The Effects of the COVID-19 Crisis on Risk Factors and Option-Implied Expected Market Risk Premia: An International Perspective

Abstract

:1. Introduction

2. Data

3. The COVID-19 Crisis versus the Pre-COVID Period: Factor Returns

3.1. Mean Returns, Volatilities, and Sharpe Ratios

3.2. Risk-Adjusted Returns

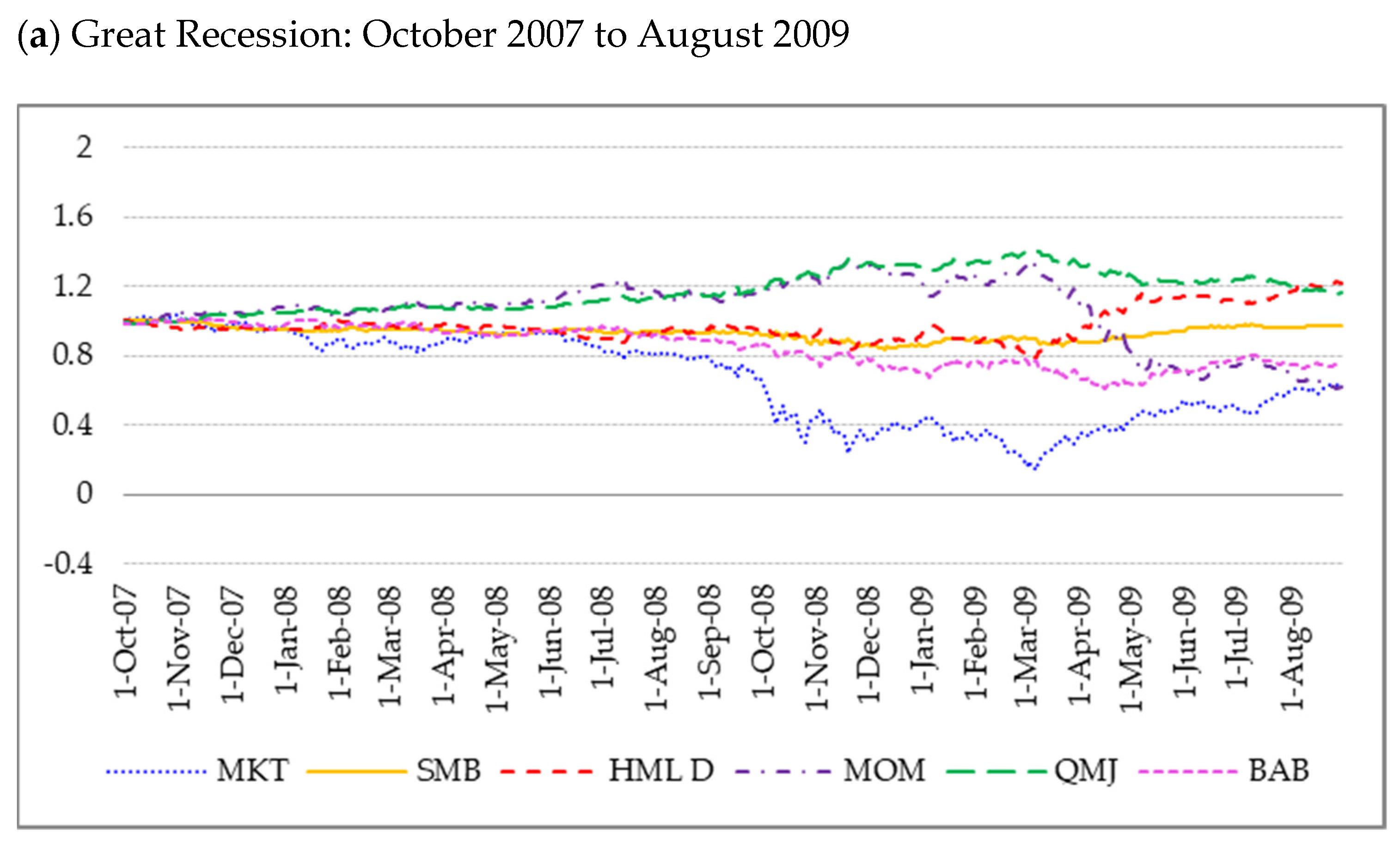

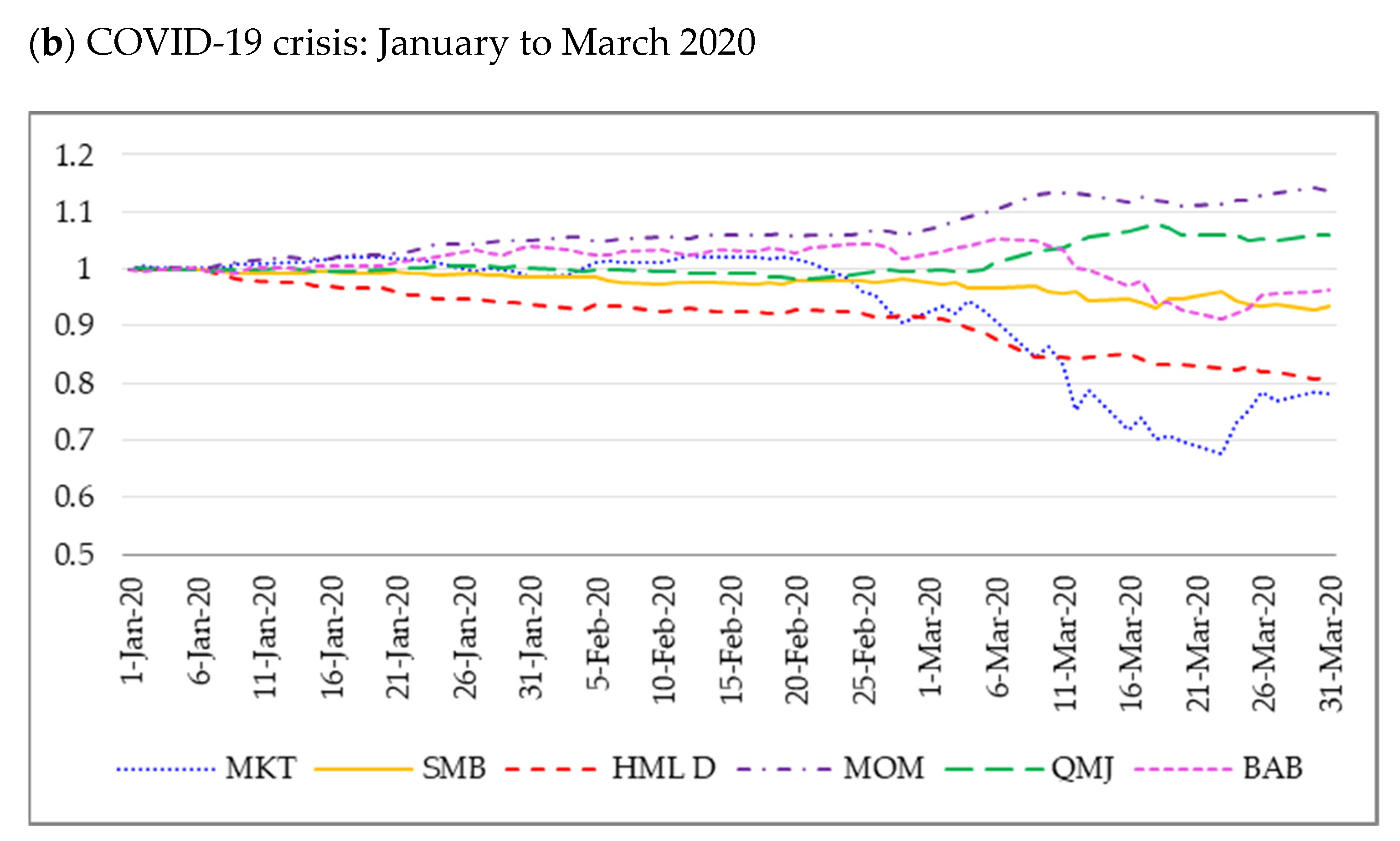

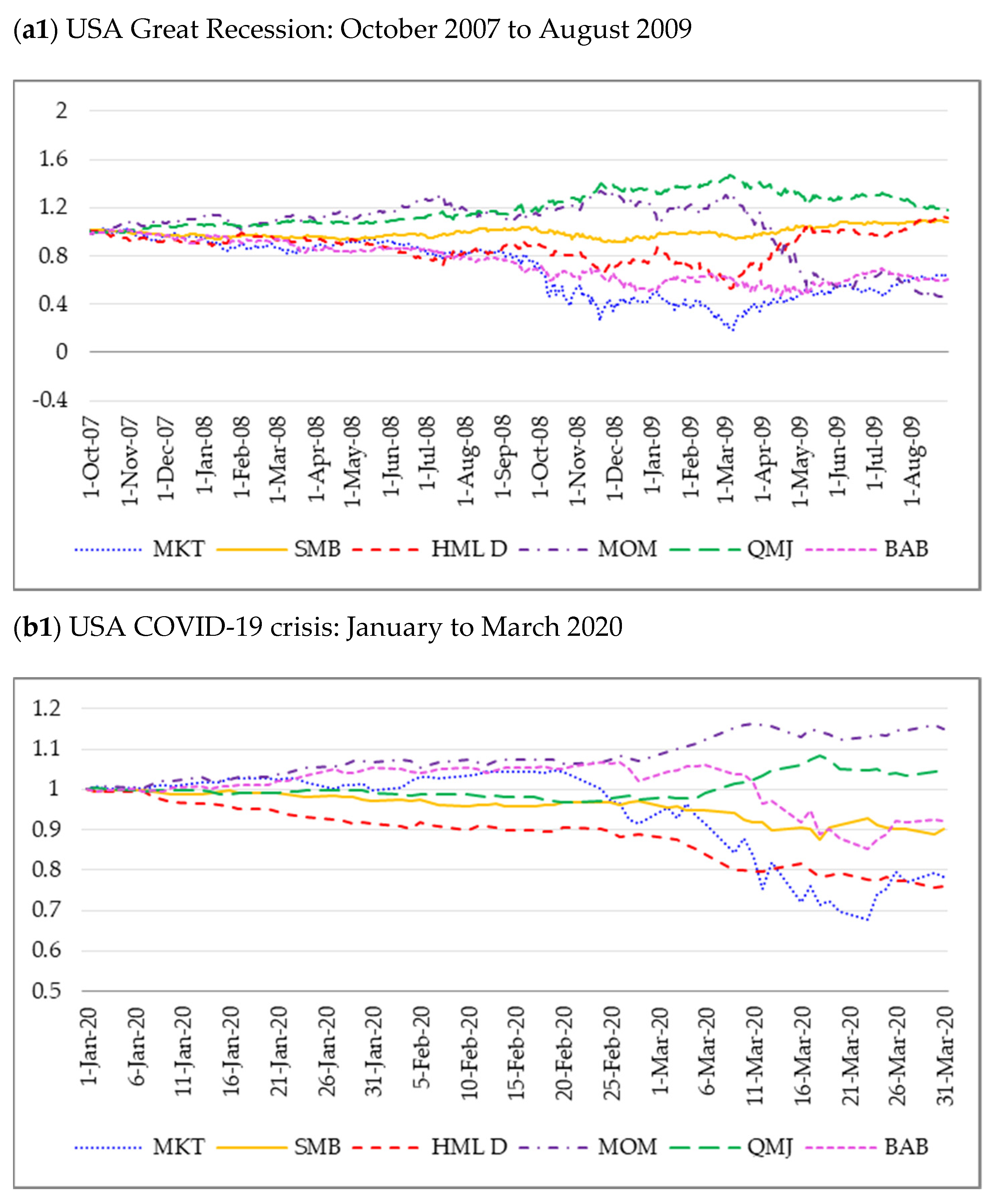

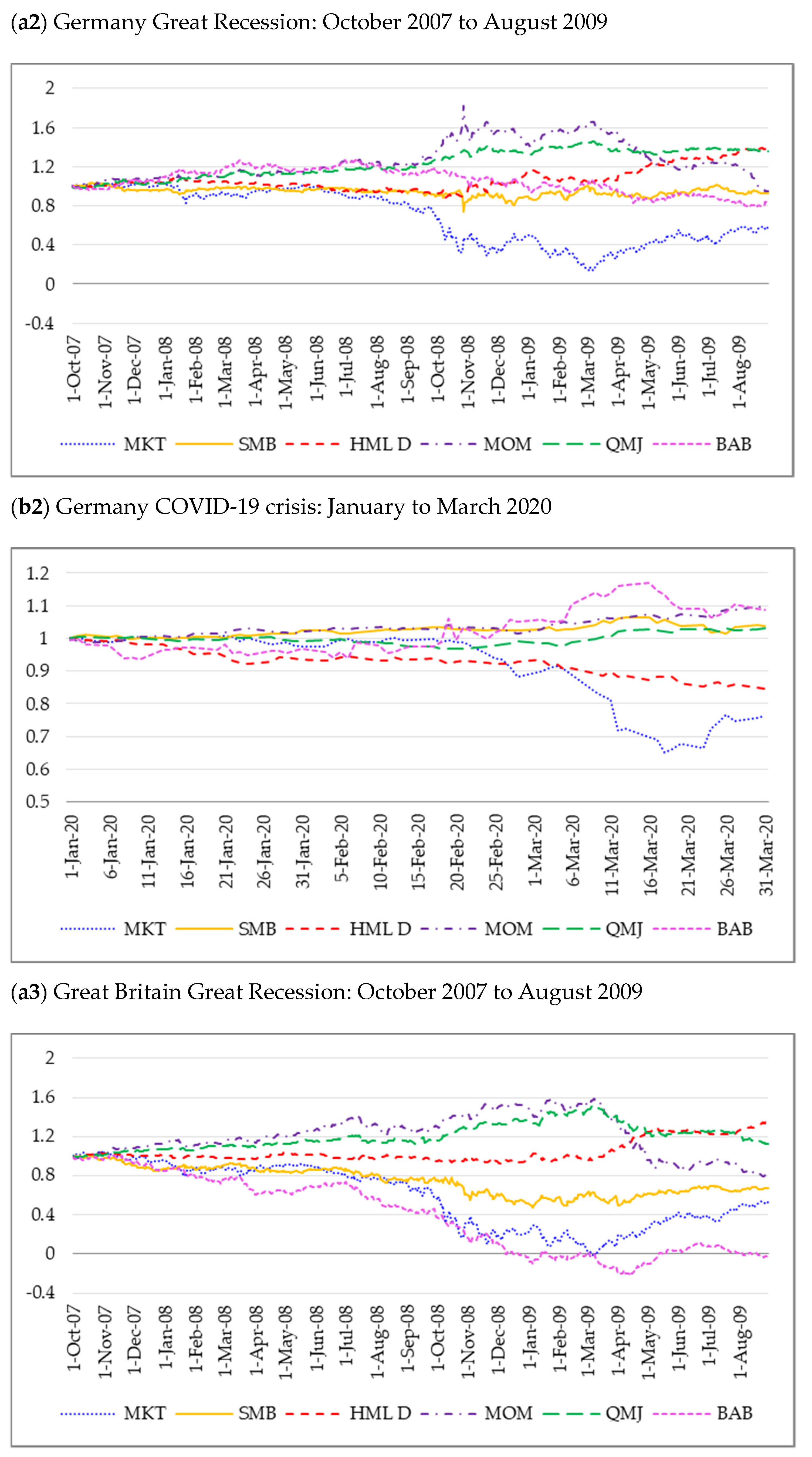

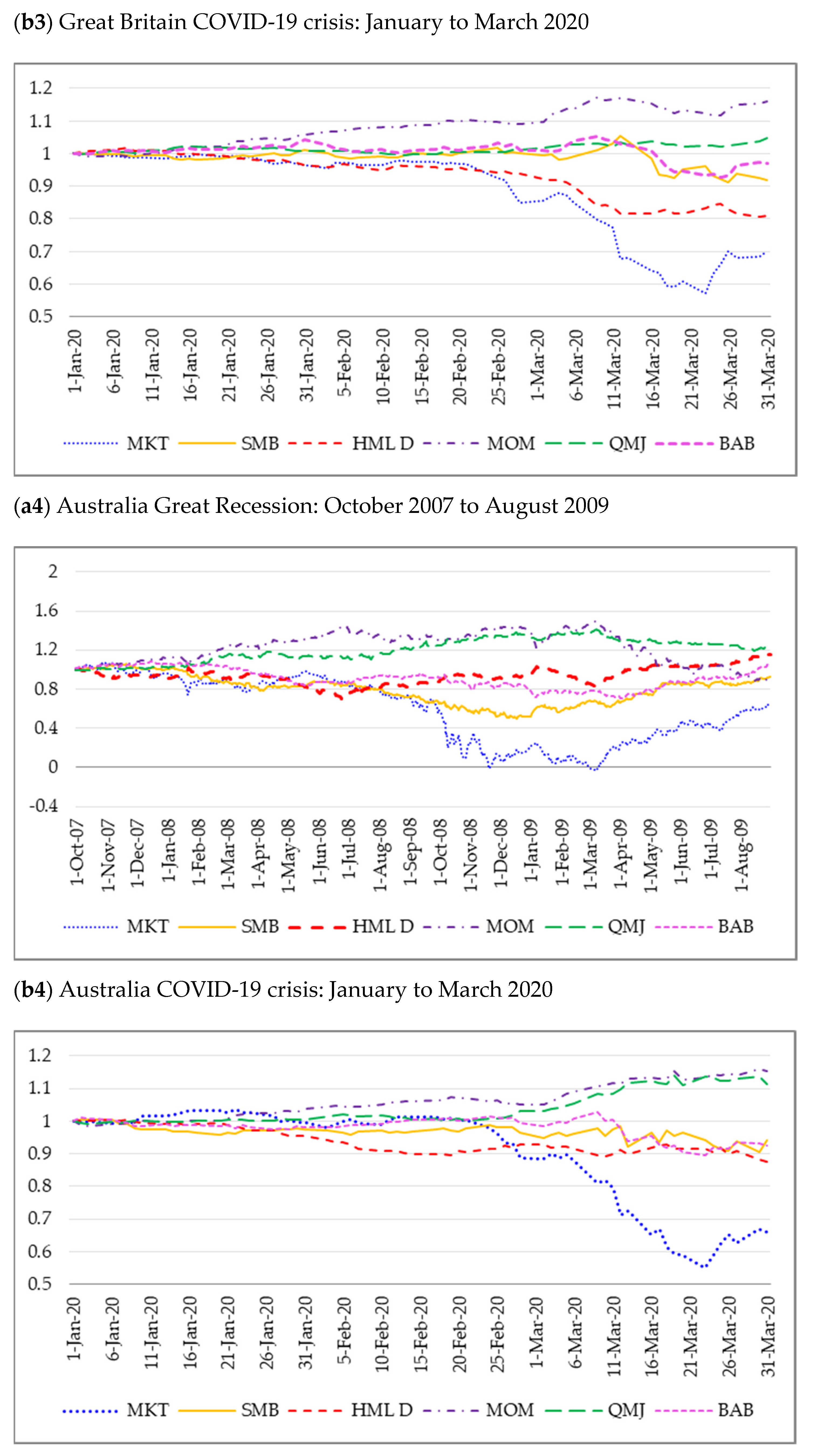

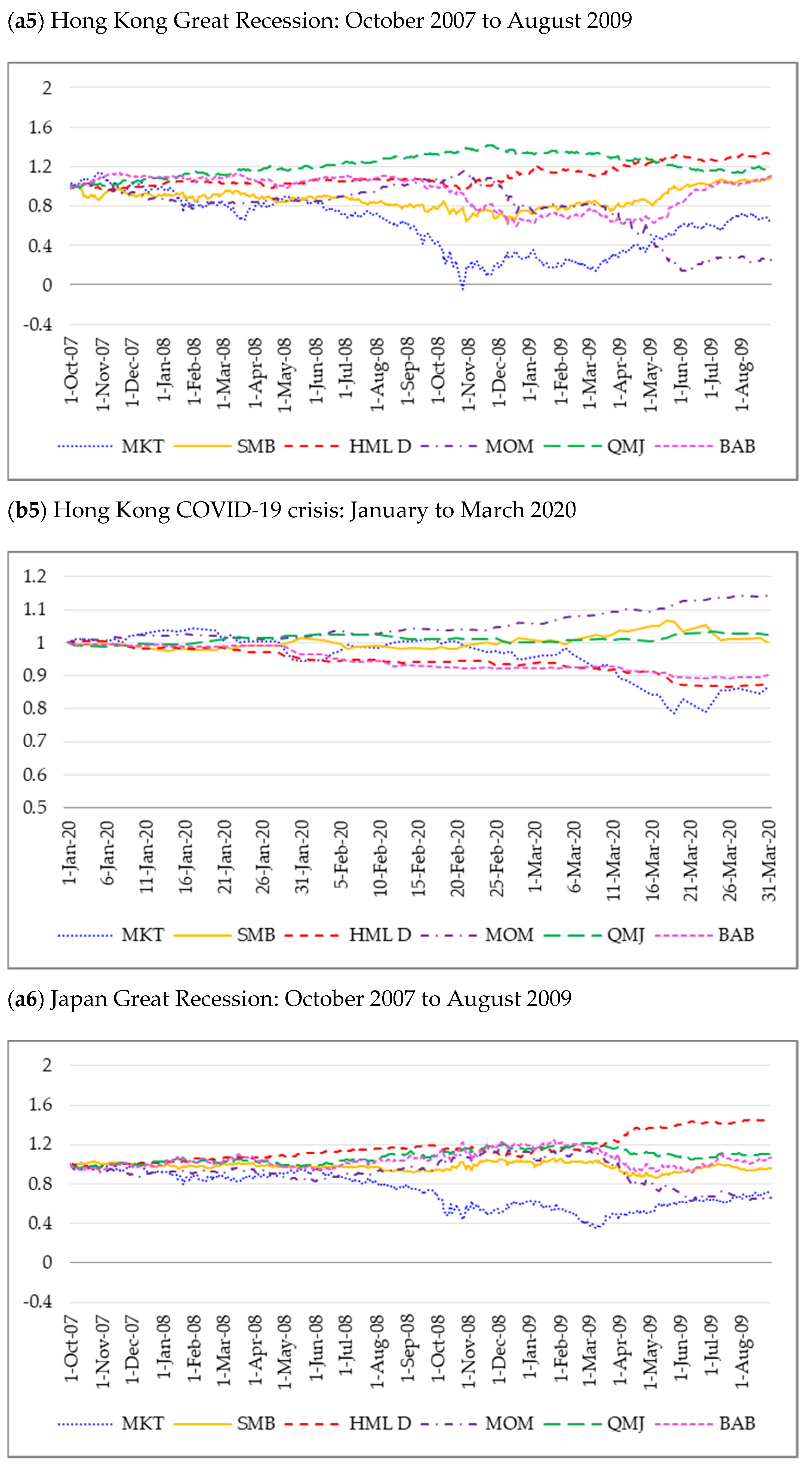

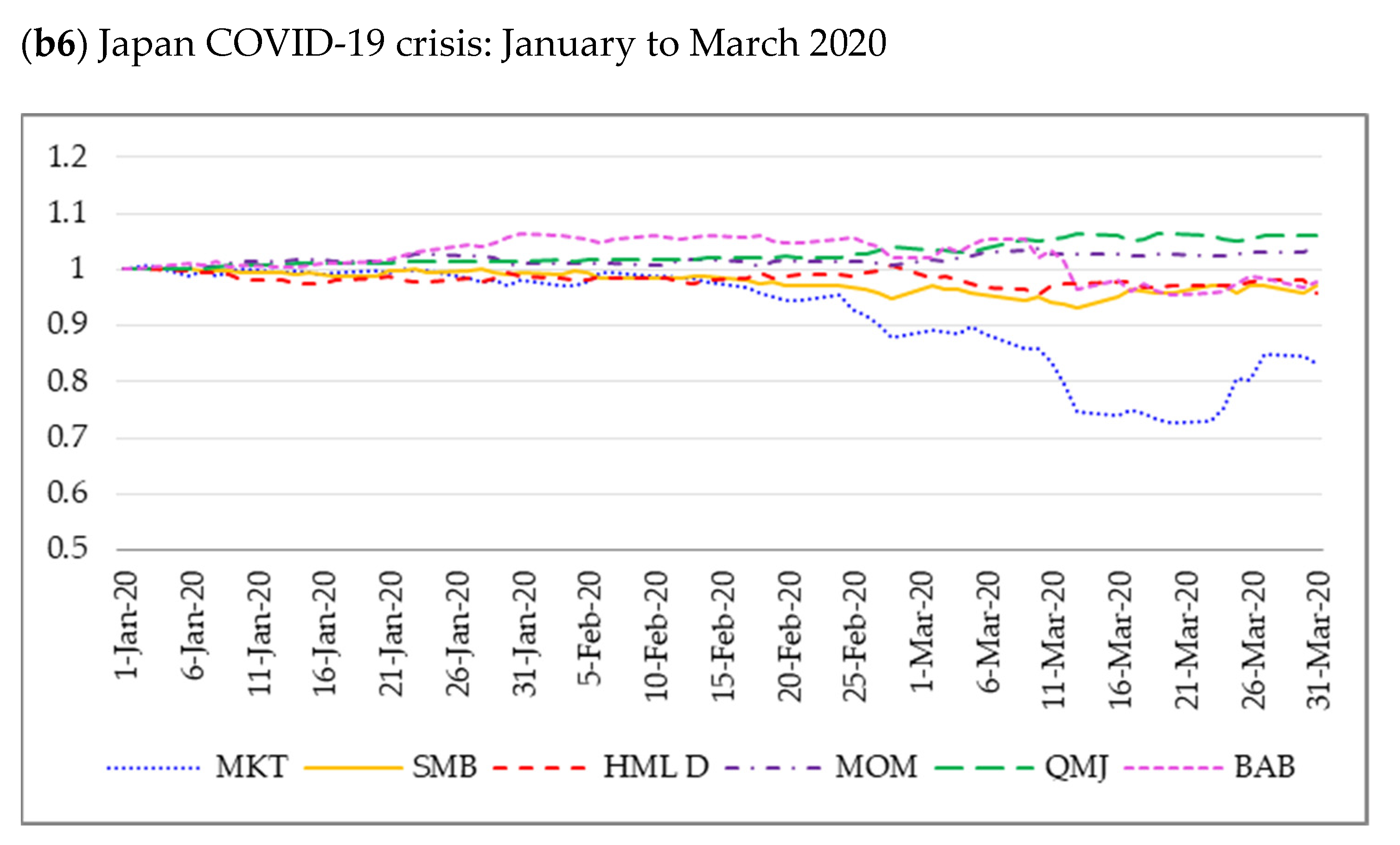

4. The Great Recession and the COVID-19 Crises: Cumulative Factor Returns and Expected Risk Premia

4.1. Cumulative Factor Returns

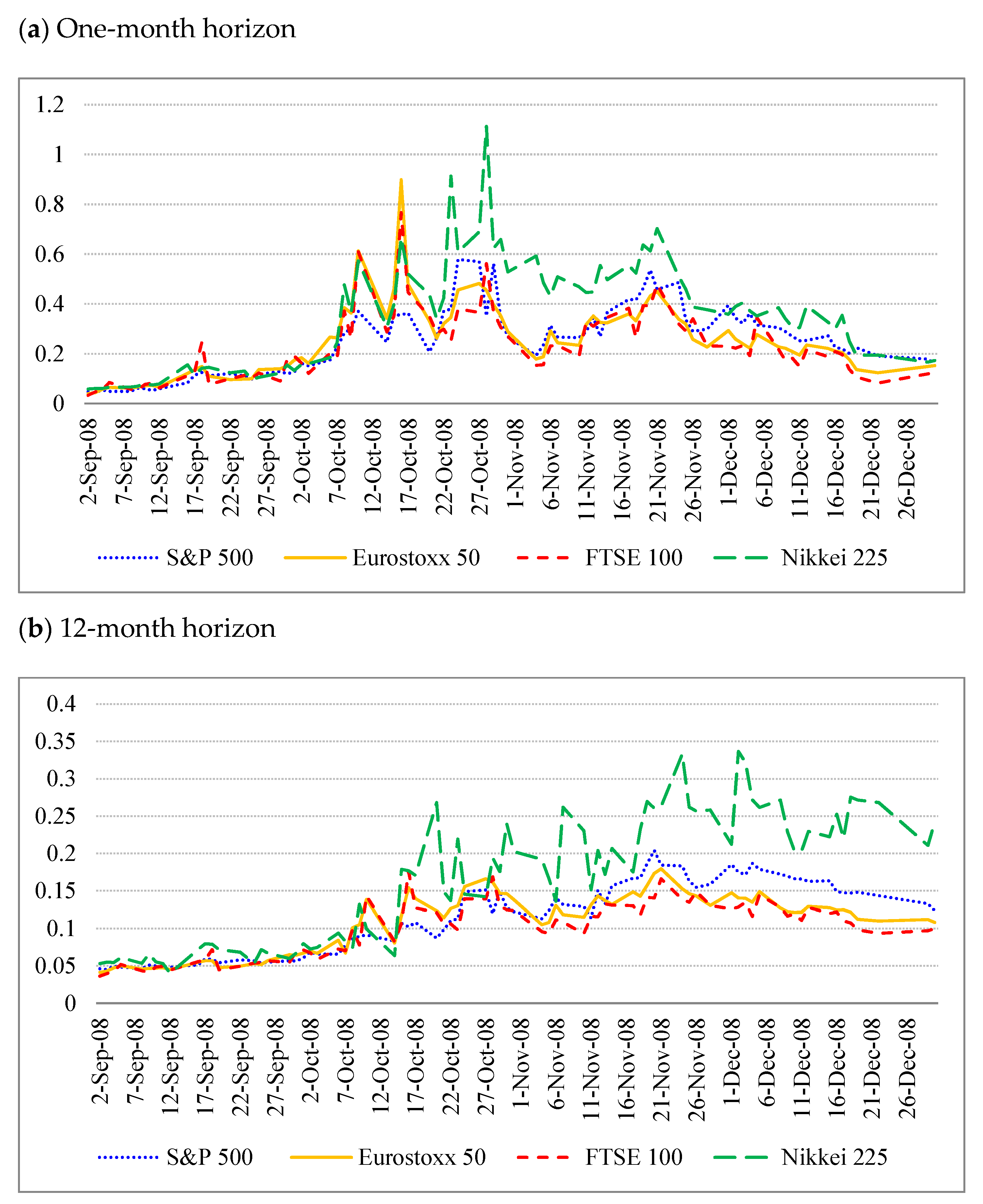

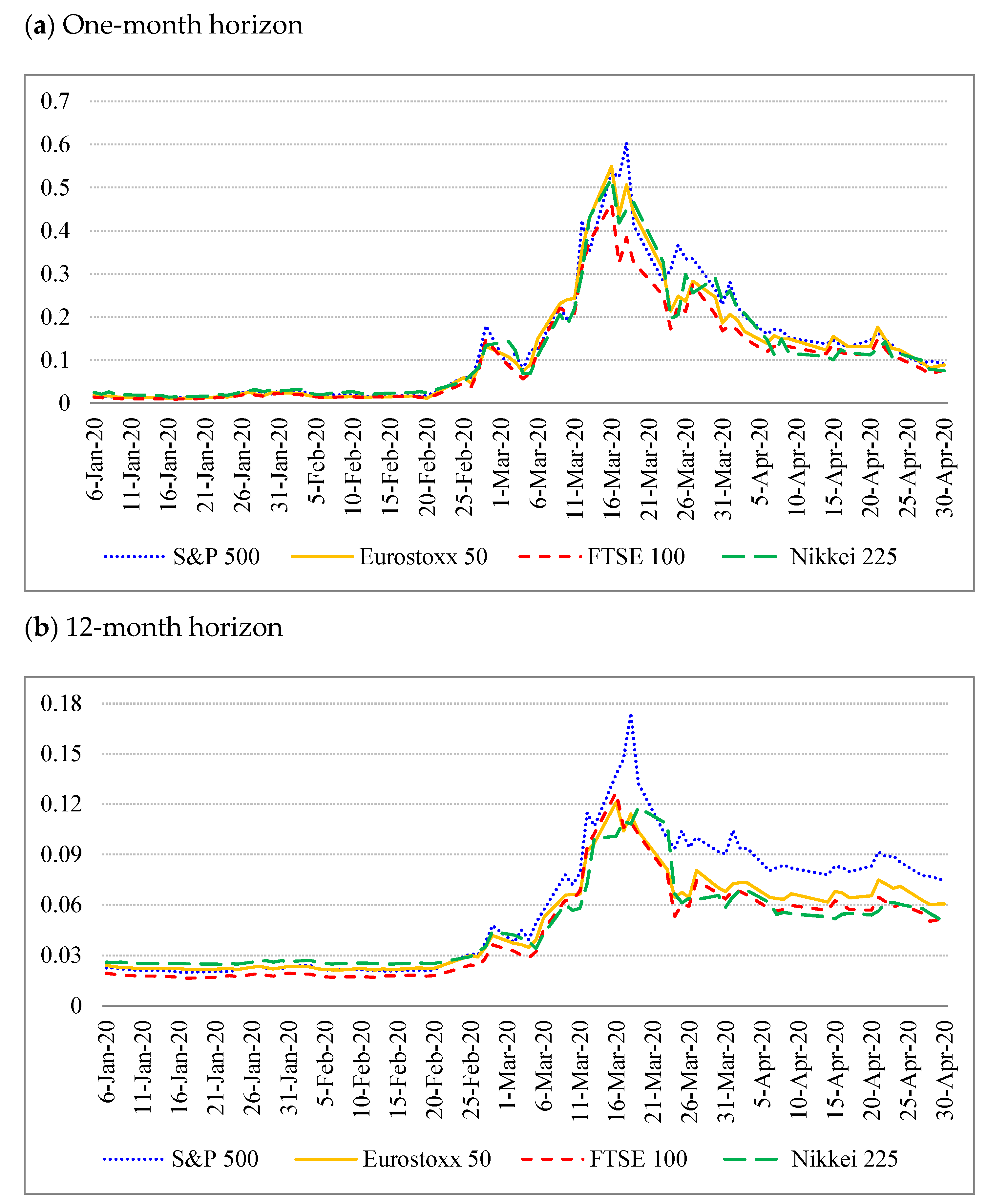

4.2. Expected Market Risk Premia

4.2.1. The Estimation Procedure of Expected Market Risk Premia

4.2.2. The Time-Varying Behavior of the Expected Market Risk Premia

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | Regarding the size effect, see also Alquist et al. (2018). |

| 2 | See Asness et al. (2020); Chen and Lu (2019) for additional detailed discussion on the BAB factor and funding liquidity. See Schneider et al. (2020), for a skewness-based explanation of the BAB factor. |

| 3 | See Bouchard et al. (2016); González-Urteaga and Rubio (2021) for additional complementary evidence on the QMJ factor. |

| 4 | The drop of the Italian GDP during the first quarter of 2020 relative to the previous quarter was 4.8%, while other large European countries like Spain or France experienced higher drops of 5.2% and 5.8%, respectively. It may be explained by the heterogenous effects of the COVID-19 on the different sectors of the economies. |

