The Role of Local Citizen Energy Communities in the Road to Carbon-Neutral Power Systems: Outcomes from a Case Study in Portugal

Abstract

:1. Introduction

- Discusses the required market designs of future electricity markets with near 100% renewable generation;

- Presents the current and future key role of CECs towards carbon neutrality;

- Presents a case-study that uses real-data to illustrate the current role of CECs, considering self-consumption, microgrid trades and local agreements.

2. The Future of European Electricity Markets

- Reliable, supporting enough generation and flexibility to avoid shortages;

- Flexible, considering several options for temporal, spatial and sectoral flexibility on both supply and demand sides;

- Economically efficient, contributing to increase competition and ensuring low prices to consumers in a transparent approach;

- Carbon-neutral, leading to attractive investments in renewable generation without externalities, like subsidies or other incentives.

3. The Role of Local Citizen Energy Communities

4. Measures of Environmental, Sustainability, Performance and Economic Impact

4.1. Carbon-Neutral and Energy Sustainable Indexes

4.2. Performance Indicators: Renewable Resource Index and Capacity Factor

4.3. Technology LCOE and Remuneration

4.4. Consumers and CECs Costs with Electricity

- Grid access, including the general economic interest cost (GEIC);

- Global system use;

- Transportation grid use;

- Distribution grid use:

- ∘

- High voltage;

- ∘

- Medium voltage;

- ∘

- Low voltage.

- Commercialization.

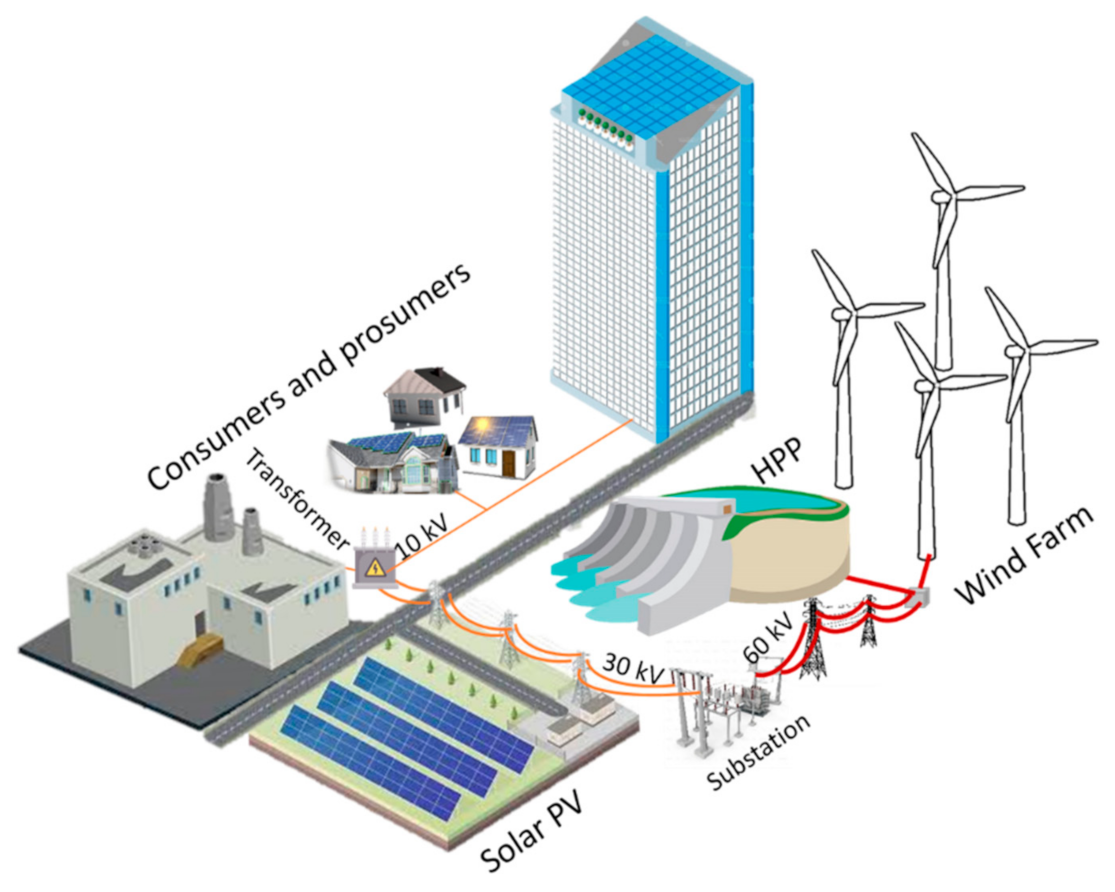

5. Case-Study on Local Citizen Energy Communities

5.1. Microgrid

5.2. CEC Tariffs, Technologies and Contracts

- Energy: 59.60 €/MWh (only for regulated tariffs);

