Bio-inspired Machine Learning for Distributed Confidential Multi-Portfolio Selection Problem

Abstract

:1. Introduction

2. Problem Formulation

2.1. Building Blocks of Portfolio Selection

2.1.1. Expected Return

2.1.2. Risk

2.1.3. Total Investment

2.1.4. Total Transaction Cost

2.1.5. Cardinality Constraint

2.2. Portfolio Selection Models

2.2.1. Mean-Variance Model

2.2.2. Efficient Frontier Model

2.2.3. Sharpe Ratio Model

3. Distributed Beetle Antennae Search (DBAS)

3.1. BAS Formulation and Algorithm

| Algorithm 1 BAS Algorithm. |

|

3.2. DBAS Formulation and Algorithm

3.2.1. DBAS Updating Criteria

| Algorithm 2 DBAS Algorithm. |

3.2.2. DBAS Privacy Policy

4. Simulation Results

4.1. Stock Data

- Software: MATLAB;

- System: MacBook Pro;

- Processor: 2.2 GHz;

- Cores: 6–Core Intel Core i7;

- Memory: 6 GB 2400 MHz DDR4;

- Graphics: Radeon Pro 555X 4 GB.

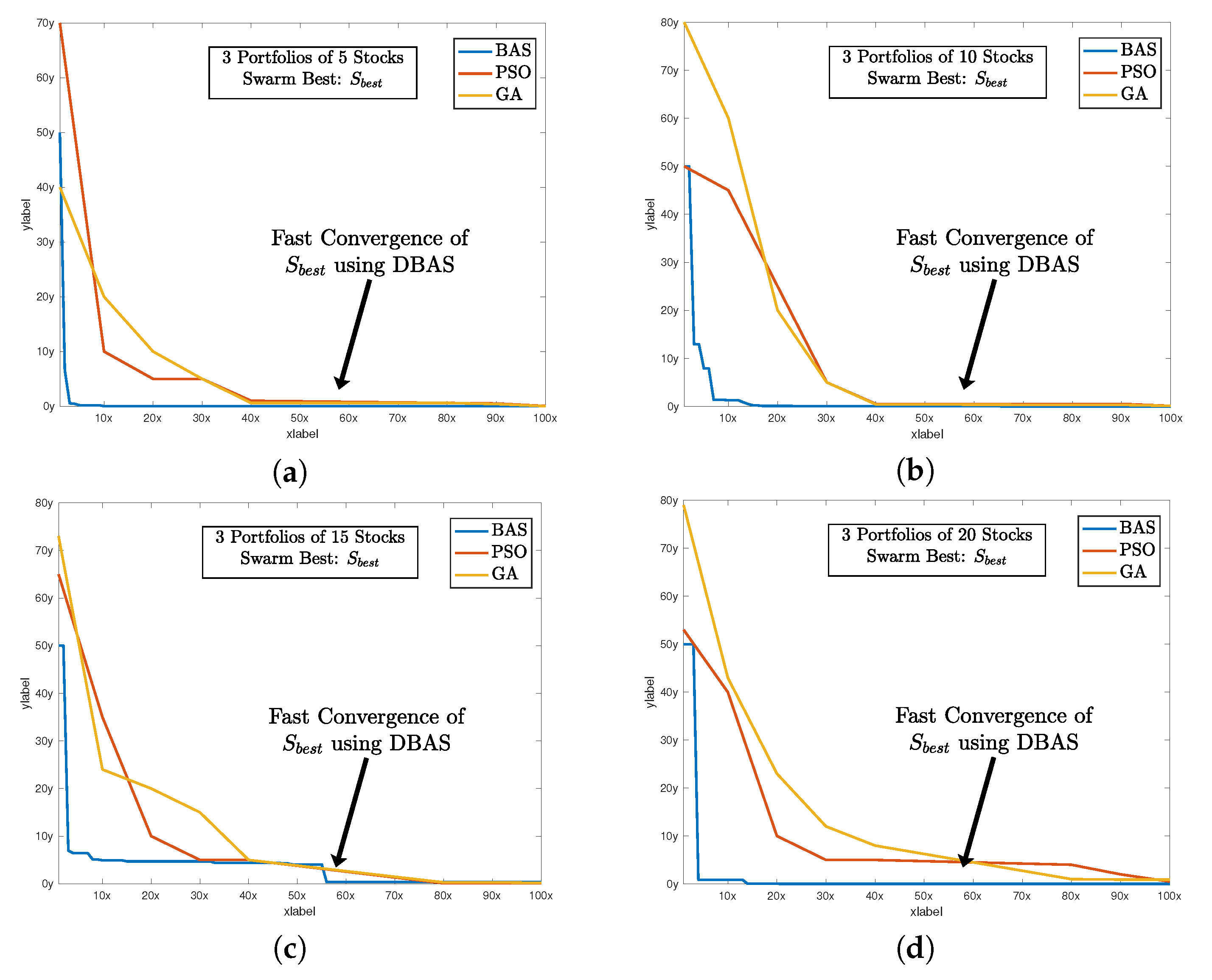

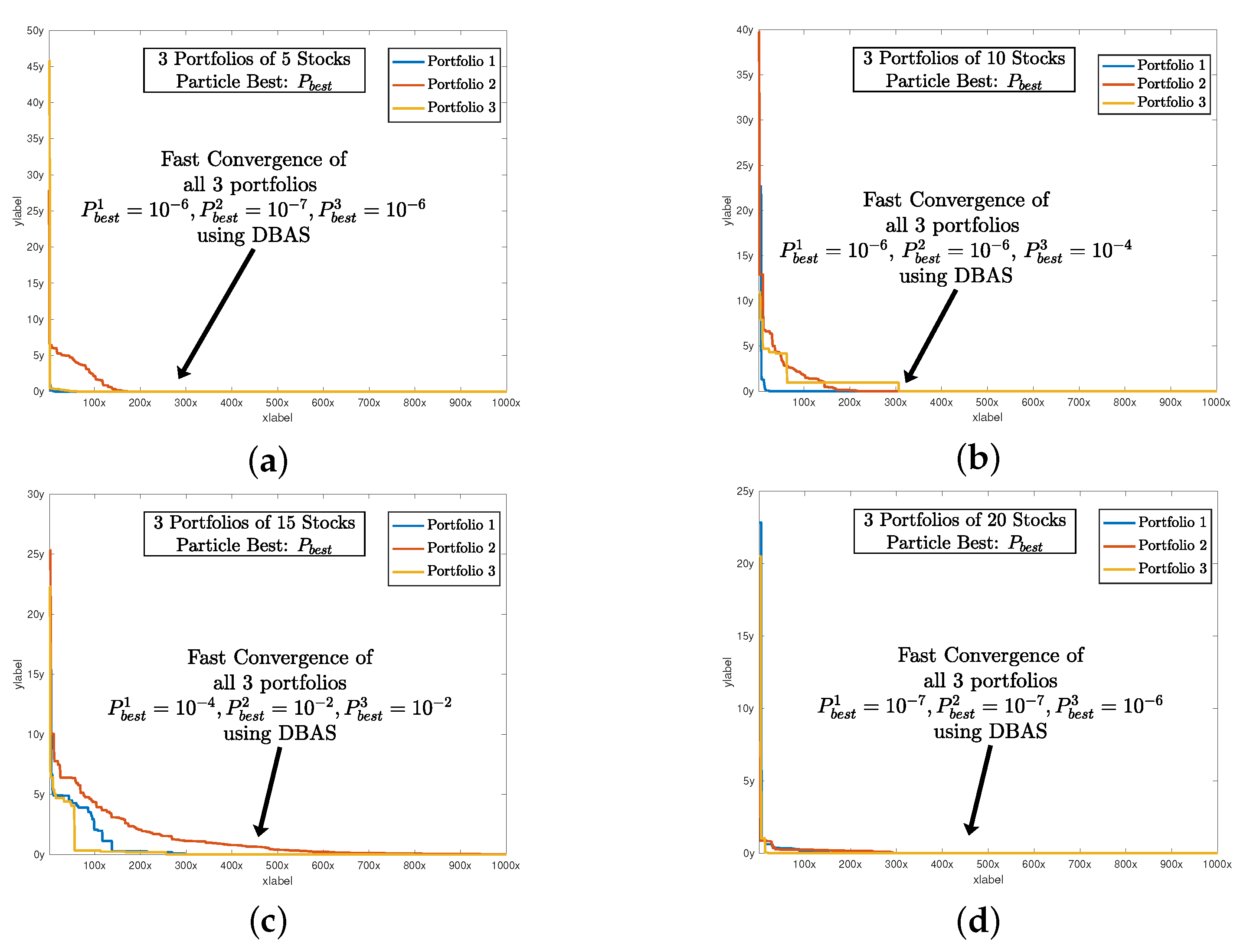

4.2. Three Portfolios of Five Stock Companies

4.3. Three Portfolios of 10 Stock Companies