| 5 | With the unique exception of France in the case of the Fama–French risk-adjusted return. |

| 6 | Results regarding the other countries are available upon request. |

| 7 | This evidence is consistent with the results provided by Ramelli and Wagner (2020), who show that, initially, only firms especially exposed to China underperformed. |

| 8 | See Van Binsbergen and Koijen (2017); Bansal et al. (2019); Chabi-Yo and Loudis (2020); Bakshi et al. (2020); Gormsen (2021), for recent evidence on the term structure of the expected market risk premium under alternative procedures and data on either dividend futures or option prices. |

| 9 | Rubio et al. (2021), who use the same indexes employed in this paper, find that on average the term structure of expected market risk premia is slightly downward sloping, but, more importantly, it becomes highly downward sloping in bad economic times. |

References

- Alquist, Ron, Ronen Israel, and Tobias J. Moskowitz. 2018. Fact, Fiction, and the Size Effect. The Journal of Portfolio Management 45: 3–30. [Google Scholar] [CrossRef]

- Ampudia, Miguel, Ursel Baumann, and Fabio Fornari. 2020. Coronavirus (COVID-19): Market Fear as Implied by Options Prices. ECB Economic Bulletin 4: 1–9. Available online: https://www.ecb.europa.eu/pub/economic-bulletin/focus/2020/html/ecb.ebbox202004_02~26672a3808.en.html (accessed on 15 July 2021).

- Asness, Cliffor S., Andrea Frazzini, Ronen Israel, and Tobias J. Moskowitz. 2015a. Fact, Fiction, and Momentum Investing. The Journal of Portfolio Management 40: 75–92. [Google Scholar] [CrossRef]

- Asness, Clifford S., Andrea Frazzini, Ronen Israel, and Tobias J. Moskowitz. 2015b. Fact, Fiction, and Value Investing. The Journal of Portfolio Management 42: 34–52. [Google Scholar] [CrossRef]

