1. Introduction

Low carbon transition of energy systems is critical to global carbon mitigation. According to an report from International Energy Agency (IEA), 90% of global carbon emissions came from burning fossil fuels in 2015 [

1]. In 2019, global carbon emissions from energy sectors reached 34.2 billion tonnes with an average growth rate of 1.1% in the last decade [

2]. Despite rapid growth of renewable energy in recent years, fossil fuels still accounted for 84% in global primary energy supply in 2019 [

2]. In energy consumption sectors, fossil fuels accounted for 67% of global energy final use, whilst electricity only accounted for 19% [

1].

Achieving a carbon neutral or even negative emissions target would reshape energy systems thoroughly from primary energy supply to final use. Applying carbon removal technologies and improving shares of electricity, hydrogen, biomass, and other renewable resources in energy final use sectors to replace fossil energy are essential to reduce carbon emissions. In view that most renewable resources are converted to electricity, improving electrification in final energy use is an inevitable choice to reduce carbon emissions [

3]. Fossil energy use in some specific production and household sectors, such as steel sector, cannot be replaced by electricity, whilst hydrogen has great potential in these sectors [

4]. Further, biomass resources and their conversion products, as carbon neutral fuels in life-span, can also play an important role in some specific sectors to replace fossil fuels, such as power sector [

5]. Carbon capture and storage (CCS) can be deployed in industry sectors and power sectors with fossil fuels combustion to remove most carbon emissions, which converts fossil technologies to carbon neutral technologies [

6]. Bioenergy with carbon capture and storage (BECCS) [

7] and direct air capture (DAC) [

8] enable negative carbon emissions. Moreover, renewable subsidies, carbon taxes, and carbon trade are effective measures to reduce carbon emissions in energy supply and conversion sectors, especially in power sectors [

9].

Different transition targets would lead to different transition costs from reshaping energy supply systems, with corresponding transition actions. Faster transition would not only lead to massive deployment of decarbonisation technologies with higher costs, but also result in huge stranded costs of existing fossil energy infrastructure. Various transition targets have been put forward by international organizations and many countries. The Paris Agreement adopted in December 2015 aims to limit the temperature increase to well below 2 degree above pre-industrial levels and to pursue efforts to limit the temperature increase to 1.5 degree [

10]. The Intergovernmental Panel on Climate Change (IPCC) pointed out that carbon emissions should be reduced to net zero around 2050 and 2070 to achieve the 1.5-degree target and the 2-degree target, respectively [

11]. European Commission has proposed a strategy to achieve carbon neutrality within the European Union by 2050 [

12]. China, the largest developing country in the world, has pledged to reach summit of carbon emissions by around 2030, and improve non-fossil energy shares to 50% in primary energy supply by 2050 [

13].

Reducing energy supply system transition costs to obtain an affordable and executable transition strategy is attractive, and energy infrastructure is critical in cost reduction due to its massive investment and long life-span. Firstly, energy infrastructure is imperative to secure energy supply, and inadequate non-fossil energy infrastructure would block carbon reduction. Secondly, energy demand would keep growing in many countries, and consequently energy infrastructure would be constructed along with growing demand to secure energy supply. Thirdly, a faster transition would result in significant investment on non-fossil energy infrastructure, and also lead to stranded investment in fossil energy infrastructure.

In the meanwhile, albeit the fact that hydrogen is widely considered as an imperative energy carrier to reach a carbon neutral target due to its potential to replace fossil fuels in end-use sectors with zero carbon emissions [

14], multiple hydrogen production alternatives can lead to a life-span carbon neutral ultimate with different energy system deployment and transition costs. Hydrogen can be produced from fossil fuels and non-fossil power, and consequently classified into three categories, namely green hydrogen, blue hydrogen and black hydrogen [

15]. Green hydrogen and black hydrogen indicate that hydrogen is produced from non-fossil power and fossil fuels respectively, and blue hydrogen indicates that hydrogen is produced from fossil fuels with CCS to remove carbon emissions. Green hydrogen and blue hydrogen can both lead to carbon neutral, but result in different energy system deployment and transition costs. Green hydrogen would significantly accelerate the expansion of the power system, leading to large investment of non-fossil power infrastructure. Blue hydrogen would moderate fossil energy demand reduction, and part of fossil energy infrastructure can be remained, which would consequently reduce stranded costs of fossil energy infrastructure, but CCS facilities would lead to huge costs.

