Empirical Analysis of the User Needs and the Business Models in the Norwegian Charging Infrastructure Ecosystem

Abstract

:1. Introduction

2. BEV Ownership and Charging Infrastructure Use in Norway

2.1. BEV Ownership in Norway

2.2. BEV Charging in Norway

3. Business Models for Charging Stations

4. Materials and Methods

4.1. Methods Used to Investigate User Needs

4.1.1. Literature Review

4.1.2. Vehicle User Survey

4.1.3. BEV Owner Interviews

4.2. Methods Used to Investigate the Functioning of the Charging Infrastructure Ecosystem

4.2.1. Literature Review

4.2.2. Open Data Collection

4.2.3. Charging Infrastructure Ecosystem Value Chain Analysis

4.2.4. Charging Ecosystem Actor Interaction Mapping

4.2.5. Semi-Structured Interviews with Charging Infrastructure Actors

4.3. Charging Infrastructure Scenarios

5. Results

5.1. User Needs

5.1.1. User-Friendliness

“There are many different systems in terms of physical plugs. What kind of plug is this? What power can I get out of this one? What is most up to date? Is it the same standard on a Tesla? After a while, you start to understand”.Informant 6

“Often I see people that are not accustomed to driving an electric vehicle, trying to use the charger that I’m already using, thinking they can use the other cable (there are two options, one that I can’t remember the name of and CSS). Visible information on the charger should have been available where it says that you can only use one cable at a time”.Informant 8

