Testing for Causality-In-Mean and Variance between the UK Housing and Stock Markets

Abstract

:

1. Introduction

2. Empirical Techniques

3. Data, Descriptive Statistics, and Results of an Augmented Dickey–Fuller Test

4. Estimation of an AR-EGARCH Model

5. Testing for Causality-In-Variance

6. Conclusions

Acknowledgments

Conflicts of Interest

References

- Alaganar, V. T., and Ramaprasad Bhar. 2003. An International Study of Causality-in-Variance: Interest Rate and Financial Sector Returns. Journal of Economics and Finance 27: 39–55. [Google Scholar] [CrossRef]

- Bhar, Ramaprasad, and Shigeyuki Hamori. 2005. Causality in Variance and the Type of Traders in Crude Oil Futures. Energy Economics 27: 527–39. [Google Scholar] [CrossRef]

- Bhar, Ramaprasad, and Shigeyuki Hamori. 2008. Information Content of Commodity Futures Prices for Monetary Policy. Economic Modelling 25: 274–83. [Google Scholar] [CrossRef]

- Bollerslev, Tim, and Jeffrey. M. Wooldridge. 1992. Quasi-Maximum Likelihood Estimation and Inference in Dynamic Models with Time Varying Covariances. Econometric Reviews 11: 143–72. [Google Scholar] [CrossRef]

- Chang, Chia-Lin, and Michael McAleer. 2017a. A simple test for causality in volatility. Econometrics 5: 15. [Google Scholar] [CrossRef]

- Chang, Chia-Lin, and Michael McAleer. 2017b. The correct regularity condition and interpretation of asymmetry in EGARCH. Economics Letters 161: 52–55. [Google Scholar] [CrossRef]

- Cheung, Yin-Wong, and Lilian K. Ng. 1996. A Causality-in-Variance Test and Its Applications to Financial Market Prices. Journal of Econometrics 72: 33–48. [Google Scholar] [CrossRef]

- Gyourko, Joseph, and Donald B. Keim. 1992. What Does the Stock Market Tell Us about Real Estate Returns? Journal of the American Real Estate Finance and Urban Economics Association 20: 457–86. [Google Scholar] [CrossRef]

- Hafner, Christian M., and Helmut Herwartz. 2008. Testing for Causality in Variance Using Multivariate GARCH Models. Annals of Economics and Statistics 89: 215–41. [Google Scholar] [CrossRef]

- Hamori, Shigeyuki. 2003. An Empirical Investigation of Stock Markets: The CCF Approach. Dordrecht: Kluwer Academic Publishers. [Google Scholar]

- Hong, Yongmiao. 2001. A Test for Volatility Spillover with Application to Exchange Rates. Journal of Econometrics 103: 183–224. [Google Scholar] [CrossRef]

- Hoshikawa, Takeshi. 2008. The Causal Relationships between Foreign Exchange Intervention and Exchange Rate. Applied Economics Letters 15: 519–22. [Google Scholar] [CrossRef]

- Ibbotson, Roger G., and Laurence B. Siegel. 1984. Real Estate Returns: A Comparison with Other Investments. Real Estate Economics 12: 219–42. [Google Scholar] [CrossRef]

- Ibrahim, Mansor H. 2010. House Price-Stock Price Relations in Thailand: An Empirical Analysis. International Journal of Housing Markets and Analysis 3: 69–82. [Google Scholar] [CrossRef]

- Jarque, Carlos M., and Anil K. Bera. 1987. Test for Normality of Observations and Regression Residuals. International Statistical Review 55: 163–72. [Google Scholar] [CrossRef]

- Kapopoulos, Panayotis, and Fotios Siokis. 2005. Stock and Real Estate Prices in Greece: Wealth versus Credit-Price Effect. Applied Economics Letters 12: 125–28. [Google Scholar] [CrossRef]

- Lin, Pin-te, and Franz Fuerst. 2014. The Integration of Direct Real Estate and Stock Markets in Asia. Applied Economics 46: 1323–34. [Google Scholar] [CrossRef]

- Liow, Kim Hiang, and Haishan Yang. 2005. Long-Term Co-Memories and Short-Run Adjustment: Securitized Real Estate and Stock Markets. The Journal of Real Estate Finance and Economics 31: 283–300. [Google Scholar] [CrossRef]