This paper aims to obtain transition pathways oriented from different transition targets with least system transition costs and specific energy infrastructure deployment strategies, and analyze the impact of hydrogen production alternatives on energy system planning and transition costs.

Top-down methods are widely applied to quantify carbon mitigation costs, such as computable general equilibrium (CGE) models, but detailed infrastructure planning strategies cannot be obtained by these methods. These models are suited to quantify economic impacts, whilst they cannot reduce system costs by optimization, and the resolution of time, space, technology and energy carriers is insufficient when quantifying energy supply system transition costs. Most studies focus on the costs resulting from a single policy or strategy, whilst a few provide a comprehensive view. Fujimori et al. [

16] quantified GDP losses in Japan with a comprehensive mitigation strategy based on a CGE model, which varied from 1.2% to 2.5% of GDP to reduce 80% of carbon emissions by 2050. McCollum et al. [

14] estimated global energy investment to fulfill the Paris Agreement by 2050 using a few widely applied models, which all comprised of CGE models. Zhang et al. [

17] analyzed the impact of carbon trade policies based on a CGE model, and pointed out that the GDP losses would be 0.16%, 1.33%, and 1.42% in U.S., Japan, and South Korea, respectively. Liu and Lu [

18] applied a dynamic CGE model to quantify the economic impact of carbon tax in China. Wang et al. quantified the cost to achieve Copenhagen targets in Guangdong, China, which would be 1.4% of GDP based on a two-region CGE model [

19].

Bottom-up methods, such as energy planning models (EPM), are widely applied to obtain the deployment of energy systems with least costs by optimization. Most of these researches focus on specific technology, energy carrier, and sectors, and thus they cannot quantify the transition costs in the overall energy systems, whilst those models that describe the entire energy system have yet to be improved in terms of infrastructure description and temporal and spatial resolution [

20]. Emodi et al. [

21] analyzed impacts of transition policies in Nigeria towards 2040 based on the Long-range Energy Alternative Planning (LEAP) model, in which only energy mix was described. Apostolou [

22] developed an optimization model to obtain the planning of hydrogen system, in which hydrogen would be used in power and transport sectors. Chen et al. [

23] developed a multi-regional and multi-period optimization model of power systems in China, whilst new transmission grids and power storage facilities were not described. Zhang et al. [

24] developed a multi-regional model to obtain the planning of gas pipelines in China, whilst monthly demand fluctuation and storage facilities were neglected. Pan et al. [

25] developed a model of the oil supply chain in China, whilst regional variation was neglected. Mou and Li [

26] obtained the optimal coal flow amongst regions in China, whilst infrastructure limitation was not taken into consideration, such as production capacity and transmission capacity.

Most bottom-up models of hydrogen supply systems focus on green hydrogen rather than blue hydrogen, and impacts of hydrogen systems on the power and fossil energy systems are not analyzed. Samsatli and Staffell [

27] developed a wind-hydrogen integrated optimization model to obtain the optimal hydrogen system planning in Great Britain. Baufume and Grueger [

28] developed a hydrogen pipeline optimization model using Geographical Information System (GIS) method, and all hydrogen was produced from renewable power. A hydrogen-renewable system model was developed to analyze the impacts of hydrogen systems on curtailment reduction [

29].

