Transparency in Global Agribusiness: Transforming Brazil’s Soybean Supply Chain Based on Companies’ Accountability

Abstract

:1. Introduction

2. Theoretical Framework

2.1. Soybean Agribusiness

2.2. Agribusiness Companies’ Accountability

3. Methods

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Segment | Market Size in 2020 (in USD Billion) | Proportion of the Whole Market (%) | Source |

|---|---|---|---|

| Seeds | 2.0 | 2.3 | BRL 8 billion worth market [36] |

| Machinery | 2.3 | 2.6 | BRL 11 billion worth market, 85% soybean [42] |

| Fertilisers | 4.7 | 5.4 | Soybean represents 47% of Brazil’s fertiliser market worth USD 10.2 billion [37] * |

| Agrochemicals | 8.1 | 9.3 | Soybean represents 71% of Brazil’s pesticides market worth USD 11.5 billion (Santos & Glass, 2018) |

| Farming | 28.6 | 32.9 | Considering 114.8 tons produced in 2020 [43] |

| Trading | 41.2 | 47.5 | USD 34.7 billion exported plus domestic market [44] |

| Total | 86.9 | 100 |

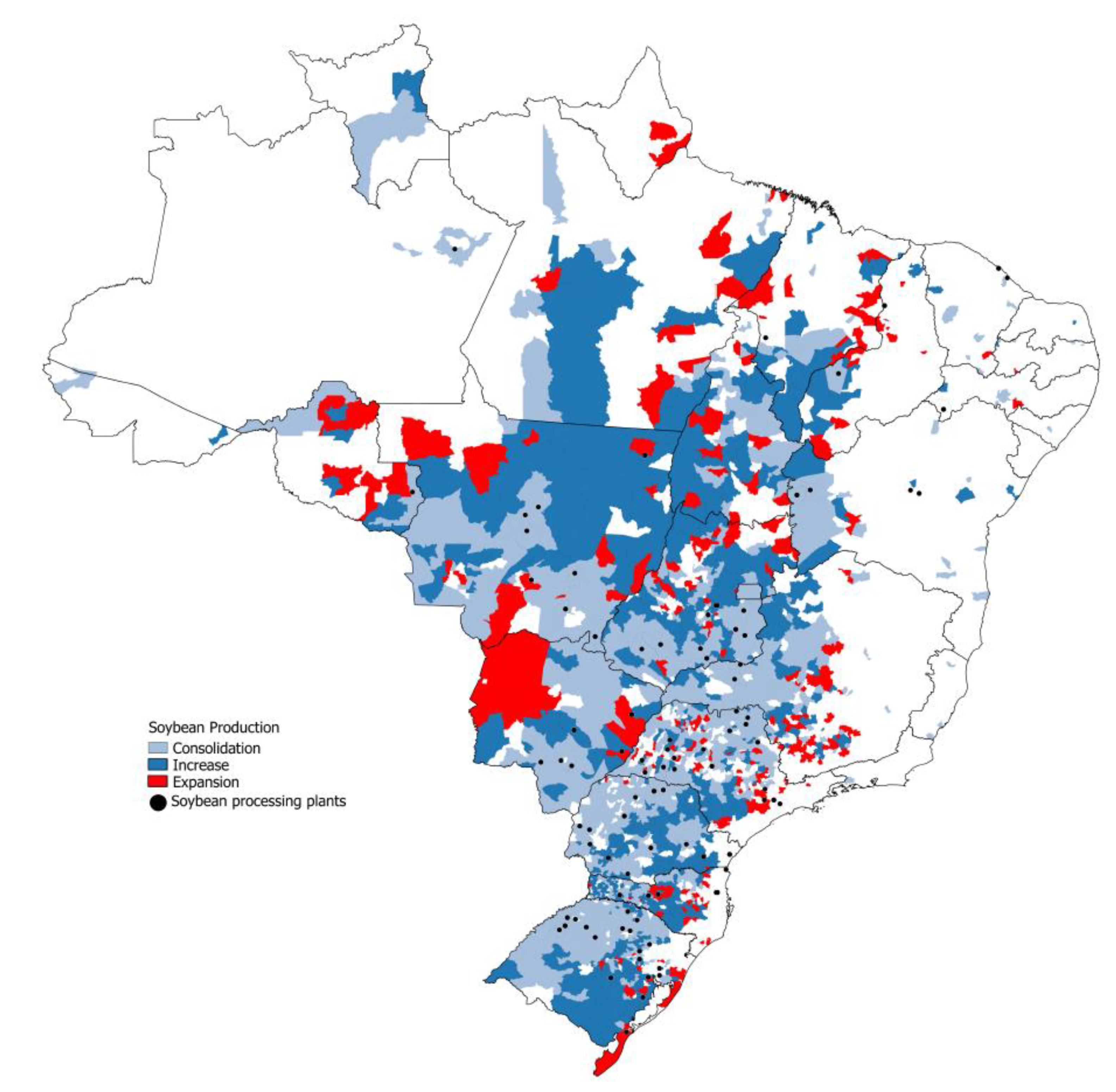

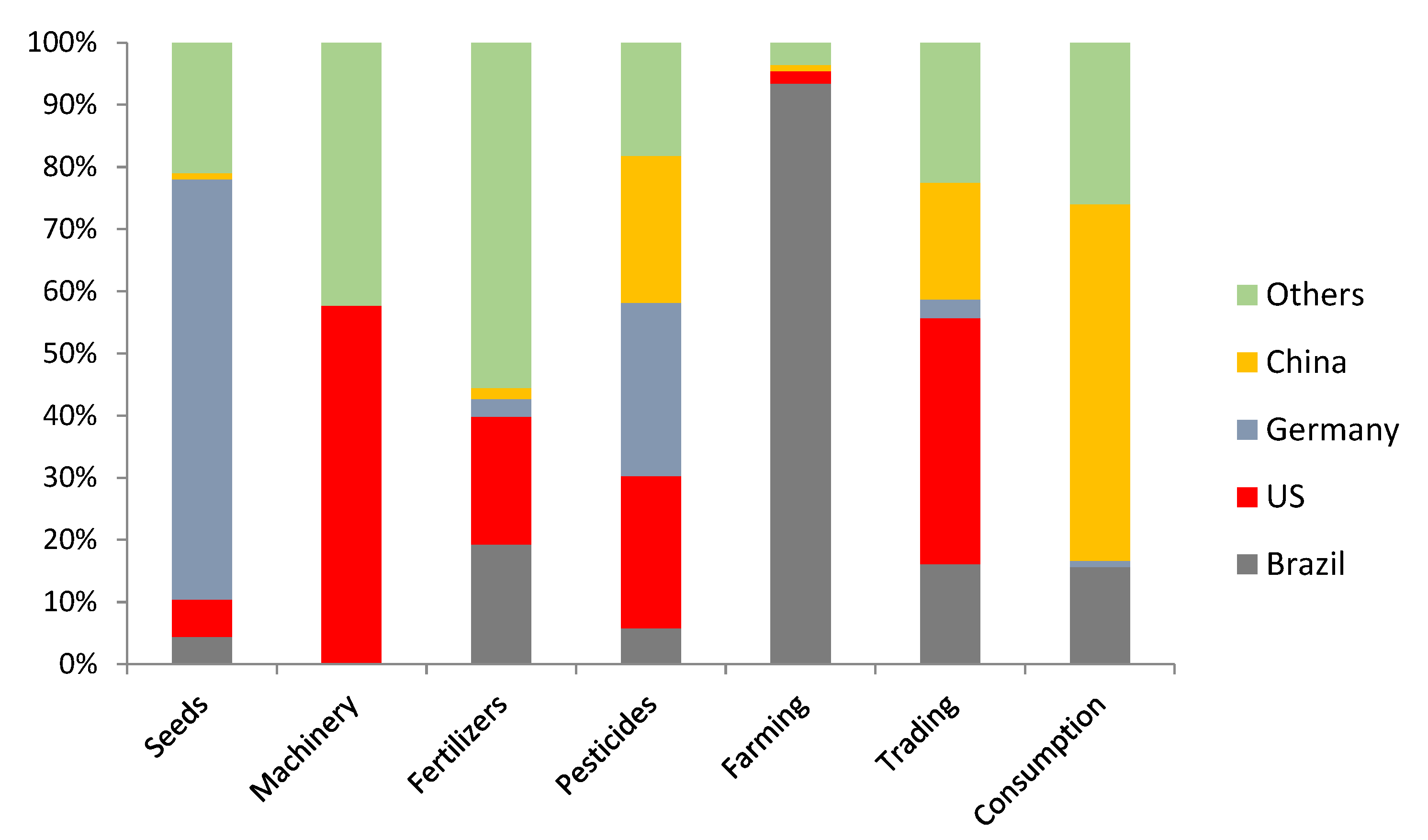

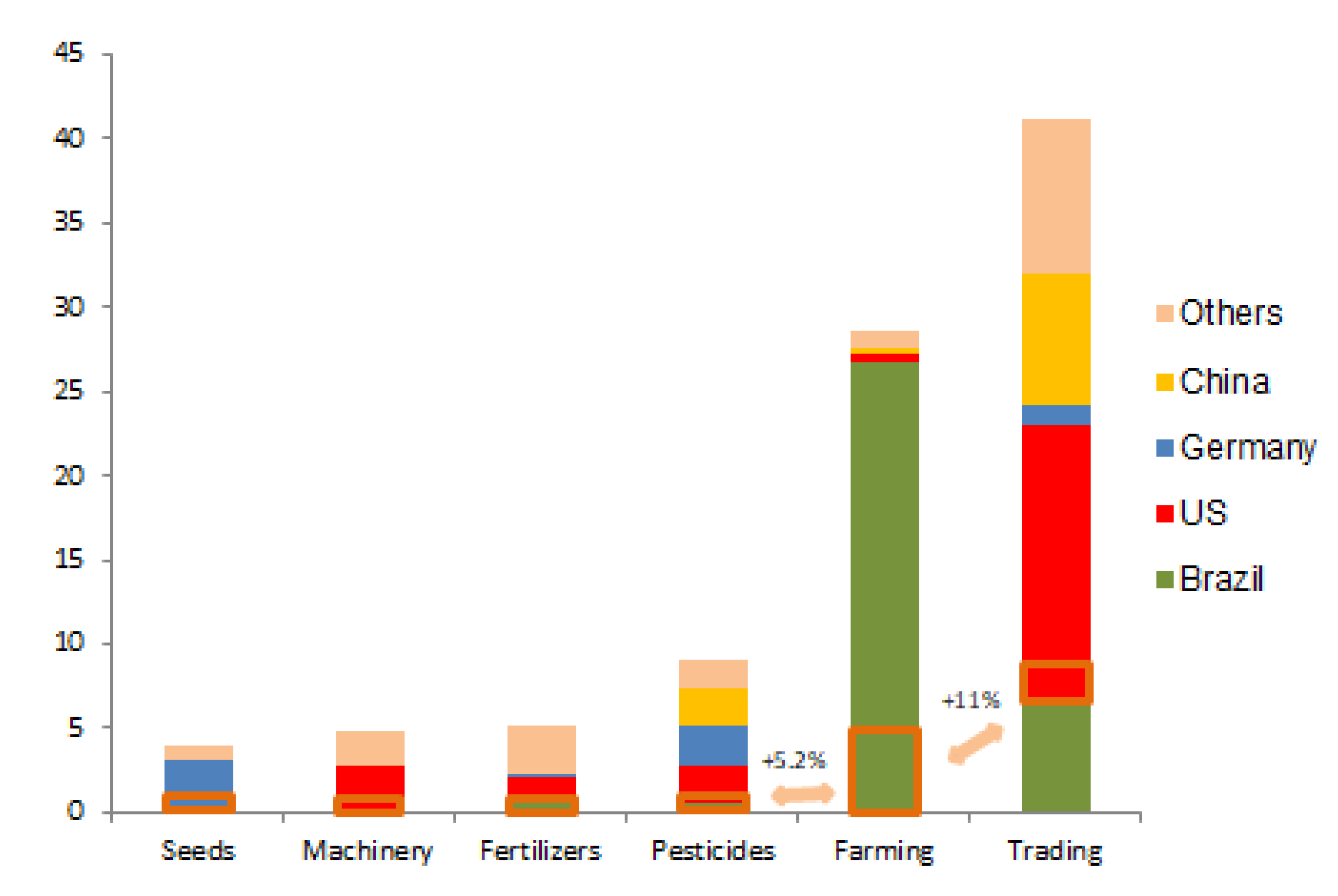

4. Results

4.1. Key Stakeholders Based on Market Shares

4.2. Trade-Offs Based on Market Size

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- de Janvry, A.; Sadoulet, E. Using agriculture for development: Supply- and demand-side approaches. World Dev. 2020, 133, 105003. [Google Scholar] [CrossRef]

- FAO. The State of Food and Agriculture, 1st ed.; FAO: Rome, Italy, 2019. [Google Scholar]

- Thomé, K.M.; Cappellesso, G.; Ramos, E.L.A.; Duarte, S.C.d.L. Food Supply Chains and Short Food Supply Chains: Coexistence conceptual framework. J. Clean. Prod. 2021, 278, 123207. [Google Scholar] [CrossRef]

- Godar, J.; Suavet, C.; Gardner, T.A.; Dawkins, E.; Meyfroidt, P. Balancing detail and scale in assessing the sustainability of commodity supply chains. Environ. Res. Lett. 2016, 11, 1–12. [Google Scholar] [CrossRef] [Green Version]

- Boström, M.; Jönsson, A.M.; Lockie, S.; Mol, A.P.; Oosterveer, P. Sustainable and responsible supply chain governance: Challenges and opportunities. J. Clean. Prod. 2015, 107, 1–7. [Google Scholar] [CrossRef]

- Husted, B.W.; de Sousa-Filho, J.M. The impact of sustainability governance, country stakeholder orientation, and country risk on environmental, social, and governance performance. J. Clean. Prod. 2017, 155, 93–102. [Google Scholar] [CrossRef]

