022. [Google Scholar] [CrossRef]

- Miles, I. Service Innovation. In Handbook of Service Science; Springer: New York, NY, USA, 2010; pp. 511–533. [Google Scholar] [CrossRef]

- Chen, C.L.; Deng, Y.Y.; Tsaur, W.J.; Li, C.T.; Lee, C.C.; Wu, C.M. A Traceable Online Insurance Claims System Based on Blockchain and Smart Contract Technology. Sustainability 2021, 13, 9386. [Google Scholar] [CrossRef]

- Hassan, A.; Ali, M.I.; Ahammed, R.; Khan, M.M.; Alsufyani, N.; Alsufyani, A. Secured Insurance Framework Using Blockchain and Smart Contract. Sci. Program. 2021, 2021, 6787406. [Google Scholar] [CrossRef]

- Bennacer, S.A.; Sabiri, K.; Aaroud, A.; Akodadi, K.; Cherradi, B. A comprehensive survey on blockchain-based healthcare industry: Applications and challenges. Indones. J. Electr. Eng. Comput. Sci. 2023, 30, 1558–1571. [Google Scholar] [CrossRef]

- Han, H.; Shiwakoti, R.K.; Jarvis, R.; Mordi, C.; Botchie, D. Accounting and auditing with blockchain technology and artificial Intelligence: A literature review. Int. J. Account. Inf. Syst. 2023, 48, 100598. [Google Scholar] [CrossRef]

- Konstantinidis, I.; Siaminos, G.; Timplalexis, C.; Zervas, P.; Peristeras, V.; Decker, S. Blockchain for Business Applications: A Systematic Literature Review. In Business Information Systems; Springer: Berlin/Heidelberg, Germany, 2018; pp. 384–399. [Google Scholar] [CrossRef]

- Rainer, A. Case Study Research in Software Engineering Guidelines and Examples; Wiley: Hoboken, NJ, USA, 2012. [Google Scholar]

- Wieringa, R.J. Design Science Methodology for Information Systems and Software Engineering; Springer: Berlin/Heidelberg, Germany, 2014. [Google Scholar] [CrossRef]

- Störrle, H.; Hausmann, J.H. Towards a formal semantics of UML 2.0 activities. In Proceedings of the Software Engineering 2005; Liggesmeyer, P., Pohl, K., Goedicke, M., Eds.; Gesellschaft für Informatik: Bonn, Germany, 2005; pp. 117–128. [Google Scholar]

- Geambaşu, C.V. BPMN vs. UML activity diagram for business process modeling. Account. Manag. Inf. Syst. 2012, 11, 637–651. [Google Scholar]

- Russell, N.; van der Aalst, W.M.P.; ter Hofstede, A.H. Workflow Patterns; MIT Press Ltd.: Cambridge, MA, USA, 2016. [Google Scholar]

- Xu, X.; Weber, I.; Staples, M. Architecture for Blockchain Applications; Springer: Cham, Switzerland, 2019. [Google Scholar] [CrossRef]

- Malone, T.W.; Crowston, K.; Herman, G.A. Organizing Business Knowledge: The MIT Process Handbook; The MIT Press: Cambridge, MA, USA, 2003. [Google Scholar]

- APQC. APQC Process Classification Framework (PCF)—Banking PCF—PDF Version 1.0.0. 2023. Available online: https://www.apqc.org/resource-library/resource-listing/apqc-process-classification-framework-pcf-banking-pcf-pdf-3 (accessed on 28 January 2023).

- APQC. APQC Process Classification Framework (PCF)—Cross Industry—Excel Version 7.2.1. 2023. Available online: https://www.apqc.org/resource-library/resource-listing/apqc-process-classification-framework-pcf-cross-industry-excel-7 (accessed on 28 January 2023).