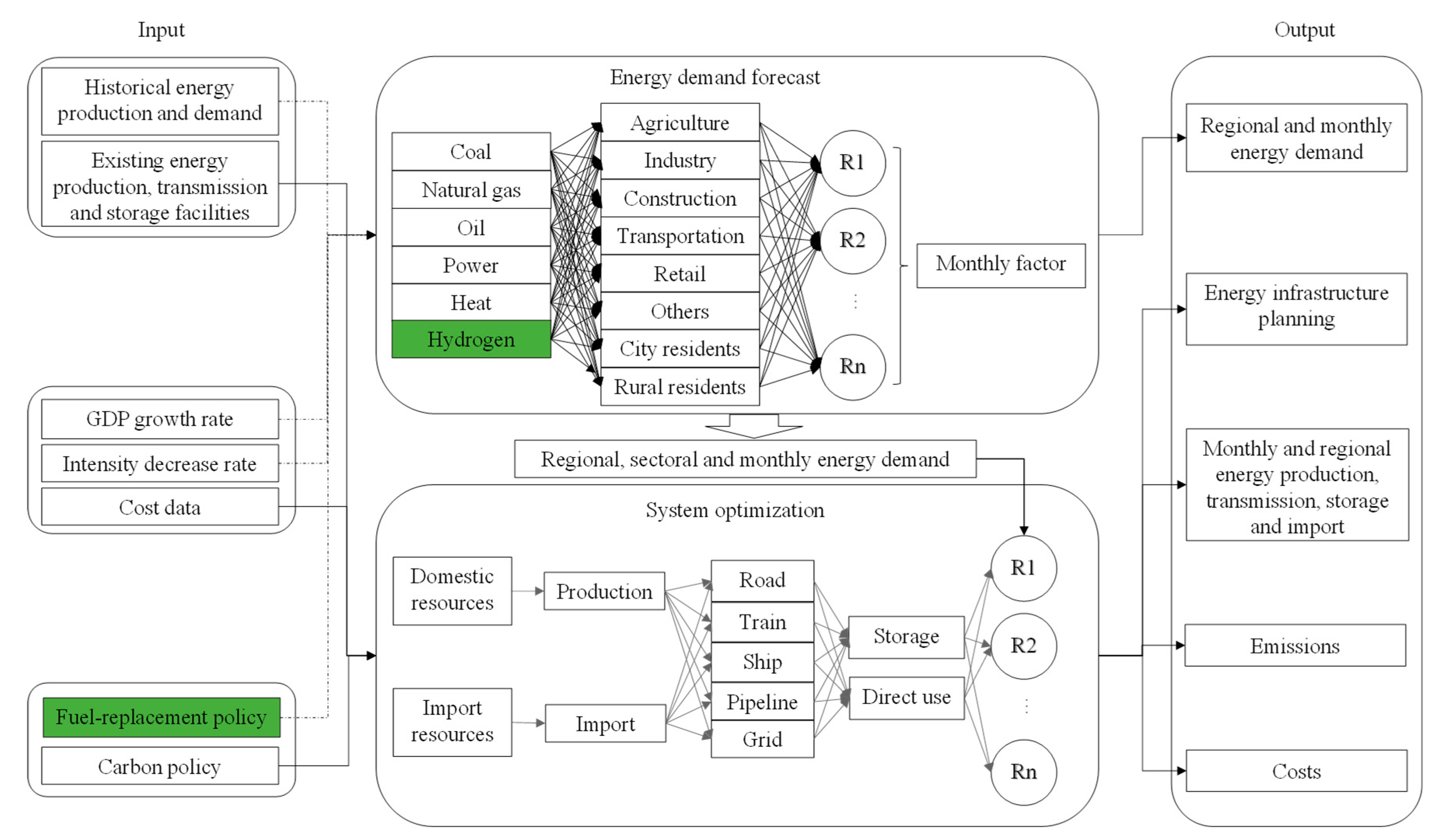

In our previous work, we developed the China Regional Energy Supply System Optimization Model (CRESOM) [

30], which is a multi-regional, multi-period and infrastructure-based optimization model integrating coal, natural gas, oil and power systems in China, to obtain the energy system planning strategy with least costs. The pathway with least costs oriented from stated transition targets in 2050 was then analyzed, and the infrastructure planning strategy was pointed out [

31]. However, Hydrogen systems and carbon removal technologies were not included in CRESOM, so that transition pathways towards carbon neutral could not be described.