4.4. Three Portfolios of 15 Stock Companies

4.5. Three Portfolios of 20 Stock Companies

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Bienstock, D. Computational study of a family of mixed-integer quadratic programming problems. Math. Program. 1996, 74, 121–140. [Google Scholar] [CrossRef]

- Ertenlice, O.; Kalayci, C.B. A survey of swarm intelligence for portfolio optimization: Algorithms and applications. Swarm Evol. Comput. 2018, 39, 36–52. [Google Scholar] [CrossRef]

- Perrin, S.; Roncalli, T. Machine learning optimization algorithms & portfolio allocation. In Machine Learning for Asset Management: New Developments and Financial Applications; Wiley: Hoboken, NJ, USA, 2020; pp. 261–328. [Google Scholar]

- Ta, V.D.; Liu, C.M.; Tadesse, D.A. Portfolio optimization-based stock prediction using long-short term memory network in quantitative trading. Appl. Sci. 2020, 10, 437. [Google Scholar] [CrossRef]

- Leung, M.F.; Wang, J. Minimax and Biobjective Portfolio Selection Based on Collaborative Neurodynamic Optimization. IEEE Trans. Neural Netw. Learn. Syst. 2021, 32, 2825–2836. [Google Scholar] [CrossRef] [PubMed]

- Kadry, S.; Smaili, K. A design and implementation of a wireless iris recognition attendance management system. Inf. Technol. Control. 2007, 36, 323–329. [Google Scholar]

- Kadry, S. On the generalization of probabilistic transformation method. Appl. Math. Comput. 2007, 190, 1284–1289. [Google Scholar] [CrossRef]

- Katsikis, V.N. Computational methods in portfolio insurance. Appl. Math. Comput. 2007, 189, 9–22. [Google Scholar] [CrossRef]

- Zhang, Y.; Gong, H.; Yang, M.; Li, J.; Yang, X. Stepsize Range and Optimal Value for Taylor–Zhang Discretization Formula Applied to Zeroing Neurodynamics Illustrated via Future Equality-Constrained Quadratic Programming. IEEE Trans. Neural Netw. Learn. Syst. 2019, 30, 959–966. [Google Scholar] [CrossRef]

- Liao, B.; Zhang, Y. Different Complex ZFs Leading to Different Complex ZNN Models for Time-Varying Complex Generalized Inverse Matrices. IEEE Trans. Neural Netw. Learn. Syst. 2014, 25, 1621–1631. [Google Scholar] [CrossRef]