- Koberg, E.; Longoni, A. A systematic review of sustainable supply chain management in global supply chains. J. Clean. Prod. 2018, 207, 1084–1098. [Google Scholar] [CrossRef]

- Jia, F.; Peng, S.; Green, J.; Koh, L.; Chen, X. Soybean supply chain management and sustainability: A systematic literature review. J. Clean. Prod. 2020, 255, 120254. [Google Scholar] [CrossRef]

- Gibbs, H.K.; Rausch, L.; Munger, J.; Schelly, I.; Morton, D.C.; Noojipady, P.; Soares-Filho, B.; Barreto, P.; Micol, L.; Walker, N.F. Brazil’s Soy Moratorium. Science 2015, 347, 377–378. [Google Scholar] [CrossRef] [PubMed]

- Spring, J. Exclusive: European Investors Threaten Brazil Divestment over Deforestation; Reuters: London, UK, 2020; Available online: https://www.reuters.com/article/us-brazil-environment-divestment-exclusi/exclusive-european-investors-threaten-brazil-divestment-over-deforestation-idUSKBN23Q1MU (accessed on 20 December 2020).

- Green, J.M.H.; Croft, S.A.; Durán, A.P.; Balmford, A.P.; Burgess, N.D.; Fick, S. Linking global drivers of agricultural trade to on-the-ground impacts on biodiversity. Proc. Natl. Acad. Sci. USA 2019, 116, 23202–23208. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Kamali, F.P.; Meuwissen, M.P.M.; de Boer, I.J.M.; van Middelaar, C.E.; Moreira, A.; Lansink, A.G.J.M.O. Evaluation of the environmental, economic, and social performance of soybean farming systems in southern Brazil. J. Clean. Prod. 2017, 142, 385–394. [Google Scholar] [CrossRef]

- Negash, M.; Lemma, T.T. Institutional pressures and the accounting and reporting of environmental liabilities. Bus. Strategy Environ. 2020, 29, 1941–1960. [Google Scholar] [CrossRef]

- Gualandris, J.; Klassen, R.; Vachon, S.; Kalchschmidt, M.G.M. Sustainable evaluation and verification in supply chains: Aligning and leveraging accountability to stakeholders. J. Oper. Manag. 2015, 38, 1–13. [Google Scholar] [CrossRef] [Green Version]

- Cattelan, A.; Dall’Agnol, A. The rapid soybean growth in Brazil. OCL 2018, 25, D102. [Google Scholar] [CrossRef] [Green Version]

- Lima, M.; Junior, C.A.S.; da Rausch, L.; Gibbs, H.K.; Johann, J.A. Demystifying sustainable soy in Brazil. Land Use Policy 2019, 82, 349–352. [Google Scholar] [CrossRef]

- Medina, G.; Santos, A. Curbing enthusiasm for Brazilian agribusiness: The use of actor-specific assessments to transform sustainable development on the ground. Appl. Geogr. 2017, 85, 101–112. [Google Scholar] [CrossRef]

- CPT. Conflitos no campo no Brasil 2020. Available online: https://www.cptnacional.org.br/publicacoes-2/destaque/5664-conflitos-no-campo-brasil-2020 (accessed on 20 June 2021).

- Ferrante, L.; Fearnside, P.M. Brazil’s new president and ‘ruralists’ threaten Amazonia’s environment, traditional peoples and the global climate. Environ. Conserv. 2019, 46, 261–263. [Google Scholar] [CrossRef]

- Villén-Pérez, S.; Moutinho, P.; Nóbrega, C.C.; De Marco, P. Brazilian Amazon gold: Indigenous land rights under risk. Elem. Sci. Anthr. 2020, 8. [Google Scholar] [CrossRef]

- Stabile, M.C.C.; Guimarães, A.L.; Silva, D.S.; Ribeiro, V.; Macedo, M.N.; Coe, M.T.; Pinto, E.; Moutinho, P.; Alencar, A. Solving Brazil’s land use puzzle: Increasing production and slowing Amazon deforestation. Land Use Policy 2020, 91, 104362. [Google Scholar] [CrossRef]

- Soterroni, A.C.; Ramos, F.M.; Mosnier, A.; Fargione, J.; Andrade, P.R.; Baumgarten, L.; Pirker, J.; Obersteiner, M.; Kraxner, F.; Câmara, G.; et al. Expanding the soy moratorium to Brazil’s Cerrado. Sci. Adv. 2019, 5. [Google Scholar] [CrossRef] [Green Version]

- Rajão, R.; Soares-Filho, B.; Nunes, F.; Börner, J.; Machado, L.; Assis, D.; Oliveira, A.; Pinto, L.; Ribeiro, V.; Rausch, L.; et al. The rotten apples of Brazil’s agribusiness. Science 2020, 369, 246–248. [Google Scholar] [CrossRef]