- Brocke, J.v.; Mendling, J. Frameworks for business process management: A taxonomy for business process management cases. In Business Process Management Cases; Springer: Berlin/Heidelberg, Germany, 2018; pp. 1–17. [Google Scholar]

- Herian, R. Regulating disruption: Blockchain, Gdpr, and questions of data sovereignty. J. Internet Law 2018, 22, 1–16. [Google Scholar]

- Pisoni, G.; Molnár, B.; Tarcsi, Á. Data Science for Finance: Best-Suited Methods and Enterprise Architectures. Appl. Syst. Innov. 2021, 4, 69. [Google Scholar] [CrossRef]

- Pisoni, G. Going digital: Case study of an Italian insurance company. J. Bus. Strategy 2020, 42, 106–115. [Google Scholar] [CrossRef]

- Kherbouche, M.; Zghal, Y.; Molnár, B.; Benczúr, A. The Use of M2P in Business Process Improvement and Optimization. In ADBIS 2022: New Trends in Database and Information Systems; Scimago Q4; Springer: Berlin/Heidelberg, Germany, 2022; pp. 109–118. [Google Scholar] [CrossRef]

- Seijas, P.L.; Thompson, S. Marlowe: Financial Contracts on Blockchain; Lecture Notes in Computer Science; Springer: Berlin/Heidelberg, Germany, 2018; pp. 356–375. [Google Scholar] [CrossRef]

- Xu, X.; Weber, I.; Staples, M. Blockchain Patterns. In Architecture for Blockchain Applications; Springer: Berlin/Heidelberg, Germany, 2019. [Google Scholar]

- Lo, S.K.; Xu, X.; Chiam, Y.K.; Lu, Q. Evaluating Suitability of Applying Blockchain. In Proceedings of the 22nd IEEE International Conference on Engineering of Complex Computer Systems (ICECCS), Fukuoka, Japan, 5–8 November 2017. [Google Scholar] [CrossRef]

- Morabito, V. Business Innovation through Blockchain: The B³ Perspective; Springer: Cham, Switzerland, 2017. [Google Scholar] [CrossRef]

- von Rosing, M.; von Scheel, H.; Scheer, A.W. The Complete Business Process Handbook: Body of Knowledge from Process Modeling to Bpm; Morgan Kaufmann Publishers Inc.: Burlington, MA, USA, 2014; Volume 1. [Google Scholar]

- Erl, T. Service-Oriented Architecture: Analysis and Design for Services and Microservices; Prentice Hall, Service Tech Press: Boston, MA, USA, 2017. [Google Scholar]

- Voigt, P.; von dem Bussche, A. The EU General Data Protection Regulation (GDPR); Springer: Berlin/Heidelberg, Germany, 2017. [Google Scholar]

- Fraga-Lamas, P.; Fernández-Caramés, T.M. Leveraging Blockchain for Sustainability and Open Innovation: A Cyber-Resilient Approach toward EU Green Deal and UN Sustainable Development Goals. In Computer Security Threats; IntechOpen: London, UK, 2020. [Google Scholar]

- Ye, C.; Li, G.; Cai, H.; Gu, Y.; Fukuda, A. Analysis of security in blockchain: Case study in 51%—Attack detecting. In Proceedings of the 5th IEEE International Conference on Dependable Systems and Their Applications (DSA), Dalian, China, 22–23 September 2018; pp. 15–24. [Google Scholar]

- Sayeed, S.; Marco-Gisbert, H. Assessing blockchain consensus and security mechanisms against the 51% attack. Appl. Sci. 2019, 9, 1788. [Google Scholar] [CrossRef]

- Commission Nationale Informatique et des Libertés. Blockchain and the GDPR: Solutions for a Responsible Use of the Blockchain in the Context of Personal Data. 2018. Available online: https://www.cnil.fr/en/blockchain-and-gdpr-solutions-responsible-use-blockchain-context-personal-data (accessed on 15 January 2023).

- Beckers, K. Kristian Beckers; Springer: Berlin/Heidelberg, Germany, 2015; p. 474. [Google Scholar] [CrossRef]

- Molnár, B.; Pisoni, G.; Tarcsi, Á. Data Lakes for Insurance Industry: Exploring Challenges and Opportunities for Customer Behaviour Analytics, Risk Assessment, and Industry Adoption. In Proceedings of the 17th International Conference on e-Business, ICE-B 2020, Hong Kong, China, 5–8 December 2020. [Google Scholar]

- Bouafia, K.; Molnár, B. Analysis Approach for Enterprise Information Systems Architecture Based on Hypergraph to Aligned Business Process Requirements. In Proceedings of the CENTERIS—International Conference on ENTERprise Information Systems/ProjMAN—International Conference on Project MANagement/HCist—International Conference on Health and Social Care Information Systems and Technologies, Heraklion, Greece, 3–5 May 2019; Scika Science and Technology Publications: Valletta, Malta, 2019. [Google Scholar] [CrossRef]