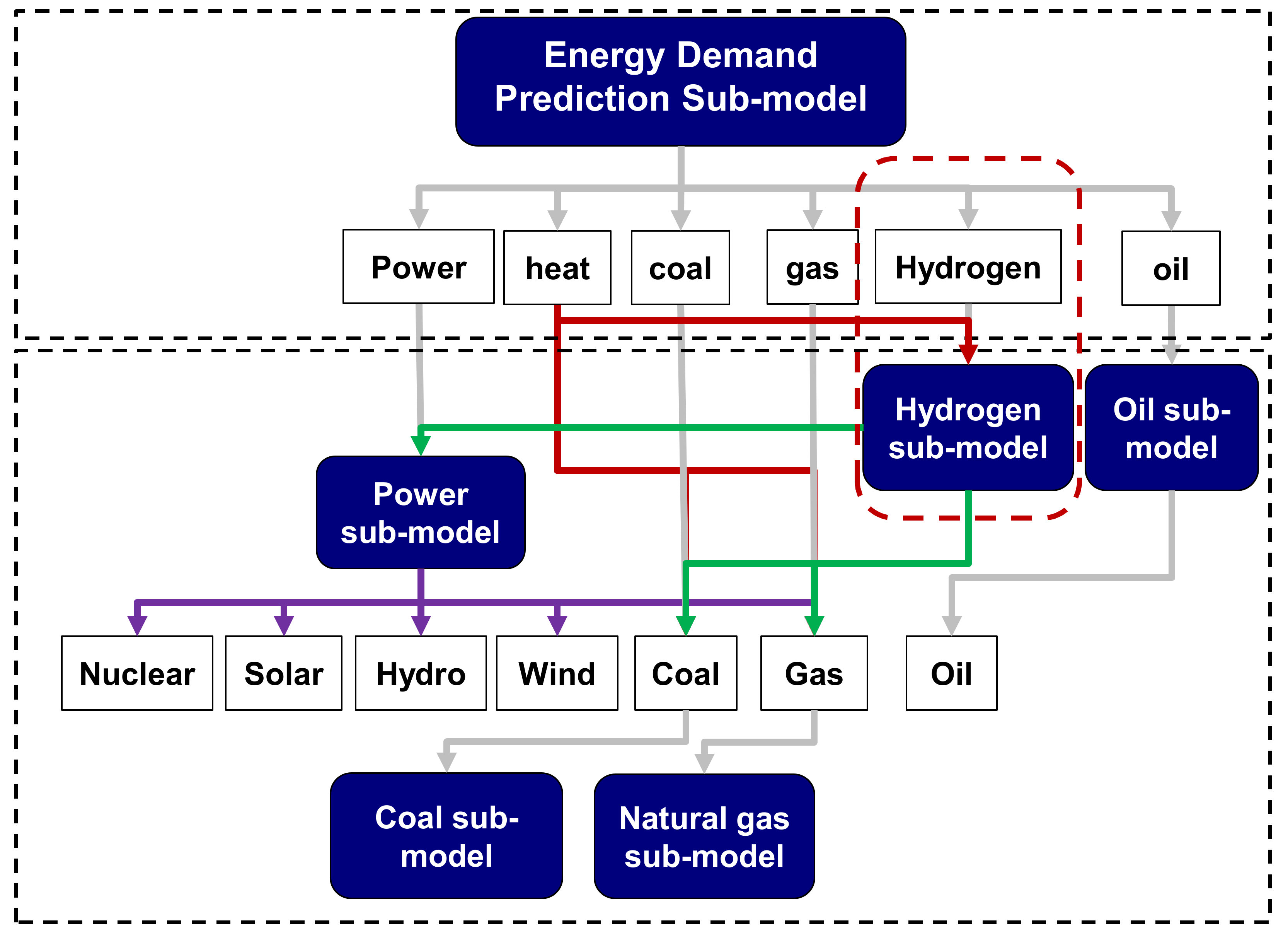

In this paper, CRESOM is applied and improved to carry out this analysis. Firstly, a hydrogen system planning sub-model with multiple production options, including fossil fuels and non-fossil power, is developed and integrated into the existing model, so that the improved CRESOM can describe transition pathways towards carbon neutral. Secondly, representative transition pathways are designed applying low carbon technologies and varying degrees of strategies mentioned above, namely improving electrification and hydrogen penetration in final use, raising carbon prices and applying carbon removal technologies. Thirdly, the optimal energy system planning and transition costs in all pathways are obtained and compared using improved CRESOM, and impacts of technology choice on hydrogen production are analyzed.