- Håkansson, H.; Snehota, I. No business is an island: The network concept of business strategy. Scand. J. Manag. 1989, 5, 187–200. [Google Scholar] [CrossRef]

- Ahumada, O.; Villalobos, J.R. Application of planning models in the agri-food supply chain: A review. Eur. J. Oper. Res. 2009, 196, 1–20. [Google Scholar] [CrossRef]

- Lambert, D.; Cooper, M. Issues in Supply Chain Management in Indian Agriculture. Ind. Mark. Manag. 2000, 29, 65–83. [Google Scholar] [CrossRef]

- dos Santos, R.R.; Guarnieri, P. Social gains for artisanal agroindustrial producers induced by cooperation and collaboration in agri-food supply chain. Soc. Responsib. J. 2020. [Google Scholar] [CrossRef]

- Bager, S.L.; Lambin, E.F. Sustainability strategies by companies in the global coffee sector. Bus. Strateg. Environ. 2020. [Google Scholar] [CrossRef]

- Schnittfeld, N.L.; Busch, T. Sustainability Management within Supply Chains—A Resource Dependence View. Bus. Strategy Environ. 2016, 25, 337–354. [Google Scholar] [CrossRef]

- Krishnan, R.; Agarwal, R.; Bajada, C.; Arshinder, K. Redesigning a food supply chain for environmental sustainability—An analysis of resource use and recovery. J. Clean. Prod. 2019, 242, 118374. [Google Scholar] [CrossRef]

- Castro, N.R.; Swart, J. Building a roundtable for a sustainable hazelnut supply chain. J. Clean. Prod. 2017, 168, 1398–1412. [Google Scholar] [CrossRef]

- Seitanidi, M.M.; Crane, A. Implementing CSR Through Partnerships: Understanding the Selection, Design and Institutionalisation of Nonprofit-Business Partnerships. J. Bus. Ethics 2009, 85, 413–429. [Google Scholar] [CrossRef]

- Solér, C.; Sandström, C.; Skoog, H. How can high-biodiversity coffee make it to the mainstream market? The performativity of voluntary sustainability standards and outcomes for coffee diversification. Environ. Manag. 2017, 59, 230–248. [Google Scholar] [CrossRef] [Green Version]

- Medaets, J.P.P.; Fornazier, A.; Thomé, K.M. Transition to sustainability in agrifood systems: Insights from Brazilian trajectories. J. Rural. Stud. 2020, 76, 1–11. [Google Scholar] [CrossRef]

- Scherer, F.M.; Ross, D. Industrial Market Structure and Economic Performance; Houghton-Mifflin: Boston, MA, USA, 1990. [Google Scholar]

- Anprosem. Associação Nacional dos Produtores de Sementes; Aprosem. 2020. Available online: https://anprosem.com.br/site/ (accessed on 20 December 2020).

- Anda. Anuário Estatístico; Associação Nacional para Difusão de Adubos: São Paulo, Brasil, 2020; Available online: http://anda.org.br/arquivos/ (accessed on 20 December 2020).

- Aenda. “Associados da Associação Brasileira dos Defensivos Genéricos,” Associação Brasileira dos Defensivos Genéricos (AENDA). 2020. Available online: https://www.aenda.org.br/ (accessed on 20 December 2020).

- Anfavea. Anuario da Indústria Automobilística Brasileira; Associação Nacional dos Fabricantes de Veículos Automotores: São Paulo, Brasil, 2020; Available online: https://doi.org/10.1017/CBO9781107415324.004 (accessed on 20 December 2020).

- Aprosoja. Associação dos Produtores de Soja; Aprosoja. 2020. Available online: https://aprosojabrasil.com.br/ (accessed on 1 August 2020).

- Cepea. PIB do Agronegócio—Dados de 1994 a 2019; Cepea: Piracicaba, Brazil, 2020; Available online: https://www.cepea.esalq.usp.br/br/pib-do-agronegocio-brasileiro.aspx (accessed on 20 December 2020).

- Tiengo, R. Setor de máquinas agrícolas tem alta de 15% e fatura R$ 2,38 bilhões no 1o trimestre. 2020. Available online: https://g1.globo.com/sp/ribeirao-preto-franca/agrishow/2017/noticia/setor-de-maquinas-agricolas-tem-alta-de-15-e-fatura-r-238-bilhoes-no-1-trimestre-de-2017.ghtml (accessed on 20 December 2020).

- Conab. Acompanhamento da Safra Brasileira: Cana-de-Açúcar; Companhia Nacional de Abastecimento (Conab): Brasília, Brasil, 2020. [Google Scholar]

- Escher, F.; Wilkinson, J. A economia política do complexo Soja-Carne Brasil-China. Rev. Econ. Sociol. Rural. 2019, 57, 656–678. [Google Scholar] [CrossRef]

- Marin, A.; Stubrin, L. Innovation in natural resources: New opportunities and new challenges The case of the Argentinian seed industry. In Innovation. 2015, 1. Issue 1. Available online: http://www.merit.unu.edu/publications/wppdf/2015/wp2015-015.pdf (accessed on 20 December 2020).

