Impact of Engineering Changes on Value Movement in Fund Flow: Monte Carlo-System Dynamics Modeling Approach

Abstract

:1. Introduction

2. Literature Review

2.1. Engineering Change

2.2. Project Fund Flow

2.3. System Dynamics

3. Proposed Approach

3.1. Characterization of Fund Flow under ECs

3.2. Key Assumptions of the Model

- The cost disbursements are normalized in reference to their timing [23].

- The stability of project fund origins remains unaffected by impediments such as loan difficulties.

- Fund interest rate stability remains throughout time, unaffected by temporal or other effects.

- ECs are observed to follow a normal probability distribution, with each alteration event being independent.

- Contractors consider unforeseen occurrences to be outside the scope of the system and so do not consider them.

- Despite increased costs, time extensions, or resource limitations as a result of engineering changes, the project’s continuity remains unbroken.

3.3. Model Building

- Because certain variables in the model have different dimensions, a method of function mapping or scaling by multiples has been adopted to control them within the same order of magnitude.

- According to the reinforcement theory in behavioral economics, positive rewards influence human activities, causing them to be repeated, while negative reinforcement causes them to diminish. In this article, the decision-maker’s risk tolerance is introduced as a critical factor. When the reserve fund is greater than zero, the decision-maker chooses to extend the processing time for engineering changes, resulting in a risk tolerance setting of 1.1. Conversely, when the reserve fund is not greater than zero, the processing time is reduced [31].

- Change probabilities remain within a distribution range with a positive probability density and a unimodal shape. This property is shared by probability distributions such as the normal distribution, the Beta Distribution, and the triangular distribution. Empirical evidence shows that the normal distribution accurately describes the distribution characteristics of variables [32].

