Coopetition in the SoC Industry: The Case of Qualcomm Incorporated

Abstract

:1. Introduction

2. Literature Review

2.1. Competitive Dynamics

2.2. Coopetition

3. Research Method

4. Qualcomm Background

4.1. History

4.2. Vision and Major Products

4.3. Snapdragon

4.4. Fabless Model

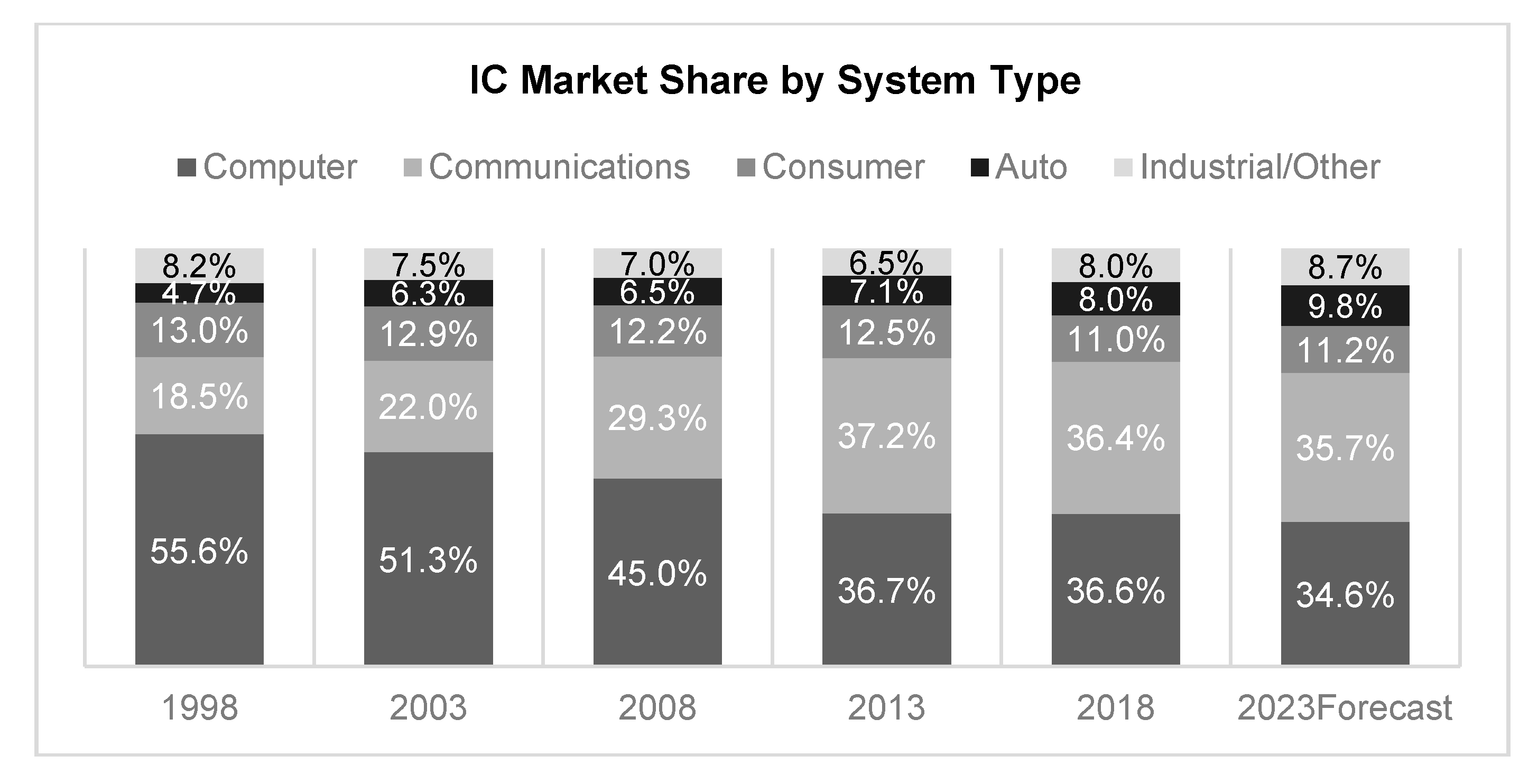

5. SoC Industry

5.1. Types of SoC Business Models

5.2. Market Situation

6. Factors in Qualcomm’s Success

6.1. R&D Investment in Advanced Technologies

6.2. Technology Acquisitions

7. Qualcomm’s Coopetition with Samsung

8. Discussion

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

References

- Tani, M.; Papaluca, O.; Sasso, P. The system thinking perspective in the open-innovation research: A systematic review. J. Open Innov. Technol. Mark. Complex. 2016, 4, 38. [Google Scholar] [CrossRef] [Green Version]

- Nalebuff, B.J.; Brandenburger, A.; Maulana, A. Co-Opetition; Harper Collins Business: London, UK, 1996. [Google Scholar]

- Afuah, A. How much do your co-opetitors’ capabilities matter in the face of technological change? Strateg. Manag. J. 2000, 21, 397–404. [Google Scholar] [CrossRef]

- Bonel, E.; Rocco, E. Coopeting to survive; surviving coopetition. Int. Stud. Manag. Organ. 2007, 37, 70–96. [Google Scholar] [CrossRef]

- Chou, H.H.; Zolkiewski, J. Coopetition and value creation and appropriation: The role of interdependencies, tensions and harmony. Ind. Mark. Manag. 2018, 70, 25–33. [Google Scholar] [CrossRef]

- Park, B.J.; Srivastava, M.K.; Gnyawali, D.R. Impact of coopetition in the alliance portfolio and coopetition experience on firm innovation. Technol. Anal. Strateg. Manag. 2014, 26, 893–907. [Google Scholar] [CrossRef]