- Grid access: 78.60 €/MWh:

- ∘

- Single self-consumption: −21.80 €/MWh;

- ∘

- CEC self-consumption: −43.70 €/MWh;

- Global system use: 4.83 €/MWh;

- Transport grid use: 6.30 €/MWh;

- Distribution grid use:

- ∘

- High voltage: 1.70 €/MWh;

- ∘

- Medium voltage: 6.90 €/MWh;

- ∘

- Low voltage: 15.40 €/MWh;

- Commercialization: 5.40 €/MWh;

- Total for residential consumers: 178.73 €/MWh

- Weight of wholesale energy price: 33.35%

- VAT: 12%

- Total cost for residential consumers: 200.18 €/MWh. Excluding the energy part: 133.43 €/MWh (other-part);

- Potential cost of the other-part of the variable term for energy sustainable CECs with self-consumption and microgrid agreements: 71.38 €/MWh (47% less than single residential consumers).

5.3. CEC Composition and Results

6. Final Remarks and Future Work

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| ACER | Agency for the Cooperation of Energy Regulators |

| BESS | Battery energy storage system |

| CEC | Citizen energy community |

| CET | Central European Time |

| CO2 | Dioxide carbon |

| DAM | Day-ahead market |

| DR | Demand response |

| DSO | Distributed system operator |

| EM | Electricity market |

| ETS | Emissions trading system |

| EV | Electric vehicle |

| EU | European Union |

| G2V | Grid-to-vehicle |

| GDP | Gross Domestic Product |

| GEIC | General Economic Interest Cost |

| HPP | Hydroelectric power plants |

| IDM | Intraday market |

| LCOE | Levelized cost of the energy |

| MTS | Multivariate time series |

| RES | Renewable Energy Source |

| RMSE | Normalized mean square error |

| P2P | Peer-to-peer |

| PPA | Power purchase agreement |

| PV | Photovoltaic |

| SO | System operator |

| TSO | Transmission system operator |

| V2G | Vehicle-to-grid |

| VAT | Value Added Tax |

| VRE | Variable renewable energy |

| Indices | |

| Bilateral contract | |

| Lag | |

| Time | |

| Parameters | |

| , , , , , | Lags number |

| Variable costs | |

| Fixed costs | |

| I | Number of bilateral contracts and self-consumption units |

| Discount rate | |

| Time period | |

| Technology life-cycle | |

| Variables | |

| , , ,, , | Regressions variables |

| , | Errors of random events |

| Technology variable costs | |

| Technology fixed costs | |

| Variable cost of consumers or CECs with electricity | |

| Average variable cost of consumers or CECs with electricity | |

| Capacity factor | |

| Carbon-neutral index | |

| Electricity sustainability index | |

| Renewable resource index | |

| Gross Domestic Product | |

| Nominal power | |

| Bilateral contract or self-consumption electricity price | |

| DAM price | |

| Expected DAM price | |

| Down deviations price | |

| Retail energy price of the variable-term of the tariff | |

| Retail other prices of the variable-term of the tariff | |

| Up deviation price | |

| Nominal quantity of energy | |

| Observed quantity of energy | |

| Forecasted quantity of energy | |

| Quantity of all bilateral contracts and self-consumption units | |

| Bilateral contract or self-consumption quantity | |

| Average deviation of energy | |

| All energy transacted in the DAM | |

| Bidded DAM quantity of energy | |

| Consumer or CEC consumption of energy | |

| Consumer or CEC consumption forecast | |

| Observed net-load | |

| Reference renewable production of energy | |

| Renewable production of energy | |

| Forecast of the renewable production | |

| Remuneration of each technology | |

| Average remuneration of each technology | |

| DAM share of RES | |

References

- Kirschen, D.; Strbac, G. Fundamentals of Power System Economics, 2nd ed.; John Wiley & Sons: Chichester, UK, 2018. [Google Scholar]

- Lopes, F. Electricity markets and intelligent agents. Part I: Market architecture and structure. In Electricity Markets with Increasing Levels of Renewable Generation: Structure, Operation, Agent-Based Simulation and Emerging Designs; Springer: Cham, Switzerland, 2018; pp. 23–48. [Google Scholar]