- Sindiveg. Associadas; Sindicato Nacional Da Indústria de Produtos Para Defesa Vegetal (Sindiveg). 2020. Available online: https://sindiveg.org.br/associadas/ (accessed on 20 December 2020).

- Hage, F.; Peixoto, M.; Filho, J.V. Aquisição de Terras por Estrangeiros no Brasil: Uma Avaliação Jurídica e Econômica. Núcleo de Estudos e Pesquisas do Senado. 20 December 2012. Available online: http://www.senado.gov.br/senado/conleg/textos_discussao/TD114-FabioHage-MarcusPeixoto-JoseEustaquio.pdf (accessed on 20 December 2020).

- Trase. Transparent Supply Chains for Sustainable Economies; 2020. Available online: https://trase.earth/ (accessed on 24 March 2020).

- Santos, M.; Glass, V. Atlas do Agronegócio: Fatos e Números Sobre as Corporações que Controlam o Que Comemos; Fundação Heinrich Böll: Berlin, Germany, 2018. [Google Scholar]

- Gurzawska, A. Towards Responsible and Sustainable Supply Chains—Innovation, Multi-stakeholder Approach and Governance. Philos. Manag. 2019, 19, 267–295. [Google Scholar] [CrossRef] [Green Version]

- Ferrari, V.; Pacheco, M. Propriedade intelectual e inovações tecnológicas na indústria de sementes: Discussões sobre os conflitos judiciais entre a Monsanto e os agricultores brasileiros. Rev. Estud. Soc. 2019, 20, 89–103. [Google Scholar] [CrossRef]

- Schielein, J.; Börner, J. Recent transformations of land-use and land-cover dynamics across different deforestation frontiers in the Brazilian Amazon. Land Use Policy 2018, 76, 81–94. [Google Scholar] [CrossRef]

- Illukpitiya, P.; Yanagida, J.F. Farming vs forests: Trade-off between agriculture and the extraction of non-timber forest products. Ecol. Econ. 2010, 69, 1952–1963. [Google Scholar] [CrossRef]

- Nascimento, N.; West TA, P.; Börner, J.; Ometto, J. What Drives Intensification of Land Use at Agricultural Frontiers in the Brazilian Amazon? Evidence from a Decision Game. Forests 2019, 10, 464. [Google Scholar] [CrossRef] [Green Version]

- OECD; FAO. OECD-FAO Guidance for Responsible Agricultural Supply Chains; FAO: Rome, Italy, 2013. [Google Scholar]

- Klimek, B.; Bjørkhaug, H. Norwegian Agro-Food Attracting Private Equity Capital; Varieties of Capitalism—Varieties of Financialisation? Sociol. Rural. 2015, 57, 171–190. [Google Scholar] [CrossRef] [Green Version]

- Coronel, D.A. Processo de desindustrialização da economia brasileira e possibilidade de reversão. Rev. Econ. Agronegócio 2020, 17, 389–398. [Google Scholar] [CrossRef]

| Segments | Organisations |

|---|---|

| Seeds | Brazilian Association of Soybean Seeds Producers (Abrass) |

| Fertilisers | National Fertilisers Association (ANDA) |

| Agrochemicals | Brazilian Association of Generic Pesticides (Aenda) |

| Machinery | National Manufacturers Association of Motor Vehicles (Anfavea) |

| Farmers | Soybean Producers Association (Aprosoja) |

| 2015 | 2020 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Segment | Company | Home Country | Total | Brazil | Total | Brazil | US | Germany | China | Others | |

| Seeds | Technology | Bayer (Monsanto) | Germany | 88.8 | 0.0 | 90.0 | 0.0 | 0.0 | 90.0 | 0.0 | 0.0 |

| Pioneer/Corteva | United States | 5.8 | 0.0 | 6.0 | 0.0 | 6.0 | 0.0 | 0.0 | 0.0 | ||

| Others | Multinational | 5.4 | 0.0 | 4.0 | 0.0 | 0.0 | 0.0 | 0.0 | 4.0 | ||

| Production | GDM and others | Multinational | 50.0 | 0.0 | 75.0 | 0.0 | 6.0 | 29.0 | 2.0 | 38.0 | |

| TMG and others | Brazil | 50.0 | 16.5 | 25.0 | 8.7 | 0.0 | 16.3 | 0.0 | 0.0 | ||

| Subtotal | 100.0 | 16.5 | 100.0 | 8.7 | 6.0 | 67.6 | 1.0 | 21.0 | |||

| Machinery | Tractors | AGCO Massey | United States | 25.6 | 0.0 | 16.9 | 0.0 | 16.9 | 0.0 | 0.0 | 0.0 |