- Liow, Kim Hiang. 2006. Dynamic Relationship between Stock and Property Markets. Applied Financial Economics 16: 371–76. [Google Scholar] [CrossRef]

- Liow, Kim Hiang. 2012. Co-Movements and Correlations Across Asian Securitized Real Estate and Stock Markets. Real Estate Economics 40: 97–129. [Google Scholar] [CrossRef]

- Ljung, Greta M., and George E. P. Box. 1978. On a Measure of Lack of Fit in Time Series Models. Biometrika 66: 265–70. [Google Scholar] [CrossRef]

- Louis, Henock, and Amy X. Sun. 2013. Long-Term Growth in Housing Prices and Stock Returns. Real Estate Economics 41: 663–708. [Google Scholar] [CrossRef]

- McAleer, Michael, and Christian M. Hafner. 2014. A one line derivation of EGARCH. Econometrics 2: 92–97. [Google Scholar] [CrossRef] [Green Version]

- Miyazaki, Takashi, and Shigeyuki Hamori. 2013. Testing for causality between the gold return and stock market performance: Evidence for gold investment in case of emergency. Applied Financial Economics 23: 27–40. [Google Scholar] [CrossRef]

- Nakajima, Tadahiro, and Shigeyuki Hamori. 2012. Causality-in-Mean and Causality-in-Variance among Electricity Prices, Crude Oil Prices, and Yen-US Dollar Exchange Rates in Japan. Research in International Business and Finance 26: 371–86. [Google Scholar] [CrossRef]

- Nelson, Daniel B. 1991. Conditional Heteroskedasticity in Asset Returns: A New Approach. Econometrica 59: 347–70. [Google Scholar] [CrossRef]

- Okunev, John, and Patrick J. Wilson. 1997. Using Nonlinear Tests to Examine Integration between Real Estate and Stock Markets. Real Estate Economics 25: 487–503. [Google Scholar] [CrossRef]

- Okunev, John, Patrick Wilson, and Ralf Zurbruegg. 2000. The Causal Relationship between Real Estate and Stock Markets. Journal of Real Estate Finance and Economics 21: 251–61. [Google Scholar] [CrossRef]

- Quan, Daniel C., and Sheridan Titman. 1999. Do Real Estate Prices and Stock Prices Move Together? An International Analysis. Real Estate Economics 27: 183–207. [Google Scholar] [CrossRef]

- Ross, Stephen A. 1989. Information and Volatility: No-Arbitrage Martingale Approach to Timing and Resolution Irrelevancy. Journal of Finance 44: 1–17. [Google Scholar] [CrossRef]

- Su, Chi-Wei. 2011. Non-Linear Causality between the Stock and Real Estate Markets of Western European Countries: Evidence from Rank Tests. Economic Modelling 28: 845–51. [Google Scholar] [CrossRef]

- Schwarz, Gideon. 1978. Estimating the Dimension of a Model. Annals of Statistics 6: 461–64. [Google Scholar] [CrossRef]

- Tsai, I-Chun, Cheng-Feng Lee, and Ming-Chu Chiang. 2012. The Asymmetric Wealth Effect in the U.S. Housing and Stock Markets: Evidence from the Threshold Cointegration Model. Journal of Real Estate Finance and Economics 45: 1005–20. [Google Scholar] [CrossRef]

- Tamakoshi, Go, and Shigeyuki Hamori. 2014. Causality-in-variance and causality-in-mean between the Greek sovereignbond yields and Southern European banking sector equity returns. Journal of Economics and Finance 38: 627–42. [Google Scholar] [CrossRef]