- Asness, Clifford S., and Andrea Frazzini. 2013. The Devil in HML’s Details. The Journal of Portfolio Management 39: 49–68. [Google Scholar] [CrossRef]

- Asness, Clifford S., Andrea Frazzini, and Lasse H. Pedersen. 2019. Quality Minus Junk. Review of Accounting Studies 24: 34–112. [Google Scholar] [CrossRef] [Green Version]

- Asness, Clifford S., Andrea Frazzini, Niels J. Gormsen, and Lasse H. Pedersen. 2020. Betting against Correlation: Testing Theories of the Low-Risk Effect. Journal of Financial Economics 135: 629–52. [Google Scholar] [CrossRef]

- Asness, Clifford S., Andrea Frazzini, Ronen Israel, Tobias J. Moskowitz, and Lasse H. Pedersen. 2018. Size Matters if you Control your Junk. Journal of Financial Economics 129: 479–509. [Google Scholar] [CrossRef]

- Asness, Clifford S., Antti Ilmanen, Ronen Israel, and Tobias J. Moskowitz. 2015c. Investing with Style. Journal of Investment Management 13: 27–63. [Google Scholar]

- Asness, Clifford S., Tobias J. Moskowitz, and Lasse H. Pedersen. 2013. Value and Momentum Everywhere. The Journal of Finance 68: 929–85. [Google Scholar] [CrossRef] [Green Version]

- Baker, Scott R., Nicholas Bloom, Steven J. Davis, Kyle Kost, Macro Sammon, and Tasaneeya Viratyosin. 2020. The Unprecedent Stock Market Reaction to COVID-19. The Review of Asset Pricing Studies 10: 742–58. [Google Scholar] [CrossRef]

- Bakshi, Gurdip, John Crosby, Xiaohui Gao, and Wei Zhou. 2020. A New Formula for the Expected Excess Return of the Market. Available online: https://ssrn.com/abstract=3464298 (accessed on 30 January 2021).

- Bansal, Ravi, Shane Miller, Dongho Song, and Amir Yaron. 2019. The Term Structure of Equity Risk Premia. NBER. Working Paper 25690. Available online: https://www.nber.org/papers/w25690 (accessed on 4 June 2019).