- Smart, N.P. Cryptography: An Introduction; McGraw-Hill: New York, NY, USA, 2003; Volume 3, p. 433. [Google Scholar]

- Katz, J.; Lindell, Y. Introduction to Modern Cryptography, 3rd ed.; Taylor & Francis Group: Abingdon, UK, 2020. [Google Scholar]

- Zheng, Z. Modern Cryptography Volume 1. A Classical Introduction to Informational and Mathematical Principle; Springer: Singapore, 2022. [Google Scholar]

- Zheng, Z.; Tian, K.; Liu, F. Modern Cryptography Volume 2. A Classical Introduction to Informational and Mathematical Principle; Springer: Singapore, 2022. [Google Scholar]

- Fekete, D.L.; Kiss, A. A Survey of Ledger Technology-Based Databases. Future Internet 2021, 13, 197. [Google Scholar] [CrossRef]

- Akhigbe, A.; Whyte, A.M. The Gramm-Leach-Bliley Act of 1999: Risk implications for the financial services industry. J. Financ. Res. 2004, 27, 435–446. [Google Scholar] [CrossRef]

- Lee, W.B.; Lee, C.D. A Cryptographic Key Management Solution for HIPAA Privacy/Security Regulations. IEEE Trans. Inf. Technol. Biomed. 2008, 12, 34–41. [Google Scholar] [CrossRef]

- Ricardo, C.C. HS.Register—An audit-trail tool to respond to the General Data Protection Regulation (GDPR). Stud. Health Technol. Inform. 2018, 247, 81. [Google Scholar]

- Government of Canada. Government of Canada’s Artificial Intelligence and Data Act: Brief Overview. 2023. Available online: https://www.osler.com/en/resources/regulations/2022/government-of-canada-s-artificial-intelligence-and-data-act-brief-overview (accessed on 23 February 2023).

- Force, J.T. Security and Privacy Controls for Information Systems and Organizations. CSRC | NIST. 2020. Available online: https://csrc.nist.gov/publications/detail/sp/800-53/rev-5/archive/2020-09-23 (accessed on 24 February 2023).

- Ruohonen, J. Recent Trends in Cross-Border Data Access by Law Enforcement Agencies. arXiv 2023, arXiv:2302.09942. [Google Scholar]

- EU. The Artificial Intelligence Act. 2021. Available online: https://artificialintelligenceact.eu/the-act (accessed on 24 February 2023).

- Erl, T. SOA Design Patterns; Prentice Hall: Hoboken, NJ, USA, 2009; p. 814. [Google Scholar]

- Achouri, A.; Ayed, L.J.B. A Formal Semantic for UML 2.0 Activity Diagram based on Institution Theory. arXiv 2016, arXiv:1606.02311. [Google Scholar]

- Yaoqiang. BPMN Modeler. 2019. Available online: https://sourceforge.net/projects/bpmn/ (accessed on 21 April 2023).

- About the Unified Modeling Language Specification Version 2.5.1. 2023. Available online: https://www.omg.org/spec/UML (accessed on 21 April 2023).

- YAWL BPM. 2023. Available online: https://yawlfoundation.github.io, (accessed on 21 April 2023).

- desRivieres, J.; Wiegand, J. Eclipse: A platform for integrating development tools. IBM Syst. J. 2004, 43, 371–383. [Google Scholar] [CrossRef]

- Eclipse Foundation. Eclipse Downloads|The Eclipse Foundation. 2023. Available online: https://www.eclipse.org/downloads (accessed on 21 April 2023).

- Deeba, F.; Kun, S.; Shaikh, M.; Dharejo, F.A.; Hayat, S.; Suwansrikham, P. Data transformation of UML diagram by using model driven architecture. In Proceedings of the 3rd IEEE International Conference on Cloud Computing and Big Data Analysis (ICCCBDA), Chengdu, China, 20–22 April 2018; pp. 300–303. [Google Scholar]

- Mtsweni, J. Exploiting UML and acceleo for developing Semantic Web Services. In Proceedings of the 2012 International Conference for Internet Technology and Secured Transactions, London, UK, 10–12 December 2012; pp. 753–758. [Google Scholar]

- Acceleo | Home. 2023. Available online: https://www.eclipse.org/acceleo (accessed on 21 April 2023).

