Evolution, Forecasting, and Driving Mechanisms of the Digital Financial Network: Evidence from China

,

,

Abstract

:1. Introduction

2. Data and Methods

2.1. Data Source and Index System

2.1.1. Data Source

2.1.2. Index System

2.2. Research Methods

2.2.1. Geographic Detector

2.2.2. Modified Gravity Model

2.2.3. Social Network Analysis

2.2.4. Geographically and Temporally Weighted Regression

3. Analysis of Urban Digital Financial Network

3.1. Five Core Drivers Are Detected

3.2. Evolution of Urban Digital Financial Network

3.2.1. Connection Intensity Is at a Low Level, Showing a Multi-Polar Trend

3.2.2. Cities with Higher Betweenness Centrality Are Concentrated in the Megacities

3.2.3. Community Structure Shows a Stable State

3.2.4. Regions with the Greatest Possibility of Connection Are Located in the PRD and the YRD

3.3. Drivers of DF Development Vary by Region and Time

3.3.1. Model Feasibility

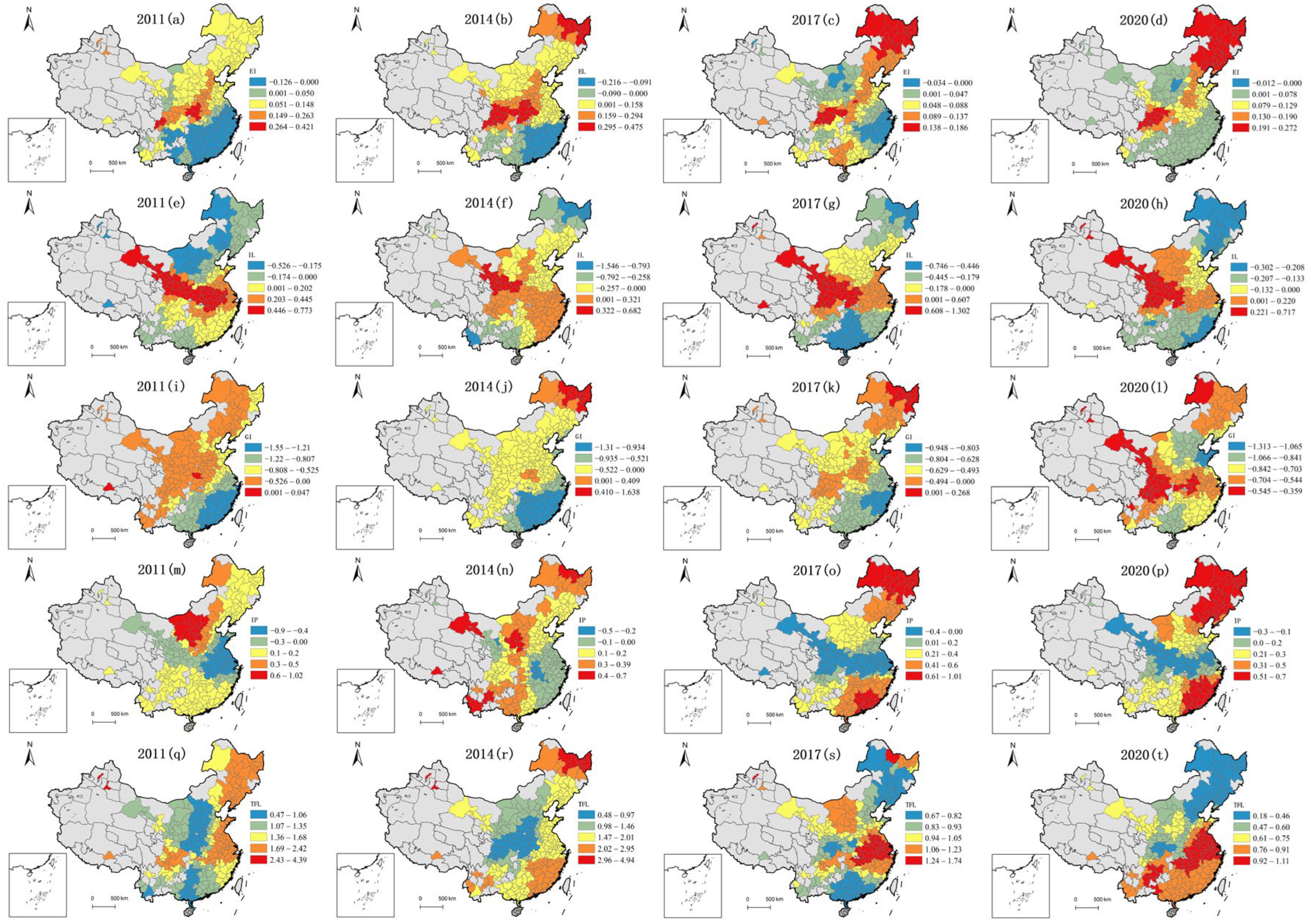

3.3.2. Spatiotemporal Differentiation of Driving Factors’ Influence

4. Discussion

4.1. Exploration of the Evolution of Urban DF Network

4.2. The Drivers Present Significant Spatial Heterogeneity over Time

5. Conclusions and Implications

5.1. Main Conclusions

5.2. Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Culpeper, R. The Role of the G20 in Enhancing Financial Inclusion; Heinrich Böll Stiftung (The Green Political Foundation) Publication: Berlin, Germany, 2012; pp. 1–22. [Google Scholar]

- Ozili, P.K. Impact of Digital Finance on Financial Inclusion and Stability. Borsa Istanb. Rev. 2018, 18, 329–340. [Google Scholar] [CrossRef]

- Guo, F.; Wang, J.; Wang, F.; Kong, T.; Zhang, X.; Cheng, Z. Measuring China’s Digital Financial Inclusion: Index Compilation and Spatial Characteristics. China Econ. Q. 2020, 19, 1401–1418. [Google Scholar] [CrossRef]

- Ren, B.; Li, L.; Zhao, H.; Zhou, Y. The Financial Exclusion in the Development of Digital Finance—A Study Based on Survey Data in the Jingjinji Rural Area. Singap. Econ. Rev. 2018, 63, 65–82. [Google Scholar] [CrossRef]

- Ozili, P.K. Financial Inclusion Research around the World: A Review. Forum Soc. Econ. 2021, 50, 457–479. [Google Scholar] [CrossRef]

