1. Introduction

Since the 1990s, the public-private partnership (PPP) has been widely used by many countries to deliver public infrastructure and services and to implement redevelopment processes. PPP takes into account (i) the limited financial resources in public entities balance able to bear the entire costs assessed for the realization and the management of these initiatives and (ii) the frequent inadequate managerial skills of public subjects [

1,

2,

3].

In this regard, the containment of budget limits and the rule system aimed at monitoring public funds, in fact, represents the main obstacle for the investment policies of public administrations for sustainable territorial development [

4].

However, for the period 2009–2019, the European PPP Expertise Centre—EPEC—has pointed out a declining trend in the European PPP market both in terms of the project numbers and of investment value: only in 2019, in fact, the market has decreased 31% in value terms and 24% in transactions number terms compared to the previous year. Nevertheless, in 2018, an increase of average investment value (375 million euro compared to 345 million euro in 2017 and 174 million euro in 2016) was revealed, although there has been an overall reduction of the number of projects carried out through public-private cooperation equal to—11% compared to 2017. In the same period (2009–2019), it was observed that the United Kingdom was characterized by the most active PPP market, with 1032 concluded contracts and 160 billion euro, followed by France (183 contracts and 38.5 billion euro) and Spain (161 contracts and 35.2 billion euro) [

5].

In this context, the European Court of Auditors has highlighted that, despite PPPs having the potential to ensure faster infrastructures intervention implementation and good management policies, these projects have not always been effectively carried out, by not guarantying an adequate balance of benefits and costs. Therefore, the assessed potential benefits of PPPs do often not concretize, for delays, cost increases, and underutilization, by resulting in 1.5 billion euro of inefficient and ineffective spending, of which 0.4 billion are EU funds. This has been mainly due to the inadequacy of the analysis developed in the initiative first phases, of the strategies for the use of PPPs and of the institutional and regulatory frameworks [

6]. It is evident, in fact, that a consolidated experience and expertise in the successful implementation of PPP investments is fundamental for projects completion, by avoiding a higher EU funds use—in the case of so-called PPP with mixed financing—or—in extreme situations—the works interruption.

Thus, the relevance, the high costs, and the long term of PPP procedures require specific skills to assess the future outputs deriving from the project construction and management: the preliminary analysis is very often based on excessively optimistic scenarios related to the expected reference market demand and to the planned infrastructures use. Furthermore, the risk sharing between public and private partners is usually inconsistent, by leading to significant delays and assessed cost overrun.

With reference to a specific intervention to be carried out through the PPP operational tool in an Italian small town, the present research intends to be a valuable methodological study in order to illustrate precisely the different steps to develop for the verification of the convenience of this modality in enhancement and redevelopment interventions.

Focusing on the current Italian context, the economic and social effects caused by the COVID-19 pandemic have been determining the necessity to define the essential measures in the short and medium period in order to promote a revival phase for the public investments. Among the ten strategic actions identified by the National Builders Association (ANCE) for the country recovery, the urban redevelopment represents one of the main sectors in which to invest [

7]. The recovery fund, in fact, could become a fundamental vehicle for boosting urban renovation programs aimed to stimulate (i) the small towns growth, avoiding their depopulation, (ii) the medium and big cities peripheries rehabilitation and inclusion, (iii) the transformation of disused urban areas through local services and new job opportunities activation. In this sense, in the medium-large cities and metropolitan areas, the redevelopment initiatives are very often most attractive for private investors in monetary profit terms compared to those in the small towns. The first, in fact, are usually characterized by high investment costs and corresponding risks, as they constitute radical transformation operations of abandoned public properties or degraded urban areas, but also by potential high revenues. On the other hand, instead, in the small towns, scaled down recovery interventions are more frequent, according to the geographical context extension, for which investment costs, management risks, and revenues for potential investors are lower.

In the Italian legal context, section IV of the public works regulation (Legislative Decree No. 50/2016) specifies the PPP definition through the identification of their main characteristics and contractual typologies. The private investors take part in initiatives aimed at renovation or realization of public infrastructures, properties or areas exclusively on the condition that the financial balance of the initiative is positive, i.e., the profit deriving from the cash flows related to the intervention is higher than the zero value [

8]. With reference to the Italian regulation, the private subject can obtain the full management of the redeveloped property or urban area and, furthermore, can receive a public contribution in order to achieve the financial balance of the initiative. This monetary amount was initially set equal to the maximum limit of 30% of the total investment cost of the PPP initiative, including any financial charges. The Legislative Decree No. 56/2017 has increased this contribution until the 49% both for the concession initiatives (article 165 paragraph 2 Legislative Decree No. 50/2016) and for the PPPs (article 180 paragraph 6 Legislative Decree No. 50/2016). The growth of the maximum threshold of the public contribution allows the PPP procedure to be more implemented and the effective use of these cooperation forms, also taking into account the recovery fund to be applied for urban renovation projects.

In order to evaluate the costs to be considered in the public budget associated with an urban transformation initiative, it is necessary to refer to the classification of the projects according to the ability to self-finance through cash flows. In particular: (i) projects without public contributions, i.e., PPP projects in which revenues allow the private subject to fully recover investment costs and to obtain a monetary surplus, (ii) projects in which a public contribution is envisaged, i.e., PPP interventions for which it is necessary to implement a case-by-case assessment for the definition of the public financial sharing, guarantees, or the risks transfer [

9].

In this sense, the economic and financial plan specifies the basic assumptions that determine the financial balance of investment and management for the entire analysis period [

10]. Therefore, it constitutes a fundamental tool able to assess the project profitability. It justifies the amount fees, costs, and revenues and, eventually, the need for public contributions to cover the intervention realization and operational phase’s costs. In fact, as already mentioned, the public entity can pay a monetary amount if the private subject is imposed to apply selling prices lower than those corresponding to investment remuneration, e.g., in social housing projects, to ensure the economic and financial balance of intervention (article 143 Legislative Decree No. 163/2006—repealed—and article 165, paragraph 2 Legislative Decree No. 50/2016).