- Toyoshima, Yuki, and Shigeyuki Hamori. 2012. Volatility Transmission of Swap Spreads among the United States, Japan, and the United Kingdom: A Cross-Correlation Function Approach. Applied Financial Economics 22: 849–62. [Google Scholar] [CrossRef]

| 1 | Some examples include studies by Hamori (2003), Alaganar and Bhar (2003), Bhar and Hamori (2005, 2008), Hoshikawa (2008), Nakajima and Hamori (2012), Miyazaki and Hamori (2013), Tamakoshi and Hamori (2014), and Toyoshima and Hamori (2012). |

| 2 | See Hafner and Herwartz (2008) and Chang and McAleer (2017a) for the causality-in-variance analysis using multivariate GARCH models. |

| 3 | |

| 4 | |

| 5 | |

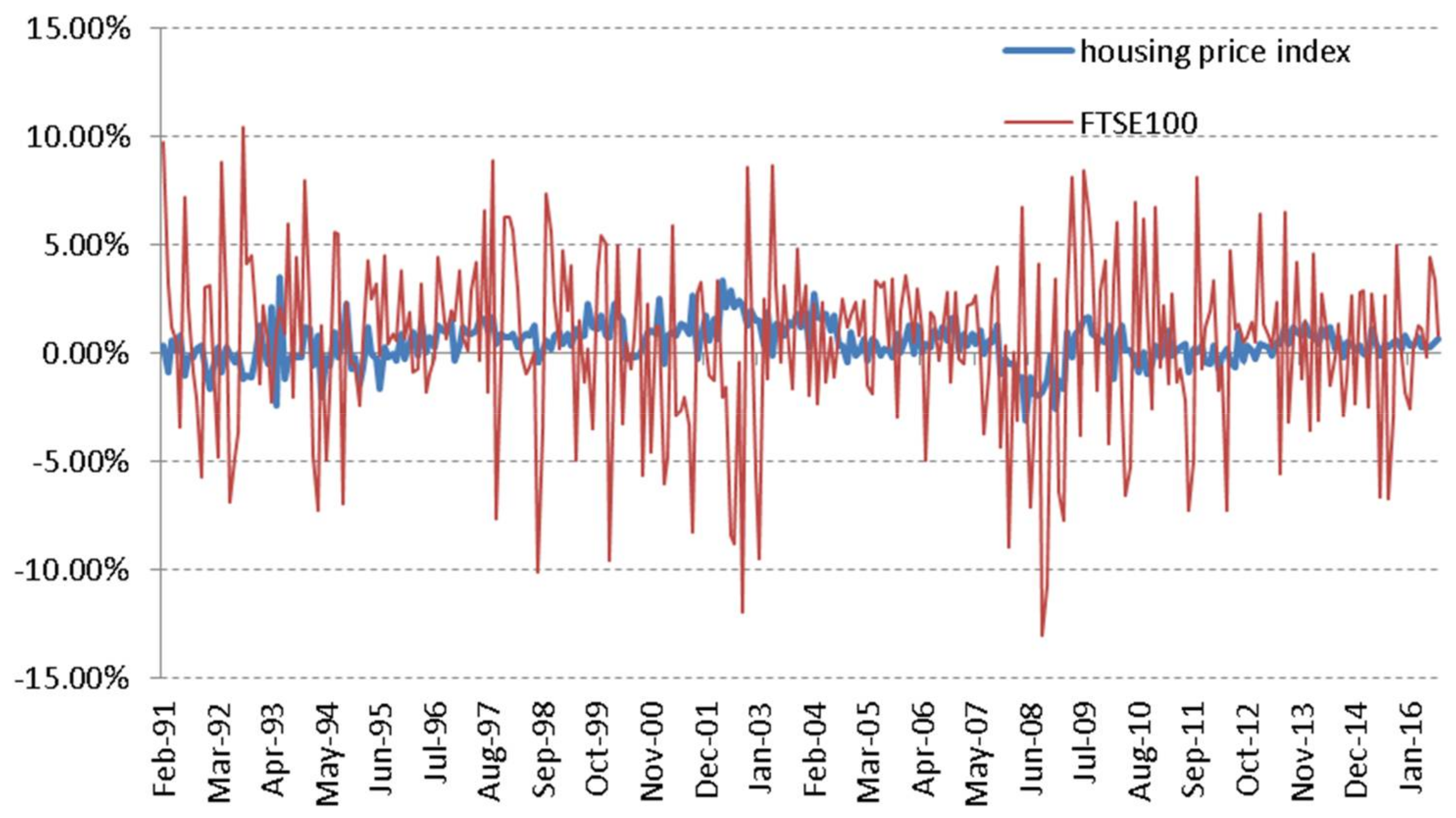

| 6 | We obtained the data from the URL below: http://www.nationwide.co.U.K./about/house-price-index/download-data#tab:Downloaddata. |