- Bast, W.; Kleppe, A.G.; Warmer, J.B. MDA Explained: The Model Driven Architecture™: Practice and Promise, 1st ed.; Addison-Wesley Professional: Boston, MA, USA, 2003. [Google Scholar]

- Essebaa, I.; Chantit, S.; Ramdani, M. MoDAr-WA: Tool Support to Automate an MDA Approach for MVC Web Application. Computers 2019, 8, 89. [Google Scholar] [CrossRef]

- Wei, R.; Zolotas, A.; Rodriguez, H.H.; Gerasimou, S.; Kolovos, D.S.; Paige, R.F. Automatic generation of UML profile graphical editors for Papyrus. Softw. Syst. Model. 2020, 19, 1083–1106. [Google Scholar] [CrossRef]

- Papyrus. 2023. Available online: https://www.eclipse.org/papyrus (accessed on 21 April 2023).

- Johannesson, P.; Perjons, E. An Introduction to Design Science; Springer: Berlin/Heidelberg, Germany, 2014. [Google Scholar] [CrossRef]

- Ariouat, H.; Hanachi, C.; Andonoff, É.; Benaben, F. A conceptual framework for social business process management. Procedia Comput. Sci. 2017, 112, 703–712. [Google Scholar] [CrossRef]

- Viriyasitavat, W.; Hoonsopon, D. Blockchain characteristics and consensus in modern business processes. J. Ind. Inf. Integr. 2019, 13, 32–39. [Google Scholar] [CrossRef]

- Fanning, K.; Centers, D.P. Blockchain and its coming impact on financial services. J. Corp. Account. Financ. 2016, 27, 53–57. [Google Scholar] [CrossRef]

- Milani, F.; García-Bañuelos, L.; Dumas, M. Blockchain and business process improvement. BPTrends Newsletter, 3 October 2016. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Title of Publication | Author(s) | Year | Summary of the Publication | Assessment |

|---|---|---|---|---|

| A comprehensive survey on blockchain-based healthcare industry: applications and challenges [44] | S.A. Bennacer, K. Sabiri, A. Aaroud, K. Akodadi, and B. Cherradi | 2023 | The paper presents a comprehensive survey on the applications and challenges of blockchain technology in the healthcare industry. The authors use the PRISMA approach and review 56 research publications in high-ranking scientific journals from 2016 to 2022. The paper discusses how blockchain technology can potentially address a variety of challenges faced by healthcare systems, such as data management, security, data sharing, and patient privacy. The study identifies the potential of blockchain technology to assist patients and healthcare providers in diagnosis and data processing. | The paper provides a valuable overview of the current state of blockchain technology in the healthcare industry. The authors use a systematic approach to review a large number of research publications, highlighting the potential applications of blockchain technology in healthcare. However, the study does not provide a detailed analysis of the challenges and limitations of implementing blockchain technology in the healthcare industry, which could have added further value to the paper. |

| Accounting and auditing with blockchain technology and artificial Intelligence: A literature review [45] | H. Han, R.K. Shiwakoti, R. Jarvis, C. Mordi, and D. Botchie | 2023 | The paper surveys the literature on the impact of blockchain technology on accounting and auditing, with a specific focus on the integration of AI-enabled auditing. The authors explore how blockchain technology can enhance transparency and trust in accounting practices, and how professionals can leverage blockchain data to improve decision-making. They identify four themes that have emerged from the literature, namely the event approach to accounting, real-time accounting, triple-entry accounting, and continuous auditing. The study also discusses the challenges associated with adopting blockchain. | The paper offers a comprehensive review of the literature on the integration of blockchain and AI in accounting and auditing and provides valuable insights into the potential benefits and challenges of this approach. The study is well-structured and organized, with a clear focus on the research questions and themes. The authors also provide a thorough analysis of the findings, linking them to agency theory and stakeholder theory to advance understanding in the field. The study’s limitations are not explicitly discussed, which could limit the generalizability of the findings. However, overall, this paper provides a valuable contribution to the literature on blockchain technology’s potential impact on accounting and auditing. |