- Mi, J.J.; Zhu, H. Can Funding Platforms’ Self-Initiated Financial Innovation Improve Credit Availability? Evidence from China’s P2P Market. Appl. Econ. Lett. 2017, 24, 396–398. [Google Scholar] [CrossRef]

- Rosavina, M.; Rahadi, R.A.; Kitri, M.L.; Nuraeni, S.; Mayangsari, L. P2P Lending Adoption by SMEs in Indonesia. Qual. Res. Financ. Mark. 2019, 11, 260–279. [Google Scholar] [CrossRef]

- Chen, S.; Zhang, H. Does Digital Finance Promote Manufacturing Servitization: Micro Evidence from China. Int. Rev. Econ. Financ. 2021, 76, 856–869. [Google Scholar] [CrossRef]

- Li, J.; Wu, Y.; Xiao, J.J. The Impact of Digital Finance on Household Consumption: Evidence from China. Econ. Model. 2020, 86, 317–326. [Google Scholar] [CrossRef]

- Li, X.; Shao, X.; Chang, T.; Albu, L.L. Does Digital Finance Promote the Green Innovation of China’s Listed Companies? Energy Econ. 2022, 114, 106254. [Google Scholar] [CrossRef]

- Liu, S.; Koster, S.; Chen, X. Digital Divide or Dividend? The Impact of Digital Finance on the Migrants’ Entrepreneurship in Less Developed Regions of China. Cities 2022, 131, 103896. [Google Scholar] [CrossRef]

- Wang, Q.; Yang, J.; Chiu, Y.; Lin, T.-Y. The Impact of Digital Finance on Financial Efficiency. Manag. Decis. Econ. 2020, 41, 1225–1236. [Google Scholar] [CrossRef]

- Xue, Q.; Feng, S.; Chen, K.; Li, M. Impact of Digital Finance on Regional Carbon Emissions: An Empirical Study of Sustainable Development in China. Sustainability 2022, 14, 8340. [Google Scholar] [CrossRef]

- Liang, M. Research on the Impact of Chinese Digital Inclusive Finance on Industrial Structure Upgrade—Based on Spatial Dubin Model. Open J. Stat. 2020, 10, 863. [Google Scholar] [CrossRef]

- Guo, H.; Gu, F.; Peng, Y.; Deng, X.; Guo, L. Does Digital Inclusive Finance Effectively Promote Agricultural Green Development?—A Case Study of China. Int. J. Environ. Res. Public Health 2022, 19, 6982. [Google Scholar] [CrossRef] [PubMed]

- Lv, C.; Song, J.; Lee, C.-C. Can Digital Finance Narrow the Regional Disparities in the Quality of Economic Growth? Evidence from China. Econ. Anal. Policy 2022, 76, 502–521. [Google Scholar] [CrossRef]