- Shahidehpour, M.; Yamin, H.; Li, Z. Market Operations in Electric Power Systems: Forecasting, Scheduling, and Risk Management, 1st ed.; John Wiley & Sons: Chichester, UK, 2003. [Google Scholar]

- Algarvio, H.; Couto, A.; Lopes, F.; Santana, S.; Estanqueiro, A. Effects of regulating the European Internal Market on the integration of variable renewable energy. WIREs Energy Environ. 2019, 8, 346. [Google Scholar] [CrossRef]

- Algarvio, H.; Lopes, F.; Couto, A.; Estanqueiro, A. Participation of wind power producers in day-ahead and balancing markets: An overview and a simulation-based study. WIREs Energy Environ. 2019, 8, 343. [Google Scholar] [CrossRef]

- Voss, K.; Musall, E. Net Zero Energy Buildings: International Projects of Carbon Neutrality in Buildings; Walter de Gruyter: Berlin, Germany, 2012. [Google Scholar]

- Lehmann, P.; Creutzig, F.; Ehlers, M.H.; Friedrichsen, N.; Heuson, C.; Hirth, L.; Pietzcker, R. Carbon lock-out: Advancing renewable energy policy in Europe. Energies 2012, 5, 323–354. [Google Scholar] [CrossRef] [Green Version]

- Moro, A.; Lonza, L. Electricity carbon intensity in European Member States: Impacts on GHG emissions of electric vehicles. Transp. Res. Part D Transp. Environ. 2018, 64, 5–14. [Google Scholar] [CrossRef]

- Nicolini, M.; Tavoni, M. Are renewable energy subsidies effective? Evidence from Europe. Renew. Sustain. Energy Rev. 2018, 74, 412–423. [Google Scholar] [CrossRef]

- Algarvio, H.; Lopes, F.; Santana, J. Renewable energy support policy based on contracts for difference and bilateral negotiation. In Proceedings of the International Conference on Practical Applications of Agents and Multi-Agent Systems, PAAMS, L’Aquila, Italy, 7–9 October 2020; Springer: Cham, Switzerland, 2020. [Google Scholar]

- Gils, H.; Scholz, Y.; Pregger, T.; de Tena, D.; Heide, D. Integrated modelling of variable renewable energy-based power supply in Europe. Energy 2017, 123, 173–188. [Google Scholar] [CrossRef] [Green Version]

- Prol, J.; Steininger, K.; Zilberman, D. The cannibalization effect of wind and solar in the California wholesale electricity market. Energy Econ. 2020, 85, 104552. [Google Scholar] [CrossRef]

- Algarvio, H.; Lopes, F.; Sousa, J.; Lagarto, J. Multi-agent electricity markets: Retailer portfolio optimization using Markowitz theory. Electr. Power Syst. Res. 2017, 148, 282–294. [Google Scholar] [CrossRef]

- Wei, N.; Li, C.; Peng, X.; Zeng, F.; Lu, X. Conventional models and artificial intelligence-based models for energy consumption forecasting: A review. J. Pet. Sci. Eng. 2019, 181, 106187. [Google Scholar] [CrossRef]

- Algarvio, H.; Lopes, F.; Santana, J. A linear programming model to simulate the adaptation of multi-agent power systems to new sources of energy. In Highlights in Cyber-Physical Multi-Agent Systems; Springer: Cham, Switzerland, 2017; pp. 350–360. [Google Scholar]

- Morales-España, G.; Nycander, E.; Sijm, J. Reducing CO2 emissions by curtailing renewables: Examples from optimal power system operation. Energy Econ. 2021, 99, 105277. [Google Scholar] [CrossRef]

- International Energy Agency. The Power of Transformation: Wind, Sun and the Economics of Flexible Power Systems. Available online: https://www.oecd.org/publications/the-power-of-transformation-9789264208032-en.htm (accessed on 18 March 2021).