| Blockchain—Internet of Things Applications: Opportunities and Challenges for Industry 4.0 and Society 5.0 [35] | A.K. Tyagi, S. Dananjayan, D. Agarwal, and H.F.T. Ahmed | 2023 | The paper discusses the potential of blockchain technology and Internet of Things (IoT) integration for Industry 4.0 and Society 5.0. It highlights the security and transparency features of blockchain technology and how it can be used to build trust in different industries such as banking, insurance, logistics, and transportation. The paper also emphasizes the real-time applications of blockchain technology and IoT integration. However, the paper also acknowledges the challenges and open issues in the integration of these technologies and suggests future research opportunities for expanding the knowledge base. | The paper provides a concise overview of the potential of blockchain technology and IoT integration in Industry 4.0 and Society 5.0. The authors have given relevant examples to support their claims and discussed the challenges and open issues that need to be addressed in the future. However, the paper could have delved deeper into the technical aspects of how blockchain and IoT integration can work together and the potential benefits and drawbacks of such integration. |

| Exploring the potential of blockchain technology within the fashion and textile supply chain with a focus on traceability, transparency, and product authenticity: A systematic review [33] | A. Badhwar, S. Islam, and C.S.L. Tan | 2023 | The paper provides a systematic review of the potential of blockchain technology in the fashion and textile industry’s supply chain for improving traceability, transparency, and product authenticity. The authors have scrutinized a significant number of research papers and non-scholarly resources to highlight the opportunities and challenges of adopting blockchain technology in this industry. The selected research papers include empirical analysis, argumentative, case studies, opinion articles, review articles, short reports, and book chapters. The study concludes that blockchain technology has immense potential to improve the fashion and textile industry’s supply chain, but challenges such as scalability, interoperability, and standardization need to be addressed to fully realize its benefits. | Overall, the paper provides a thorough and insightful review of the potential of blockchain technology in the fashion and textile industry’s supply chain. The authors have done an excellent job of synthesizing the existing research and identifying the gaps and challenges in the literature. However, the study could have been strengthened by providing more specific examples of blockchain applications in the fashion and textile industry and analyzing their effectiveness in improving traceability, transparency, and product authenticity. |

| Secured Insurance Framework Using Blockchain and Smart Contract [43] | A. Hassan, Md. I. Ali, R. Ahammed, M.M. Khan, N. Alsufyani, and A. Alsufyani, | 2021 | The paper presents a framework that uses blockchain and smart contracts to create a secured insurance process. Traditional insurance policy settlements are manual, time-consuming, and prone to errors. The authors suggest that implementing blockchain and smart contracts in the insurance process can provide security, transparency, and authenticity. The framework proposed in the paper uses smart contracts that are stored on the blockchain, and the conditions are immutable. The blockchain network uses the proof of authority (PoA) consensus algorithm to validate transactions. | The paper provides a practical and effective solution to the problems in traditional insurance policy settlement. The framework proposed by the authors can eliminate the chances of fraud claims by the insured and hidden conditions from the insurer. The use of blockchain and smart contracts can make the insurance process more efficient, transparent, and secure. The authors have provided a detailed description of the implementation of the framework, and the use of the Solidity programming language and the PoA consensus algorithm makes the framework more reliable. Overall, the paper provides valuable insight into how blockchain and smart contracts can transform the insurance industry. |

| A Traceable Online Insurance Claims System Based on Blockchain and Smart Contract Technology [42] | C.-L. Chen, Y.-Y. Deng, W.-J. Tsaur, C.-T. Li, C.-C. Lee, and C.-M. Wu | 2021 | The current medical insurance claims process is inefficient and involves a complex set of services. Patients have to apply for a diagnosis certificate and receipt from the hospital, send the relevant application documents to the insurance company, and then wait for the company to verify the information before receiving compensation. To solve this problem, the authors propose using blockchain and smart contract technology to create a traceable online insurance claims system. They argue that this technology can effectively open up information channels, promote industry integration, enhance information acquisition, improve supervision, solve risk control and anti-money laundering problems, and provide security requirements. | The paper presents an interesting application of blockchain and smart contract technology in the insurance industry, specifically in the medical insurance claims process. The authors identify some inefficiencies and complexities of the current process and argue that blockchain technology can help solve these problems. However, the paper does not provide a detailed explanation of how exactly the proposed system will work. There are also no empirical results to demonstrate the effectiveness of the proposed system. Nonetheless, the proposed system is a promising area of research and could potentially bring about significant improvements in the efficiency and security of the medical insurance claims process. |

| Blockchain for Business Applications: A Systematic Literature Review [46] | I. Konstantinidis, G. Siaminos, C. Timplalexis, P. Zervas, V. Peristeras, and S. Decker | 2018 | This paper presents a systematic literature review on the current state of blockchain technology adoption in both public and private sectors for various business applications. While the primary focus of blockchain has been on financial services, the study highlights the potentially disruptive effects of the technology in other areas. Overall, the study provides insights into the potential of blockchain technology for business applications and calls for further investigation and development in this field. | The paper provides a valuable overview of the current state of blockchain technology adoption in various business sectors. However, the study does not provide a detailed analysis of the specific business applications of blockchain or the challenges faced by organizations implementing this technology. Additionally, the paper does not offer a comprehensive analysis of the existing literature on the topic, limiting the generalizability of the findings. Nonetheless, the study provides a useful starting point for researchers and practitioners interested in exploring the potential of blockchain technology for business applications. |