China is taken as a case study, the largest energy consumer with growing energy demand. In 2019, China accounted for 24% of global primary energy consumption and 29% of global carbon emissions, and fossil fuels still accounted for 85% in primary energy supply in China [

2]. According to BP Outlook 2019 [

32], total energy demand in China would keep growing with an average annual growth rate of 1.1% from 2017 to 2040. China has pledged to carry out low carbon transition and reduce carbon emissions. In stated policies, non-fossil energy would account for 15%, 20%, and 50%of primary energy demand in 2020, 2030 and 2050 respectively [

13].

The novelty of this paper can be summarized as three points compared with previous studies. Firstly, an infrastructure-based hydrogen supply system model is developed and integrated with coal, natural gas, oil and power systems, so that impacts of hydrogen system planning on existing energy systems can be analyzed, and impacts of hydrogen production technology is pointed out. Secondly, a bottom-up and infrastructure-based model describing entire energy systems can be applied to obtain energy system planning strategies with least costs. Thirdly, energy system transition costs and corresponding planning strategies oriented from various transition targets are pointed out, with higher resolution compared to other models.

This paper is organized as follows. In

Section 2, the methodology is illustrated. In

Section 3, the design of all scenarios is described. In

Section 4, results are demonstrated and discussed. In

Section 5, the main conclusions are summarized.