From a strictly financial point of view, it is possible to assess the congruity of the value of the public contribution by using techniques for forecasting capital needs, i.e., capital budgeting [

11]. Taking into account that the main goal of the public fee is to ensure the economic and financial feasibility of investment and related management, the application of these techniques leads to verify the bankability and profitability of the project by identifying possible critical points. It should be highlighted that the public monetary contribution during the intervention construction phase reduces the private capital to be used and to be borrowed by mortgage. On the other hand, in the management phase, the financial sharing determines an increase of the annual cash flow, thus allowing a higher and faster coverage of the overall financial capital and achieving a monetary surplus.

2. Aim

With reference to PPP operational tools, the present research aims to point out the relevant role played by public administration in these procedures implementation in order to determine the economic and financial balance of investments for the private investors. For this purpose, the public subject can contribute to make the financial initiative convenient through a periodic fee to be paid to the private investor during the analysis period.

In the present study, the feasibility of a redevelopment initiative of a public property asset related to a redevelopment intervention of a building located in the small town of Cesano Romano (Italy) and carried out through PPP operational tool, is analyzed.

Focusing on the verification of the intervention feasibility from the private point of view developed through the discounted cash-flow analysis (DCFA), in the first step of the research, the financial sustainability is examined, taking into account the revenues deriving exclusively from the management of the activities planned (situation 1—no public monetary participation).

Due to the financial convenience absence verified in situation 1, in the second step of the research, the public contribution is included among the revenue items (situation 2—public monetary participation). This monetary amount is determined in order (i) to ensure the financial sustainability of the initiative for the private subject and, at the same time, (ii) to comply with the regulatory constraints imposed by the Italian Decree No. 50/2016, article 180, according to which the actualized total amount of the periodic fees must be lower than 49% of the sum of investment costs and financial charges.

In particular, taking into account the disposition provided by the Italian Law, the total investment cost is determined borrowing the financial mathematics logic, i.e., calculating the actualized total amount of investment costs, including financial charges. This operation is carried out considering a public actualization rate, equal to the current net rate of return on 20 years government bond [

12]. Furthermore, in the research, a sensitivity analysis on the results obtained is performed, in order to study the variations of public subject financial sharing, considering different likely situations and to provide for a wide range of different scenarios in terms of amount of the public contribution, able to support both public and private sectors in the bargaining phases.

The research is divided into five sections. In

Section 3, the main background on PPP procedures with reference to the risks to the subjects involved in these initiatives is reported. In

Section 4, the main features of DCFA are recalled in order to outline the relevance of the project’s initial assumptions definition that could vary if the analysis outputs are negative in terms of the financial convenience for the private investor. In

Section 5, the case study is illustrated: after having described the current state of the building and the redevelopment project, the investment and management costs, the revenues and the cash flows in situation 1—

no public monetary participation—are assessed and schematized. Moreover, the main performance indicators are determined to verify the financial feasibility of the initiative. In

Section 6, situation 2—

public monetary participation—is introduced and a periodic fee paid by the public subject to the private one is determined, in order to ensure the sustainability of the outputs, in terms of positive financial balance of the initiative and compliance with the regulatory constraints. Finally, in

Section 7, the conclusions of the work are drawn.

3. Background

In the existing literature related to the analysis of the PPP operational tools for urban redevelopment interventions, many contributions aimed at defining the risks for the economic investors are included [

13,

14,

15,

16,

17,

18,

19,

20].

Several authors have defined the public-private cooperation forms as a significant means of project financing and management [

21,

22,

23,

24]. In the last decades, in fact, the main reasons behind the application of PPPs concern (i) the limited financial resources of the public sector; (ii) the growing requirement for infrastructures or public services; (iii) the need to improve the urban quality through recovery interventions [

25,

26,

27,

28,

29,

30]. A sustainability-oriented PPP framework, in fact, emphasizes this mechanism as a tool for urban governance to achieve feasible development goals in the context of public scarce financial resources and, at the same time, of the strong need of infrastructures, urban areas and public properties renovations [

31]. During the implementation of the procedures based on the collaboration between public and private sectors, the clear definition of the government/public entities responsibilities constitutes a critical factor for their success [

32].

The continuing spread of private sector involvement—especially its financial human resources—in the process of public service provision, attests the fundamental role assumed by PPP for the territorial development [

33,

34,

35]. In particular, the public sector delegates the collective services realization, the existing property asset enhancement, the degraded urban areas renovation which require large investment in monetary terms, and the associated risks to the private investor [

36,

37,

38,

39,

40,

41,

42]. Furthermore, the PPP-based projects, ensuring the managerial experience of the private sector, allow to implement them quicker and with higher quality [

43,

44].

In the last years, the application of PPPs has become especially attractive during the economic crisis and, in fact, the procedural model has been widely used in many countries [

45,

46]. In several cases, a high complexity characterizes the PPP projects, mainly due to their huge scale, large investment, and long-term relationships among different participants—very often with conflictual interests—leading to difficulty in managing performance risk.

Many PPP projects are frequently unsuccessful in achieving quality, meeting deadlines, and respecting budgets fixed in the preliminary phases. Moreover, most of them have been exposed to various risks [

18] due to the increased uncertainties during the prolonged contract periods of PPP projects [

47]. It is evident that a thorough risk assessment [

48] and an effective risk allocation [

49] can reduce the implementation costs [

50,

51].

The assessment of the potential risks of infrastructure projects in their various contractual stages throughout the life cycle of the project is necessary to avoid the negative impacts that may lead to the failure of this type of projects. In particular, risks can be defined as circumstances from the perspective of parties that have a negative impact on their goals that they expect to achieve from the project [

52].