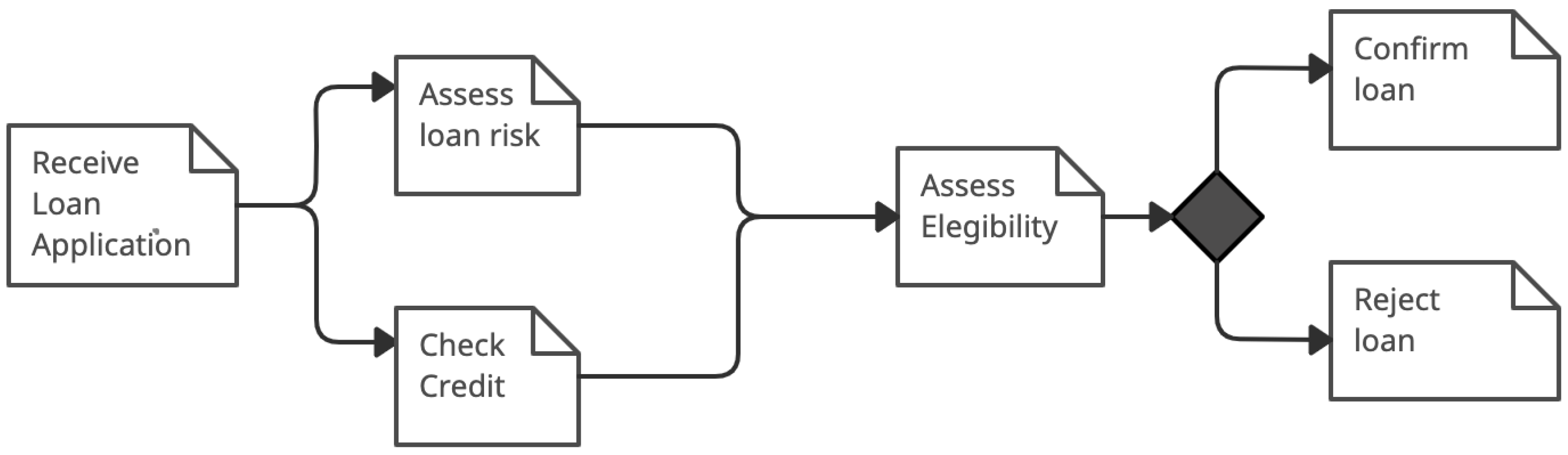

| Loan Application Pattern | |

|---|---|

| Description |

|

| Goal | To describe a sequence of tasks in a model that depicts the approval or rejection of the loan request. |

| Problem | This pattern obliges the verification and approval that ought to be done at the beginning, and during the execution of the process when different personal and confidential data is used; proper security systems ought to be applied (e.g., blockchain) subsequently. |