- Bernath, C.; Deac, G.; Sensfuß, F. Impact of sector coupling on the market value of renewable energies—A model-based scenario analysis. Appl. Energy 2021, 281, 115985. [Google Scholar] [CrossRef]

- Algarvio, H.; Viegas, J.; Lopes, F.; Amaro, D.; Pronto, A.; Vieira, S. Electricity usage efficiency in large buildings: DSM measures and preliminary simulations of DR programs in a public library. In Proceedings of the International Conference on Practical Applications of Agents and Multi-Agent Systems, Salamanca, Spain, 3–5 June 2015; Springer: Cham, Switzerland, 2015; pp. 249–259. [Google Scholar]

- Algarvio, H.; Lopes, F.; Couto, A.; Estanqueiro, A.; Santana, J. Variable renewable energy and market design: New market products and a real-world study. Energies 2019, 12, 4576. [Google Scholar] [CrossRef] [Green Version]

- Strbac, G.; Papadaskalopoulos, D.; Chrysanthopoulos, N.; Estanqueiro, A.; Algarvio, H.; Lopes, F.; de Vries, L.; Morales-España, G.; Sijm, J.; Hernandez-Serna, R.; et al. Decarbonization of electricity systems in Europe: Market design challenges. IEEE Power Energy Mag. 2021, 19, 53–63. [Google Scholar] [CrossRef]

- European Commission. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee, the Committee of the Regions and the European Investment Bank. Clean Energy for All Europeans (COM/2016/0860 Final). Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52016DC0860 (accessed on 18 March 2021).

- European Commission. Regulation (EU) 2019/943 of the European Parliament and of the Council on the Internal Market for Electricity. 5 June 2019. Available online: http://data.europa.eu/eli/reg/2019/943/oj (accessed on 10 May 2021).

- Jager-Waldau, A. JRC Science for Policy Report, PV Status Report 2019. Available online: https://ec.europa.eu/jrc/en/publication/eur-scientific-and-technical-research-reports/pv-status-report-2019 (accessed on 18 March 2021).

- US Energy Information Association. Levelized Costs of New Generation Resources in the Annual Energy Outlook 2021. US Department of Energy. Available online: https://www.eia.gov/outlooks/aeo/pdf/electricity_generation.pdf (accessed on 18 March 2021).

- IRENA. Renewable Power Generation Costs in 2017. 2018. Available online: https://www.irena.org/publications/2018/Jan/Renewable-power-generation-costs-in-2017 (accessed on 18 March 2021).

- Pinna, A.; Massidda, L. A procedure for complete census estimation of rooftop photovoltaic potential in urban areas. Smart Cities 2020, 3, 873–893. [Google Scholar] [CrossRef]

- Bódis, K.; Kougias, I.; Jäger-Waldau, A.; Taylor, N.; Szabó, S. A high-resolution geospatial assessment of the rooftop solar photovoltaic potential in the European Union. Renew. Sustain. Energy Rev. 2019, 114, 109309. [Google Scholar] [CrossRef]

- Pinto, G.; Abdollahi, E.; Capozzoli, A.; Savoldi, L.; Lahdelma, R. Optimization and multicriteria evaluation of carbon-neutral technologies for district heating. Energies 2019, 12, 1653. [Google Scholar] [CrossRef] [Green Version]

- Eikeland, P. The Third Internal Energy Market Package: New Power Relations among Member States, EU Institutions and Non-state Actors? JCMS J. Common Mark. Stud. 2011, 49, 243–263. [Google Scholar] [CrossRef]

- Sleisz, Á.; Sőrés, P.; Raisz, D. Algorithmic properties of the all-European day-ahead electricity market. In Proceedings of the 11th International Conference on the European Energy Market (EEM 14), Krakow, Poland, 28–30 May 2014; IEEE: Piscataway, NJ, USA, 2014. [Google Scholar]

- Algarvio, H.; Lopes, F.; Santana, J. Simple and linear bids in multi-agent daily electricity markets: A preliminary report. In Distributed Computing and Artificial Intelligence, In 15th International Conference; Springer International Publishing: Cham, Switzerland, 2018. [Google Scholar]

- Zsiborács, H.; Baranyai, N.; Vincze, A.; Zentkó, L.; Birkner, Z.; Máté, K.; Pintér, G. Intermittent renewable energy sources: The role of energy storage in the european power system of 2040. Electronics 2019, 8, 729. [Google Scholar] [CrossRef] [Green Version]

- Bistline, J.; Santen, N.; Young, D. The economic geography of variable renewable energy and impacts of trade formulations for renewable mandates. Renew. Sustain. Energy Rev. 2019, 106, 79–96. [Google Scholar] [CrossRef]

- Halttunen, K.; Staffell, I.; Slade, R.; Green, R.; Saint-Drenan, Y.; Jansen, M. Global Assessment of the Merit-Order Effect and Revenue Cannibalisation for Variable Renewable Energy. Available online: https://ssrn.com/abstract=3741232 (accessed on 18 March 2021).