- Qiu, J.; Chen, W.; Tao, R.; Wang, C. The Temporal and Spatial Evolution of Digital Inclusive Finance and Its Boosting Effect on Rural Revitalization in China. Preprints 2022, 2022070274. [Google Scholar] [CrossRef]

- Liao, G.; Li, Z.; Wang, M.; Albitar, K. Measuring China’s urban digital finance. Quant. Financ. Econ. 2022, 6, 385–404. [Google Scholar] [CrossRef]

- Ye, C.; Sun, C.; Chen, L. New Evidence for the Impact of Financial Agglomeration on Urbanization from a Spatial Econometrics Analysis. J. Clean. Prod. 2018, 200, 65–73. [Google Scholar] [CrossRef]

- Zhao, Y.; Zhang, G.; Zhao, H. Spatial Network Structures of Urban Agglomeration Based on the Improved Gravity Model: A Case Study in China’s Two Urban Agglomerations. Complexity 2021, 2021, 6651444. [Google Scholar] [CrossRef]

- Liu, X.; Zhu, J.; Guo, J.; Cui, C. Spatial association and explanation of China’s digital financial inclusion development based on the network analysis method. Complexity 2021, 2021, 6649894. [Google Scholar] [CrossRef]

- Schweitzer, F.; Fagiolo, G.; Sornette, D.; Vega-Redondo, F.; Vespignani, A.; White, D.R. Economic Networks: The New Challenges. Science 2009, 325, 422–425. [Google Scholar] [CrossRef]

- Hautsch, N.; Schaumburg, J.; Schienle, M. Financial Network Systemic Risk Contributions. Rev. Financ. 2015, 19, 685–738. [Google Scholar] [CrossRef]

- Battiston, S.; Farmer, J.D.; Flache, A.; Garlaschelli, D.; Haldane, A.G.; Heesterbeek, H.; Hommes, C.; Jaeger, C.; May, R.; Scheffer, M. Complexity Theory and Financial Regulation. Science 2016, 351, 818–819. [Google Scholar] [CrossRef]

- Bardoscia, M.; Barucca, P.; Battiston, S.; Caccioli, F.; Cimini, G.; Garlaschelli, D.; Saracco, F.; Squartini, T.; Caldarelli, G. The Physics of Financial Networks. Nat. Rev. Phys. 2021, 3, 490–507. [Google Scholar] [CrossRef]

- Chu, A.M.; Chan, L.S.; So, M.K. Stochastic Actor-oriented Modelling of the Impact of COVID-19 on Financial Network Evolution. Stat 2021, 10, e408. [Google Scholar] [CrossRef] [PubMed]

- Zhang, W.; Zhuang, X.; Li, Y. Dynamic Evolution Process of Financial Impact Path under the Multidimensional Spatial Effect Based on G20 Financial Network. Phys. Stat. Mech. Its Appl. 2019, 532, 121876. [Google Scholar] [CrossRef]

- Samitas, A.; Kampouris, E.; Polyzos, S. Covid-19 Pandemic and Spillover Effects in Stock Markets: A Financial Network Approach. Int. Rev. Financ. Anal. 2022, 80, 102005. [Google Scholar] [CrossRef]

- Markose, S.; Giansante, S.; Shaghaghi, A.R. ‘Too Interconnected to Fail’Financial Network of US CDS Market: Topological Fragility and Systemic Risk. J. Econ. Behav. Organ. 2012, 83, 627–646. [Google Scholar] [CrossRef]

- Chinazzi, M.; Fagiolo, G.; Reyes, J.A.; Schiavo, S. Post-Mortem Examination of the International Financial Network. J. Econ. Dyn. Control 2013, 37, 1692–1713. [Google Scholar] [CrossRef]

- Huang, Y.; Hong, T.; Ma, T. Urban Network Externalities, Agglomeration Economies and Urban Economic Growth. Cities 2020, 107, 102882. [Google Scholar] [CrossRef]

- Anderson, J.E. The Gravity Model. Annu. Rev. Econ. 2011, 3, 133–160. [Google Scholar] [CrossRef]

- Fan, Y.; Zhang, S.; He, Z.; He, B.; Yu, H.; Ye, X.; Yang, H.; Zhang, X.; Chi, Z. Spatial Pattern and Evolution of Urban System Based on Gravity Model and Whole Network Analysis in the Huaihe River Basin of China. Discret. Dyn. Nat. Soc. 2018, 2018, 3698071. [Google Scholar] [CrossRef]