- Bouchard, Jean-Philippe, Stefano Ciliberti, Augustin Landier, Guillaume Simon, and David Thesmar. 2016. The Excess Returns of “Quality” Stocks: A Behavioral Anomaly. Journal of Investing Strategies 5: 51–61. [Google Scholar] [CrossRef] [Green Version]

- Bretscher, Lorenzo, Alex Hsu, Peter Simasek, and Andrea Tamoni. 2020. COVID-19 and the Cross-Section of Equity Returns: Impact and Transmission. The Review of Asset Pricing Studies 10: 705–41. [Google Scholar] [CrossRef]

- Carhart, Mark M. 1997. On Persistence in Mutual Fund Performance. The Journal of Finance 52: 57–82. [Google Scholar] [CrossRef]

- Chabi-Yo, Fousseni, and Johnathan Loudis. 2020. The Conditional Expected Market Return. Journal of Financial Economics 137: 752–86. [Google Scholar] [CrossRef]

- Chen, Zhuo, and Andrea Lu. 2019. A Market-Based Funding Liquidity Measure. The Review of Asset Pricing Studies 9: 356–93. [Google Scholar] [CrossRef]

- Clarke, Charles. 2021. The Level, Slope, and Curve Factor Models for Stocks. Journal of Financial Economics 143: 159–87. [Google Scholar] [CrossRef]

- Cochrane, John H. 2011. Presidential Address: Discount Rates. The Journal of Finance 66: 1047–108. [Google Scholar] [CrossRef] [Green Version]

- Fama, Eugene F., and Kenneth R. French. 1993. Common Risk Factors in the Return of Stocks and Bonds. Journal of Financial Economics 33: 3–56. [Google Scholar] [CrossRef]

- Frazzini, Andrea, and Lasse H. Pedersen. 2014. Betting against Beta. Journal of Financial Economics 111: 1–25. [Google Scholar] [CrossRef] [Green Version]

- González-Sánchez, Mariano, Juan Nave, and Gonzalo Rubio. 2018. Macroeconomic Determinants of Stock Market Betas. Journal of Empirical Finance 45: 26–44. [Google Scholar] [CrossRef]