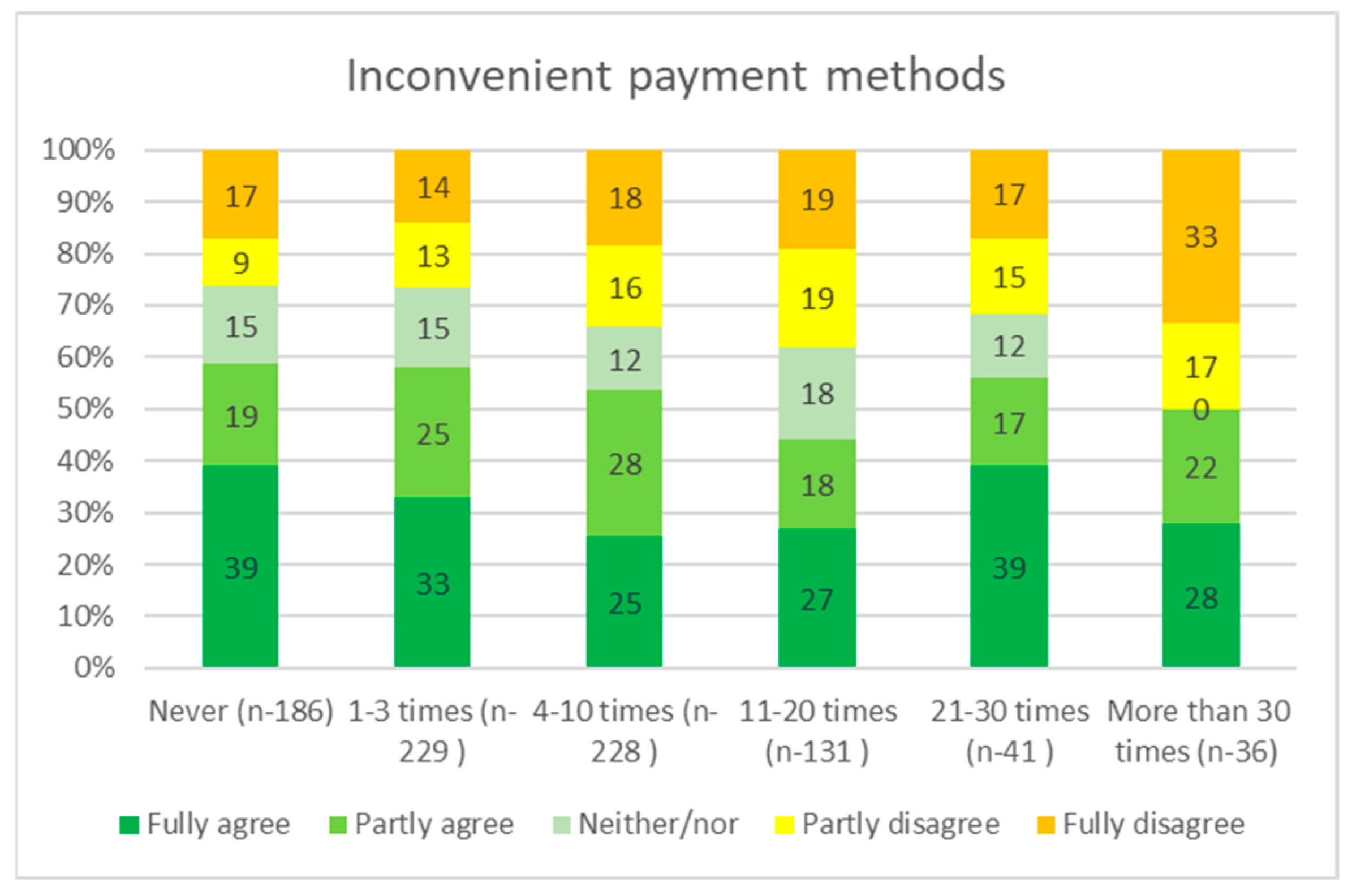

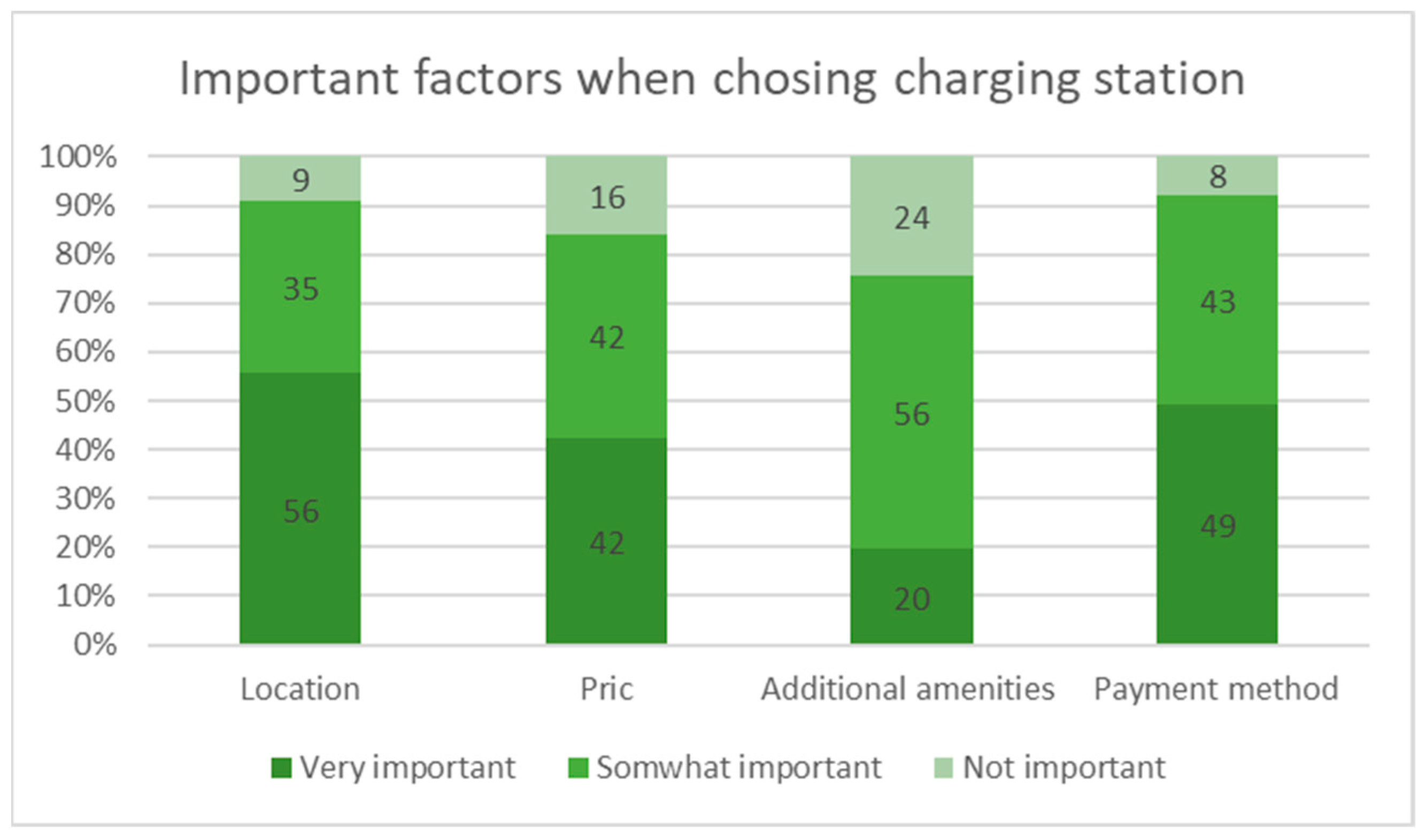

5.1.2. Pricing and Payment Method

“What annoys me is the price. The taximeter starts before the charging has begun and it ends a couple of seconds after the charging is finished. The Norwegian Metrology Service should conduct controls on fast charger stations, like they do on gas stations, so we are not taken advantage of. It boils down to seconds”.Informant 4

“The problem is lacking information about how fast I’m charging; how much I’m charging and how much it costs. These three things tend to be hidden at most charging stations. It’s normally when you have finished charging that you know how much you’ve spent, unless you’ve brought a calculator and do the math yourself”.Informant 9

“It’s like going to a petrol station where they’ve covered all the prices with white tags. You can’t see the price before after you’ve charged. That really sucks”.Informant 5

“It is hopeless that precise pricing is not available, like at petrol stations. I would prefer information about actual costs and received kWh during the charging session. Ideally, I could indicate the wanted charging percentage at the beginning, and the charging session would automatically stop when this percentage is achieved”.

“I want to be able to pay by credit/debit card, get information on the price before I start the charging, and receive information about the actual costs after the charging session is ended”.