In the context of the construction industry, the risk management process of PPP concerns its identification [

53], assessment (financial, political, environmental, and revenue), allocation, and strategies [

54,

55,

56].

Grimsey and Lewis [

57] have analyzed the risks of PPP arrangements from the perspectives of the various parties. The contractual relations between the subjects in infrastructure projects involve the mechanisms of distributing risks during different phases of the project. Through the analytical hierarchy process (AHP), the weights resulting from the probability of occurrence of such risks can be assigned, in order to ensure projects’ success in achieving the concept of sustainable development and its economic, social, and environmental aspects [

58].

The multi-attribute decision-making (MADM) techniques in PPP projects have been explored by Valipour et al. [

59] in order to support the parties (i) to select the best risk assessment method, (ii) to reduce the costs associated to the risks, (iii) to identify the most relevant uncertainties, and (iv) to ensure successful in risk management [

60].

The risks identified by several authors mainly concern the limited capital, an improper design, the variation in the value of land plots due to inflation, the termination of concession by the public subject, the delay in resolving a contractual dispute, an inadequate investigation, and insufficient data [

61,

62]. For example, Nguyen et al. [

63] investigated critical risks affecting the financial viability of PPP toll road projects in Vietnam. They grouped risks into the four main categories: construction cost-related risks, operating revenue-related risks, operational and maintenance cost-related risks, and financing cost-related risks. Hande and Zeynep [

64] presented a PPP airport project to identify the effect of stakeholder associated risks to the success of mega-engineering projects.

In the context of China, Chan et al. [

32] defined a fair risk allocation mechanism between the different sectors as fundamental for the successful implementation of PPP projects, having to be distributed to that who prefers to undertake risks. Furthermore, the authors aimed to identify and assess the main risks for the PPP initiatives implementation in order to allocate them in a proper modality between private investors and public subjects: They identified three fundamental risk factors in PPP projects—i.e., government intervention, government corruption, and poor public decision-making processes—and found the inefficient legislative and supervisory systems of the Chinese government as one of the main obstacles to the success of PPP projects in the specific geographical area of China. In the same territorial context, nine case studies were examined to explore the critical risks influencing the success of PPP water projects to analyze the risk origin and their allocation mechanism [

65]. The downfall of product or service performance, the functional problems, the decrease in profitability, and low possibility of refinancing are the main potential dimensions of residual value risk factors defined by Yuan et al. [

66,

67,

68] in the risk management in China PPP projects. Integration between design and construction phases and excessive design variation are considered by Aladag and Isik [

69] as the key factors in PPP transportation projects.

With reference to motorway PPP projects, the analysis carried out by Carbonara et al. [

70] concerns providing the empirical-based guidelines for the risk management for both public and private entities, identifying for them both the effective distribution and the suitable mitigation strategies. Iyer and Sagheer [

71] pointed out that the initiative success depends on the efficient risks transfer to the sector that can best manage them. In particular, the authors suggested the use of interpretative structural modeling (ISM) to prepare a hierarchical structure as well as the interrelationships of these risks that would enable decision makers to take appropriate steps. In the Indian infrastructure sector, seventeen risks during the development phase of PPP interventions were selected, identifying fourteen weak factors, i.e., the delay in financial terms, the risk of costs, or time overruns are related to other risk components.

By developing an integrated risk management system (IRMS), Kumaraswamy et al. [

72] demonstrated that particular project requirements can be met, such as reducing complexity, establishing risk awareness, covering the different perspectives of the subjects involved, defining a common understanding of the nature of risks and opportunity, by providing detailed instructions in an emergency and improving the information data available.

In the Italian legislative context, the system for the risk assignment in the PPP initiatives is investigated in Art. 3 paragraph 1 and Art. 180 paragraph 3 of Legislative Decree No. 50/2016. In particular, in the PPP contracts, the transfer of risk to the economic operator involves the allocation of (i) operative risk, i.e., associated to the management of works or services from the demand or the supply side or both points of view, (ii) construction risk, i.e., related to delay in delivery times, non-compliance with project standards, increased costs, technical problems, and failure to finish the planned work, (iii) availability risk, i.e., linked to the ability, on the part of the concessionaire, to provide the agreed contractual services, both in terms of volume and expected quality standards, (iv) risk of demand for the services provided for, in cases of profitable activities, associated to the lack of users and therefore of cash flows. It should be highlighted, in fact, that the satisfaction of the financial criterion of the initiative, i.e., its capacity to remunerate the capital initially invested and to generate an adequate profit for the private investor, is the fundamental condition for the private subject participation in a PPP intervention. Thus, the private entrepreneur will decide to invest his capital and bear the initiative risks only in the situation in which the feasibility assessment attests that the revenues will be higher than the transformation and management costs, including the expected profit.

However, in the framework set out, there are also risks arising both from conditions not attributable to the economic operator and not foreseeable, i.e., sudden market demand variations or external events related, for example, to deep economic crisis periods.

4. The Implementation of DCFA

The PPP initiatives concern public works realization able to synergistically combine technical, financial, and managerial skills of public and private subjects and to involve monetary investments by private entrepreneurs in order to obtain a profit deriving from the use or the selling of planned services.

The financial sustainability of an investment is usually verified by developing a DCFA. The main steps of its implementation include: (i) the investment and management cost assessment e.g., completion, transaction, and financing costs; (ii) the revenue assessment; (iii) the calculation of the cash-flows generated during the analysis period for the private subject; (iv) the determination of the performance indicators (net present value (NPV), internal rate of return (IRR), and discounted payback period (PbP)) in order to verify the convenience of the initiative. In particular, a higher zero value of the NPV immediately confirms the investment financial convenience, whereas the IRR and the PbP must be compared with “threshold” values [

73].