- Katsikis, V.N. An Alternative Computational Method for Finding the Minimum-Premium Insurance Portfolio. In In Proceedings of the AIP Conference Proceedings, Penang, Malaysia, 10–12 April 2016; AIP Publishing LLC: Melville, NY, USA, 2016; Volume 1738, p. 480020. [Google Scholar]

- Stanimirović, P.S.; Katsikis, V.N.; Li, S. Integration enhanced and noise tolerant ZNN for computing various expressions involving outer inverses. Neurocomputing 2019, 329, 129–143. [Google Scholar] [CrossRef]

- Lai, Z.R.; Dai, D.Q.; Ren, C.X.; Huang, K.K. A Peak Price Tracking-Based Learning System for Portfolio Selection. IEEE Trans. Neural Netw. Learn. Syst. 2018, 29, 2823–2832. [Google Scholar] [CrossRef] [PubMed]

- Stanimirović, P.S.; Ćirić, M.; Katsikis, V.N.; Li, C.; Ma, H. Outer and (b, c) inverses of tensors. Linear Multilinear Algebra 2020, 68, 940–971. [Google Scholar] [CrossRef]

- Brajević, I.; Ignjatović, J. An upgraded firefly algorithm with feasibility-based rules for constrained engineering optimization problems. J. Intell. Manuf. 2019, 30, 2545–2574. [Google Scholar] [CrossRef]

- Brajević, I.; Stanimirović, P. An improved chaotic firefly algorithm for global numerical optimization. Int. J. Comput. Intell. Syst. 2018, 12, 131–148. [Google Scholar] [CrossRef]

- Lai, Z.R.; Dai, D.Q.; Ren, C.X.; Huang, K.K. Radial Basis Functions With Adaptive Input and Composite Trend Representation for Portfolio Selection. IEEE Trans. Neural Netw. Learn. Syst. 2018, 29, 6214–6226. [Google Scholar] [CrossRef] [PubMed]

- O’Cinneide, C.; Scherer, B.; Xu, X. Pooling Trades in a Quantitative Investment Process. J. Portf. Manag. 2006, 32, 33–43. [Google Scholar] [CrossRef]

- Liao, B.; Hua, C.; Can, X.; Katsikis, V.N.; Li, S. Complex Noise-Resistant Zeroing Neural Network for Computing Complex Time-Dependent Lyapunov Equation. Mathematics 2022, 10, 2817. [Google Scholar] [CrossRef]

- Ji, R.; Lejeune, M.A. Risk-budgeting multi-portfolio optimization with portfolio and marginal risk constraints. Ann. Oper. Res. 2018, 262, 547–578. [Google Scholar] [CrossRef]

- Savelsbergh, M.W.P.; Stubbs, R.A.; Vandenbussche, D. Multiportfolio Optimization: A Natural Next Step. In Handbook of Portfolio Construction; Guerard, J.B., Ed.; Springer US: Boston, MA, USA, 2010; pp. 565–581. [Google Scholar] [CrossRef]

- Iancu, D.; Trichakis, N. Fairness and Efficiency in Multiportfolio Optimization. Oper. Res. 2014, 62, 1285–1301. [Google Scholar] [CrossRef]

- Jing, F. Information pooling game in multi-portfolio optimization. Contrib. Game Theory Manag. 2017, 10, 27–41. [Google Scholar]

- Zhang, G.; Zhang, Q. Multiportfolio optimization with CVaR risk measure. J. Data Inf. Manag. 2019, 1, 91–106. [Google Scholar] [CrossRef] [Green Version]

- Yu, G.; Cai, X.; Long, D.Z. Multi-Portfolio Optimization: A Fairness-Aware Target-Oriented Model 2020. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3740629 (accessed on 30 July 2022).