- González-Sánchez, Mariano, Juan Nave, and Gonzalo Rubio. 2020. Effects of Uncertainty and Risk Aversion on the Exposure of Investment-Style Factor Returns to Real Activity. Research in International Business and Finance 53: 583–96. [Google Scholar] [CrossRef]

- González-Urteaga, Ana, and Gonzalo Rubio. 2021. The Quality Premium with Leverage and Liquidity Constraints. International Review of Financial Analysis 75: 101699. [Google Scholar] [CrossRef]

- Gormsen, Niels J. 2021. Time Variation of the Equity Term Structure. The Journal of Finance 76: 1959–99. [Google Scholar] [CrossRef]

- Gormsen, Niels J., and Ralph S. J. Koijen. 2020. Coronavirus: Impact on Stock Prices and Growth Expectations. The Review of Asset Pricing Studies 10: 574–97. [Google Scholar] [CrossRef]

- Harvey, Campbell R., Yan Liu, and Heqing Zhu. 2016. … and the Cross-Section of Expected Returns. The Review of Financial Studies 29: 5–68. [Google Scholar] [CrossRef] [Green Version]

- Israel, Ronen, and Thomas Maloney. 2014. Understanding Style Premia. The Journal of Investing 23: 15–22. [Google Scholar] [CrossRef]

- Israel, Ronen, Kristoffer Lauren, and Scott Richardson. 2021. Is (Systematic) Value Investing Dead? The Journal of Portfolio Management 47: 38–62. [Google Scholar] [CrossRef]

- Jackwerth, Jens. 2020. What Do Index Options Teach US About COVID-19? The Review of Asset Pricing Studies 10: 618–34. [Google Scholar] [CrossRef]

- Jensen, Theis I., Bryan T. Kelly, and Lasse H. Pedersen. 2021. Is There a Replication Crisis in Finance? NBER Working Paper 28432. Available online: https://www.nber.org/papers/w28432 (accessed on 10 May 2021).

- Kelly, Bryan T., Tobias J. Moskowitz, and Seth Pruitt. 2021. Understanding Momentum and Reversal. Journal of Financial Economics 140: 726–43. [Google Scholar] [CrossRef]

- Maio, Paulo, and Dennis Philip. 2018. Economic Activity and Momentum Profits: Further Evidence. Journal of Banking and Finance 88: 466–82. [Google Scholar] [CrossRef] [Green Version]

- Martin, Ian. 2017. What is the Expected Return on the Market? The Quarterly Journal of Economics 132: 367–433. [Google Scholar] [CrossRef] [Green Version]

- Ramelli, Stefano, and Alexander F. Wagner. 2020. Feverish Stock Price Reactions to COVID-19. The Review of Corporate Finance Studies 9: 622–55. [Google Scholar] [CrossRef]

- Rossi, Alberto G., and Allan Timmermann. 2015. Modelling Covariance Risk in Merton’s ICAPM. The Review of Financial Studies 28: 1428–61. [Google Scholar] [CrossRef] [Green Version]

- Rubio, Gonzalo, Pedro Serrano, and Antoni Vaello. 2021. University CEU Cardenal Herrera, Elche, Sapin, University Carlos III, Madrid, Spain, University Islas Baleares, Mallorca, Sapin. The Term Structure of International Option-Implied Expected Equity Risk Premia and its Reaction to Uncertainty and Risk Aversion Shocks. Personal communication. [Google Scholar]

- Schneider, Paul, Christian Wagner, and Josef Zechner. 2020. Low Risk Anomalies? The Journal of Finance 75: 2673–718. [Google Scholar] [CrossRef] [Green Version]

- Spatt, Chester S. 2020. A Tale of Two Crises: The 2008 Mortgage Meltdown and the 2020 COVID-19 Crisis. The Review of Asset Pricing Studies 10: 759–90. [Google Scholar] [CrossRef]

- Van Binsbergen, Jules H., and Ralph S. J. Koijen. 2017. The Term Structure of Returns: Facts and Theory. Journal of Financial Economics 124: 1–21. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Lu. 2005. The Value Premium. The Journal of Finance 60: 67–103. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Panel A: Pre-COVID-19 | Panel B: COVID-19 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| January through March for All Years 1997–2019 | January through March 2020 | |||||||||||||

| MKT | SMB | HML | HML D | MOM | QMJ | BAB | MKT | SMB | HML | HML D | MOM | QMJ | BAB | |

| SWI | 0.054 | 0.086 | 0.089 | 0.014 | 0.184 | 0.055 | 0.131 | −0.536 | −0.240 | −0.362 | −0.559 | 0.279 | 0.307 | 1.959 |

| DEU | 0.056 | 0.045 | 0.020 | −0.016 | 0.185 | 0.035 | 0.054 | −0.969 | 0.146 | −0.495 | −0.641 | 0.348 | 0.116 | 0.380 |

| DNK | 0.171 | 0.050 | −0.028 | −0.050 | 0.033 | 0.059 | 0.125 | −0.342 | 0.032 | −0.591 | −1.063 | 0.598 | 0.839 | 0.151 |

| SPN | 0.055 | 0.220 | 0.077 | 0.047 | 0.017 | 0.003 | 0.118 | −1.190 | −0.029 | 0.171 | −0.184 | 0.882 | 0.214 | 0.334 |

| FRA | 0.072 | 0.072 | 0.045 | −0.003 | 0.108 | −0.003 | 0.214 | −1.105 | 0.009 | −0.374 | −0.415 | 0.210 | 0.565 | 0.205 |

| GBR | 0.022 | 0.059 | 0.053 | 0.043 | 0.136 | 0.078 | 0.092 | −1.276 | −0.302 | −0.526 | −0.796 | 0.581 | 0.180 | −0.103 |

| ITA | 0.094 | 0.108 | 0.118 | 0.007 | 0.124 | 0.068 | 0.161 | −1.137 | −0.185 | −0.376 | −0.693 | 0.618 | 0.369 | −0.063 |

| NLD | 0.065 | 0.130 | 0.017 | 0.002 | 0.129 | 0.048 | 0.111 | −0.785 | −0.239 | −0.184 | −0.350 | 0.701 | 1.016 | 0.002 |

| AUS | 0.104 | −0.018 | 0.112 | 0.013 | 0.246 | 0.051 | 0.118 | −1.493 | −0.196 | −0.468 | −0.506 | 0.558 | 0.429 | −0.291 |

| JPN | 0.053 | 0.077 | 0.071 | 0.163 | −0.065 | −0.021 | 0.030 | −0.669 | −0.106 | −0.083 | −0.156 | 0.170 | 0.236 | −0.067 |

| HKG | 0.033 | 0.132 | 0.011 | 0.014 | 0.190 | 0.078 | 0.282 | −0.506 | 0.019 | −0.469 | −0.516 | 0.521 | 0.097 | −0.402 |

| USA | 0.077 | 0.047 | 0.002 | 0.023 | 0.063 | 0.006 | 0.137 | −0.793 | −0.394 | −0.912 | −1.055 | 0.552 | 0.182 | −0.272 |

| Global | 0.064 | 0.058 | 0.035 | 0.043 | 0.080 | 0.018 | 0.131 | −0.936 | −0.265 | −0.674 | −0.807 | 0.525 | 0.239 | −0.212 |

| Panel A: Pre-COVID-19 | Panel B: COVID-19 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| January through March for All Years 1997–2019 | January through March 2020 | |||||||||||||

| MKT | SMB | HML | HML D | MOM | QMJ | BAB | MKT | SMB | HML | HML D | MOM | QMJ | BAB | |

| SWI | 0.159 | 0.093 | 0.104 | 0.110 | 0.123 | 0.112 | 0.162 | 0.287 | 0.106 | 0.118 | 0.122 | 0.164 | 0.148 | 0.363 |

| DEU | 0.187 | 0.115 | 0.106 | 0.120 | 0.133 | 0.092 | 0.197 | 0.327 | 0.093 | 0.113 | 0.125 | 0.089 | 0.074 | 0.327 |

| DNK | 0.169 | 0.126 | 0.154 | 0.158 | 0.144 | 0.129 | 0.173 | 0.294 | 0.151 | 0.166 | 0.178 | 0.124 | 0.129 | 0.163 |

| SPN | 0.206 | 0.110 | 0.117 | 0.129 | 0.145 | 0.132 | 0.179 | 0.356 | 0.141 | 0.147 | 0.137 | 0.131 | 0.174 | 0.257 |

| FRA | 0.185 | 0.116 | 0.094 | 0.103 | 0.118 | 0.094 | 0.166 | 0.358 | 0.146 | 0.104 | 0.104 | 0.086 | 0.104 | 0.213 |

| GBR | 0.167 | 0.114 | 0.090 | 0.097 | 0.111 | 0.080 | 0.109 | 0.370 | 0.173 | 0.134 | 0.149 | 0.104 | 0.061 | 0.146 |

| ITA | 0.208 | 0.117 | 0.116 | 0.126 | 0.148 | 0.126 | 0.141 | 0.416 | 0.159 | 0.118 | 0.133 | 0.108 | 0.107 | 0.134 |

| NLD | 0.182 | 0.114 | 0.135 | 0.151 | 0.166 | 0.145 | 0.183 | 0.329 | 0.125 | 0.132 | 0.185 | 0.165 | 0.166 | 0.244 |

| AUS | 0.174 | 0.098 | 0.082 | 0.098 | 0.103 | 0.075 | 0.103 | 0.386 | 0.212 | 0.116 | 0.130 | 0.101 | 0.112 | 0.151 |

| JPN | 0.209 | 0.086 | 0.067 | 0.088 | 0.127 | 0.088 | 0.145 | 0.253 | 0.099 | 0.088 | 0.101 | 0.066 | 0.048 | 0.147 |

| HKG | 0.211 | 0.126 | 0.110 | 0.116 | 0.129 | 0.113 | 0.138 | 0.295 | 0.137 | 0.092 | 0.093 | 0.071 | 0.062 | 0.070 |

| USA | 0.158 | 0.074 | 0.071 | 0.092 | 0.119 | 0.072 | 0.094 | 0.427 | 0.114 | 0.114 | 0.138 | 0.114 | 0.087 | 0.223 |

| Global | 0.125 | 0.049 | 0.046 | 0.061 | 0.086 | 0.053 | 0.069 | 0.331 | 0.071 | 0.075 | 0.091 | 0.074 | 0.059 | 0.139 |

| Panel A: Pre-COVID-19 | Panel B: COVID-19 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| January through March for All Years 1997–2019 | January through March 2020 | |||||||||||||