| 7 | See Jarque and Bera (1987). |

| 8 | The EGARCH model suffers from a number of fundamental problems, including the lack of regularity conditions and hence the absence of any asymptotic properties. See McAleer and Hafner (2014) and Chang and McAleer (2017b) for details. |

| 9 | |

| 10 | We selected the final models from EGARCH(1,1), EGARCH(1,2), EGARCH(2,1), and EGARCH(2,2). |

| 11 | See Ljung and Box (1978). |

{kind=link}

{kind=link}

{kind=link}

| Authors | Empirical Technique | Country | Principal Results |

|---|---|---|---|

| Gyourko and Keim (1992) | Market regression model | the US | Lagged equity REIT and stock return are predictors of property index. |

| Ibbotson and Siegel (1984) | Correlation, Regression | the US | Low correlation between the real estate and stocks, bonds is found. |

| Ibrahim (2010) | VAR model, Granger causality tests | Thailand | Unidirectional causality from stock prices to house prices is found. |

| Kapopoulos and Siokis (2005) | VAR model, Granger causality tests | Greece | Unidirectional causality from stock prices to house prices is found. |

| Lin and Fuerst (2014) | Johansen, Gregory-Hansen ,Nonlinear cointegration tests | 9 Asian countries | Market segmentation is observed in China, Japan, Thailand, Malaysia, Indonesia and South Korea. |

| Liow (2006) | ARDL cointegration tests | Singapore | Contemporaneous long-term relationship between thestock market, residential and office property prices is found. |

| Liow (2012) | Asymmetric DCC model | 8 Asian countries | Conditional real estate-stock correlations are time varying and asymmetric in some cases. |

| Liow and Yang (2005) | FIVEC model, VEC model | 4 Asian countries | FIVECM improves the forecasting performance over conventional VECM models. |

| Louis and Sun (2013) | Fama–MacBeth procedure | the US | Firms’ long-term abnormal stock returns are negatively related to past growth in housing prices. |

| Okunev and Wilson (1997) | Cointegration tests | the US | Weak and nonlinear relationship between the stock and real estate markets is found. |

| Okunev et al. (2000) | Linear and nonlinear causality tests | the US | Strong uni-directional relationship from the stock market to the real estate market is found in nonlinear causality test. |

| Quan and Titman (1999) | Cross-sectional regression | 17 countries | Positive relation between real estate values and stock returns is found. |

| Su (2011) | TEC model, Non-parametric rank test | 8 Western European countries | Unidirectional causality from the real estate markets to the stock market is found in the Germany, Netherlands and the UK. |

| Tsai et al. (2012) | M-TAR cointegration model | the US | Threshold cointegration relationship between the housing market and the stock market is found. |