With reference to the project to be analyzed, firstly, the analysis period, i.e., the time in which the private bears the costs of the initiative and obtains the revenues deriving from the management or the selling of the built/redeveloped property/urban area, is set. Furthermore, the minimum annual return rate expected by the private investor is determined taking into account the risks of similar initiatives in the reference market.

In the early phase of the analysis, it is necessary to define the project’s initial assumptions, i.e., the costs and the revenues nature for the private investor and the role played by the public administration during the entire analysis period. In this sense, the revenue items could result from (i) the direct management of the renovated property/urban area, (ii) the selling of the buildings, (iii) the free ownership transfer of a building land plot, to be transformed in properties to sell/rent, (iv) the periodic fee paid by the public administration to the private subject.

In this sense, it should be highlighted that the economic contribution could be fundamental to the financial convenience of the operation from the private point of view. This monetary amount, in fact, could allow, on the one hand, the private subject to ensure the financial balance of the initiative, by obtaining the profit after the project realization. On the other hand, the public entities do not excessively burden their economic balance sheets, by distributing the fees over the time period considered.

In the present research, a redevelopment initiative carried out by the PPP procedure is analyzed, hypothesizing firstly, situation 1—no public monetary participation—related to the direct—i.e., private investor—property management for thirty years. Then, after having verified the absence of financial convenience for the investor in situation 1, a periodic fee paid by the public subject is included among the revenue items—situation 2 public monetary participation. This contribution is able to define the convenience threshold of the private balance sheet and to comply with the regulatory constraints imposed by the Italian Legislative Decree No. 50/2016 (article 180, paragraph 6).

The preliminary analysis of the financial feasibility of the intervention, as it is known, constitutes a fundamental phase for the concrete implementation of a PPP. The strategies that can be applied by the private subject to achieve the financial sustainability are several, e.g., decreasing the investment costs, acting on the raw materials quality to be used or on the surfaces extension to be realized, reducing the management costs by extending the time intervals between scheduled maintenance interventions or neglecting adequate ordinary maintenance, raising revenues, increasing the selling prices and/or rental fees.

Each of these possible strategies may not be successful, as they are not in line with the standards envisaged by the project (in the case of a lower project quality level than standard one) or with the spending power of potential buyers (in the case of a strong increase in selling prices).

5. Case Study: The Castle of Cesano Romano

5.1. Description of the Current State

The case study concerns the redevelopment initiative of a disused building—commonly known as a “castle”—located in the small town of Cesano Romano, in the fifty-second area of the city of Rome (Italy) and close to the border with the municipalities of Anguillara Sabazia, Campagnano of Rome, and Formello. The medieval town of Cesano Romano is situated on a promontory at 240 m above sea level and it is 24 km north of the historical center of the city of Rome and in the Agro Romano hearticle. A portion of the Cesano Romano municipal territory is included in the regional natural park of the Bracciano-Martignano complex, sharing a border with the Veio regional park in the east side.

Figure 1 shows the location of the small town of Cesano Romano in the context of the metropolitan city of Rome.

The castle (

Figure 2) is located on the top of the promontory and overlooks the main square of the city. The building was rebuilt between the end of the 19th century and the beginning of the 20th century on previous tufa blocks of medieval age. The current castle with a central clock tower and cornices characterized by fortresses battlements, dates back to 1908, and from 1922 to 1969 was used for charitable activities, i.e., kindergarten for indigent children or sewing school. The complex is owned by a Public Institution of Assistance and Charity.

The high façades overlooking the square are embellished by a central prothyrum on the ground floor, i.e., a building portion with two columns leaning against the central arch, and by the World War memorial at the right edge (

Figure 3). The castle is built in load-bearing masonry and develops on three levels. The trapezoidal in the shape plan has a central stairwell of 32 m

2, whereas the three rooms occupy a surface area of respectively 48 m

2, 28 m

2, and 27 m

2. Finally, the building parts added on the south and eastern facades extend for 18 m

2 and 14 m

2, for a total area of 167 m

2.

5.2. The Redevelopment Project

The redevelopment intervention concerns the functional reconversion of the Cesano Romano castle into a nursing home for care-dependent persons to be used for a variable period (from a few weeks to indefinitely). According to the Italian legislation (Guideline Ministry of Health on nursing home n. 106/1994), this facility typology must provide guests (i) residential home-like accommodation, while stimulating socialization among guests; (ii) all medical interventions, nursing, and rehabilitation needed to prevent and treat chronic diseases and their possible exacerbations; (iii) personalized assistance, geared to the protection and improvement of the levels of autonomy, to the maintenance of personal interests and the promotion of wellness.

In the context of the Recovery Plan after the global Covid-19 pandemic and, in particular, of the EU4Health program for the 2021–2027 period for the improvement of the European citizens’ health, the strengthening health sector’s resilience and the encouragement of the health sector innovation, the function planned for the case study analyzed is in line with the strategy’s main goals. In particular, in order to optimize the functioning and performance of EU health systems, the European Commission has proposed to invest € 9.4 billion in public health through specific actions for disease prevention and the improvement in access to health care for elder people [

6]. Furthermore, it should be highlighted that partnerships between the public and private sector in scaling up health service delivery are currently being discussed in many countries [

74], as there are several possible financing modalities in such partnerships. In particular, the public sector plays a stewardship or regulatory role without financing private sector provision or the participation of the private sector in government-subsidized risk-pooling mechanisms for the poorest people [

45].

Moreover, with reference to the case study considered in the present analysis, the intervention aimed at the functional transformation of the castle into a nursing home meets the need to fill the lack of a facility for semi-self-sufficient elderly people in the specific urban territory. This takes into account that the percentage of potential users reaches almost a quarter of the Cesano Romano population—22% of total inhabitants number of Cesano Romano [

75].

Then, in the geographical territory of Cesano Romano, the analysis of the competitors indicates a total absence of a similar building intended for a nursing home.