| AGCO Valtra | United States | 22.3 | 0.0 | 13.4 | 0.0 | 13.4 | 0.0 | 0.0 | 0.0 | ||

| CNH Case | Italy | 6.4 | 0.0 | 9.4 | 0.0 | 0.0 | 0.0 | 0.0 | 9.4 | ||

| CNH New Holland | Italy | 19.3 | 0.0 | 23.1 | 0.0 | 0.0 | 0.0 | 0.0 | 23.1 | ||

| John Deere | United States | 22.5 | 0.0 | 36.7 | 0.0 | 36.7 | 0.0 | 0.0 | 0.0 | ||

| Agrale S.A | Brazil | 3.8 | 3.8 | 0.4 | 0.4 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Combines | AGCO Massey | United States | 10.3 | 0.0 | 6.4 | 0.0 | 6.4 | 0.0 | 0.0 | 0.0 | |

| AGCO Valtra | EU | 3.2 | 0.0 | 0.9 | 0.0 | 0.9 | 0.0 | 0.0 | 0.0 | ||

| CNH Case | Italy | 15.5 | 0.0 | 18.5 | 0.0 | 0.0 | 0.0 | 0.0 | 18.5 | ||

| CNH New Holland | Italy | 31.0 | 0.0 | 33.5 | 0.0 | 0.0 | 0.0 | 0.0 | 33.5 | ||

| John Deere | United States | 40.0 | 0.0 | 40.7 | 0.0 | 40.7 | 0.0 | 0.0 | 0.0 | ||

| Subtotal | 100.0 | 1.9 | 100.0 | 0.2 | 57.5 | 0.0 | 0.0 | 42.3 | |||

| Fertilisers | Phosphorus | Vale (now Mosaic) | United States | 29.6 | 29.6 | 29.7 | 0.0 | 29.7 | 0.0 | 0.0 | 0.0 |

| Anglo American | UK | 5.9 | 0.0 | 6.7 | 0.0 | 0.0 | 0.0 | 0.0 | 6.7 | ||

| Others | Brazil/Multinationals | 20.6 | 10.3 | 19.6 | 17.5 | 0.0 | 0.0 | 0.0 | 2.1 | ||

| Imported | 44.0 | 0.0 | 44.0 | 0.0 | 7.5 | 0.0 | 7.0 | 29.5 | |||

| Potassium | Vale (now Mosaic) | United States | 8.0 | 8.0 | 5.0 | 0.0 | 5.0 | 0.0 | 0.0 | 0.0 | |

| Imported | 92.0 | 0.0 | 95.0 | 0.0 | 0.0 | 11.4 | 0.0 | 83.6 | |||

| Manufacture | Yara | Norway | 20.5 | 20.5 | 25.0 | 0.0 | 0.0 | 0.0 | 0.0 | 25.0 | |

| Mosaic/ADM | United States | 19.0 | 19.0 | 20.0 | 0.0 | 20.0 | 0.0 | 0.0 | 0.0 | ||

| Dreyfus | France | 1.5 | 1.5 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Nutrien | Canada | 0.0 | 0.0 | 10.0 | 0.0 | 0.0 | 0.0 | 0.0 | 10.0 | ||

| Fertipar | Brazil | 17.7 | 17.7 | 15.0 | 15.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Heringer (undergoing judicial recovery) | Brazil (56%) | 13.3 | 7.4 | 6.0 | 3.3 | 0.0 | 0.0 | 0.0 | 2.7 | ||

| Regional | Brazil | 8.2 | 8.0 | 7.0 | 6.5 | 0.0 | 0.0 | 0.0 | 0.5 | ||

| Outros | Brazil/Multinationals | 17.3 | 8.6 | 17.0 | 5.0 | 0.0 | 0.0 | 0.0 | 12.0 | ||

| Subtotal | 100.0 | 33.5 | 100.0 | 19.2 | 20.5 | 2.9 | 1.8 | 55.6 | |||

| Pesticides | Syngenta/ChemChina | China | 21.2 | 0.0 | 18.6 | 0.0 | 0.0 | 0.0 | 18.6 | 0.0 | |