| Statistics | Housing | Stock |

|---|---|---|

| Sample Size | 307 | 307 |

| Mean | 0.4421% | 0.4527% |

| Std. Dev. | 0.9544% | 4.0076% |

| Skewness | −0.2221 | −0.4557 |

| Kurtosis | 1.1434 | 0.5011 |

| Maximum | 3.4912% | 10.3952% |

| Minimum | −3.1084% | −13.0247% |

| Jarque-Bera | 19.2472 | 13.8362 |

| Probability | 0.0066% | 0.0990% |

| Variable | Auxuliary Model | |||

|---|---|---|---|---|

| Const | Const & Trend | None | ||

| housing | Level | −0.2988 | −2.3811 | 1.5701 |

| First difference | −4.5065 *** | −4.5019 *** | −3.8047 *** | |

| stock | Level | −1.8598 | −2.2418 | 0.7945 |

| First difference | −17.3975 *** | −17.4146 *** | −17.2370 *** | |

| Parameters | Housing | Stock | ||

|---|---|---|---|---|

| AR(3)-EGARCH(1,1) | AR(1)-EGARCH(1,1) | |||

| Estimate | SE | Estimate | SE | |

| a0 | 0.0021 *** | (0.0007) | 0.0088 *** | (0.0024) |

| a1 | 0.0321 | (0.061) | −0.0791 | (0.0602) |

| a2 | 0.4095 *** | (0.0518) | ||

| a3 | 0.2522 *** | (0.0582) | ||

| b0 | −0.0011 | (0.0007) | −0.007 * | (0.0037) |

| ω | −0.4465 * | (0.2485) | −1.3275 *** | (0.4386) |

| α1 | 0.2362 *** | (0.0818) | 0.3162 *** | (0.1148) |

| γ1 | −0.0074 | (0.0476) | −0.1191 * | (0.0614) |

| β1 | 0.9741 *** | (0.0224) | 0.8365 *** | (0.058) |

| Log Likelihood | 1074.4320 | 571.2161 | ||

| SBIC | −6.8994 | −3.6025 | ||

| Q(24) | 35.4320 | 11.6550 | ||

| P-value | 0.0620 | 0.9840 | ||

| Q2(24) | 0.0000 | 19.3240 | ||

| P-value | 0.0000 | 0.7350 | ||

| Lag k | Housing and Stock (−k) | Housing and Stock (+k) | ||

|---|---|---|---|---|

| Mean | Variance | Mean | Variance | |

| 1 | −0.0271 | 0.0067 | 0.0011 | 0.0320 |

| 2 | −0.0262 | 0.0549 | 0.0651 | −0.0196 |

| 3 | −0.0675 | 0.0259 | 0.0363 | −0.0358 |

| 4 | 0.0037 | 0.0589 | 0.0709 | 0.0920 * |

| 5 | −0.0390 | 0.1460 *** | 0.0322 | −0.0423 |

| 6 | 0.1366 *** | −0.0407 | −0.0797 | 0.0530 |

| 7 | 0.0016 | 0.0007 | −0.0380 | 0.0256 |

| 8 | −0.0386 | 0.0050 | 0.0105 | −0.0298 |

| 9 | 0.0410 | 0.1444 *** | −0.0114 | −0.0154 |

| 10 | 0.0375 | 0.0101 | 0.0179 | 0.0630 |

| 11 | 0.0269 | 0.0238 | −0.0132 | 0.0012 |

| 12 | −0.0728 | 0.0150 | −0.0204 | 0.1879 *** |

| 13 | −0.0695 | −0.0248 | −0.0084 | 0.0257 |

| 14 | −0.0648 | 0.0234 | −0.1309 | 0.0503 |

| 15 | −0.0835 | 0.0087 | −0.0859 | −0.0555 |

| 16 | −0.0120 | −0.0113 | −0.0087 | −0.1055 |

| 17 | 0.0301 | 0.0263 | −0.0620 | −0.0064 |

| 18 | −0.0497 | 0.0383 | −0.0341 | 0.0603 |

| 19 | −0.0406 | 0.0092 | −0.0573 | 0.0592 |

| 20 | −0.0200 | 0.0175 | 0.0051 | 0.0288 |

| 21 | −0.0161 | −0.0574 | 0.0944 ** | 0.0129 |

| 22 | −0.0141 | −0.0669 | −0.0235 | 0.0560 |

| 23 | −0.0868 | −0.0501 | 0.0720 | 0.0092 |

| 24 | −0.1098 | −0.0152 | −0.0469 | −0.0259 |

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Toyoshima, Y. Testing for Causality-In-Mean and Variance between the UK Housing and Stock Markets. J. Risk Financial Manag. 2018, 11, 21. https://doi.org/10.3390/jrfm11020021

Toyoshima Y. Testing for Causality-In-Mean and Variance between the UK Housing and Stock Markets. Journal of Risk and Financial Management. 2018; 11(2):21. https://doi.org/10.3390/jrfm11020021

Chicago/Turabian StyleToyoshima, Yuki. 2018. "Testing for Causality-In-Mean and Variance between the UK Housing and Stock Markets" Journal of Risk and Financial Management 11, no. 2: 21. https://doi.org/10.3390/jrfm11020021

APA StyleToyoshima, Y. (2018). Testing for Causality-In-Mean and Variance between the UK Housing and Stock Markets. Journal of Risk and Financial Management, 11(2), 21. https://doi.org/10.3390/jrfm11020021