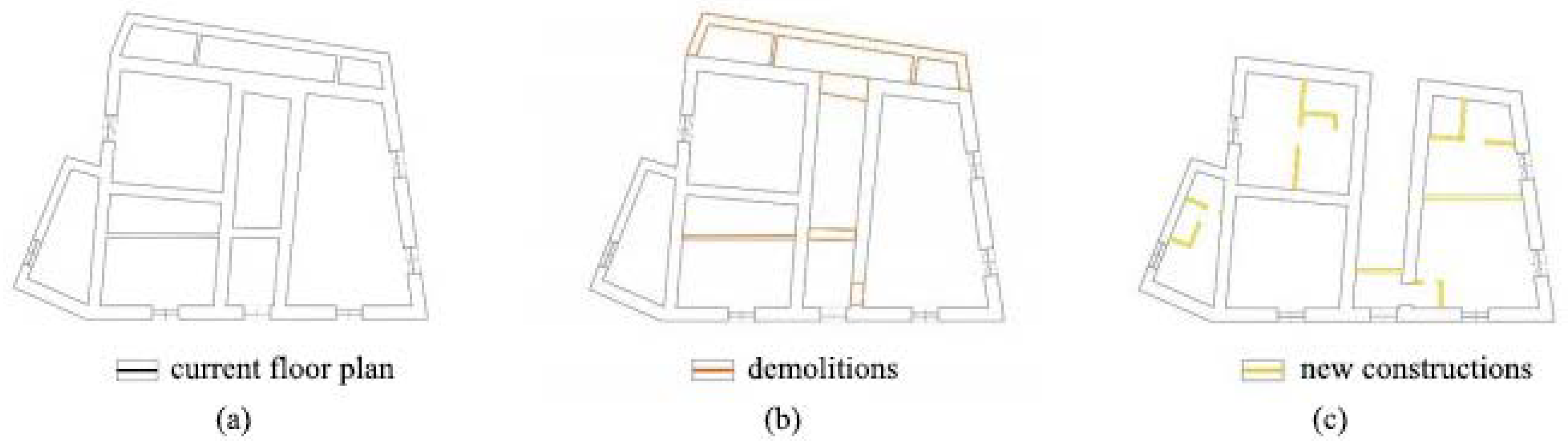

The project solution considered in the present research includes several workings (

Figure 4). In particular—in compliance with the cultural constraints set out by reference public institutions—demolitions are provided for the building part added on the south facades and the stairway in the central portion. Then, new constructions must be realized for (i) the introduction of the staircase in a new building, that leans on the south-west facade, (ii) the dividing walls for a new internal spaces redefinition, (iii) the existing green area renovation.

With reference to the planned functions, the building ground floor will be intended for a lunchroom, a reception, an outdoor equipped area, service and reading rooms, a disabled toilet, a medication place, a gym, and an area for recreational activities. In the accommodation of the nursing home, users will be located on the first and the second floor and they will differ in size and number of beds. In particular, the project provides four accommodation typologies: accomodation A characterized by a total surface of 35 m

2 and two bed places, accomodation B with a surface of 29.2 m

2 and one bed place for disabled person, accomodation C in which there will be three bed places with an overall surface of 40 m

2 and, finally, accomodation D with an internal surface equal to 53 m

2 and three bed places. In each accommodation, a living room with kitchen and a bedroom will be placed. Furthermore, for each floor level, a maximum number of nine users will be hosted, including one disabled person, for a total of eighteen users for the entire building. In

Figure 5, the intended uses in the ground floor plan are reported.

5.3. The PPP Procedure

A PPP operational tool implementation is assumed for the redevelopment of the Cesano Romano castle. In particular, it is assumed that the Public Institution of Assistance and Charity—current owner of the building in disuse—and a private investor, individual or—more frequently—in a corporate form, conclude an onerous and written agreement for a fixed time period (equal to thirty years), in order to redevelop and reconvert the functions of the existing castle. The PPP procedure provides that the building’s refurbishment and new construction interventions be carried out by the private investor, in exchange for the temporary use of the building for the fixed time period. At the end of the concession period, the availability of the property will come back to the owner subject, as well as the acquisition of any transformation, improvement, addition, and accession realized by the private developer. Under this assumption, the private investor (i) bears the costs related to the renovation of the castle, including the new realization costs and the existing green spaces redevelopment and (ii) manages the new nursing home for the entire concession period. In this sense, the private subject bears the management costs for the years in which the activity is operative, performing the planned functions, i.e., insurance, extraordinary expenditure provisions, personnel expenses, and expenditure for the raw materials purchase. With reference to situation 1—no public monetary participation—it is assumed that in exchange for the burdens illustrated, the revenues for private investor will derive exclusively from the tariffs paid by the nursing home users for the provision of planned services.

5.4. Implementation of the DCFA in Situation 1

The verification of the financial feasibility from the private investor point of view related to PPP redevelopment intervention has been carried out through the development a DCFA. In particular, in the first step of the present research related to situation 1—no public monetary participation—the analysis aims to assess if the project will be able to balance or overcome the minimal convenience threshold for the investor and, eventually, to determine the adequate profit in terms of financial criterion satisfaction.