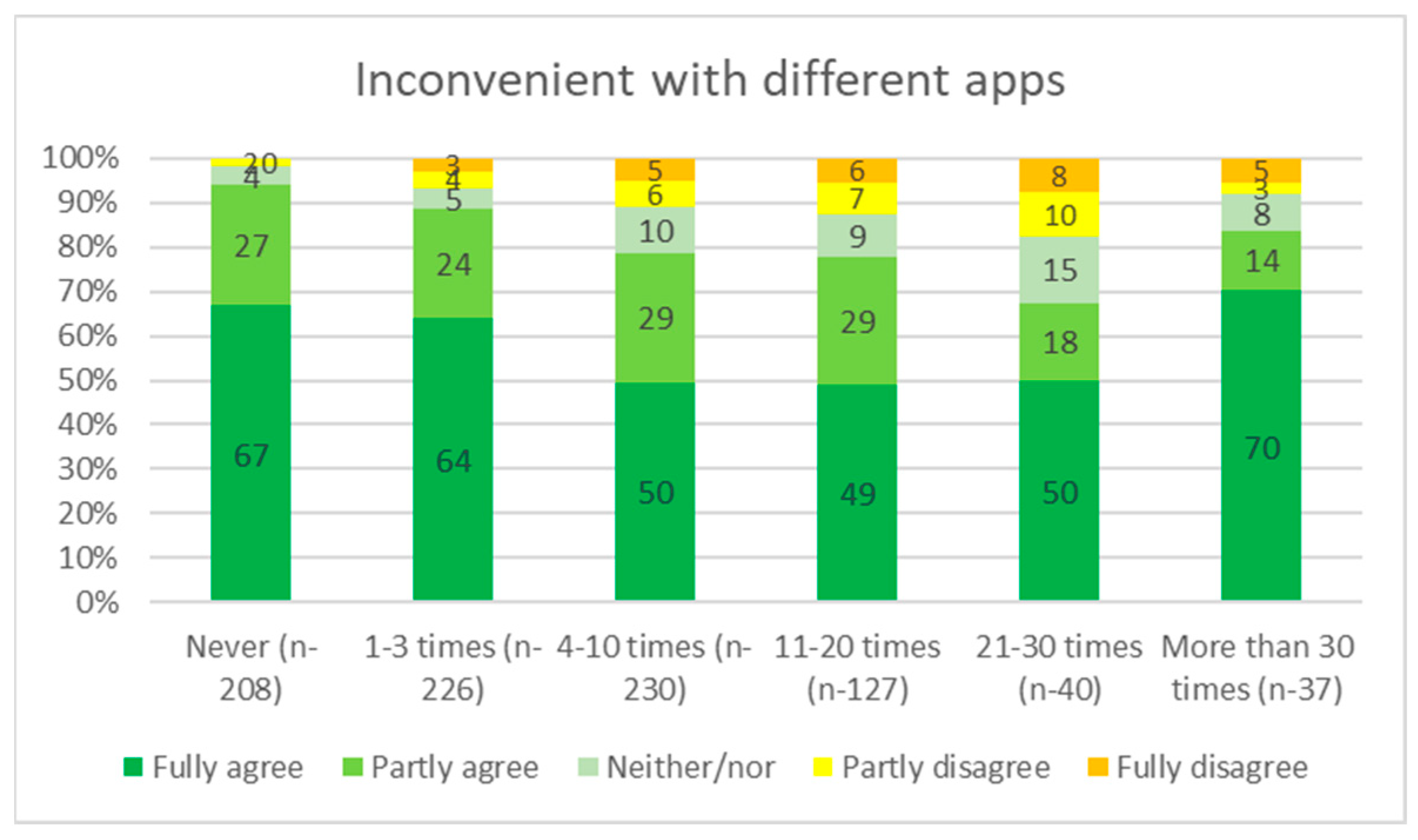

“Having all these apps is confusing, because if I’m planning a trip, I can’t just use Google Maps and find all the different charger services there. My experience is that I’m unable to get a full overview, and that I’m forced to use each app individually to locate charging stations, and get information about the terms and so forth, and then I’m not even sure if I have the right app”.Informant 10

“An opportunity for simpler payment would be nice. To be able to pay with credit card (…). An elderly person who uses fast chargers on rare occasions would want to do it as simple as possible. If this was better, I think the development in terms of the number of electric vehicles would go much faster”.Informant 5

“It should have been a common method for payment at all public charging stations, without having to download an app to the phone. Should be possible to pay with debit or credit card. Not everybody is comfortable with apps, especially the elderly”.

5.1.3. Information and On-Site Services

“I normally charge where I can use toilets, buy ice-cream, coffee etc. That is much more OK than (charging stations) where there are just two chargers in the middle of nowhere. It’s nice to be able to do something other than just sit in the car. I would not let it determine my path, but along the route I am going, I would choose charging stations with extra service options. This is more important than if I save 15 kroner (NOK, NOK 1 = EUR 0.1) on charging”.Informant 7

“I’m not very fond of chargers that are in the middle of nowhere. It must be facilities that allows you to do something there while charging. Gas station, toilet, etc.”.Informant 8

“I have experienced that the there are no available charging points when arriving at a charging station. It’s difficult to know how long others plan to charge and where to park in the meantime. How does the queuing system work? Are you supposed to drive to the next charging point? (…) I get that all charging points are busy sometimes, but the fact that you’re not provided with any information regarding when it will be available, creates a sense of uncertainty. There should be a function on the charger where you could plot in ‘I need to have 50 km left so I get home, how long does it take?’”.Informant 5

“When it comes to amenities, the type of amenities is not so important, if it is a grocery store, a kiosk or a café. The important thing is that there is something. The best option would be if the chargers were placed at petrol station because they are usually open 24/7 and have toilet facilities”.

“A form of booking/queue handling system should be available, to avoid arguments and “pointed elbows” on popular weekends”.

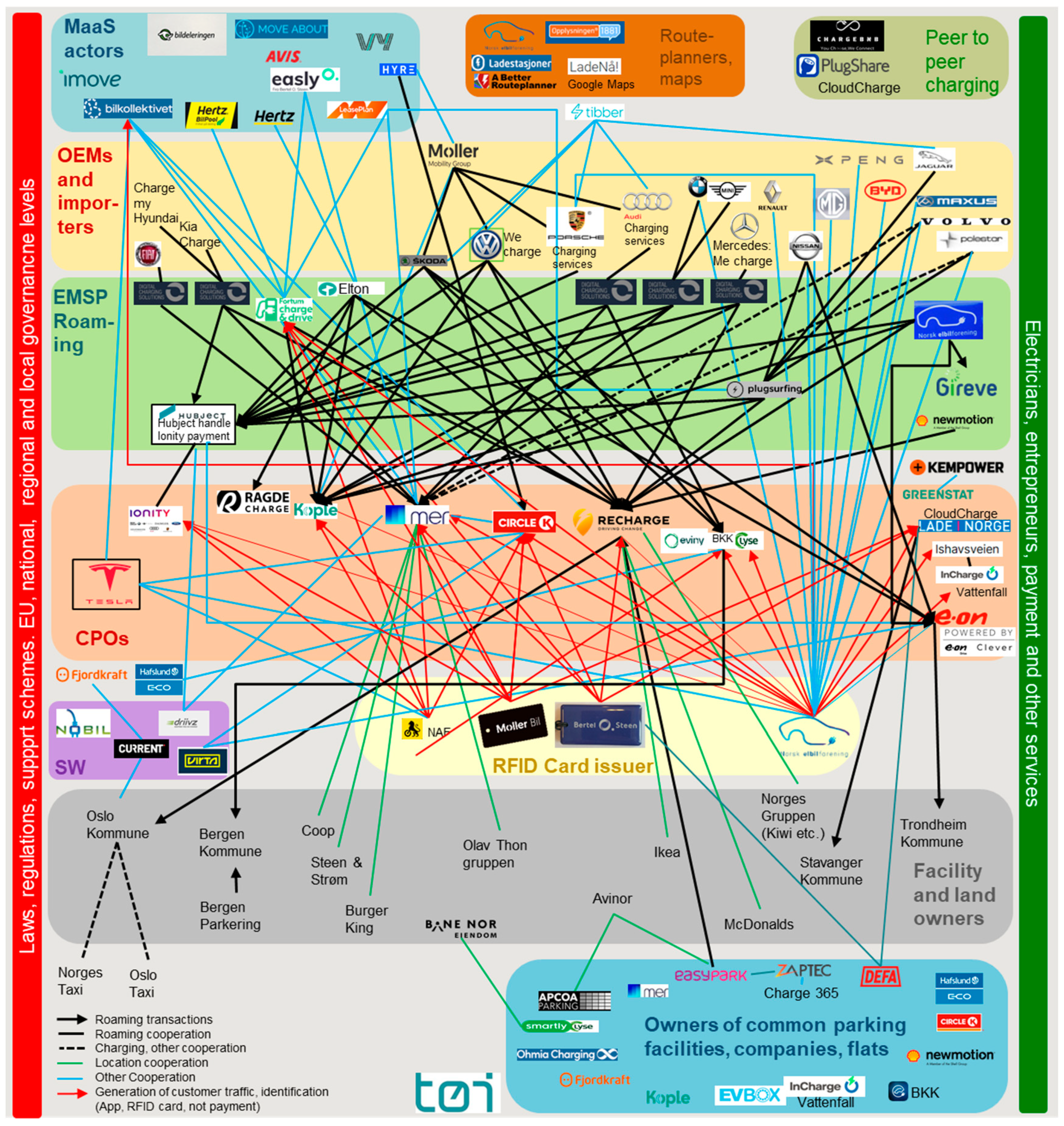

5.2. The Norwegian Charging Infrastructure Ecosystem Actor Landscape

5.3. Promising Business Models in the Norwegian Charging Infrastructure Ecosystem

- Integrated location owner + CPO + EMSP + charging system supplier for housing cooperatives/condominiums, private households and companies, semi-closed but cooperates with other CPOs (Circle K).