- Chen, Y.; Nie, B.; Huang, Z.; Zhang, C. Spatial relevancy of digital finance in the urban agglomeration of Pearl River Delta and the influence factors. Electron. Res. Arch. 2023, 31, 4378–4405. [Google Scholar] [CrossRef]

- Li, J.; Ye, S.; Wang, S. Spatial Network Analysis on the Coupling Coordination of Digital Finance and Technological Innovation. Sustainability 2023, 15, 6354. [Google Scholar] [CrossRef]

- Huang, R.; Kale, S.; Paramati, S.R.; Taghizadeh-Hesary, F. The Nexus between Financial Inclusion and Economic Development: Comparison of Old and New EU Member Countries. Econ. Anal. Policy 2021, 69, 1–15. [Google Scholar] [CrossRef]

- Shen, Y.; Hu, W.; Hueng, C.J. Digital Financial Inclusion and Economic Growth: A Cross-Country Study. Procedia Comput. Sci. 2021, 187, 218–223. [Google Scholar] [CrossRef]

- Ren, X.; Zeng, G.; Gozgor, G. How Does Digital Finance Affect Industrial Structure Upgrading? Evidence from Chinese Prefecture-Level Cities. J. Environ. Manag. 2023, 330, 117125. [Google Scholar] [CrossRef]

- Hasan, M.M.; Yajuan, L.; Khan, S. Promoting China’s Inclusive Finance through Digital Financial Services. Glob. Bus. Rev. 2022, 23, 984–1006. [Google Scholar] [CrossRef]

- Quinn, D.; Schindler, M.; Toyoda, A.M. Assessing Measures of Financial Openness and Integration. IMF Econ. Rev. 2011, 59, 488–522. [Google Scholar] [CrossRef]

- Thathsarani, U.S.; Wei, J.; Samaraweera, G. Financial Inclusion’s Role in Economic Growth and Human Capital in South Asia: An Econometric Approach. Sustainability 2021, 13, 4303. [Google Scholar] [CrossRef]

- Tram, T.X.H.; Lai, T.D.; Nguyen, T.T.H. Constructing a Composite Financial Inclusion Index for Developing Economies. Q. Rev. Econ. Financ. 2023, 87, 257–265. [Google Scholar] [CrossRef]

- Kanungo, R.P.; Gupta, S. Financial Inclusion through Digitalisation of Services for Well-Being. Technol. Forecast. Soc. Change 2021, 167, 120721. [Google Scholar] [CrossRef]

- Jiang, Z.; Ma, G.; Zhu, W. Research on the Impact of Digital Finance on the Innovation Performance of Enterprises. Eur. J. Innov. Manag. 2022, 25, 804–820. [Google Scholar] [CrossRef]

- Cao, S.; Nie, L.; Sun, H.; Sun, W.; Taghizadeh-Hesary, F. Digital Finance, Green Technological Innovation and Energy-Environmental Performance: Evidence from China’s Regional Economies. J. Clean. Prod. 2021, 327, 129458. [Google Scholar] [CrossRef]

- Morgan, P.J.; Huang, B.; Trinh, L.Q. The Need to Promote Digital Financial Literacy for the Digital Age. In The Future of Work and Education for the Digital Age; G20 Insights; ADBI Press: Tokyo, Japan, 2019; pp. 36–52. [Google Scholar]

- Chai, D.; Du, J.; Yu, Z.; Zhang, D. City Network Mining in China’s Yangtze River Economic Belt Based on “Two-Way Time Distance” Modified Gravity Model and Social Network Analysis. Front. Phys. 2022, 10, 1018993. [Google Scholar] [CrossRef]

- Duan, Q.; Tan, M. Using a Geographical Detector to Identify the Key Factors That Influence Urban Forest Spatial Differences within China. Urban For. Urban Green. 2020, 49, 126623. [Google Scholar] [CrossRef]

- Newman, M.E. Equivalence between Modularity Optimization and Maximum Likelihood Methods for Community Detection. Phys. Rev. E 2016, 94, 052315. [Google Scholar] [CrossRef] [PubMed]

- Fotheringham, A.S.; Crespo, R.; Yao, J. Geographical and Temporal Weighted Regression (GTWR). Geogr. Anal. 2015, 47, 431–452. [Google Scholar] [CrossRef]

- Chu, H.; Ning, Y.; Qie, X. Measurement and Spatial Correlation Analysis of the Development Level of the Digital Economy in the Yangtze River Delta Urban Agglomeration. Sustainability 2023, 15, 13329. [Google Scholar] [CrossRef]