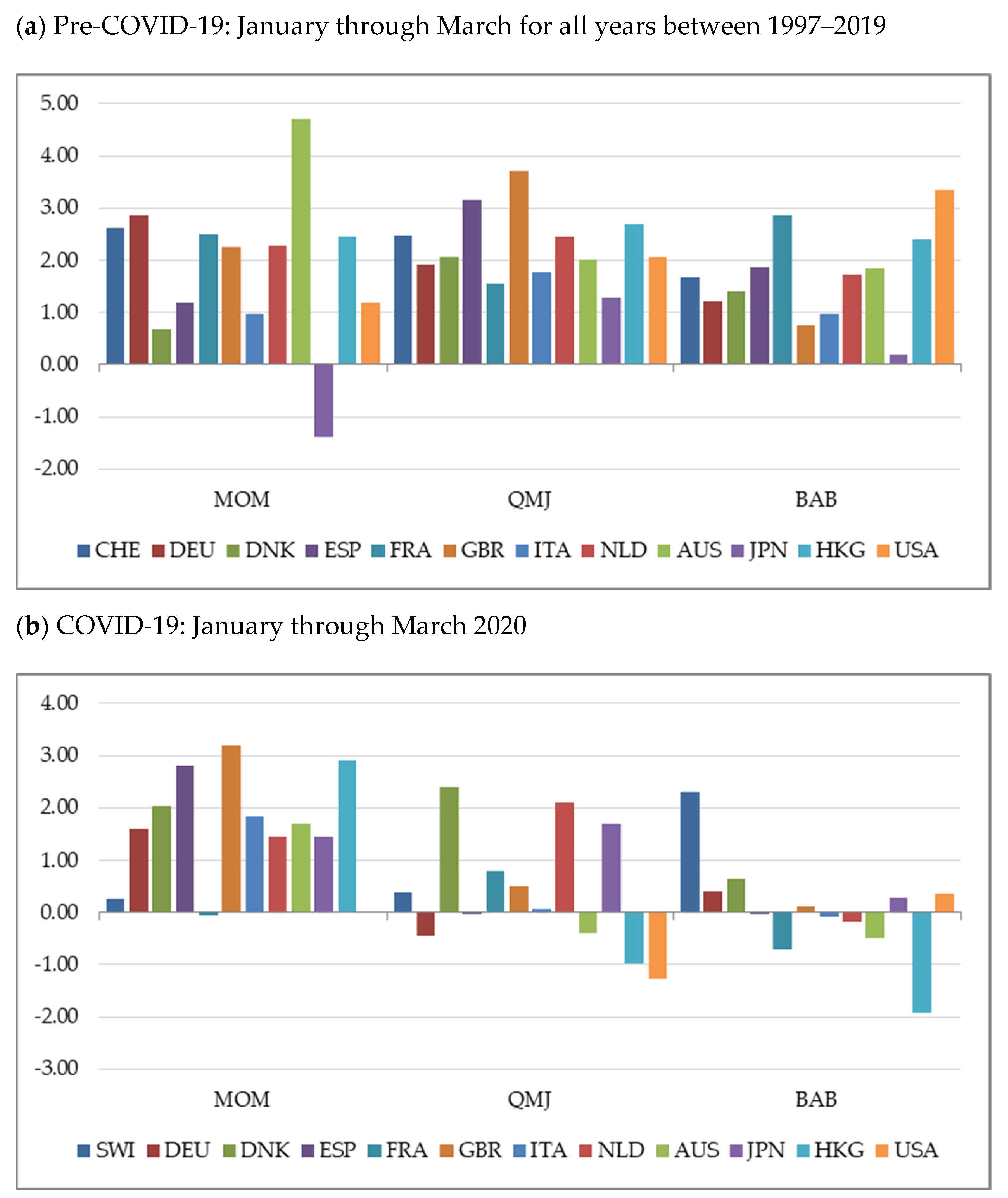

| MKT | SMB | HML | HML D | MOM | QMJ | BAB | MKT | SMB | HML | HML D | MOM | QMJ | BAB | |

| SWI | 0.282 | 0.280 | 0.276 | 0.071 | 0.542 | 0.065 | 0.191 | −0.596 | −0.548 | −0.654 | −0.653 | 0.674 | 0.653 | 0.789 |

| DEU | 0.229 | 0.214 | 0.085 | −0.056 | 0.489 | 0.130 | 0.042 | −1.013 | 0.527 | −1.100 | −1.371 | 0.943 | 0.213 | 0.568 |

| DNK | 0.417 | 0.168 | 0.053 | −0.055 | 0.166 | 0.163 | 0.293 | −0.332 | 0.766 | −1.054 | −1.714 | 1.247 | 1.932 | 0.423 |

| SPN | 0.200 | 0.662 | 0.204 | 0.090 | 0.141 | 0.041 | 0.263 | −0.986 | 0.114 | 0.349 | −0.410 | 1.976 | 0.207 | 0.263 |

| FRA | 0.267 | 0.263 | 0.201 | −0.006 | 0.438 | −0.014 | 0.374 | −1.056 | −0.041 | −0.907 | −1.044 | 0.856 | 1.178 | 0.370 |

| GBR | 0.198 | 0.248 | 0.173 | 0.035 | 0.650 | 0.327 | 0.469 | −1.251 | −0.206 | −1.122 | −1.470 | 1.889 | 0.734 | 0.040 |

| ITA | 0.260 | 0.300 | 0.297 | 0.031 | 0.362 | 0.208 | 0.345 | −0.739 | −0.492 | −0.730 | −1.284 | 1.859 | 0.762 | −0.152 |

| NLD | 0.283 | 0.397 | 0.047 | −0.050 | 0.318 | 0.138 | 0.296 | −0.766 | 0.124 | −0.686 | −0.694 | 1.363 | 1.891 | 0.028 |

| AUS | 0.240 | −0.050 | 0.449 | 0.034 | 0.898 | 0.226 | 0.409 | −0.948 | −0.504 | −1.227 | −1.356 | 1.498 | 0.906 | −0.347 |

| JPN | 0.152 | 0.330 | 0.403 | 0.520 | 0.219 | 0.026 | 0.136 | −1.016 | −0.843 | −0.161 | −0.333 | 0.704 | 1.915 | 0.174 |

| HKG | 0.190 | 0.312 | 0.057 | 0.002 | 0.612 | 0.410 | 0.714 | −0.469 | 0.089 | −1.395 | −1.556 | 2.235 | 0.352 | −1.414 |

| USA | 0.370 | 0.237 | 0.010 | 0.026 | 0.403 | 0.033 | 0.807 | −0.617 | −0.978 | −2.637 | −2.608 | 1.638 | −0.024 | −0.086 |

| Global | 0.353 | 0.441 | 0.292 | 0.175 | 0.607 | 0.145 | 0.891 | −0.893 | −1.006 | −2.807 | −2.864 | 2.226 | 0.535 | −0.050 |

| Panel A: Pre-COVID-19 | Panel B: COVID-19 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| January through March for All Years 1997–2019 | January through March 2020 | |||||||||||

| SMB | HML | HML D | MOM | QMJ | BAB | SMB | HML | HML D | MOM | QMJ | BAB | |

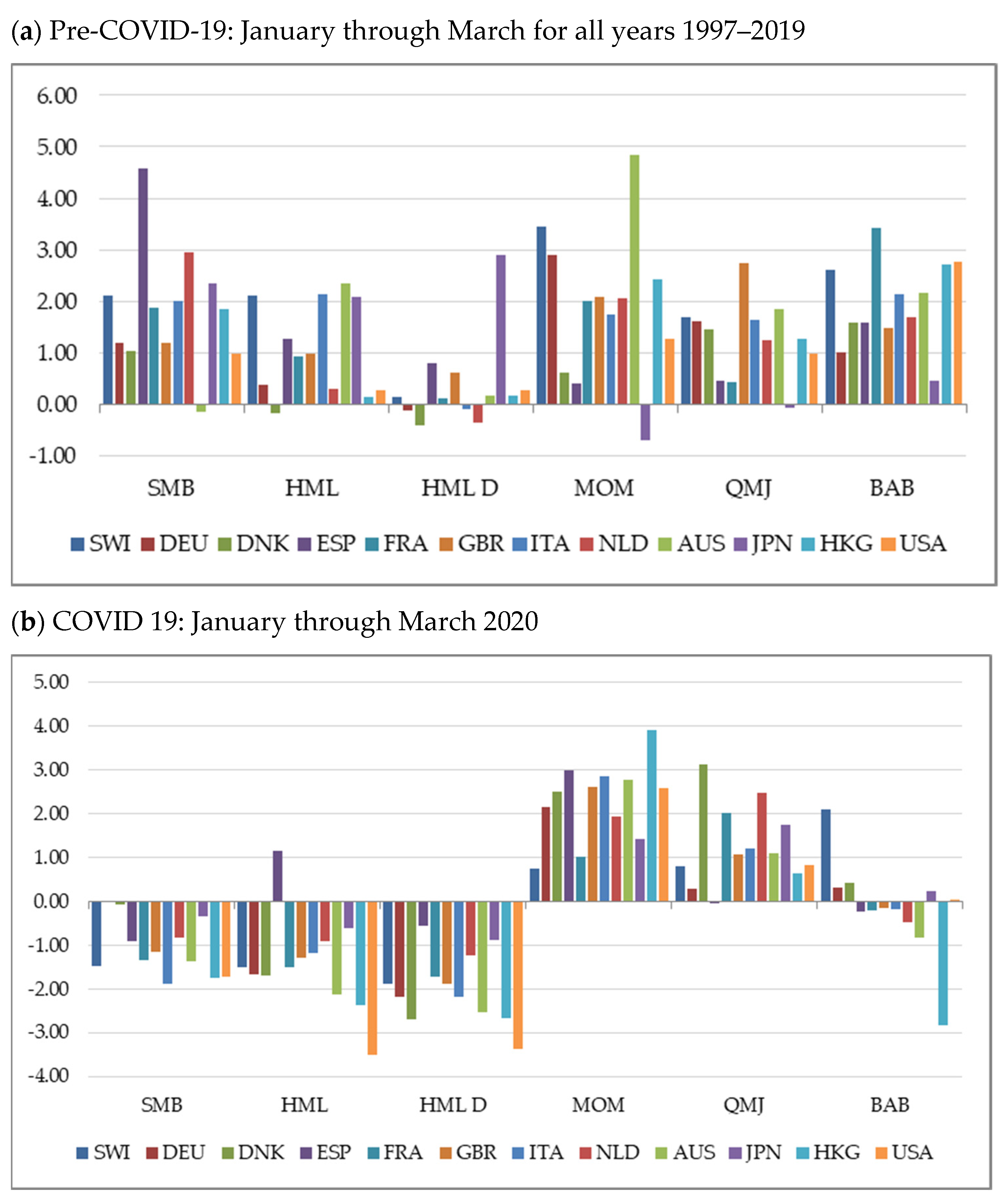

| SWI | 0.096 | 0.097 | 0.007 | 0.195 | 0.077 | 0.140 | −0.320 | −0.378 | −0.541 | 0.277 | 0.259 | 1.957 |

| (2.10) | (2.10) | (0.14) | (3.44) | (1.69) | (2.61) | (−1.47) | (−1.52) | (−1.88) | (0.75) | (0.80) | (2.09) | |