- Integrated CPO + EMSP + charging system supplier for apartment buildings, companies + pop-up charging, open for roaming and also a provider of CPO services under contract for a number of municipalities/counties (Kople).

- Roaming EMSP with map services (Elton).

- Provider of platform solutions for CPOs, EMSPs, installers, electricity producers, and grid companies, which enable operation and management, smart charging, and eventually V2G (current).

- Electricity supplier EMSP (without roaming) + supplier of hardware and software solutions for charging at homes, housing cooperatives/condominiums, workplaces, and destinations (Fortum Charge and Drive).

- Integrated CPO + EMSP + charging system supplier for apartment buildings and companies, semi-closed. Can also be an asset owner, and in some cases a site owner (Mer and BKK).

- Manufacturer of hardware and software—all segments (up to 22 kW AC) (Easee and Zaptec). These actors mainly produce chargers for home and parking facilities.

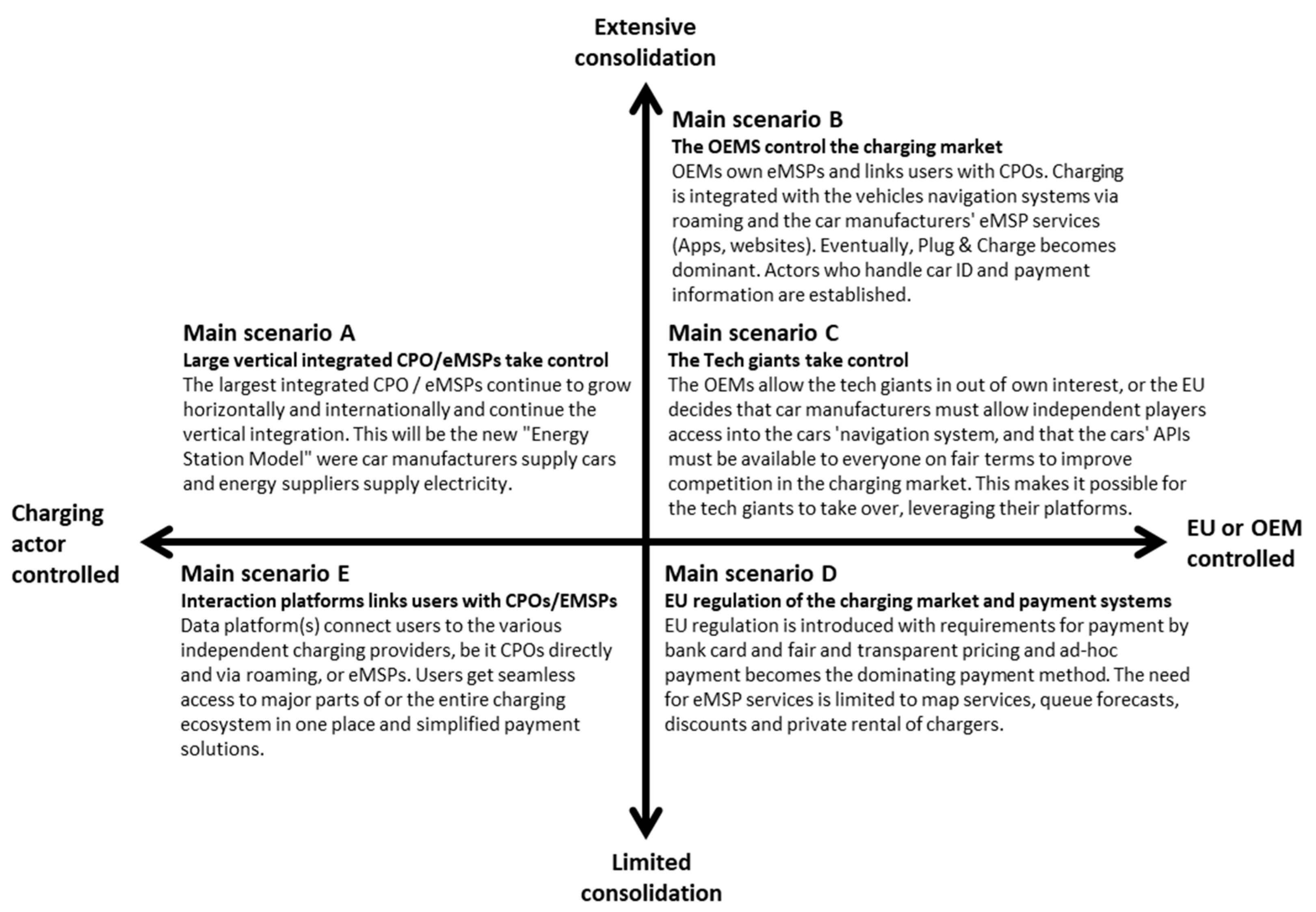

5.4. Scenarios for the Future

- Business-as-usual (BAU) with many and probably increasing number of players. Voluntary roaming is limited, and none of the CPO networks are large enough by themselves so that BEV drivers can get by with only one user interface on a long trip to a new destination. New actors joining will lead to increased user complexity by adding more apps and payment solutions to the overall system. The user needs for simple and efficient charging analyzed in Section 5.1 will thus not be met.

- Consolidation into large, vertically integrated semi-closed CPOs. The least profitable CPOs have dropped out of the market or merged with the large remaining ones that grow alongside the BEV market. They tend to have a large horizontal (multiple charging customer segments) and vertical coverage (e.g., energy retail and energy stations with convenience products). This scenario will function better for users than the BAU. The number of actors will be reduced, and each actor will have a larger network. Given their size, some users may only need to use one network.

- Interaction and roaming platforms connect charging infrastructure players with charging customers. Interaction and roaming platforms gain enough volume so that it becomes hard for the “stubborn” CPOs and EMSPs to “lock in” their customers by refusing roaming. This scenario will allow users to virtually interact with only one app to gain access to multiple CPOs networks, as Elton is today on a small scale. This development would improve the user-friendliness of charging but can be more costly for the user as the platform will add a small cost to the transaction.