3. Scenarios and Assumptions

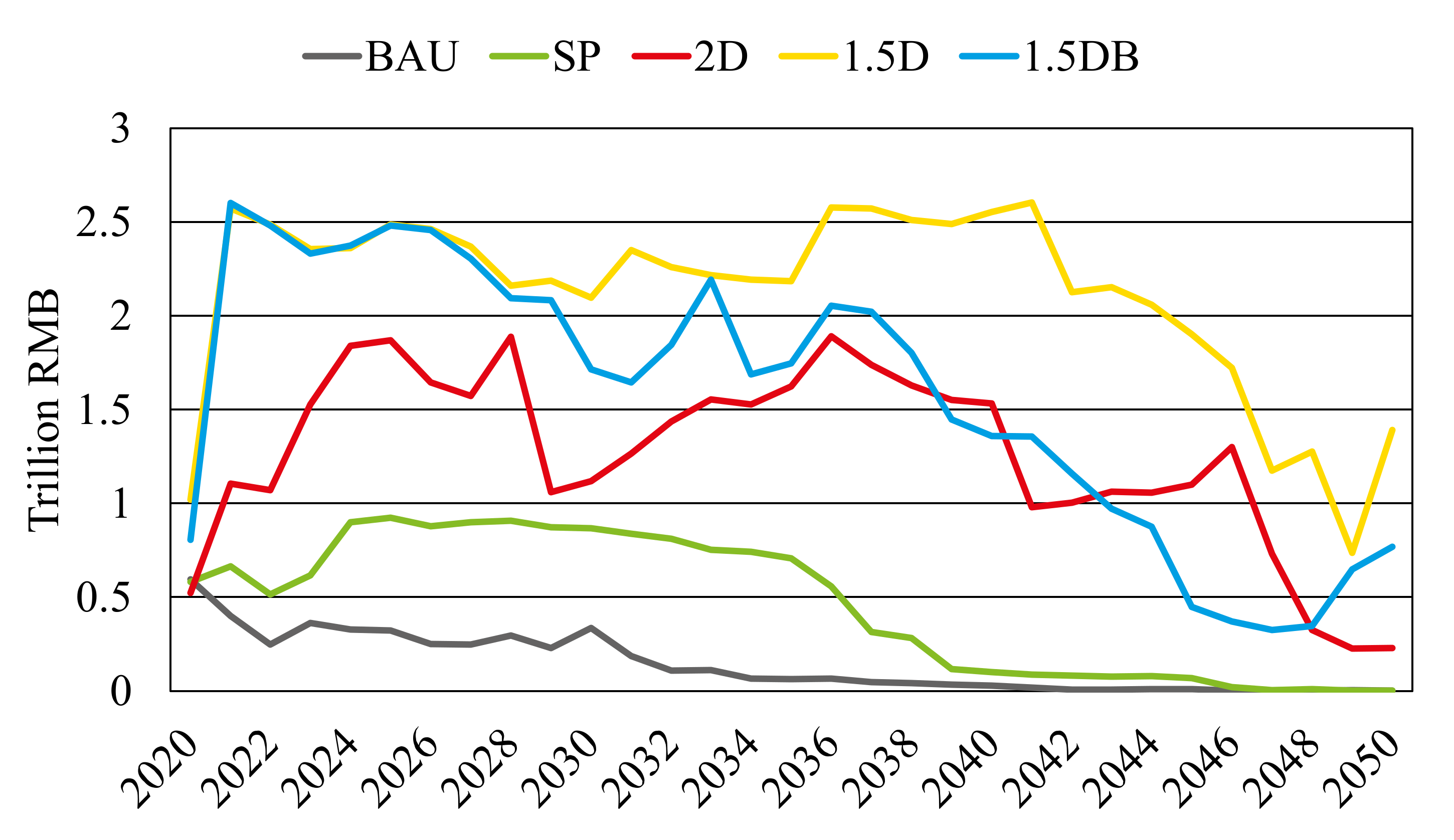

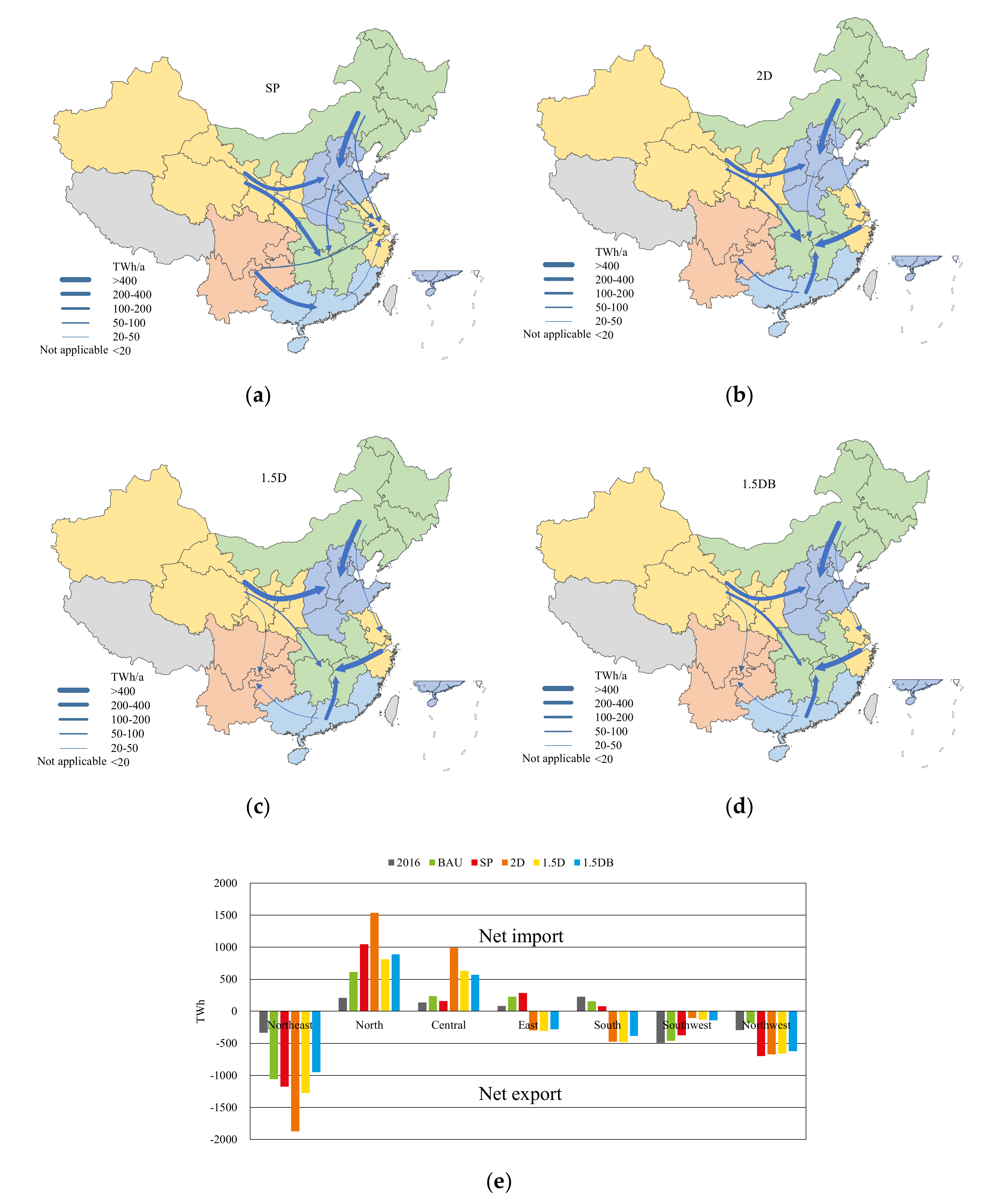

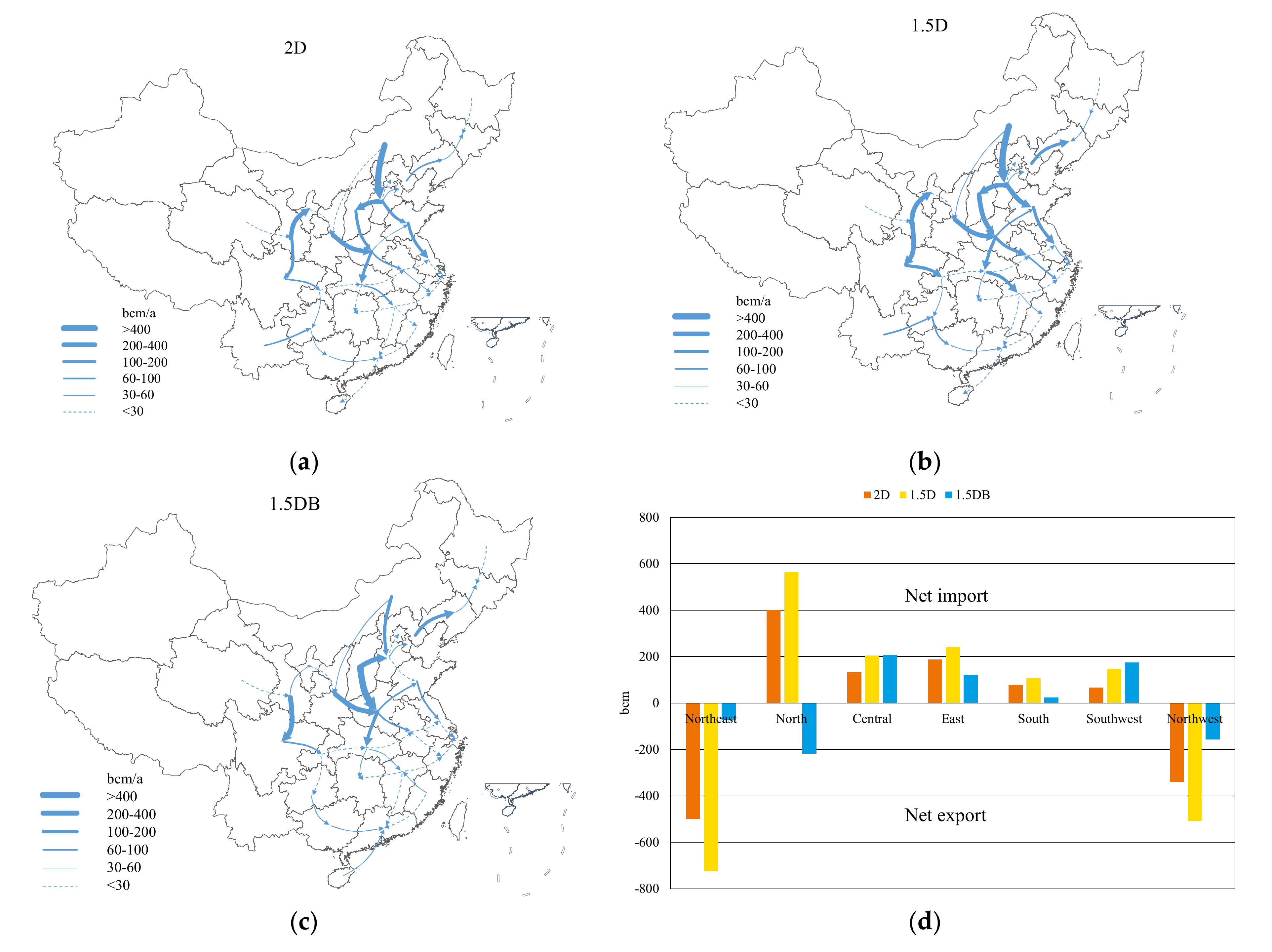

Five representative transition pathways are designed to fulfill different transition targets. The business-as-usual scenario (BAU) describes the pathway which does not necessarily to fulfill any transition targets, whilst the low carbon transition is still under way due to efficiency improvement and cost reduction along with technology progress. The stated policy scenario (SP) describes the pathway to achieve stated policies by improving non-fossil and natural gas shares in primary energy supply. In current policies, non-fossil energy is expected to account for 50% by 2050, and natural gas is expected to account for 20% by 2030. The 2-degree scenario (2D) describes the pathway to achieve the target of “well below 2 degree” in the Paris Agreement, which indicates to reach carbon neutral by 2070. In the 2D scenario, carbon emissions are assumed to be cut by 72% by 2050 compared to emissions in 2016, because the planning period in CRESOM only covers from 2016 to 2050. The 1.5-degree scenario (1.5D) describes the pathway to achieve the target of “1.5 degree” in the Paris Agreement, which indicates to reach carbon neutral by 2050. Consequently, in the 1.5D