- Yami, S.; Nemeh, A. Organizing coopetition for innovation: The case of wireless telecommunication sector in Europe. Ind. Mark. Manag. 2014, 43, 250–260. [Google Scholar] [CrossRef]

- Bengtsson, M.; Raza-Ullah, T.; Vanyushyn, V. The coopetition paradox and tension: The moderating role of coopetition capability. Ind. Mark. Manag. 2016, 53, 19–30. [Google Scholar] [CrossRef]

- Ketchen, D.J., Jr.; Snow, C.C.; Hoover, V.L. Research on competitive dynamics: Recent accomplishments and future challenges. J. Manag. 2004, 30, 779–804. [Google Scholar] [CrossRef]

- Chen, M.J.; Miller, D. Competitive dynamics: Themes, trends, and a prospective research platform. Acad. Manag. Ann. 2012, 6, 135–210. [Google Scholar] [CrossRef]

- Chen, M.J.; Miller, D. Competitive attack, retaliation and performance: An expectancy-valence framework. Strateg. Manag. J. 1994, 15, 85–102. [Google Scholar] [CrossRef]

- Silverman, B.S.; Baum, J.A. Alliance-based competitive dynamics. Acad. Manag. J. 2002, 45, 791–806. [Google Scholar]

- Nair, A.; Selover, D.D. A study of competitive dynamics. J. Bus. Res. 2012, 65, 355–361. [Google Scholar] [CrossRef]

- Luo, X.; Rindfleisch, A.; Tse, D.K. Working with rivals: The impact of competitor alliances on financial performance. J. Mark. Res. 2007, 44, 73–83. [Google Scholar] [CrossRef]

- Della Corte, V. Innovation through Coopetition: Future Directions and New Challenges. J. Open Innov. Technol. Mark. Complex. 2018, 4, 47. [Google Scholar] [CrossRef] [Green Version]

- Bengtsson, M.; Eriksson, J.; Wincent, J. Co-opetition dynamics–an outline for further inquiry. Compet. Rev. 2010, 20, 194–214. [Google Scholar] [CrossRef]

- Luo, Y. A coopetition perspective of global competition. J. World Bus. 2007, 42, 129–144. [Google Scholar] [CrossRef]