- Zeng, C.; Liu, Y.; Stein, A.; Jiao, L. Characterization and spatial modeling of urban sprawl in the Wuhan Metropolitan Area, China. Int. J. Appl. Earth Obs. Geoinf. 2015, 34, 10–24. [Google Scholar] [CrossRef]

- Peng, X.; Luo, X.; Li, J. Meaning construction and judicial identification: Difficulties and countermeasures of criminal regulation of illegal fundraising behavior on online P2P lending platforms. Int. J. Leg. Discourse 2019, 4, 47–68. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| First-Level Index | Second-Level Index | Calculation Method | Reference |

|---|---|---|---|

| Inclusive level | Digital financial inclusion | China’s Digital Financial Inclusion Index | [3,21] |

| Economic quality | Economic level | Per capita GDP | [21,34,36,37] |

| Industrial structure | Added value of tertiary industry/GDP | [14,21,38] | |

| Traditional financial level | Per capita loans | [34,39] | |

| Opening-up level | Actual utilization of foreign capital | [34,40] | |

| City scale | Demographic information | Population at the end of the year | [41,42] |

| Internet popularity | Number of Internet users | [21,34,43] | |

| Development potential | Innovation level | Number of patents granted | [44,45] |

| Education level | Number of students in colleges and middle schools | [34,46] | |

| Government intervention | Government fiscal expenditure/GDP | [7,18] |

| First-Level Index | Second-Level Index | Calculation Method | q2011 | q2014 | q2017 | q2020 |

|---|---|---|---|---|---|---|

| Economic quality | Economic level | Per capita GDP | 0.4697 | 0.5541 | 0.5101 | 0.5650 |

| Industrial structure | Added value of tertiary industry/GDP | 0.1935 | 0.2625 | 0.2101 | 0.1922 | |

| Traditional financial level | Per capita loans | 0.4286 | 0.4826 | 0.5364 | 0.5208 | |

| Opening-up level | Actual utilization of foreign capital | 0.3811 | 0.4222 | 0.3460 | 0.3271 | |

| City scale | Demographic information | Population at the end of the year | 0.0538 | 0.0327 | 0.0782 | 0.1370 |

| Internet popularity | Number of Internet users | 0.3783 | 0.2994 | 0.3488 | 0.4801 | |

| Development potential | Innovation level | Number of patents granted | 0.3959 | 0.4237 | 0.4659 | 0.5523 |

| Education level | Number of students in colleges and middle schools | 0.1664 | 0.1831 | 0.1934 | 0.2685 | |

| Government intervention | Government fiscal expenditure/GDP | 0.3621 | 0.3021 | 0.3890 | 0.5001 |

| First-Level Index | Second-Level Index | Calculation Method |

|---|---|---|

| Inclusive level | Digital financial inclusion | China’s Digital Financial Inclusion Index |

| Economic quality City scale | Economic level | Per capita GDP |

| Traditional financial level | Per capita loans | |

| Internet popularity | Number of Internet users | |

| Development potential | Innovation level | Number of patents granted |

| Government intervention | Government fiscal expenditure/GDP |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ding, R.; Shen, S.; Zhu, Y.; Du, L.; Chen, S.; Liang, J.; Wang, K.; Xiao, W.; Hong, Y. Evolution, Forecasting, and Driving Mechanisms of the Digital Financial Network: Evidence from China. Sustainability 2023, 15, 16072. https://doi.org/10.3390/su152216072

Ding R, Shen S, Zhu Y, Du L, Chen S, Liang J, Wang K, Xiao W, Hong Y. Evolution, Forecasting, and Driving Mechanisms of the Digital Financial Network: Evidence from China. Sustainability. 2023; 15(22):16072. https://doi.org/10.3390/su152216072

Chicago/Turabian StyleDing, Rui, Siwei Shen, Yuqi Zhu, Linyu Du, Shihui Chen, Juan Liang, Kexing Wang, Wenqian Xiao, and Yuxuan Hong. 2023. "Evolution, Forecasting, and Driving Mechanisms of the Digital Financial Network: Evidence from China" Sustainability 15, no. 22: 16072. https://doi.org/10.3390/su152216072

APA StyleDing, R., Shen, S., Zhu, Y., Du, L., Chen, S., Liang, J., Wang, K., Xiao, W., & Hong, Y. (2023). Evolution, Forecasting, and Driving Mechanisms of the Digital Financial Network: Evidence from China. Sustainability, 15(22), 16072. https://doi.org/10.3390/su152216072