| DEU | 0.052 | 0.023 | −0.010 | 0.204 | 0.051 | 0.063 | −0.001 | −0.372 | −0.562 | 0.399 | 0.041 | 0.204 |

| (1.19) | (0.38)) | (−0.13) | (2.89) | (1.61) | (1.01) | (−0.01) | (−1.67) | (−2.18) | (2.16) | (0.29) | (0.31) | |

| DNK | 0.061 | −0.011 | −0.028 | 0.038 | 0.072 | 0.135 | −0.026 | −0.589 | −1.059 | 0.635 | 0.804 | 0.144 |

| (1.04) | (−0.18) | (−0.42) | (0.63) | (1.45) | (1.58) | (−0.08) | (−1.69) | (−2.69) | (2.51) | (3.12) | (0.42) | |

| SPN | 0.221 | 0.077 | 0.048 | 0.029 | 0.023 | 0.116 | −0.243 | 0.332 | −0.157 | 0.845 | −0.018 | −0.101 |

| (4.59) | (1.28) | (0.79) | (0.40) | (0.45) | (1.60) | (−0.92) | (1.16) | (−0.56) | (3.00) | (−0.05) | (−0.23) | |

| FRA | 0.082 | 0.058 | 0.008 | 0.121 | 0.018 | 0.222 | −0.317 | −0.348 | −0.395 | 0.184 | 0.401 | −0.073 |

| (1.87) | (0.92) | (0.10) | (2.01) | (0.42) | (3.42) | (−1.34) | (−1.51) | (−1.73) | (1.02) | (2.02) | (−0.19) | |

| GBR | 0.063 | 0.051 | 0.039 | 0.145 | 0.082 | 0.093 | −0.464 | −0.380 | −0.641 | 0.607 | 0.135 | −0.045 |

| (1.19) | (0.99) | (0.63) | (2.08) | (2.74) | (1.48) | (−1.15) | (−1.28) | (−1.88) | (2.62) | (1.08) | (−0.14) | |

| ITA | 0.092 | 0.098 | −0.008 | 0.143 | 0.106 | 0.157 | −0.468 | −0.300 | −0.631 | 0.655 | 0.263 | −0.046 |

| (2.01) | (2.14) | (−0.11) | (1.75) | (1.65) | (2.14) | (−1.88) | (−1.19) | (−2.17) | (2.86) | (1.21) | (−0.17) | |

| NLD | 0.128 | 0.017 | −0.023 | 0.158 | 0.076 | 0.116 | −0.232 | −0.251 | −0.478 | 0.709 | 0.768 | −0.213 |

| (2.95) | (0.29) | (−0.36) | (2.05) | (1.23) | (1.70) | (−0.82) | (−0.91) | (−1.23) | (1.94) | (2.48) | (−0.46) | |

| AUS | −0.007 | 0.115 | 0.008 | 0.267 | 0.065 | 0.101 | −0.619 | −0.519 | −0.656 | 0.605 | 0.261 | −0.293 |

| (−0.15) | (2.34) | (0.16) | (4.83) | (1.86) | (2.17) | (−1.37) | (−2.13) | (−2.52) | (2.79) | (1.09) | (−0.83) | |

| JPN | 0.074 | 0.071 | 0.158 | −0.052 | −0.002 | 0.027 | −0.082 | −0.113 | −0.182 | 0.189 | 0.176 | 0.073 |

| (2.35) | (2.09) | (2.89) | (−0.69) | (−0.06) | (0.46) | (−0.35) | (−0.61) | (−0.87) | (1.43) | (1.76) | (0.22) | |

| HKG | 0.130 | 0.009 | 0.013 | 0.199 | 0.100 | 0.291 | −0.191 | −0.441 | −0.502 | 0.548 | 0.078 | −0.393 |

| (1.85) | (0.13) | (0.16) | (2.44) | (1.27) | (2.72) | (−1.74) | (−2.38) | (−2.67) | (3.92) | (0.64) | (−2.83) | |

| USA | 0.042 | 0.013 | 0.017 | 0.095 | 0.034 | 0.168 | −0.458 | −0.895 | −1.047 | 0.603 | 0.170 | 0.018 |

| (0.99) | (0.28) | (0.29) | (1.28) | (1.00) | (2.76) | (−1.74) | (−3.51) | (−3.38) | (2.59) | (0.83) | (0.05) | |

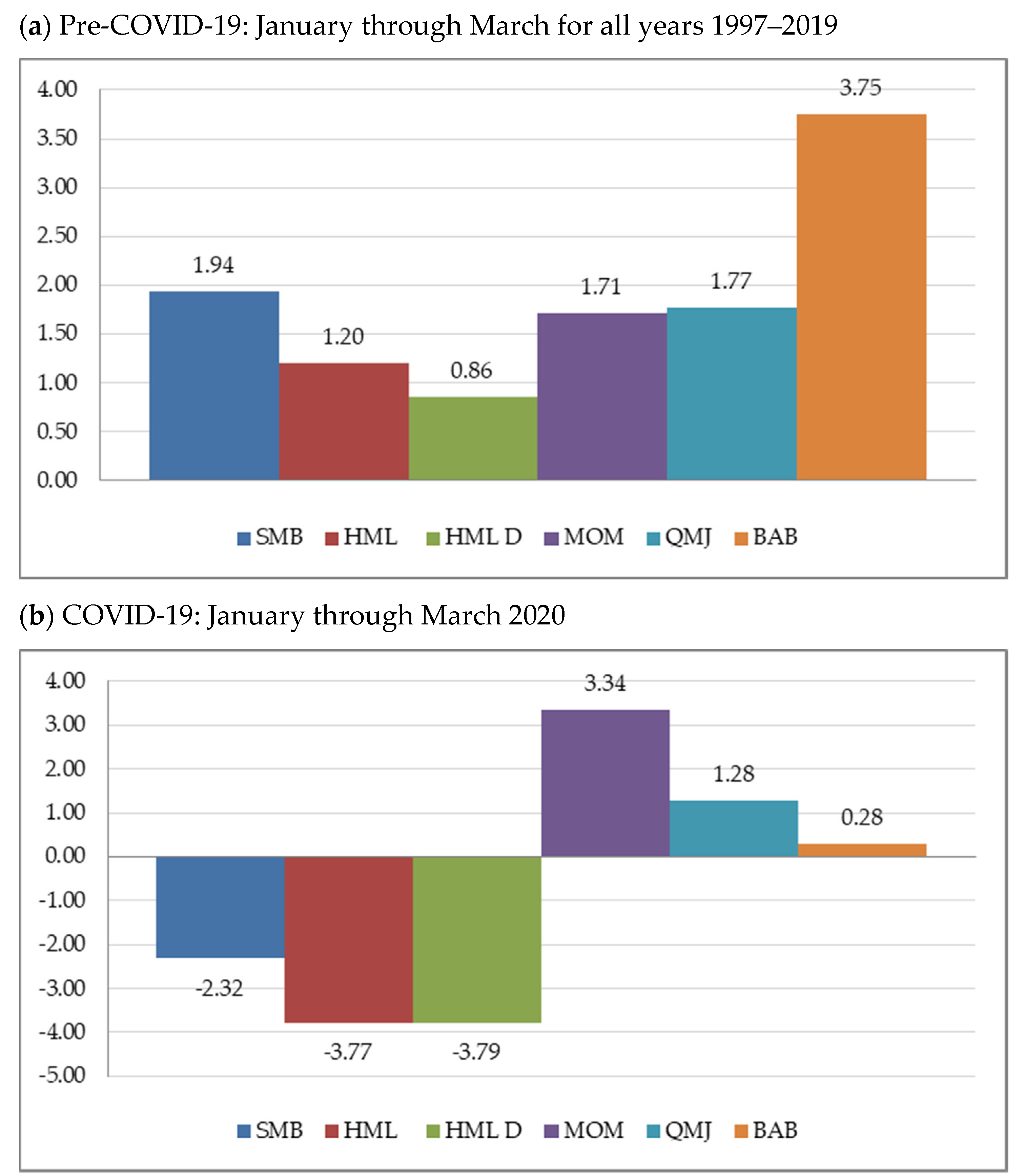

| Global | 0.058 | 0.043 | 0.042 | 0.102 | 0.040 | 0.147 | −0.347 | −0.635 | −0.786 | 0.531 | 0.169 | 0.068 |

| (1.94) | (1.20) | (0.86) | (1.71) | (1.77) | (3.75) | (−2.32) | (−3.77) | (−3.79) | (3.34) | (1.28) | (0.28) | |

| Panel A: Pre-COVID-19 | Panel B: COVID-19 | |||||

|---|---|---|---|---|---|---|

| January through March for All Years 1997–2019 | January through March 2020 | |||||