With reference to the case study, the main assumptions of the analysis can be summarized as follows:

- -

The period of the analysis is equal to thirty years. This time period is divided into four phases: (i) step 1—preparatory phase—one year, in which the refurbishment and realization processes are not yet started and the administrative and bureaucratic operations are carried out; (ii) step 2—construction phase—two years, in which the construction activities are done and finished; (iii) step 3—development phase—five years, i.e., from the fourth year to the eighth year, in which the nursing home functions are performed but the building full activities are not yet reached. In this step, it is assumed a development index equal to 20% in the first year of the development phase, i.e., the fourth year of the entire analysis period, to 40% in the second year of this phase, that is the fifth year of the concession period, to 60% in the third year of the development phase, corresponding to the sixth year of the considered whole period, to 80% in the fourth year of the present phase, as in the seventh year of the 20 year period, to 90% in the last fifth year of the development phase, i.e., the overall eighth year; (iv) step 4—fully operational phase—twenty-two years, i.e., from the ninth year of the concession period to its end in the thirtieth year, in which the maximum functioning and exploitation of the planned intended use are verified and, thus, the revenues for the private are equal to 100%. This phase ends with the activity transfer to the Public Institution of Assistance and Charity that could decide to manage the nursing home, to grant the use of the structure to another subject or to sell the building with the existing intended use.

- -

The minimum annual return rate expected by the private investor is equal to 8.50%. This amount has been determined taking into account the risks of similar initiatives in the reference market obtained by consulting different reference reports [

76,

77]. In particular, the investment annual return rate is connected to (i) the revenues volatility, (ii) the initiative dimension, (iii) the reference sector in which the intervention is included (in the specific case, the “hospitality” one), (iv) the ranking of the urban context in which the project is located, (v) the “bankability” of the investment, in terms of its leverage associated to the initial capital percentage to be borrowed.

- -

The 40% of the investment costs related to the refurbishment (building and green area) and new realizations interventions and to the technical costs and general expenses are borrowed from a credit institution, through a 10-year mortgage to be returned through constant annual down payments with an interest rate equal to 4.50%.

- -

The analysis is carried out considering the current and constant prices.

The cost (investment and management) and the revenue items for the DCFA development in situation 1—no public monetary participation—are explained and assessed below.

5.4.1. Costs

The costs of the initiative concern (i) the investment for the refurbishment of the existing castle (building and outdoor area) and for the new realizations, (ii) the management of the nursing home.

Investment Costs

The investment costs are related to (i) the renovation of the existing building, i.e., the demolition of the internal partition walls and the building part on the south facades and the construction of the new dividing walls for the accommodation spaces distribution, (ii) the realization of the new building on the south-west façade for the inclusion of the staircase, (iii) the redevelopment of the green area through the creation of paved paths and green places and introduction of gardens furniture as benches and fountains, (iv) the technical costs and the general expenses deriving from the total refurbishment and construction costs, determined in percentage terms and respectively equal to +6% and +3% of them, (v) the financial charges that identify the interest on the capital borrowed for the realization of the entire transformation project in the specific hypothesis for which the 40% of the construction costs is carried out with loan capital considering an interest rate equal to 4.50%. It should be pointed out that the refurbishment (building and green area) and new realization costs are assessed by price lists of public and private works, currently used in the Lazio region and by the data reported in the “Building typology prices” list [

78]. The costs are also validated by consulting local operators and construction companies. Furthermore, in the technical costs, the expenses for preliminary surveys, design, works management, testing, etc., related to the intervention are included; in the general expenses, the fees for specialized technicians and professionals, the costs of the insurance for the construction phase, etc., are involved.

The renovation of the existing building, the redevelopment of the green area, and the realization of the new building costs are borne by the private investor in the two years of the construction phase, i.e., in the second and third years of the entire analysis period, and the monetary amounts are evenly divided between the two years. The technical costs and general expenses are paid in the first year of the analysis, during the preparatory phase in which the administrative and bureaucratic operations are carried out. Finally, the financial charges burden on the financial balance of the private investor from the first year to the tenth year of the concession period, i.e., the duration of the loan amortization plan based on constant capital repayments.

In

Table 1, the investment costs are shown.

Management Costs

The management costs concern the expenses for the activities of the nursing home carried out in the renovated building. They are determined taking into account the operating costs ordinarily burdened by the local market operators. The management cost items include (i) the insurance for the operating phase costs—calculated equal to 0.1% of the refurbishment and construction costs; (ii) the provision for extraordinary expenditure—determined considering the 0.5% of the refurbishment and construction costs; (iii) the expenses related to the utilities services (electricity, water from the municipal aqueduct, heating, phone, etc.) and to the raw materials purchase—assessed equal to 12% on the revenues related to the nursing home; (iv) the staff salaries. This cost is assessed taking into account the national average salary and the number of sanitary assistants provided by Italian and regional regulations [

79,

80].

The management costs are borne by the private investor from the first year of the development phase, i.e., the fourth year of the entire analysis period, to the end of the concession period, i.e., the thirtieth year. In particular, the insurance costs and the provision for extraordinary expenditure are uniformly divided between the years, whereas the staff salaries, the utilities services, and the raw materials costs are not equally distributed as they are connected to the revenues and, therefore, to the progressive increase of the activities operativity.

Table 2 shows the management cost items in the fully operational phase, i.e., from the ninth year, related to the transformation intervention considered in the present research.

5.4.2. Revenues

With reference to situation 1—no public monetary participation—the revenue items for the investor will derive exclusively from the management of the nursing home.

In

Table 3, the annual revenues deriving from the total annual rates paid by the nursing home users during the analysis period, from the first year of the development phase to the thirtieth year of the Cesano Romano castle use concession period, are reported.

In particular, it should be noted that the revenues have been assessed taking into account the guests’ period of stay in the nursing home, assuming a 365 days/year opening and the total number of beds available equal to eighteen. The average occupation rate was obtained by consulting with the geographic information system on health and healthcare, named “Health for All” of the Italian National Statistics Institute (ISTAT) [

81] with reference to the city of Rome for 2020 and it is equal to 70%.

In order to define the daily rate to be paid by the nursing home users, the Lazio region established the criteria for calculating the fee, distinguishing the amount according to the assistance level received (Delibera della Giunta Regionale n. 790, 20 December 2016). With reference to the specific nursing home services considered in the analysis, the daily rate is equal to 59.20 €. Furthermore, this amount is consistent with the daily tariffs charged in the specific reference context, obtained by consulting healthcare professionals and administrative staff of some nursing homes (possible “competitors”) located in the province of Rome.