4. Simulation Analysis

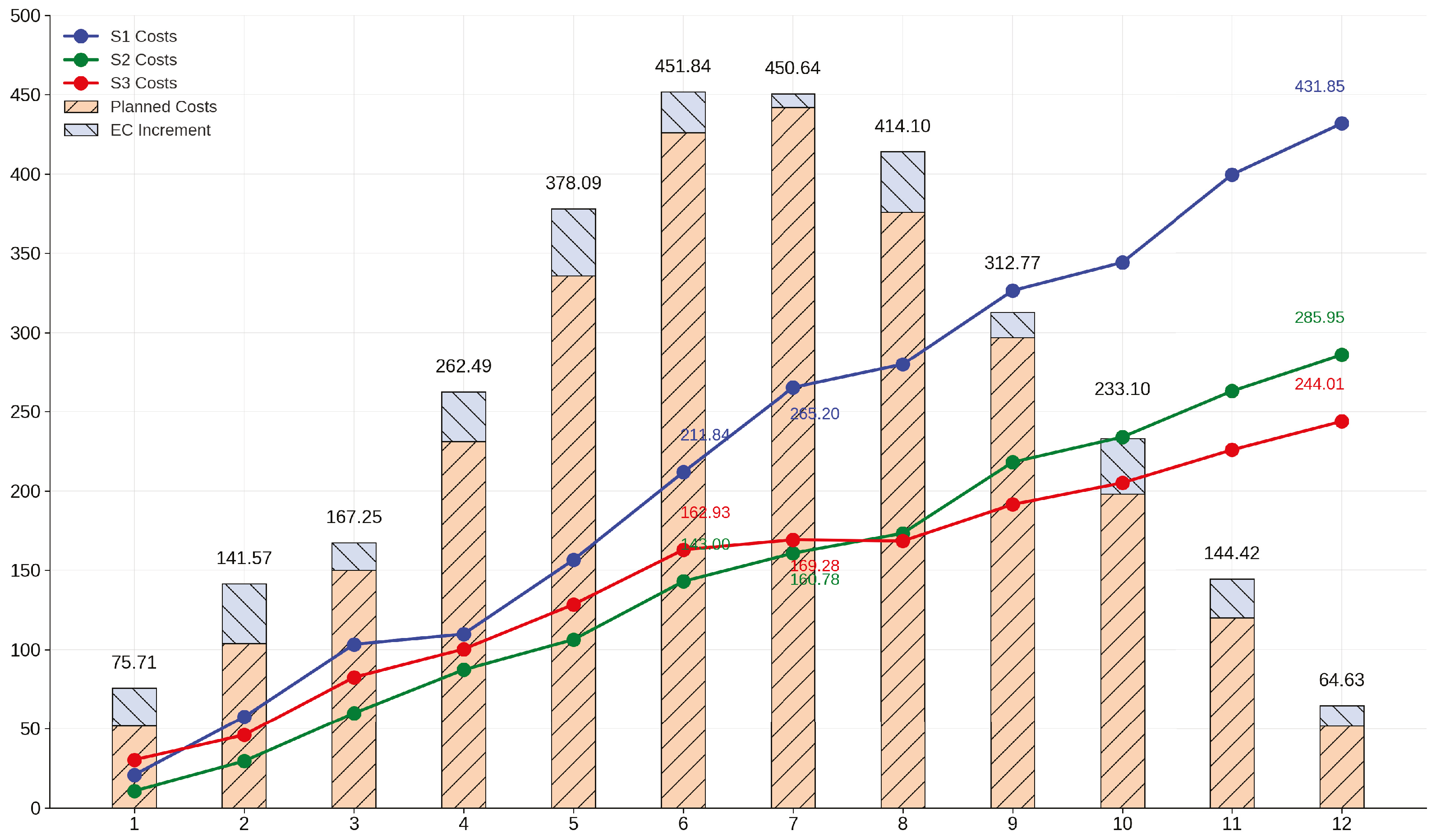

4.1. Fundamental Data

4.2. Model Validation

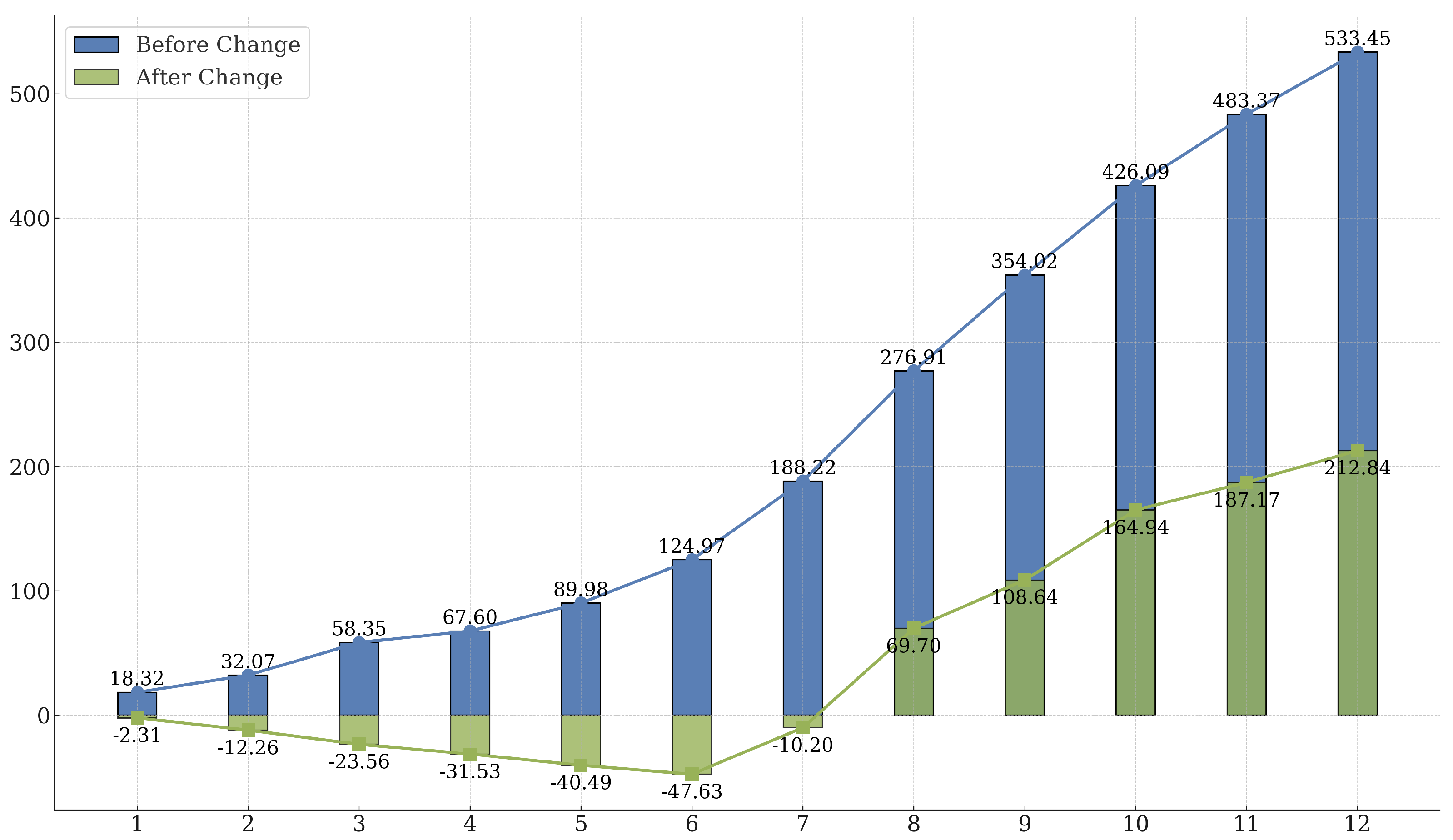

4.3. Fluctuation Patterns and Risks of Fund Flow Value under ECs

4.4. Sensitivity Analysis

4.4.1. Impact of Delay Handling Time Changes on Fund Reserves

4.4.2. Impact on Fund Reserves: Risk Level and Delay Time Changes

5. Conclusions

- (1)

- The reserve fund of a project varies significantly in the face of different ECs. Funds may diverge dramatically from their original path, especially when resources are supplemented. Furthermore, ECs can have a significant impact on fund flows. Such effects are sometimes long-lasting, especially when large changes are involved, potentially leading to fund flow imbalances.

- (2)

- As a result of the disruptions caused by ECs, contractors face significantly higher risk pressures in the early stages of a project than in the middle and later stages. This means that fund liquidity and risk-resilience may be significantly worse during these early stages. As a result, project decision-makers should prioritize protection against occasional risk factors. Simultaneously, it is critical to increase the project’s risk reserve to offset the negative effects of ECs.

- (3)

- The delay handling time and risk level are critical components of the EC-influenced fund flow system. It was discovered through simulation experiments and sensitivity analysis that by decreasing the delay handling time and the project’s risk level, contractors can secure timely compensation in the form of additional funds. Consequently, reaching global Pareto optimality in fund flow becomes more feasible.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Jarratt, T.; Eckert, C.M.; Caldwell, N.H.; Clarkson, P.J. Engineering change: An overview and perspective on the literature. Res. Eng. Des. 2011, 22, 103–124. [Google Scholar] [CrossRef]

- Williams, T.; Eden, C.; Ackermann, F.; Tait, A. The effects of design changes and delays on project costs. J. Oper. Res. Soc. 1995, 46, 809–818. [Google Scholar] [CrossRef]

- Barrie, D.S.; Paulson, B.C., Jr. Professional Construction Management: Including Contracting CM, Design-Construct, and General Contracting; McGraw-Hill: New York, NY, USA, 1992. [Google Scholar]