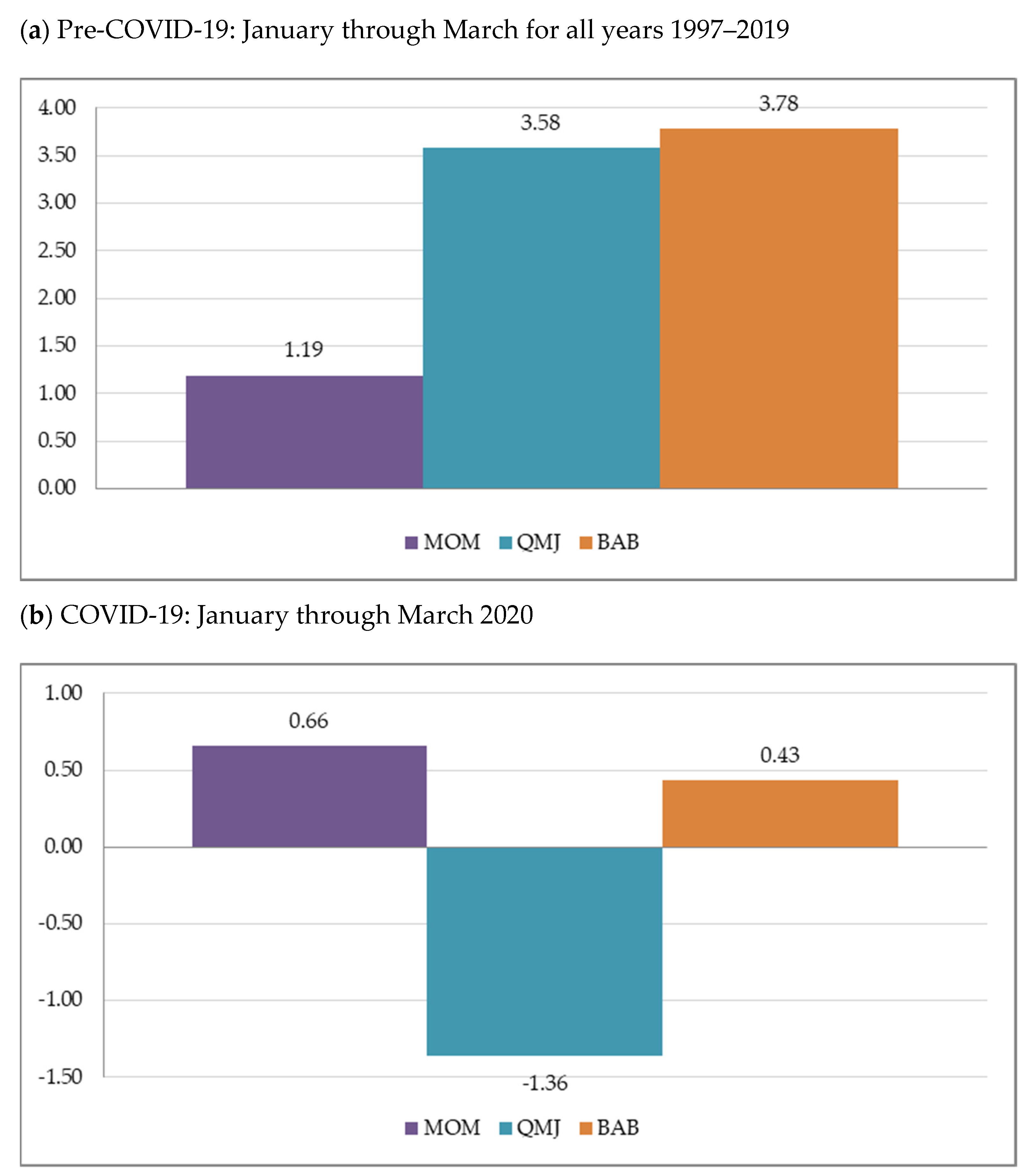

| MOM | QMJ | BAB | MOM | QMJ | BAB | |

| SWI | 0.161 | 0.118 | 0.095 | 0.093 | 0.121 | 2.223 |

| (2.63) | (2.46) | (1.67) | (0.25) | (0.37) | (2.30) | |

| DEU | 0.201 | 0.059 | 0.076 | 0.252 | −0.058 | 0.271 |

| (2.86) | (1.91) | (1.22) | (1.58) | (−0.44) | (0.40) | |

| DNK | 0.042 | 0.092 | 0.120 | 0.477 | 0.506 | 0.225 |

| (0.68) | (2.06) | (1.41) | (2.02) | (2.39) | (0.64) | |

| SPN | 0.099 | 0.154 | 0.154 | 0.807 | −0.004 | −0.006 |

| (1.19) | (3.16) | (1.87) | (2.82) | (−0.01) | (−0.01) | |

| FRA | 0.153 | 0.059 | 0.184 | −0.010 | 0.125 | −0.277 |

| (2.51) | (1.55) | (2.87) | (−0.07) | (0.79) | (−0.72) | |

| GBR | 0.159 | 0.105 | 0.044 | 0.538 | 0.064 | 0.026 |

| (2.26) | (3.70) | (0.74) | (3.20) | (0.51) | (0.10) | |

| ITA | 0.082 | 0.117 | 0.069 | 0.419 | 0.013 | −0.027 |

| (0.98) | (1.76) | (0.97) | (1.84) | (0.06) | (−0.09) | |

| NLD | 0.186 | 0.148 | 0.127 | 0.412 | 0.541 | −0.077 |

| (2.27) | (2.44) | (1.73) | (1.45) | (2.10) | (−0.17) | |

| AUS | 0.273 | 0.070 | 0.089 | 0.329 | −0.075 | −0.147 |

| (4.69) | (2.01) | (1.84) | (1.70) | (−0.39) | (−0.49) | |

| JPN | −0.107 | 0.042 | 0.013 | 0.140 | 0.158 | 0.099 |

| (−1.37) | (1.29) | (0.20) | (1.44) | (1.69) | (0.30) | |

| HKG | 0.202 | 0.171 | 0.220 | 0.342 | −0.106 | −0.271 |

| (2.46) | (2.69) | (2.40) | (2.92) | (−0.98) | (−1.93) | |

| USA | 0.090 | 0.054 | 0.176 | 0.003 | −0.232 | 0.132 |

| (1.18) | (2.06) | (3.35) | (0.02) | (−1.28) | (0.35) | |

| Global | 0.075 | 0.067 | 0.126 | 0.079 | −0.159 | 0.115 |

| (1.19) | (3.58) | (3.78) | (0.66) | (−1.36) | (0.43) | |

| Panel A: The Great Recession | |||||||

| October 2007–August 2009 | |||||||

| MKT | SMB | HML | HML D | MOM | QMJ | BAB | |

| DEU | −29.53 | −2.46 | 0.53 | 15.52 | 10.74 | 20.98 | −4.66 |

| GBR | −35.68 | −21.00 | 5.73 | 14.70 | −5.50 | 12.87 | −55.74 |

| AUS | −34.21 | −7.89 | 5.69 | 2.07 | 3.31 | 16.73 | −7.27 |

| JPN | −21.86 | −4.47 | 7.14 | 22.81 | −15.79 | 4.98 | −1.41 |

| HKG | −24.75 | −1.52 | −1.64 | 18.10 | −46.53 | 11.32 | −9.84 |

| USA | −27.70 | 2.40 | −10.71 | 0.01 | −25.36 | 15.22 | −23.81 |

| Global | −28.46 | −3.30 | −3.80 | 7.62 | −16.58 | 13.00 | −16.10 |

| Panel B: COVID-19 | |||||||

| January 2020–March 2020 | |||||||

| MKT | SMB | HML | HML D | MOM | QMJ | BAB | |

| DEU | −196.83 | 24.99 | −45.24 | −56.99 | 25.14 | 9.42 | 60.94 |

| GBR | −258.10 | −18.49 | −59.47 | −83.92 | 53.42 | 10.74 | −31.25 |

| AUS | −273.80 | −27.96 | −42.34 | −41.16 | 57.36 | 58.96 | −49.71 |

| JPN | −147.13 | −20.18 | −5.97 | −13.89 | 12.02 | 27.83 | −21.03 |

| HKG | −109.51 | 28.19 | −60.63 | −61.18 | 50.79 | 11.74 | −51.14 |

| USA | −179.23 | −34.62 | −104.89 | −116.09 | 55.67 | 21.52 | −72.59 |

| Global | −179.23 | −18.19 | −76.81 | −88.32 | 49.60 | 26.19 | −41.30 |

| Panel A: The Great Recession | |||

| September 2008–December 2008 | |||

| S&P 500 | Euro Stoxx 50 | Nikkei 225 | FTSE 100 |

| −0.140 | −0.144 | −0.186 | −0.133 |

| (−6.69) | (−6.15) | (−4.98) | (−6.32) |

| Panel B: COVID-19 | |||

| January 2020–April 2020 | |||

| S&P 500 | Euro Stoxx 50 | Nikkei 225 | FTSE 100 |

| −0.075 | −0.074 | −0.074 | −0.061 |

| (−3.25) | (−3.22) | (−3.37) | (−3.46) |

| Panel A: The Great Recession | ||||

| September 2008–December 2008 | ||||

| S&P 500 | Euro Stoxx 50 | Nikkei 225 | FTSE 100 | |

| Intercept | −0.128 | −0.122 | −0.171 | −0.115 |

| (−6.74) | (−6.67) | (−4.74) | (−6.52) | |

| Slope | −0.052 | −0.090 | −0.063 | −0.075 |

| (−1.57) | (−2.42) | (−1.49) | (−1.81) | |

| Adj. R2 (%) | 3.36 | 9.17 | 0.78 | 7.04 |

| Panel B: COVID-19 | ||||

| January 2020–April 2020 | ||||

| S&P 500 | Euro Stoxx 50 | Nikkei 225 | FTSE 100 | |

| Intercept | −0.052 | −0.051 | −0.065 | −0.039 |

| (−2.91) | (−2.90) | (−2.82) | (−4.35) | |

| Slope | −0.112 | −0.107 | −0.045 | −0.101 |

| (−3.16) | (−3.55) | (−1.46) | (−5.17) | |

| Adj. R2 (%) | 17.05 | 17.10 | 2.10 | 25.78 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nieto, B.; Rubio, G. The Effects of the COVID-19 Crisis on Risk Factors and Option-Implied Expected Market Risk Premia: An International Perspective. J. Risk Financial Manag. 2022, 15, 13. https://doi.org/10.3390/jrfm15010013

Nieto B, Rubio G. The Effects of the COVID-19 Crisis on Risk Factors and Option-Implied Expected Market Risk Premia: An International Perspective. Journal of Risk and Financial Management. 2022; 15(1):13. https://doi.org/10.3390/jrfm15010013

Chicago/Turabian StyleNieto, Belén, and Gonzalo Rubio. 2022. "The Effects of the COVID-19 Crisis on Risk Factors and Option-Implied Expected Market Risk Premia: An International Perspective" Journal of Risk and Financial Management 15, no. 1: 13. https://doi.org/10.3390/jrfm15010013

APA StyleNieto, B., & Rubio, G. (2022). The Effects of the COVID-19 Crisis on Risk Factors and Option-Implied Expected Market Risk Premia: An International Perspective. Journal of Risk and Financial Management, 15(1), 13. https://doi.org/10.3390/jrfm15010013