Therefore, considering the total number of beds—eighteen—the number of days in the year which the facility will be open—365—the average occupation rate—70%—the daily fee paid by the patients—59.20 €—the annual revenues assessed are equal to 272,260.80 €.

Table 4 shows the temporal distribution assumed for the revenues, due to the progressive increase of the functional operativity in the development and fully operational phases.

The outputs obtained from the implementation of the DCFA to the case study related to the transformation project of the Cesano Romano castle in situation 1—no public monetary participation—do not verify the financial feasibility of the initiative for the private investor. In particular, in fact, the main performance indicators (NPV, IRR) assessed considering a discounting rate equal to 8.50% have pointed out the absence of convenience for the subject to take part in the PPP operation, i.e., to invest own capital in a failed procedure in terms of monetary profit. It should be recalled that 8.50% is the acceptability threshold of the investment for the private subject.

6. Introduction of Situation 2

Recalling the aim of the present analysis related to the significant role played by the public subjects in PPP initiatives, a likely new situation—situation 2 public monetary participation—has been identified. In particular, this situation includes the involvement of a public entity, in order to ensure the positive financial balance for the private investor and, consequently, to start the redevelopment project. Moreover, to comply with the regulatory constraints imposed by the Italian Legislative Decree No. 50/2016, article 180, i.e., the actualized total amount of the periodic fees must be lower than 49% of the sum of investment costs and financial charges of the initiative, the amount of the contribution to be paid by public entity for each year of the entire period of analysis is determined.

In the specific case, the monetary amount is assessed taking into account the temporal distribution of the revenue items. This is related to the progressive increase of the activity’s operativity following the functional reconversion of the Cesano Romano building and it is included among the revenue items for the private subject. Therefore, the fee is assessed by considering a “full” down payment from the fifth year, whereas for the previous years, reduced amounts are provided (=20% for the first year, 40% for the second year, 60% for the third year, and 80% for the fourth one).

With reference to parameters considered in the specific urban area, i.e., the average occupation rate equal to 70% recorded for the city of Rome, and to the risks of the reference market, for which the discounting rate is set equal to 8.50%, which is the ordinary situation, the public contribution is equal to 4378.44 €. The regulatory constraints have been verified, as the actualized sum of the periodic fees (= 92,361.51 €) with a public actualization rate equal to 1.8%—i.e., the current net rate of return on 20 years government bond—is lower than the 49% of the actualized sum of the total investment costs including the financial charges (= 427,077.47 €).

Furthermore, in this research, a sensitivity analysis was developed on the results obtained in order to study the variations of financial sharing of the public subject, by considering different occupation rates in a range (65–75%), with a variation equal to 1%.

In

Figure 6, a graph shows the different outputs in terms of the periodic fee in correspondence with the different occupation rates selected. In particular, it should be observed that public participation is necessary up to an occupation rate of 71%, as from 72% the revenues deriving from the total annual rates paid by the nursing home users are able to ensure the initiative financial convenience. Moreover, for each case analyzed, both the financial and normative conditions are verified, thus (i) the satisfaction of the private convenience threshold is ensured, i.e., an annual return rate equal to 8.50% and (ii) the regulatory provision is complied with, i.e., the actualized sum of the periodic fees is lower than 49% of the sum of the total investment costs and the financial charges of the entire operation.

The analysis of the present case study gives rise to interesting considerations. First of all, it should be highlighted that the public amount assessed does not significantly burden the financial public balance sheet. In fact, this sum is equal to a maximum of 17,259.57 € in the case of an occupational rate equal to 65%, which represents the worst situation for the public subject and, at the same time, the most prudent one for the private investor. In addition, it could be assumed that the nursing home will be affiliated with the National Health Service and, therefore, part of the municipal and/or regional health funds may be allocated to this purpose.

Furthermore, it should be recalled that the choice of the nursing home answers the need of a facility for semi-self-sufficient elderly people in the specific urban territory. It is connected to the percentage of potential users that reaches almost a quarter of the Cesano Romano population (22% of total inhabitants number).

Then, the building is modest in size and the project solution provides for the inclusion of an overall 18 beds. In general terms, moreover, the initiative intends to satisfy a wider demand than that of the municipality of Cesano Romano alone, as there are no similar structures within a radius of 5 km. Thus, it can be assumed that a higher percentage of the occupied beds could be recorded compared to the average occupation rate identified in the metropolitan city of Rome for 2020 (= 70%).

The radar chart in

Figure 7 represents the combinations obtained in correspondence of each occupation rate for which the public contribution is needed, i.e., in the range (65–71%), in terms of (i) periodic fee paid by public subject to the private investor, (ii) total annual rates paid by the nursing home users, (iii) periodic fee and total revenues ratio, (iv) difference between the 49% of the actualized total investment costs, including any financial charges, and the actualized total amount of the periodic fees. In the graph, the values considered have been normalized with respect to the maximum value obtained for each of them. It is evident that the periodic fee is inversely proportional to the total annual rates paid by the nursing home users, as a higher occupation rate implies a higher revenue deriving from the total annual rate paid and, consequently, a lower monetary amount necessary for the financial balance for the private investor. Moreover, the difference between the 49% of the actualized total investment cost of the PPP initiative, including any financial charges, and the actualized total amount of the periodic fees increases in correspondence of the occupational rate growth.

With reference to situation 2—public monetary participation—the project feasibility is confirmed by an IRR = 8.50%, which is the acceptability threshold of the investment for the private subject.

In

Table S2 reported in “Supplementary File”, the development of the DCFA of the case study analyzed with reference to situation 2—

public monetary participation—in the ordinary situation (occupation rate equal to 70%) is shown and the temporal distribution of the public monetary amount is highlighted in green.