- “The people want to roam freely!” Roaming becomes the industry standard. Preferences of both charging customers for maximal roaming possibilities and site owners for maximal volumes will favor CPOs that agree to roaming and put pressure on the CPOs that follow a more closed strategy. Charging will be more easily accessible for users but may be slightly more costly due to the roaming charges.

- Car manufacturer (OEM)-controlled future with charging integrated into the car’s navigation system. OEMs will directly or indirectly provide EMSP services through the cars’ navigation system, as a part of their expanded service portfolio. Such services will increase in relative importance, as revenue from vehicle maintenance services will decline. OEMs will have leverage to obtain seamless access to CPO networks and even be a force pressuring for expanded roaming possibilities. This scenario will significantly improve the user-friendliness of charging.

- Plug and charge—the cars identify themselves automatically and payment is seamless. Some OEMs and CPOs will lead the way towards increased use of plug and charge in order to compete with the customer experience of Tesla, which already offers this service. Plug and charge will make it much easier to charge where it is enabled, but may not work on all chargers, at least in a long switchover period. The potential for improved user-friendliness is very large, but in an early transition period it may add complexity by becoming yet another solution for identification and payment.

- Regulation requires a splitting into separate CPOs and eMSPs. In order to ensure more competition and less “lock-in” of customers, regulators require in this scenario that CPOs and EMSPs are separate companies and require CPOs to provide fair access to all EMSPs. This scenario will be similar for users, like scenario 4. The difference is how it comes about.

- BEVs obtain a longer range that allows charging mainly at home and at destinations. Fast charging will in this scenario be of less relative importance compared to home and destination charging, which is much cheaper. There will be a strong growth in destination charging, “become-your-own-CPO-solutions”, and peer-to-peer charging solutions. For users, this will be a simplification as charging issues will be encountered less frequently and long-distance driving will be easier.

- The EU sets the standard for ensuring seamless charging across national borders in Europe (including Norway). The regulation will make ad hoc payment simpler, likely with bank/credit cards, as well as more transparent, and it will allow BEV users to be anonymous. It will reduce the need for EMSPs. It also reduces CPOs’ ability to “lock in” customers, but other user-friendliness issues such as different plugs, power levels, and charging interfaces will remain.

- The technology giants take over. Tech giants (e.g., Google and Apple) have become the dominant EMSPs as they provide services through products the charging customer already uses, i.e., the smart phone. These tech giants have payment solutions and ample amounts of data for prediction of real-time traffic conditions to fine tune their services already. OEMs will have strong incentives to give the tech giants’ platforms access to their navigation systems. This scenario can provide BEV owners with services not available to ICEV owners, such as real-time info about the likelihood of queues when needing to charge on the basis of data they already use for travel time prediction.

6. Discussion and Conclusions

6.1. Considering Developments up to 2021

- Standardizing the payment method. The same type(s) of payment methods should be available at all stations. Preferably, it is one common app for all charging stations, as well as easy options for drop-in clients (debit/credit card option).

- Standardizing the pricing system. The price should be clearly marked, and the pricing system should be easily comparable between different charging stations (without having to download an app).

- Standardizing the charging operation (user-friendliness). Available user information, placing of charging cables to fit all vehicle models, method for starting the charging, etc. Universal design at fast charging stations (easy use independent of nationality, technological skills, or disabilities).

- Standardizing the level of amenities at fast charging stations along the major highway network, such as, for instance, toilets, light, garbage bins, road signs, roof, etc.

6.2. Future Developments and Furter Research

6.3. Caveats

- Tesla opened on 31 January a total of 15 locations and 315 charge points for non-Tesla owners, which was expanded to 58 locations and 812 charge points on 3 May. Non-Tesla owners must, however, use yet another app to gain access, and not all BEVs can use Tesla chargers due to the positioning of the charge inlet and the length of the cables.

- The EV Association launched their roaming EMSP service “Ladeklubben” (Charging club) on 17 February. A blue RFID card provides access to charging at Recharge, Kople, Ionity, E.on, and Powered by E.on, providing access to 275,000 chargers across Europe.

- The popular Norwegian instant payment service “Vipps” became more common as Mer and Eviny also took it into use during 2022.

- Pricing became standardized during 2022. All the large CPOs and EMSPs now charge in NOK per kWh.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Amundsen, A.H.; Milch, V. Demand for standardization of public fast charger stations—User perspectives. In Proceedings of the 35th International Electric Vehicle Symposium and Exhibition (EVS35), Oslo, Norway, 11–15 June 2022. [Google Scholar]

- Figenbaum, E.; Wangsness, P.B. The Norwegian Charging Infrastructure Ecosystem. In Proceedings of the 35th International Electric Vehicle Symposium and Exhibition (EVS35), Oslo, Norway, 11–15 June 2022. [Google Scholar]

- Wangsness, P.B.; Figenbaum, E. The Charging Market—Complex and Dysfunctional or Future-Oriented? TOI Report (in Norwegian) 1867/2022. Institute of Transport Economics, September 2022. Available online: https://www.toi.no/publications/the-charging-market-complex-and-dysfunctional-or-future-oriented-article37371-29.html (accessed on 27 September 2022).

- Figenbaum, E. Norway—The World Leader in BEV Adoption. In Who’s Driving Electric Cars. Lecture Notes in Mobility; Contestabile, M., Tal, G., Turrentine, T., Eds.; Springer: Cham, Switzerland, 2020. [Google Scholar] [CrossRef]

- IEA. Norway (Electromobility Status 2022). In The Electric Drive Charges Ahead. IEA HEVTCP Annual Report 2022. 2022. Available online: https://ieahev.org/wp-content/uploads/2022/05/DIGITAL-HEVTCP_2022_Annual_Report_Final-with-Cover.pdf (accessed on 1 August 2022).

- Statistics Norway, to Av Tre Nye Personbiler er Elbiler. Available online: https://www.ssb.no/transport-og-reiseliv/landtransport/statistikk/bilparken/artikler/to-av-tre-nye-personbiler-er-elbiler (accessed on 25 April 2022).

- OFVAS. Car Sales Statistics. Bilsalget i JUNI 2022 (og Første Halvår 2022). OFV AS. 2022. Available online: https://ofv.no/bilsalget/bilsalget-i-juni-2021-2-2 (accessed on 1 August 2022).