- Thomas, H.R.; Napolitan, C.L. Quantitative effects of construction changes on labor productivity. J. Constr. Eng. Manag. 1995, 121, 290–296. [Google Scholar] [CrossRef]

- Hanna, A.S.; Lotfallah, W.B.; Lee, M.J. Statistical-fuzzy approach to quantify cumulative impact of change orders. J. Comput. Civ. Eng. 2002, 16, 252–258. [Google Scholar] [CrossRef]

- Hamraz, B.; Caldwell, N.H.; Clarkson, P.J. A matrix-calculation-based algorithm for numerical change propagation analysis. IEEE Trans. Eng. Manag. 2012, 60, 186–198. [Google Scholar] [CrossRef]

- Ren, Y.; Yin, Y.; Shang, Y. Impact of Engineering Changes on Contract Price: A Mechanism Study. Proj. Manag. Tech. 2018, 16, 40–48. [Google Scholar]

- Wang, R.; Samarasinghe, D.A.S.; Skelton, L.; Rotimi, J.O.B. A study of design change management for infrastructure development projects in New Zealand. Buildings 2022, 12, 1486. [Google Scholar] [CrossRef]

- Jahan, S.; Khan, K.I.A.; Thaheem, M.J.; Ullah, F.; Alqurashi, M.; Alsulami, B.T. Modeling Profitability-Influencing Risk Factors for Construction Projects: A System Dynamics Approach. Buildings 2022, 12, 701. [Google Scholar] [CrossRef]

- Chadee, A.; Ali, H.; Gallage, S.; Rathnayake, U. Modelling the Implications of Delayed Payments on Contractors’ Cashflows on Infrastructure Projects. Civ. Eng. J. 2023, 9, 52–71. [Google Scholar] [CrossRef]

- Ashley, D.B.; Teicholz, P.M. Pre-estimate cash flow analysis. J. Constr. Div. 1977, 103, 369–379. [Google Scholar] [CrossRef]

- Sears, G.A. CPM/COST: An integrated approach. J. Constr. Div. 1981, 107, 227–238. [Google Scholar] [CrossRef]

- Park, H.; Han, S.; Russell, J. Cash flow forecasting model for general contractors using moving weights of cost categories. J. Manag. Eng. 2005, 21, 164–172. [Google Scholar] [CrossRef]

- Görög, M. A comprehensive model for planning and controlling contractor cash-flow. Int. J. Proj. Manag. 2009, 27, 481–492. [Google Scholar] [CrossRef]

- Jarrah, R.; Kulkarni, D.; O’Connor, J.T. Cash flow projections for selected TxDoT highway projects. J. Constr. Eng. Manag. 2007, 133, 235–241. [Google Scholar] [CrossRef]

- Lane, D.C. The power of the bond between cause and effect: Jay Wright Forrester and the field of system dynamics. Syst. Dyn. Rev. J. Syst. Dyn. Soc. 2007, 23, 95–118. [Google Scholar] [CrossRef]

- Cooper, K.G. Naval ship production: A claim settled and a framework built. Interfaces 1980, 10, 20–36. [Google Scholar] [CrossRef]

- He, Q.; Cheng, M. Research on Construction Project Cost Control Based on System Dynamics. J. Wuhan Inst. Metall. Manag. Cadre 2011, 21, 26–29. [Google Scholar]

- Liu, J.; Yang, W. Research on Construction Project Cost-Schedule Control Based on System Dynamics. Constr. Technol. 2016, 45, 95–99. [Google Scholar]

- van Dorp, J.R.; Duffey, M. Statistical dependence in risk analysis for project networks using Monte Carlo methods. Int. J. Prod. Econ. 1999, 58, 17–29. [Google Scholar] [CrossRef]

- Ahmed, S.; Arocho, I. Analysis of cost comparison and effects of change orders during construction: Study of a mass timber and a concrete building project. J. Build. Eng. 2021, 33, 101856. [Google Scholar] [CrossRef]