- Lado, A.A.; Boyd, N.G.; Hanlon, S.C. Competition, cooperation, and the search for economic rents: A syncretic model. Acad. Manag. Rev. 1997, 22, 110–141. [Google Scholar] [CrossRef]

- Bengtsson, M.; Kock, S. Cooperation and competition in relationships between competitors in business networks. J. Bus. Ind. Mark. 1999, 14, 178–194. [Google Scholar] [CrossRef]

- Levinthal, D.A.; March, J.G. The myopia of learning. Strateg. Manag. J. 1993, 14, 95–112. [Google Scholar] [CrossRef]

- Eisenhardt, K.M. Building theories from case study research. Acad. Manag. Rev. 1989, 14, 532–550. [Google Scholar] [CrossRef]

- Baxter, P.; Jack, S. Qualitative case study methodology: Study design and implementation for novice researchers. Qual. Rep. 2008, 13, 544–559. [Google Scholar]

- Qualcomm Announces Strategic Realignment Plan. Available online: https://www.qualcomm.com/news/releases/2015/07/22/qualcomm-announces-strategic-realignment-plan (accessed on 15 December 2015).

- Telecommunication Technology Association. Available online: http://www.tta.or.kr (accessed on 1 February 2020).

- Products. Available online: http://www.qualcomm.co.kr/products (accessed on 8 May 2015).

- Rouse, M. What is Full-Disk Encryption (FDE)?—Definition from WhatIs.Com. Available online: http://whatis.techtarget.com/definition/full-disk-encryption-FDE (accessed on 4 May 2016).

- Anthony, S. SoC vs. CPU—The Battle for the Future of Computing. Available online: http://www.extremetech.com/computing/126235-soc-vs-cpu-the-battle-for-the-future-of-computing (accessed on 4 May 2016).

- Products. Available online: https://www.qualcomm.com/snapdragon (accessed on 1 September 2019).

- 2009 Annual Report of Qualcomm. Available online: http://files.shareholder.com/downloads/QCOM/1725443717x0x349566/6D97C862-1FFD-42F1-AA36-FC416BC242BB/qualcomm_corporate_overview_09.pdf (accessed on 12 June 2016).

- Clarke, P. Qualcomm Joins IMEC Core CMOS R&D Program. Available online: http://www.eetimes.com/document.asp?doc_id=1263017 (accessed on 12 June 2016).

- Morgan, J. A Simple Explanation of ‘The Internet of Things’. Available online: https://www.forbes.com/sites/jacobmorgan/2014/05/13/simple-explanation-internet-things-that-anyone-can-understand/#2903760e1d09 (accessed on 2 June 2016).

- Communications IC Market to Again Surpass Computer IC Market. Available online: https://anysilicon.com/communications-ic-market-to-again-surpass-computer-ic-market/ (accessed on 31 August 2019).

- IC Insights. Available online: http://www.icinsights.com/news/bulletins/Communications-IC-Market-To-Again-Surpass-Computer-IC-Market/ (accessed on 2 September 2019).

- Statista. Global Smartphone Sales to End Users from 1st Quarter 2009 to 4th Quarter 2015, by Operating System (in Million Units). Available online: http://www.statista.com/statistics/266219/global-smartphone-sales-since-1st-quarter-2009-by-operating-system (accessed on 4 May 2016).

- Qualcomm Still Dominates the App Processor Market but EM Peers are Creeping. Available online: http://www.forbes.com/sites/greatspeculations/2012/10/19/qualcomm-still-dominates-the-app-processor-market-but-em-peers-are-creeping/#25c53c3372e3 (accessed on 5 May 2016).

- Kim, G.; Lee, S. Available online: https://www.mk.co.kr/news/business/view/2019/01/63865/ (accessed on 12 September 2019).

- Singh, S. Worldwide Smartphone Sales Grew 9.7% in Q4 2015; Iphone Declines: Gartner. Available online: http://timesofindia.indiatimes.com/tech/tech-news/Worldwide-smartphone-sales-grew-9-7-in-Q4-2015-iPhone-declines-Gartner/articleshow/51043074.cms (accessed on 4 May 2016).