- Khan, A.H.; Li, S.; Luo, X. Obstacle avoidance and tracking control of redundant robotic manipulator: An RNN-based metaheuristic approach. IEEE Trans. Ind. Informatics 2019, 16, 4670–4680. [Google Scholar] [CrossRef]

- Khan, A.H.; Cao, X.; Li, S.; Katsikis, V.N.; Liao, L. BAS-ADAM: An ADAM based approach to improve the performance of beetle antennae search optimizer. IEEE/CAA J. Autom. Sin. 2020, 7, 461–471. [Google Scholar] [CrossRef]

- Khan, A.T.; Li, S.; Cao, X. Control framework for cooperative robots in smart home using bio-inspired neural network. Measurement 2021, 167, 108253. [Google Scholar] [CrossRef]

- Khan, A.T.; Li, S. Human guided cooperative robotic agents in smart home using beetle antennae search. Sci. China Inf. Sci. 2021, 65, 122204. [Google Scholar] [CrossRef]

- Khan, A.T.; Li, S.; Li, Z. Obstacle avoidance and model-free tracking control for home automation using bio-inspired approach. In Advanced Control for Applications: Engineering and Industrial Systems; Wiley: Hoboken, NJ, USA, 2021; p. e.63. [Google Scholar]

- Khan, A.T.; Li, S.; Zhou, X. Trajectory optimization of 5-link biped robot using beetle antennae search. IEEE Trans. Circuits Syst. II Express Briefs 2021, 68, 3276–3280. [Google Scholar] [CrossRef]

- Khan, A.T.; Cao, X.; Li, Z.; Li, S. Enhanced Beetle Antennae Search with Zeroing Neural Network for online solution of constrained optimization. Neurocomputing 2021, 447, 294–306. [Google Scholar] [CrossRef]

- Zivkovic, M.; Bacanin, N.; Venkatachalam, K.; Nayyar, A.; Djordjevic, A.; Strumberger, I.; Al-Turjman, F. COVID-19 cases prediction by using hybrid machine learning and beetle antennae search approach. Sustain. Cities Soc. 2021, 66, 102669. [Google Scholar] [CrossRef]

- Wu, Q.; Shen, X.; Jin, Y.; Chen, Z.; Li, S.; Khan, A.H.; Chen, D. Intelligent beetle antennae search for UAV sensing and avoidance of obstacles. Sensors 2019, 19, 1758. [Google Scholar] [CrossRef]

- Li, X.; Jiang, H.; Niu, M.; Wang, R. An enhanced selective ensemble deep learning method for rolling bearing fault diagnosis with beetle antennae search algorithm. Mech. Syst. Signal Process. 2020, 142, 106752. [Google Scholar] [CrossRef]

- Huang, J.; Duan, T.; Zhang, Y.; Liu, J.; Zhang, J.; Lei, Y. Predicting the permeability of pervious concrete based on the beetle antennae search algorithm and random forest model. Adv. Civ. Eng. 2020, 2020, 8863181. [Google Scholar] [CrossRef]

- Sun, Y.; Zhang, J.; Li, G.; Wang, Y.; Sun, J.; Jiang, C. Optimized neural network using beetle antennae search for predicting the unconfined compressive strength of jet grouting coalcretes. Int. J. Numer. Anal. Methods Geomech. 2019, 43, 801–813. [Google Scholar] [CrossRef]

- Khan, A.T.; Cao, X.; Li, S.; Katsikis, V.N.; Brajevic, I.; Stanimirovic, P.S. Fraud detection in publicly traded US firms using Beetle Antennae Search: A machine learning approach. Expert Syst. Appl. 2021, 191, 116148. [Google Scholar] [CrossRef]

- Khan, A.T.; Cao, X.; Brajevic, I.; Stanimirovic, P.S.; Katsikis, V.N.; Li, S. Non-linear Activated Beetle Antennae Search: A Novel Technique for Non-Convex Tax-Aware Portfolio Optimization Problem. Expert Syst. Appl. 2022, 197, 116631. [Google Scholar] [CrossRef]