| Bayer | Germany | 15.3 | 0.0 | 15.7 | 0.0 | 0.0 | 15.7 | 0.0 | 0.0 | ||

| Basf | Germany | 12.4 | 0.0 | 9.2 | 0.0 | 0.0 | 9.2 | 0.0 | 0.0 | ||

| UPL | India | 0.0 | 0.0 | 8.9 | 0.0 | 0.0 | 0.0 | 0.0 | 8.9 | ||

| FMC | United States | 7.1 | 0.0 | 8.5 | 0.0 | 8.5 | 0.0 | 0.0 | 0.0 | ||

| Corteva | United States | 0.0 | 0.0 | 4.0 | 0.0 | 4.0 | 0.0 | 0.0 | 0.0 | ||

| DuPont | United States | 6.5 | 0.0 | 4.0 | 0.0 | 4.0 | 0.0 | 0.0 | 0.0 | ||

| Dow | United States | 5.6 | 0.0 | 3.0 | 0.0 | 3.0 | 0.0 | 0.0 | 0.0 | ||

| Others | Multinational | 26.6 | 0.0 | 22.3 | 0.0 | 5.0 | 3.0 | 5.0 | 9.3 | ||

| Nortox | Brazil | 2.3 | 2.3 | 2.7 | 2.7 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Ourofino | Brazil | 1.0 | 1.0 | 2.1 | 2.1 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Small companies | Brazil | 2.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Subtotal | 100.0 | 4.3 | 100.0 | 5.8 | 24.5 | 27.9 | 23.6 | 18.2 | |||

| Farming | Subtotal | 100.0 | 93.4 | 100.0 | 93.4 | 2.0 | 0.0 | 1.0 | 3.6 | ||

| Trading | Cargill | United States | 12.4 | 0.0 | 11.4 | 0.0 | 11.4 | 0.0 | 0.0 | 0.0 | |

| Bunge | United States | 15.7 | 0.0 | 9.4 | 0.0 | 9.4 | 0.0 | 0.0 | 0.0 | ||

| ADM | United States | 10.0 | 0.0 | 7.8 | 0.0 | 7.8 | 0.0 | 0.0 | 0.0 | ||

| Dreyfus | France | 5.4 | 0.0 | 7.5 | 0.0 | 0.0 | 0.0 | 0.0 | 7.5 | ||

| Cofco | China | 0.0 | 0.0 | 3.8 | 0.0 | 0.0 | 0.0 | 3.8 | 0.0 | ||

| Others | Multinational | 25.8 | 0.0 | 44.0 | 0.0 | 11.0 | 3.0 | 15.0 | 15.0 | ||

| Amaggi | Brazil | 4.1 | 44.0 | 6.6 | 6.6 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Coamo | Brazil | 4.5 | 4.5 | 2.3 | 2.3 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Cutrale | Brazil | 0.1 | 0.1 | 1.7 | 1.7 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Bianchini | Brazil | 3.5 | 3.5 | 1.2 | 1.2 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Caramuru | Brazil | 2.3 | 2.3 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Granol | Brazil | 3.5 | 3.5 | 0.2 | 0.2 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Comigo | Brazil | 1.7 | 1.7 | 0.1 | 0.1 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Algar Agro | Brazil | 1.7 | 1.7 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Others | Brazil | 9.3 | 9.3 | 2.9 | 2.9 | 0.0 | 0.0 | 0.0 | 0.0 | ||

| Subtotal | 100.0 | 30.7 | 100.0 | 16.1 | 39.6 | 3.0 | 18.8 | 22.5 | |||

| Current Situation | Projection | Outcome | ||||

|---|---|---|---|---|---|---|

| Expansion into agricultural frontiers | Area with soybeans in Brazil (million ha) | Gross income (USD billion) | Measure (Curb deforestation) | Area with soybeans (million ha) | % | Income (USD billion) |

| Amazon | 36.4 | 28.6 | 100% | 4.5 | 12.4 | 3.5 |

| Matopiba | 36.4 | 28.6 | 100% | 5.7 | 15.7 | 4.5 |

| Increased market share | Current domestic share | Gross income generated (USD billion) | Measure (increase in domestic market share by) | Targeted market share | % | Income generated (USD billion) |

| Trading | 16.0 | 41.2 | 11% | 27.0 | 6.6 | 4.5 |

| Whole chain | 7.1 | 86.9 | 5.2% | 12.3 | 6.2 | 4.5 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Medina, G.; Thomé, K. Transparency in Global Agribusiness: Transforming Brazil’s Soybean Supply Chain Based on Companies’ Accountability. Logistics 2021, 5, 58. https://doi.org/10.3390/logistics5030058

Medina G, Thomé K. Transparency in Global Agribusiness: Transforming Brazil’s Soybean Supply Chain Based on Companies’ Accountability. Logistics. 2021; 5(3):58. https://doi.org/10.3390/logistics5030058

Chicago/Turabian StyleMedina, Gabriel, and Karim Thomé. 2021. "Transparency in Global Agribusiness: Transforming Brazil’s Soybean Supply Chain Based on Companies’ Accountability" Logistics 5, no. 3: 58. https://doi.org/10.3390/logistics5030058

APA StyleMedina, G., & Thomé, K. (2021). Transparency in Global Agribusiness: Transforming Brazil’s Soybean Supply Chain Based on Companies’ Accountability. Logistics, 5(3), 58. https://doi.org/10.3390/logistics5030058