- McKinsey. The Internet of Things: Sizing Up the Opportunity. Available online: http://www.mckinsey.com/industries/high-tech/our-insights/the-internet-of-things-sizing-up-the-opportunity (accessed on 4 May 2016).

- Kwon, G.Y. Available online: http://news1.kr/articles/?3642857 (accessed on 12 June 2019).

- Qualcomm Incorporated—Annual Report. Available online: http://investor.qualcomm.com/secfiling.cfm?filingID=1234452-14-320&CIK=804328#QCOM10-K2014_HTM_S51508F49E447D4D6F80EC8ED838E698A (accessed on 15 May 2015).

- Experience the Amazing Exynos by Visiting Samsung Exynos Website. Available online: http://www.samsung.com/semiconductor/minisite/Exynos/w/mediacenter.html#?v=blog_History_of_Exynos_Processors (accessed on 4 May 2016).

- 2015 Annual Report of Qualcomm. Available online: http://investor.qualcomm.com/secfiling.cfm?filingID=1234452-14-320&CIK=804328qualcomm (accessed on 12 June 2016).

- Qualcomm Acquires Handheld Graphics and Multimedia Assets from AMD. Available online: https://www.qualcomm.com/news/releases/2009/01/20/qualcomm-acquires-handheld-graphics-and-multimedia-assets-amd (accessed on 14 June 2016).

- MK Economy. Available online: http://news.mk.co.kr/v2/economy/view.php?sc=50000001&cm=%C0%FC%C3%BC%20%B1%E2%BB%E7&year=2014&no=1304838&relatedcode=&wonNo (accessed on 13 May 2016).

- Press Release. Available online: https://www.qualcomm.com/news/releases/2011/05/24/qualcomm-completes-31-billion-acquisition-atheros-communications (accessed on 13 May 2016).

- Chaudhuri, S.; Tabrizi, B. Capturing the real value in high-tech acquisitions. Harv. Bus. Rev. 2009, 77, 123. Available online: https://hbr.org/1999/09/capturing-the-real-value-in-high-tech-acquisitions (accessed on 13 June 2016).

- Mobile Operating System Market Share Worldwide. Available online: https://gs.statcounter.com/os-market-share/mobile/worldwide (accessed on 4 September 2019).

- Jordan, S.; James, C. Samsung Electronics; Harvard Business School Publishing: Boston, MA, USA, 2006; HBS No. 9-705-508. [Google Scholar]

- Yu, T.F.L.; Yan, H.D. Handbook of East Asian Entrepreneurship; Routledge: Abingdon, UK, 2014; Available online: https://books.google.co.kr/books?id=VmKvBAAAQBAJ&pg=PA339&lpg=PA339&dq=samsung+license+sharp+of+japan&source=bl&ots=NpyFH9of9z&sig=qrR2Y0Qd7rzZrXuVelo5mLrc2ck&hl=en&sa=X&ved=0ahUKEwiH45v7zaLNAhViGqYKHTL9DDYQ6AEIJjAC#v=onepage&q=technology%20licensing%20from%20California-%20based%20Zytrex%20and%20Japan%27s%20Sharp.&f=false (accessed on 6 May 2016).

- Yun, J.; Jeon, J.; Park, K.; Zhao, X. Benefits and costs of closed innovation strategy: Analysis of Samsung’s Galaxy Note 7 Explosion and withdrawal scandal. J. Open Innov. Technol. Mark. Complex. 2018, 4, 20. [Google Scholar] [CrossRef] [Green Version]

- Lucic, K. Exynos-Powered Galaxy S6 Flagships Equal Significantly Less Patent Cash for Qualcomm. Available online: http://www.androidheadlines.com/2015/04/exynos-7420-powered-galaxy-s6-flagships-equal-significantly-less-patent-cash-qualcomm.html (accessed on 4 May 2016).

- Chang, W.J. Available online: https://n.news.naver.com/article/366/0000442376 (accessed on 4 September 2019).