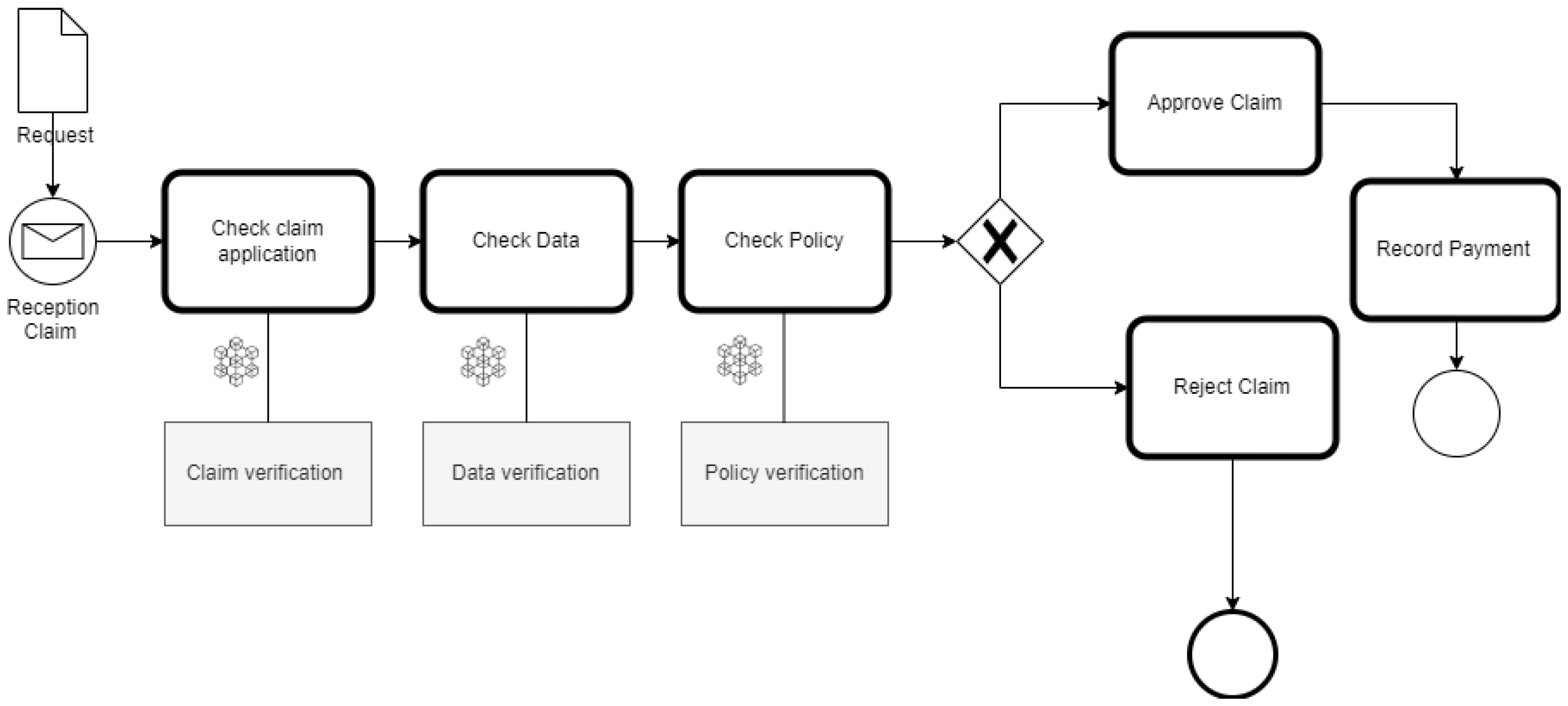

| Insurance Claim Pattern | |

|---|---|

| Description |

|

| Goal | To describe a sequence of tasks in a model that depicts the approval or rejection of the claim request. |

| Problem | This pattern obliges the verification and approval which ought to be carried out at the beginning, and during the execution of the process when different personal and confidential data is used; proper security systems ought to be applied (e.g., blockchain) subsequently. The compliance of the verification process and claim assessment should be maintained and tracked to make it transparent. The documents and the results of the procedural steps should be stored in an immutable data architecture. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Molnár, B.; Pisoni, G.; Kherbouche, M.; Zghal, Y. Blockchain-Based Business Process Management (BPM) for Finance: The Case of Credit and Claim Requests. Smart Cities 2023, 6, 1254-1278. https://doi.org/10.3390/smartcities6030061

Molnár B, Pisoni G, Kherbouche M, Zghal Y. Blockchain-Based Business Process Management (BPM) for Finance: The Case of Credit and Claim Requests. Smart Cities. 2023; 6(3):1254-1278. https://doi.org/10.3390/smartcities6030061

Chicago/Turabian StyleMolnár, Bálint, Galena Pisoni, Meriem Kherbouche, and Yossra Zghal. 2023. "Blockchain-Based Business Process Management (BPM) for Finance: The Case of Credit and Claim Requests" Smart Cities 6, no. 3: 1254-1278. https://doi.org/10.3390/smartcities6030061

APA StyleMolnár, B., Pisoni, G., Kherbouche, M., & Zghal, Y. (2023). Blockchain-Based Business Process Management (BPM) for Finance: The Case of Credit and Claim Requests. Smart Cities, 6(3), 1254-1278. https://doi.org/10.3390/smartcities6030061