- Khan, A.H.; Cao, X.; Xu, B.; Li, S. Beetle Antennae Search: Using Biomimetic Foraging Behaviour of Beetles to Fool a Well-Trained Neuro-Intelligent System. Biomimetics 2022, 7, 84. [Google Scholar] [CrossRef]

- Liao, B.; Han, L.; He, Y.; Cao, X.; Li, J. Prescribed-Time Convergent Adaptive ZNN for Time-Varying Matrix Inversion under Harmonic Noise. Electronics 2022, 11, 1636. [Google Scholar] [CrossRef]

- Liao, B.; Huang, Z.; Cao, X.; Li, J. Adopting Nonlinear Activated Beetle Antennae Search Algorithm for Fraud Detection of Public Trading Companies: A Computational Finance Approach. Mathematics 2022, 10, 2160. [Google Scholar] [CrossRef]

- Khan, A.T.; Cao, X.; Li, Z.; Li, S. Evolutionary Computation Based Real-time Robot Arm Path-planning Using Beetle Antennae Search. EAI Endorsed Trans. Robot. 2022, 1, 1–10. [Google Scholar] [CrossRef]

- Chen, Z.; Walters, J.; Xiao, G.; Li, S. An Enhanced GRU Model With Application to Manipulator Trajectory Tracking. EAI Endorsed Trans. Robot. 2022, 1, 1–11. [Google Scholar] [CrossRef]

- Ijaz, M.U.; Khan, A.T.; Li, S. Bio-inspired BAS: Run-time Path-planning And The Control of Differential Mobile Robot. EAI Endorsed Trans. Robot. 2022, 1, 1–10. [Google Scholar] [CrossRef]

- Hameed, S.W. Peaks Detector Algorithm after CFAR for Multiple Targets Detection. EAI Endorsed Trans. Robot. 2022, 1, 1–7. [Google Scholar] [CrossRef]

- Khan, A.T.; Cao, X.; Li, S. Dual Beetle Antennae Search system for optimal planning and robust control of 5-link biped robots. J. Comput. Sci. 2022, 60, 101556. [Google Scholar] [CrossRef]

- Khan, A.H.; Cao, X.; Li, S. Obstacle avoidance based decision making and management of articulated agents. In Management and Intelligent Decision-Making in Complex Systems: An Optimization-Driven Approach; Springer: Berlin/Heidelberg, Germany, 2021; pp. 1–29. [Google Scholar]

- Khan, A.H. Neural Network and Metaheuristic Based Learning and Control of Articulated Robotic Agents. Ph.D. Thesis, Hong Kong Polytechnic University, Hong Kong, China, 2021. [Google Scholar]

- Khan, A.T.; Cao, X.; Li, S.; Hu, B.; Katsikis, V.N. Quantum beetle antennae search: A novel technique for the constrained portfolio optimization problem. Sci. China Inf. Sci. 2020, 64, 152204. [Google Scholar] [CrossRef]

- Khan, A.H.; Cao, X.; Katsikis, V.N.; Stanimirović, P.; Brajević, I.; Li, S.; Kadry, S.; Nam, Y. Optimal portfolio management for engineering problems using nonconvex cardinality constraint: A computing perspective. IEEE Access 2020, 8, 57437–57450. [Google Scholar] [CrossRef]

- Chen, T.; Zhu, Y.; Teng, J. Beetle swarm optimisation for solving investment portfolio problems. J. Eng. 2018, 2018, 1600–1605. [Google Scholar] [CrossRef]

- Katsikis, V.N.; Mourtas, S.D.; Stanimirović, P.S.; Li, S.; Cao, X. Time-Varying Mean-Variance Portfolio Selection under Transaction Costs and Cardinality Constraint Problem via Beetle Antennae Search Algorithm (BAS), Proceedings of the Operations Research Forum, Online, 31 August–3 September; Springer: Berlin/Heidelberg, Germany, 2021; Volume 2, pp. 1–26. [Google Scholar]