- Wilson, M. HTC One M9 Benchmark Shows Snapdragon 810 Overheating. Available online: http://www.kitguru.net/laptops/mobile/matthew-wilson/htc-one-m9-benchmark-shows-snapdragon-810-overheating/ (accessed on 15 December 2015).

- Sun, L. Qualcomm Inc. vs. Samsung: When a Partner Becomes a Rival. Available online: http://www.fool.com/investing/general/2015/11/16/qualcomm-inc-vs-samsung-when-a-partner-becomes-a-r.aspx (accessed on 15 December 2015).

- Qualcomm CDMA Technologies Takes Delivery of MSM6050 Chip, First Wireless Baseband IC from TSMC’s 300mm Wafer Fab Line. Available online: https://www.qualcomm.com/news/releases/2001/11/08/qualcomm-cdma-technologies-takes-delivery-msm6050-chip-first-wireless (accessed on 15 December 2015).

- Abrar. The Samsung Exynos 8870 Chipset for the External Clients. Available online: http://www.updategadgets.com/the-samsung-exynos-8870-chipset-for-the-external-clients/ (accessed on 4 May 2016).

- Ren, S. TSMC: Qualcomm is Coming Back, Jpmorgan Raises Target. Available online: http://blogs.barrons.com/asiastocks/2016/03/07/tsmc-qualcomm-is-coming-back-jpmorgan-raises-target/ (accessed on 30 May 2016).

- Kang, D.C. Available online: http://biz.chosun.com/site/data/html_dir/2019/06/11/2019061100030.html (accessed on 29 September 2019).

- Kim, Y.W. Available online: http://www.businesspost.co.kr/BP?command=article_view&num=142660 (accessed on 26 September 2019).

- Gnyawali, D.R.; Park, B.J.R. Co-opetition between giants: Collaboration with competitors for technological innovation. Res. Policy 2011, 40, 650–663. [Google Scholar] [CrossRef]

- Ritala, P.; Hurmelinna-Laukkanen, P. Incremental and radical innovation in coopetition—The role of absorptive capacity and appropriability. J. Prod. Innov. Manag. 2013, 30, 154–169. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Processors | Gobi, Hy-Fi, IPQ, Izat, Powerline, Snapdragon, Small Cells, VIVE, Wi-Fi Platforms |

| Displays | Mirasol, Pixtronix |

| Software | AllPlay, 2net, Brew, HealthyCircles, Qchat, Qlearn, RaptorQ, Vuforia |

| Wireless Charging | Halo, WiPower |

| Primary Activities | |

| Operations | Qualcomm collaborates closely with its manufacturers, having a say in every single feature and product, although it does not directly manufacture its products. |

| Supporting Activities | |

| Technology Development | Qualcomm invests considerable capital into the advancement of manufacturing technology. It also creates several strategic alliances with other global semiconductor research programs, such as the Complementary Metal-Oxide-Semiconductor (CMOS) Program by IMEC, a research institute for nanoelectronics, for the development of technologies regarding semiconductors and its related products [30]. |

| Procurement | Qualcomm heavily relies on third-party manufacturing for support. As such, it maintains good relationships with its suppliers, working well with them to ensure the continuous quality and reliability of its products. |

| Rank | Company | 2017 | 2018 |

|---|---|---|---|

| 1 | Qualcomm | 37.9% | 37% |

| 2 | MediaTek | 25.7% | 23.2% |

| 3 | Apple | 14% | 13.5% |

| 4 | Samsung | 8.2% | 11.7% |

| 5 | Spreadtrum Communications | 9.4% | 4.9% |

| 6 | Others | 4.8% | 9.7% |

| Total | 100% | 100% |

| 2016 R&D Exp($M) | 2016 R&D Intensity (R&D exp/Revenue) | 2017 R&D Exp($M) | 2017 R&D Intensity (R&D exp/Revenue) | 2018 R&D Exp($M) | 2018 R&D Intensity (R&D exp/Revenue) | |