- Ghadge, A.; Er, M.; Ivanov, D.; Chaudhuri, A. Visualisation of ripple effect in supply chains under long-term, simultaneous disruptions: A system dynamics approach. Int. J. Prod. Res. 2022, 60, 6173–6186. [Google Scholar] [CrossRef]

- Karamoozian, A.; Wu, D.; Lambert, J.H.; Luo, C. Risk assessment of renewable energy projects using uncertain information. Int. J. Energy Res. 2022, 46, 18079–18099. [Google Scholar] [CrossRef]

- Gosling, J.; Naim, M.; Towill, D. Identifying and categorizing the sources of uncertainty in construction supply chains. J. Constr. Eng. Manag. 2013, 139, 102–110. [Google Scholar] [CrossRef]

- Chadee, A.A.; Martin, H.H.; Gallage, S.; Banerjee, K.S.; Roopan, R.; Rathnayake, U.; Ray, I. Risk Evaluation of Cost Overruns (COs) in Public Sector Construction Projects: A Fuzzy Synthetic Evaluation. Buildings 2023, 13, 1116. [Google Scholar] [CrossRef]

- Fang, J. Management and Control of Engineering Changes in Construction Projects. Constr. Econ. 2004, 10, 54–58. [Google Scholar]

- Al-Kofahi, Z.G.; Mahdavian, A.; Oloufa, A. System dynamics modeling approach to quantify change orders impact on labor productivity 1: Principles and model development comparative study. Int. J. Constr. Manag. 2022, 22, 1355–1366. [Google Scholar] [CrossRef]

- Karamoozian, A.; Wu, D. A hybrid approach for the supply chain risk assessment of the construction industry during the COVID-19 pandemic. IEEE Trans. Eng. Manag. 2022. [Google Scholar] [CrossRef]

- Karamoozian, A.; Wu, D.; Luo, C. Green Supplier Selection in the Construction Industry Using a Novel Fuzzy Decision-Making Approach. J. Constr. Eng. Manag. 2023, 149, 04023033. [Google Scholar] [CrossRef]

- Yousri, E.; Sayed, A.E.B.; Farag, M.A.; Abdelalim, A.M. Risk Identification of Building Construction Projects in Egypt. Buildings 2023, 13, 1084. [Google Scholar] [CrossRef]

- Skinner, B.F. Reinforcement today. Am. Psychol. 1958, 13, 94. [Google Scholar] [CrossRef]

- Song, J.; Martens, A.; Vanhoucke, M. Using Earned Value Management and Schedule Risk Analysis with resource constraints for project control. Eur. J. Oper. Res. 2022, 297, 451–466. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Number | Variable Name | Variable Definition |

|---|---|---|

| 1 | Reserve Fund | Reserve funds are used for unforeseen situations in a project. |

| 2 | Engineering Change Costs | The amount of cost change caused by engineering changes. |

| 3 | Funding Supply | Funding sources available for the project. |

| 4 | Funding Demand | The amount of funds needed for project execution. |

| 5 | Engineering Change Increment | The amount of change in project modification costs. |

| 6 | Progress Payment | Payments linked to project progress. |

| 7 | Loan Schedule | Repayment plan and scheduling for loans. |

| 8 | Planned Cost | The predetermined cost plan for the project. |

| 9 | Retention Ratio | The percentage of payments retained as a guarantee for subcontractors during project progression. |

| 10 | Payment Extension | The situation of delaying payments. |

| 11 | Project Delay | The actual completion time of the project exceeds the planned schedule. |

| 12 | Delay Handling Time | The time required to assess and process change requests. |

| 13 | Funding Interest Rate | The interest rate of loans. |

| 14 | Project Scale | The scope, size, and complexity of the project. |

| 15 | Occasional Risk Factors | Risk factors that may infrequently but significantly impact the project. |

| 16 | Management Experience | The experience and expertise of project management team members. |