- Khan, A.R.; Khan, A.T.; Salik, M.; Bakhsh, S. An optimally configured HP-GRU model using hyperband for the control of wall following robot. Int. J. Robot. Control Syst. 2021, 1, 66–74. [Google Scholar] [CrossRef]

- Zhu, H.; Wang, Y.; Wang, K.; Chen, Y. Particle Swarm Optimization (PSO) for the constrained portfolio optimization problem. Exp. Syst. Appl. 2011, 38, 10161–10169. [Google Scholar] [CrossRef]

- Jiang, X.; Li, S. BAS: Beetle Antennae Search Algorithm for Optimization Problems. arXiv 2017, arXiv:1710.10724. [Google Scholar] [CrossRef]

- Mohamed, A.W.; Hadi, A.A.; Mohamed, A.K. Gaining-sharing knowledge based algorithm for solving optimization problems: A novel nature-inspired algorithm. Int. J. Mach. Learn. Cybern. 2020, 11, 1501–1529. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Name | Notation | Values (Default) |

|---|---|---|

| Antennae Length | d | |

| Step Size | ||

| Personal Antennae Length | ||

| Global Antennae Length | ||

| Step Multiplier |

| Companies 1–5 | GOOGL | MSFT | AMZN | FB | IBM |

|---|---|---|---|---|---|

| Companies 6–10 | A | AA | AAU | AABA | AAC |

| Companies 11–15 | AADR | AAL | AAMC | AAME | AAN |

| Companies 16–20 | NCA | NCI | QAT | QD | CODI |

| Companies 20–25 | EMR | EMXC | FET | FC | ABBV |

| Companies: 5 | Companies: 10 | |||||

|---|---|---|---|---|---|---|

| Portfolio 1 | Portfolio 2 | Portfolio 3 | Portfolio 1 | Portfolio 2 | Portfolio 3 | |

| n | 5 | 5 | 5 | 7 | 8 | 9 |

| DBAS: | ||||||

| sgn | ||||||

| Some Additional Parameters: | ||||||

| T | 500 | 500 | ||||

| D | 3 | 3 | ||||

| K | 5 | 5 | ||||

| Eval. | 4500 | 4500 | ||||

| Companies: 15 | Companies: 20 | |||||

| Portfolio 1 | Portfolio 2 | Portfolio 3 | Portfolio 1 | Portfolio 2 | Portfolio 3 | |

| n | 15 | 12 | 10 | 15 | 20 | 18 |

| DBAS: | ||||||

| sgn | ||||||

| Some Additional Parameters: | ||||||

| T | 500 | 500 | ||||

| D | 3 | 3 | ||||

| K | 5 | 5 | ||||

| Eval. | 4500 | 4500 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Khan, A.T.; Cao, X.; Liao, B.; Francis, A. Bio-inspired Machine Learning for Distributed Confidential Multi-Portfolio Selection Problem. Biomimetics 2022, 7, 124. https://doi.org/10.3390/biomimetics7030124

Khan AT, Cao X, Liao B, Francis A. Bio-inspired Machine Learning for Distributed Confidential Multi-Portfolio Selection Problem. Biomimetics. 2022; 7(3):124. https://doi.org/10.3390/biomimetics7030124

Chicago/Turabian StyleKhan, Ameer Tamoor, Xinwei Cao, Bolin Liao, and Adam Francis. 2022. "Bio-inspired Machine Learning for Distributed Confidential Multi-Portfolio Selection Problem" Biomimetics 7, no. 3: 124. https://doi.org/10.3390/biomimetics7030124

APA StyleKhan, A. T., Cao, X., Liao, B., & Francis, A. (2022). Bio-inspired Machine Learning for Distributed Confidential Multi-Portfolio Selection Problem. Biomimetics, 7(3), 124. https://doi.org/10.3390/biomimetics7030124