scenario, carbon emissions are expected to decrease by 98% by 2050 compared to 2016, and all hydrogen is produced from non-fossil power. Although some emissions would still be retained, carbon neutral would still be achieved because of the carbon sink. In view that hydrogen can be produced from fossil fuels, and carbon neutral can still be achieved applying carbon capture and storage, the 1.5-degree scenario with blue hydrogen (1.5DB) is designed for comparison, and all hydrogen is produced from fossil fuels with CCS facilities.

Various transition targets are fulfilled by implementing transition strategies with varying degree in these five pathways, as shown in

Table 1. The forecast input in CRESOM are consistent in all scenarios, which indicates that energy efficiency improvement and costs reduction along with technology progress are consistent in all scenarios, as shown in

Appendix B. Transition strategies in all scenarios are designed by varying scenario input. Low, moderate, medium, high, and aggressive represent different degrees of fuel replacement in end-use sectors. Aggressive transition approaches would result in higher penetration of power and hydrogen in final energy demand, and quantitative indicators in these scenarios are shown in

Table 2.

In the SP scenario, current policies indicate to improve power and natural gas shares in final energy use to partly replace coal and oil, and carbon prices are set to improve renewable power shares in power generation to raise non-fossil energy shares in the primary energy supply. Hydrogen and CCS are assumed not to be widely applied in the SP scenario according to current policies.

In the 2D scenario, more aggressive strategies are expected to be implemented than the SP scenario to cut emissions by 72% by 2050. Besides further improving electrification and raising carbon prices, hydrogen is expected to be widely used in end-use sectors to replace fossil fuels, and CCS is set as an optional technology in power sectors. Deploying CCS depends on whether it can reduce overall costs, which basically reflects the comparison of CCS costs and carbon prices.

In the 1.5D scenario, nearly all energy demand in end-use sectors are fulfilled by power and hydrogen in order to cut most carbon emissions in final consumption. All hydrogen is produced from power, and higher carbon prices would facilitate CCS deployment in power sectors to cut all carbon emissions in power generation.

In the 1.5DB scenario, all hydrogen is produced from fossil fuels, and CCS is applied in hydrogen production sectors in order to cut all emissions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}