| 17 | Risk Level | The degree of uncertainty and risk faced by the project. |

| 18 | Engineering Change Index | An index measuring the frequency and magnitude of engineering changes in a project. |

| 19 | Project Productivity [27] | The amount of work completed within a specific time, reflecting project efficiency. |

| 20 | Technical Complexity | The complex technologies and processes involved in the project. |

| 21 | Risk Tolerance | The organisation’s or project’s ability to tolerate risks. |

| 22 | Magnitude of Change | The extent and magnitude of the impact of changes on the project. |

| 23 | Expected ROI | The expected rate of return on investment, usually expressed as a percentage. |

| 24 | Machinery Change Cost | The additional costs caused by changes in machinery. |

| 25 | Auxiliary Change Cost | The additional costs caused by changes in auxiliary production. |

| 26 | Other Change Cost | The costs brought about by changes other than those mentioned above. |

| 27 | Labor Change Cost | The additional costs caused by changes in labor. |

| 28 | Material Change Cost | The additional costs caused by changes in materials. |

| 29 | Machinery Cost per Unit Time | Cost of machinery per unit of time. |

| 30 | Transportation Cost | Transportation-related costs. |

| 31 | Transportation Allocation Rate | Ratio of cost allocation to transportation expenses. |

| 32 | Fuel Cost | Fuel-related costs. |

| 33 | Fuel Energy Distribution Rate | Ratio of fuel energy allocation to various costs. |

| 34 | Change Management Cost | Costs required for managing project changes. |

| 35 | Depreciation Change Cost | Additional costs caused by depreciation changes. |

| 36 | Depreciation Cost Rate | Ratio used to measure the gradual decrease in value of fixed assets (such as equipment) over time. |

| 37 | Wage Rates | Labor price per unit of time, related to the scarcity of job types and market demand. |

| 38 | Miscellaneous Expenses | Other costs related to transportation, materials, etc. |

| 39 | Purchase and Storage Rates | Rates for material procurement and storage. |

| 40 | Engineering Change Increment | Increment of project progress and cost due to changes. |

| 41 | Labor Hours Change | Changes in labor hours due to changes in project quantities. |

| 42 | Construction Material Change | Changes in construction materials due to changes in project quantities. |

| 43 | Machinery Shift Change | Changes in machinery shifts due to changes in project quantities. |

| Time | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Progress Payment | 52.00 | 103.99 | 150.03 | 231.15 | 335.96 | 426.01 | 441.86 | 375.92 | 297.00 | 198.05 | 120.02 | 52.00 |

| Planned Costs | 70.31 | 120.24 | 182.54 | 250.61 | 385.25 | 486.25 | 513.19 | 438.44 | 331.23 | 220.12 | 130.48 | 67.34 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jin, L.; Yin, Y.; Du, F.; Yuan, H.; Zheng, C. Impact of Engineering Changes on Value Movement in Fund Flow: Monte Carlo-System Dynamics Modeling Approach. Buildings 2023, 13, 2218. https://doi.org/10.3390/buildings13092218

Jin L, Yin Y, Du F, Yuan H, Zheng C. Impact of Engineering Changes on Value Movement in Fund Flow: Monte Carlo-System Dynamics Modeling Approach. Buildings. 2023; 13(9):2218. https://doi.org/10.3390/buildings13092218

Chicago/Turabian StyleJin, Lianghai, Yuelong Yin, Faxing Du, Hongchuan Yuan, and Chuchu Zheng. 2023. "Impact of Engineering Changes on Value Movement in Fund Flow: Monte Carlo-System Dynamics Modeling Approach" Buildings 13, no. 9: 2218. https://doi.org/10.3390/buildings13092218

APA StyleJin, L., Yin, Y., Du, F., Yuan, H., & Zheng, C. (2023). Impact of Engineering Changes on Value Movement in Fund Flow: Monte Carlo-System Dynamics Modeling Approach. Buildings, 13(9), 2218. https://doi.org/10.3390/buildings13092218