|---|---|---|---|---|---|---|

| Qualcomm | 5151 | 22% | 5485 | 25% | 5625 | 25% |

| Samsung | 1240 | 7% | 1408 | 7% | 1563 | 7% |

| Apple | 10,045 | 5% | 11,581 | 5% | 14,236 | 5% |

| Broadcom | 2674 | 20% | 3292 | 19% | 3768 | 18% |

| MediaTek | 180 | 20% | 185 | 24% | 186 | 24% |

| QCT | QTL | |

|---|---|---|

| 2016 | $15,409 | $7664 |

| As a percent of total | 65% | 33% |

| 2017 | $16,479 | $6445 |

| As a percent of total | 74% | 29% |

| 2018 | $17,282 | $5163 |

| As a percent of total | 76% | 23% |

| Date | Company | Date | Company |

|---|---|---|---|

| 01/19/09 | AMD Inc-Handhale Graphics Asts | 11/25/13 | Roadnet Technologies Inc |

| 02/10/09 | Inside Secure SA | 01/10/14 | kooaba AG |

| 03/13/09 | Digital Fountain Inc | 06/01/14 | Healthvista India Private Ltd |

| 03/23/09 | Verreon Inc | 06/18/14 | Black Sand Technologies Inc |

| 05/20/09 | Higel Power LLC | 07/03/14 | Wilocity Ltd |

| 07/12/10 | Tapioca Mobile Inc | 07/30/14 | EmpoweredU |

| 10/13/10 | iSkoot Technologies Inc | 08/26/14 | Euclid Vision Technologies BV |

| 12/28/10 | Boundary Information Group | 09/15/14 | Euvision Technologies BV |

| 01/05/11 | Atheros Communications Inc | 10/15/14 | CSR PLC |

| 01/14/11 | FleetRisk Advisors LLC | 12/12/14 | Beijing Netriver Tech Co Ltd |

| 02/12/11 | Sylectus | 12/12/14 | Beijing Qixin Yiwei Info Tech |

| 08/31/11 | Bigfoot Networks Inc | 02/02/15 | Knel Robotics |

| 11/08/11 | HaloIPT Ltd | 06/12/15 | Nujira Ltd |

| 11/13/11 | Pixtronix Inc | 06/30/15 | Maxim Integrated Prod-Bus |

| 06/18/12 | Summit Microelectronics Inc | 08/06/15 | Ikanos Communications Inc |

| 08/22/12 | DesignArt Networks Ltd | 08/14/15 | Silanna Semiconductor USA Inc |

| 10/26/12 | TransCella Inc | 09/14/15 | Capsule Tech Inc |

| 11/16/12 | EPOS Dvlp-Cert Asts | 09/14/15 | Capsule Technologie SA |

| 05/06/13 | MyTeleHealth Solutions LLC | 03/02/17 | TDK Corporation |

| 10/31/13 | Arteris Inc-Certain Assets | 03/02/17 | RF360 Holdings. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kwon, Y.; Kang, D.; Kim, S.; Choi, S. Coopetition in the SoC Industry: The Case of Qualcomm Incorporated. J. Open Innov. Technol. Mark. Complex. 2020, 6, 9. https://doi.org/10.3390/joitmc6010009

Kwon Y, Kang D, Kim S, Choi S. Coopetition in the SoC Industry: The Case of Qualcomm Incorporated. Journal of Open Innovation: Technology, Market, and Complexity. 2020; 6(1):9. https://doi.org/10.3390/joitmc6010009

Chicago/Turabian StyleKwon, Yona, Dahee Kang, Sinji Kim, and Seungho Choi. 2020. "Coopetition in the SoC Industry: The Case of Qualcomm Incorporated" Journal of Open Innovation: Technology, Market, and Complexity 6, no. 1: 9. https://doi.org/10.3390/joitmc6010009

APA StyleKwon, Y., Kang, D., Kim, S., & Choi, S. (2020). Coopetition in the SoC Industry: The Case of Qualcomm Incorporated. Journal of Open Innovation: Technology, Market, and Complexity, 6(1), 9. https://doi.org/10.3390/joitmc6010009