Lastly, in order to attest the reliability of the outputs obtained, a sensitivity analysis for the identification of the “critical variables” has been developed, by considering (i) different cost items (investment and management), (ii) different daily rates paid by nursing home users and, therefore, different amounts of revenues. In

Figure 8, a spider graph shows the results in terms of NPV by varying each parameter mentioned in a range (−30%; +30%).

Finally, a scenario analysis was carried out to determinate the public periodic fee in various cases that might take place. In particular, starting from the situation described above, i.e., considering the cost and revenue items already estimated and used for the present assessment (realistic scenario), four situations are considered: the worst-case (very bad) scenario, in which an increase of total investment costs equal to +20% and a drop of revenues of −20% have been assumed; the moderately pessimistic (bad) scenario, with a costs rise and a revenues reduction respectively of +10% and −10%; the moderately optimistic (good) scenario, for which a negative variation of −10% on costs and a revenues growth of +10% have been fixed; the best-case (very good) scenario, if a decrease in total costs of −20% and an increase in revenue items of +20% simultaneously occur.

In

Table 5, for each scenario assumed, the public periodic fee was calculated taking into account the percentage variation on investment and management costs and revenues necessary to ensure the financial feasibility of the initiative is reported. In particular, the periodic fee is set out in absolute terms (€) and in percentage terms compared to the revenues estimated in fully operational phase (%). It should be observed that in the

good and

very good scenario, the public periodic fee is not required to achieve the financial balance of the initiative, as the performance indicators attest the convenience for the private to take part in the project. With reference to the

very bad and

bad scenarios, instead, the public contribution among the revenue items for private subject is necessary to ensure the intervention financial feasibility. However, in these two scenarios, the compliance with the regulatory constraints imposed by the Italian Legislative is not verified, as the actualized total amount of the periodic fees is higher than 49% of the sum of investment costs and financial charges of the initiative. Thus, external financing should be considered to cover the difference between the monetary contribution assessed and the regulatory constraints imposed: this constitutes the unique modality to carry out the operation. Finally, the percentage of this fee is equal to approximately 30% of total revenues assessed in the

very bad scenario, whereas the periodic contribution is estimated at 15% of total revenues in the

bad scenario and at 1.60% of total revenues in the realistic one.

7. Conclusions

In the last decades, due to public budget constraints and frequent inadequate managerial skills of public subjects, the adoption of PPP procedures has been finding wide application in many countries. The increasing use of public-private cooperation forms for the realization or redevelopment of public infrastructures, degraded urban areas, or abandoned public property assets confirms the robustness of PPP tools able to combine the interests and resources of the different parties involved [

82]. The public benefits are mainly related to the need to renovate the existing property asset and to provide new services for the community and, on the other hand, not to burden the public balance sheet. The private interest, instead, concerns the profitability of the intervention, i.e., the initiative ability to generate cash-flows able to remunerate the initial costs and to determine an extra-profit.

With reference to the interventions carried out through the public-private cooperation, in fact, the public subject does not bear the high costs for the project implementation, but it could participate in the initiative through a monetary amount to be included among the revenue items for the private subject. This periodic fee could constitute a mandatory condition to ensure the financial convenience of the entire intervention for the private investor and, according to the Italian regulatory provision (Legislative Decree No. 50/2016, article 180), it “must not exceed 49% of the total investment cost of the PPP initiative, including any financial charges”.

The feasibility of a redevelopment initiative of a public property asset carried out by the PPP operational tool, has been analyzed. In particular, the project concerns a disused building located in the small town of Cesano Romano, near the metropolitan city of Rome. The analyzed project solution provides for the functional reconversion of the building into a nursing home.

In the first step, with reference to situation 1—no public monetary participation—the implementation of the DCFA in which the revenues have been derived exclusively from the total annual rates paid by the nursing home users, has not verified the financial convenience capacity of the initiative to adequately offset the capital and risks for the private investor. Thus, a new situation, called situation 2—public monetary participation—that has provided the public subject involvement through a periodic fee paid to the private has been assumed. The public contribution assessed represents an optimal Pareto frontier of two conflictual goals: (i) the financial feasibility of the initiative for the private investor; (ii) the compliance with the regulatory constraints—Legislative Decree No. 50/2016, article 180.

The paper aimed to highlight the relevant role played by public administration in PPP procedures implementation, as the monetary public contribution constitutes a compromised solution between the current contraction of the public spending capacity and the financial feasibility of the territorial investments. In this sense, this amount allows the public entities not to weigh on the limited available economic funds, by deferring the financial sum over the years of the established period and, at the same time, to actively participate in an initiative on a public property enhancement.

The contribution is part of current international research aimed to examine different aspects of PPPs, by determining the cogence for public entities to contribute to the interventions. The methodology applied for the financial sustainability verification is a flexible tool to be applied to any geographical contexts and considering different urban transformation initiatives typologies—degraded urban area renovation, public property assets enhancement, or ex novo realization.

In this sense, the work does not intend to define new theories or methods but it constitutes a valuable methodological study aimed to illustrate the phases to be carried out for the effective assessment of the convenience of PPP initiative.

Therefore, the contribution has to be included in the international literature providing for an application of the classical DCFA to a specific Italian small town and highlighting the importance of public private cooperation in terms of risks and costs.

Further insights of the research may concern the development of another scenario analysis in the context of quantitative risk assessment, by implementing the real options analysis and/or Monte Carlo methods to compute the probability distribution for critical variables, i.e., to inform about the likelihood of a given percentage variation occurring in them. Finally, a more detailed compliance of the international PPP legislative framework with the EU funds may be added in further development of the present research. In particular, after an appropriate analysis of the effects related to the COVID-19 pandemic, the role of PPP for the investigation of the main European measures to renovate and to manage the existing property assets can be better addressed and highlighted.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}