- Figenbaum, E. Retrospective Total Cost of Ownership analysis of Battery Electric Vehicles in Norway. Transp. Res. Part D 2022, 105, 105103246. [Google Scholar] [CrossRef]

- Figenbaum, E. Perspectives on Norway’s supercharged electric vehicle policy. Environ. Innov. Soc. Transit. 2017, 25, 14–34. Available online: http://www.sciencedirect.com/science/article/pii/S2210422416301162 (accessed on 22 March 2022). [CrossRef] [Green Version]

- Figenbaum, E. The 1990 to 2020 Technology Innovation System supporting Norway’s BEV revolution. Working Paper. 19 March 2022. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4061401 (accessed on 10 August 2022).

- Ministry of Transport. National Transport Plan 2022–2033. Oslo. 2021. Available online: https://www.regjeringen.no/en/topics/transport-and-communications/content-2021/national-transport-plan-20222033/id2866098/ (accessed on 10 January 2022).

- Government. UNFCCC Paris Agreement. Norway’s First NDC 2016. Norway’s Nationally Determined Contribution to the Paris Agreement. 20 June 2016. Available online: https://unfccc.int/sites/default/files/NorwayINDC.pdf (accessed on 27 September 2022).

- Figenbaum, E.; Nordbakke, S. Battery Electric Vehicle User Experiences in Norway’s Maturing Market. TØI Report 1719/2019. Available online: https://www.toi.no/publications/battery-electric-vehicle-user-experiences-in-norway-s-maturing-market-article35709-29.html?deviceAdjustmentDone=1 (accessed on 10 May 2022).

- Fevang, E.; Figenbaum, E.L.; Halse, A.H.; Hauge, K.E.; Johansen, B.J.; Raaum, O. 2021. Who goes electric? The anatomy of electric car ownership in Norway. Transp. Res. Part D 2021, 92, 102727. [Google Scholar] [CrossRef]

- Hardman, S.; Jenn, A.; Tal, G.; Axsen, J.; Beard, G.; Daina, N.; Figenbaum, E.; Jakobsson, N.; Jochem, P.; Kinnear, N.; et al. A review of consumer preferences of and interactions with electric vehicle recharging infrastructure. Transp. Res. Part D 2018, 62, 508–523. Available online: https://www.sciencedirect.com/science/article/pii/S1361920918301330 (accessed on 27 September 2022). [CrossRef] [Green Version]

- Figenbaum, E. Electromobility status in Norway: Mastering Long Distances—The Last Hurdle to Mass Adoption. TØI Report 1627/2018. Institute of Transport Economics. 2018. Available online: https://www.toi.no/publications/electromobility-status-in-norway-mastering-long-distances-the-last-hurdle-to-mass-adoption-article34903-29.html (accessed on 27 September 2022).

- Bjerkan, K.Y.; Nørbech, T.E.; Nordtømme, M.E. Incentives for Promoting Battery Electric Vehicle (BEV) Adoption in Norway. Transp. Res. Part D 2016, 43, 169–180. [Google Scholar] [CrossRef] [Green Version]

- Figenbaum, E.; Kolbenstvedt, M. Learning from Norwegian Battery Electric and Plug-In Hybrid Vehicle Users. Results from a Survey of Vehicle Owners. TØI Report 1492/2016. Institute of Transport Economics. Available online: https://www.toi.no/publications/learning-from-norwegian-battery-electric-and-plug-in-hybrid-vehicle-users-results-from-a-survey-of-vehicle-owners-article33869-29.html (accessed on 27 September 2022).

- Ydersbond, I.M.; Amundsen, A.H. Fast Charging and Long-Distance Driving by Electric Cars in Inland Norway, ISBN 978-82-480-2148-3, TOI Report 1775, Oslo, Institute of Transport Economics. 2020. Available online: https://www.toi.no/publications/fast-charging-and-long-distance-driving-by-electric-cars-in-inland-norway-article36311-29.html (accessed on 27 September 2022).

- Figenbaum, E. Battery electric fast charging—Evidence from Norwegian market. World Electr. Veh. J. 2020, 11, 38. [Google Scholar] [CrossRef]

- Norwegian Environment Agency & Norwegian Public Road Association. Kunnskapsgrunnlag om Hurtigladeinfrastruktur for Veitransport. Oslo. 2022. Available online: https://www.regjeringen.no/contentassets/a07ef2d3142344989dfddc75f5a92365/kunnskapsgrunnlag_1mars.pdf (accessed on 27 September 2022).

- Zhang, Q.; Li, H.; Zhu, L.; Campana, P.E.; Lu, H.; Wallin, F.; Sun, Q. Factors influencing the economics of public charging infrastructures for EV—A review. Renew. Sustain. Energy Rev. 2018, 94, 500–509. Available online: https://www.sciencedirect.com/science/article/abs/pii/S136403211830460X (accessed on 27 September 2022). [CrossRef]

- Greene, D.L.; Kontou, E.; Borlaug, B.; Brooker, A.; Muratori, M. Public charging infrastructure for plug-in electric vehicles: What is it worth? Transp. Res. Part D Transp. Environ. 2020, 78, 102182. Available online: https://www.sciencedirect.com/science/article/abs/pii/S1361920919305309 (accessed on 27 September 2022). [CrossRef]

- de Rubens, G.Z.; Noel, L.; Kester, J.; Sovacool, B.K. The market case for electric mobility: Investigating electric vehicle business models for mass adoption. Energy 2020, 194, 116841. Available online: https://www.sciencedirect.com/science/article/abs/pii/S0360544219325368 (accessed on 27 September 2022). [CrossRef]

- van der Kam, M.; van Sark, W.; Alkemade, F. Multiple roads ahead: How charging behavior can guide charging infrastructure roll-out policy. Transp. Res. Part D Transp. Environ. 2020, 85, 102452. Available online: https://www.sciencedirect.com/science/article/pii/S1361920920306398 (accessed on 10 August 2022). [CrossRef]

- Boston Consulting Group. Winning the Battle in the EV Charging Ecosystem. BCG. 2021. Available online: https://www.bcg.com/publications/2021/the-evolution-of-charging-infrastructures-for-electric-vehicles (accessed on 9 June 2021).

- Deloitte. Hurry up and… Wait: The Opportunities Around Electric Vehicle Charge Points in the UK. 2019. Available online: https://www2.deloitte.com/content/dam/Deloitte/uk/Documents/energy-resources/deloitte-uk-Electric-Vehicles-uk.pdf (accessed on 21 January 2021).

- Helmus, J.; Van den Hoed, R. Key performance indicators of charging infrastructure. World Electr. Veh. J. 2016, 8, 733–741. Available online: https://www.mdpi.com/2032-6653/8/4/733 (accessed on 10 August 2022). [CrossRef] [Green Version]

- Schroeder, A.; Traber, T. The economics of fast charging infrastructure for electric vehicles. Energy Policy 2012, 43, 136–144. Available online: https://www.sciencedirect.com/science/article/abs/pii/S0301421511010470 (accessed on 10 August 2022). [CrossRef]

- Pöyry 2012a. Strategi og Kriteriesett for Utplassering av Hurtigladere (del 1). Utarbeidet for Transnova og Statens Vegvesen. Pöyry Rapport R-2012-007. Available online: https://docplayer.me/1090511-Strategi-og-kriteriesett-for-utplassering-av-hurtigladere-del-1-utarbeidet-for-transnova-og-statens-vegvesen-r-2012-007.html (accessed on 10 August 2022).

- Pöyry 2012b. Alternative Forretningsmodeller for Etablering av Hurtigladestasjoner—Del 2. Available online: https://www.osti.gov/etdeweb/servlets/purl/22000205 (accessed on 10 August 2022).

- How Governments Can Solve the EV Charging Dilemma. Boston Consulting Group (BCG). 12 October 2021. Available online: https://mkt-bcg-com-public-pdfs.s3.amazonaws.com/prod/electric-vehicle-charging-station-infrastructure-plan-for-governments.pdf (accessed on 10 August 2022).

- Kley, F.; Lerch, C.; Dallinger, D. New business models for electric cars—A holistic approach. Energy Policy 2011, 39, 3392–3403. Available online: https://www.sciencedirect.com/science/article/abs/pii/S0301421511002163 (accessed on 10 August 2022). [CrossRef] [Green Version]

- ADL. Electric Vehicle Charging in Europe: What Will be the Winning Business Models in a Rising Multibillion Euro Market? 2021. Available online: https://www.adlittle.com/en/insights/viewpoints/electric-vehicle-charging-uk-and-europe (accessed on 29 September 2022).

- Capgemini. Key Factors Defining. The E-Mobility of Tomorrow: A Focus on the EV Charging Infrastructure Ecosystem and Emerging Business Models. 2019. Available online: https://www.capgemini.com/wp-content/uploads/2019/02/Capgemini-Invent-EV-charging-points.pdf (accessed on 27 September 2022).

- PwC. Powering Ahead! Making Sense of Business Models in Electric Vehicle Charging. 2018. Available online: https://www.pwc.co.uk/power-utilities/assets/powering-ahead-ev-charging-infrastructure.pdf (accessed on 21 January 2021).

- Hardin, G. Science. New Series, Volume 162, No. 3859 1968. pp. 1243–1248, American Association for the Advancement of Science. Available online: http://web.mit.edu/2.813/www/readings/HardinCommons.pdf (accessed on 27 September 2022).

- Spöttle, M.; Jörling, K.; Schimmel, M.; Staats, M.; Grizzel, L.; Jerram, L.; Drier, W.; Gartner, J. Research for TRAN Committee-Charging Infrastructure for Electric Road Vehicles. European Parliament. 2018. Available online: https://www.europarl.europa.eu/thinktank/en/document/IPOL_STU(2018)617470 (accessed on 2 July 2021).

- Pagani, M.; Korosec, W.; Chokani, N.; Abhari, R.S. User behaviour and electric vehicle charging infrastructure: An agent-based model assessment. Appl. Energy 2019, 254, 113680. Available online: https://www.sciencedirect.com/science/article/abs/pii/S0306261919313674 (accessed on 27 September 2022). [CrossRef]

- Bland, R.; Gao, W.; Noffsinger, J.; Siccardo, G. Charging Electric-Vehicle Fleets: How to Seize the Emerging Opportunity. McKinsey & Company. 2020. Available online: https://www.mckinsey.com/~/media/McKinsey/Business%20Functions/Sustainability/Our%20Insights/Charging%20electric%20vehicle%20fleets%20How%20to%20seize%20the%20emerging%20opportunity/Charging-electric-vehicle-fleets-how-to-seize-the-emerging-opportunity-FINAL.pdf (accessed on 28 April 2021).

- Thronsen, M. Ny Undersøkelse: Nær Halvparten Forstår Ikke Prismodellene for Hurtiglading. Article in Norwegian, The Norwegian EV Association, Oslo, 2021-06-16. Available online: https://elbil.no/ny-undersokelse-naer-halvparten-forstar-ikke-prismodellene-for-hurtiglading/ (accessed on 10 August 2022).

- Norwegian Automobile Federation (NAF). Skal Alle Med—Noe Må Skje, Oslo. 2021. Available online: https://res.cloudinary.com/nafmedier/image/upload/v1625087243/Elbil/Rapporter/NAF_Laderapport_2021.pdf (accessed on 27 September 2022).

- European Commission. Proposal for a Regulation of the European Parliament and of the Council on the Deployment of Alternative Fuel Infrastructure and Repealing Directive 2014/94/EU of the European Parliament and the Council. Brussels, 14.7.2021. COM(2021) 559 Final. Available online: https://eur-lex.europa.eu/resource.html?uri=cellar:dbb134db-e575-11eb-a1a5-01aa75ed71a1.0001.02/DOC_1&format=PDF (accessed on 29 September 2022).

- TU 2022a.—Etter Vår Vurdering er Dette Brudd på Loven. TU 022. February 2022. Available online: https://www.tek.no/nyheter/nyhet/i/BjnKPe/etter-vaar-vurdering-er-dette-brudd-paa-loven (accessed on 6 July 2022).

- TU 2022b.—Rullestolbrukerne må Slite for å få Ladet. TU 18. January 2022. Available online: https://www.tek.no/nyheter/nyhet/i/MLJgnM/rullestolbrukerne-maa-slite-for-aa-faa-ladet (accessed on 6 July 2022).

- Pinchasik, D.; Figenbaum, E.; Hovi, I.B.; Amundsen, A.H. Grønn Lastebiltransport? Teknologistatus, Kostnader og Brukererfaringer (Green Trucking? Technology Status, Costs, User Experiences). TØI Rapport 1855/2021 (in Norwegian). 2021. Available online: https://www.toi.no/publications/green-trucking-technology-status-costs-user-experiences-article37226-29.html (accessed on 10 August 2022).

- CharIn 2022. Megawatt Charging System (MCS). Available online: https://www.charin.global/technology/mcs/ (accessed on 7 July 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Actor Type | Role |

|---|---|

| CPOs (charge point operators) | Installs, owns, and operates charging station hardware and software standalone or in co-operation with land or facility owners. They want as many users as possible to use their chargers and offer access through roaming networks and EMSPs. |

| CPOs with EMSPs, closed | These CPOs install, own, and operate charging station hardware and software standalone or co-operating with land/facility owners, including EMSP functions. Their networks provide complete customer experiences and secure the full charging revenue stream. |

| CPOs with EMSPs, open | As above, but their network is open for roaming through other EMSPs. |

| EMSPs | Connect BEV users with a CPO charger and starts and stops the charging and organizes payment. They take a percentage of what the user pays. The rest goes to the CPO. |

| Roaming facilitators | Integrates several CPO (and EMSP) networks into one network and takes a percentage of the transaction cost. Often international. |

| Producers of charging hardware | They manufacture charging hardware for one or more of the various charging segments; slow charging (home, workplace, destination, or public charging) or fast charging. |

| Facility and landowners | Cooperate with CPOs to install chargers to attract customers to their facilities. Large actors can leverage good locations to get chargers installed also in the less attractive locations, while CPOs can include such chargers into their national network. |

| Municipalities and counties | Property owner that may cooperate with CPOs to install chargers that serve those that cannot charge at home. Municipalities and counties may also provide economic support and facilitate installation of fast chargers on municipal land and in other locations. |

| Parking facility owner | Have chargers in their facilities, i.e., public parking, or parking facilities of flat owners. They often buy turn-key solutions from suppliers. |

| OEMs, their Norwegian importers | Sell BEVs. Want to deliver good experiences for their buyers. Some will roll-out plug and charge capabilities in 2022, and some have their own EMSP integrated into the vehicle navigation systems via roaming platforms or bi-lateral agreements with CPOs. The latter is pursued by some integrated CPO/EMSPs. |

| RFID card issuers | Want to give their customers and members easier charging experiences in the absence of roaming solutions. RFID cards allow for identification and payment if the user registers the card number and payment details with the CPOs they use. |

| BEV fleet operators | Car rental and car sharing companies and leasing services have customers that need and want easy access to charging services. |

| Maps, route planners | Shows the location and type of publicly available chargers, irrespective of who is the CPO in online and app-based map/route planners. |

| Software providers | Develop software required to provide charging services, such CPO/EMSP back- and frontend systems, as well as database services with location data and technical characteristics. |

| Electricity producers and retailers | Sell electricity used for BEV charging. Some of them are owners of CPOs, and/or sell home and destination charging hardware. Some retailers bundle rebate for charging together with the household electricity supply. |

| Supporting businesses | Electricians, entrepreneurs, payment system providers, etc. |

| Structural elements | Laws and regulations, authorities, support schemes, etc. |

| Segment | Hardware Production | Hardware Sales | Ownership (Site Asset) | Hardware Management and Operation | Software Management and Operation | E-Mobility Services | Energy, Powert Management | Electricity Production, Distribution and Retail | Retail Sale, other Income Sources | End User (Individual, Fleet), End User NGO | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| MER | Public—Fast chargers | ||||||||||

| Public—Normal | |||||||||||

| Workplace—Normal | |||||||||||

| Home—Flat owner | |||||||||||

| BKK | Public—Fast chargers | ||||||||||

| Public—Normal | |||||||||||

| Workplace—Normal | |||||||||||

| Home—Flat owner | |||||||||||

| Home—Detached house | |||||||||||

| CircleK | Public—Fast chargers | ||||||||||

| Public—Normal | |||||||||||

| Workplace—Normal | |||||||||||

| Home—Flat owner | |||||||||||

| Home—Detached house | |||||||||||

| Kople | Public—Fast chargers | ||||||||||

| Public—Normal | |||||||||||

| Workplace—Normal | |||||||||||

| Home—Flat owner | |||||||||||

| Recharge | Public—Fast chargers | ||||||||||

| Public—Normal | |||||||||||

| Workplace—Normal | |||||||||||

| Home—Flat owner | |||||||||||

| Ionity | Public—Fast chargers | ||||||||||

| E.ON, Powered by E.ON Drive & Clever | Public—Fast chargers | ||||||||||

| Public—Normal | |||||||||||

| Workplace—Normal | |||||||||||

| Home—Flat owner | |||||||||||

| Defa, Lade i Norge | Public—Normal | ||||||||||

| Workplace—Normal | |||||||||||

| Home—Flat owner | |||||||||||

| Home—Detached house | |||||||||||

| Elton | Public—Fast chargers | ||||||||||

| Public—Normal | |||||||||||

| Current | Software platform | ||||||||||

| Tibber | Electricity provider | ||||||||||

| Fjordkraft | Home—Flat owner | ||||||||||

| Easypark | Public—Normal | ||||||||||

| NAF | Automobile owners Ass. | ||||||||||

| EV Ass-ociation | Public—Fast chargers | ||||||||||

| Public—Normal | |||||||||||

| Oslo Munici-pality | Public—Fast chargers | ||||||||||

| Public—Normal | |||||||||||

| Taxis—Fast chargers | |||||||||||

| ZAPTEC | Public—Normal | ||||||||||

| Workplace—Normal | |||||||||||

| Home—Flat owner | |||||||||||

| Home—Detached house | |||||||||||

| EASEE | Public—Normal | ||||||||||

| Workplace—Normal | |||||||||||

| Home—Flat owner | |||||||||||

| Home—Detached house | |||||||||||

| Bilkollektivet | Car sharing | ||||||||||

| Avinor | Airport owner | ||||||||||

| McDonalds |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Figenbaum, E.; Wangsness, P.B.; Amundsen, A.H.; Milch, V. Empirical Analysis of the User Needs and the Business Models in the Norwegian Charging Infrastructure Ecosystem. World Electr. Veh. J. 2022, 13, 185. https://doi.org/10.3390/wevj13100185

Figenbaum E, Wangsness PB, Amundsen AH, Milch V. Empirical Analysis of the User Needs and the Business Models in the Norwegian Charging Infrastructure Ecosystem. World Electric Vehicle Journal. 2022; 13(10):185. https://doi.org/10.3390/wevj13100185

Chicago/Turabian StyleFigenbaum, Erik, Paal Brevik Wangsness, Astrid Helene Amundsen, and Vibeke Milch. 2022. "Empirical Analysis of the User Needs and the Business Models in the Norwegian Charging Infrastructure Ecosystem" World Electric Vehicle Journal 13, no. 10: 185. https://doi.org/10.3390/wevj13100185

APA StyleFigenbaum, E., Wangsness, P. B., Amundsen, A. H., & Milch, V. (2022). Empirical Analysis of the User Needs and the Business Models in the Norwegian Charging Infrastructure Ecosystem. World Electric Vehicle Journal, 13(10), 185. https://doi.org/10.3390/wevj13100185