- ACER. ACER Market Monitoring Report 2019—Energy Retail and Consumer Protection Volume. 2020. Available online: https://www.acer.europa.eu/Official_documents/Acts_of_the_Agency/Publication/ACER%20Market%20Monitoring%20Report%202019%20-%20Energy%20Retail%20and%20Consumer%20Protection%20Volume.pdf (accessed on 18 March 2021).

- Algarvio, H.; Couto, A.; Lopes, F.; Estanqueiro, A. Changing the day-ahead gate closure to wind power integration: A simulation-based study. Energies 2019, 12, 2765. [Google Scholar] [CrossRef] [Green Version]

- Couto, A.; Estanqueiro, A. Exploring wind and solar PV generation complementarity to meet electricity demand. Energies 2020, 13, 4132. [Google Scholar] [CrossRef]

- Kobylinski, P.; Wierzbowski, M.; Piotrowski, K. High-resolution net load forecasting for micro-neighbourhoods with high penetration of renewable energy sources. Int. J. Electr. Power Energy Syst. 2020, 117, 105635. [Google Scholar] [CrossRef]

- van der Meer, D.; Shepero, M.; Svensson, A.; Widén, J.; Munkhammar, J. Probabilistic forecasting of electricity consumption, photovoltaic power generation and net demand of an individual building using Gaussian Processes. Appl. Energy 2018, 213, 195–207. [Google Scholar] [CrossRef]

- Sossan, F.; Nespoli, L.; Medici, V.; Paolone, M. Unsupervised disaggregation of photovoltaic production from composite power flow measurements of heterogeneous prosumers. IEEE Trans. Ind. Inform. 2018, 14, 3904–3913. [Google Scholar] [CrossRef] [Green Version]

- Koponen, P.; Ikäheimo, J.; Koskela, J.; Brester, C.; Niska, H. Assessing and comparing short term load forecasting performance. Energies 2020, 13, 2054. [Google Scholar] [CrossRef]

- Chaaraoui, S.; Bebber, M.; Meilinger, S.; Rummeny, S.; Schneiders, T.; Sawadogo, W.; Kunstmann, H. Day-ahead electric load forecast for a ghanaian health facility using different algorithms. Energies 2021, 14, 409. [Google Scholar] [CrossRef]

- Mujeeb, S.; Alghamdi, T.; Ullah, S.; Fatima, A.; Javaid, N.; Saba, T. Exploiting deep learning for wind power forecasting based on big data analytics. Appl. Sci. 2019, 9, 4417. [Google Scholar] [CrossRef] [Green Version]

- Mayer, M.; Gróf, G. Extensive comparison of physical models for photovoltaic power forecasting. Appl. Energy 2021, 283, 116239. [Google Scholar] [CrossRef]

- Dimovski, A.; Moncecchi, M.; Falabretti, D.; Merlo, M. PV forecast for the optimal operation of the medium voltage distribution network: A real-life implementation on a large scale pilot. Energies 2020, 13, 5330. [Google Scholar] [CrossRef]

- Collino, E.; Ronzio, D. Exploitation of a new short-term multimodel photovoltaic power forecasting method in the very short-term horizon to derive a multi-time scale forecasting system. Energies 2021, 14, 789. [Google Scholar] [CrossRef]

- Raza, M.; Nadarajah, M.; Ekanayake, C. Demand forecast of PV integrated bioclimatic buildings using ensemble framework. Appl. Energy 2017, 208, 1626–1638. [Google Scholar] [CrossRef]

- Sougkakis, V.; Lymperopoulos, K.; Nikolopoulos, N.; Margaritis, N.; Giourka, P.; Angelakoglou, K. An investigation on the feasibility of near-zero and positive energy communities in the Greek Context. Smart Cities 2020, 3, 362–384. [Google Scholar] [CrossRef]

- Tcholtchev, N.; Schieferdecker, I. Sustainable and reliable information and communication technology for resilient smart cities. Smart Cities 2021, 4, 156–176. [Google Scholar] [CrossRef]

- Tobey, M.; Binder, R.; Yoshida, T.; Yamagata, Y. Urban systems design case study: Tokyo’s sumida ward. Smart Cities 2019, 2, 453–470. [Google Scholar] [CrossRef] [Green Version]

- Algarvio, H.; Lopes, F.; Santana, J. Multi-agent retail energy markets: Bilateral contracting and coalitions of end-use customers. In Proceedings of the 12th International Conference on the European Energy Market (EEM), Lisbon, Portugal, 19–22 May 2015; pp. 1–5. [Google Scholar]

- Monroe, J.; Hansen, P.; Sorell, M.; Berglund, E. Agent-based model of a blockchain enabled peer-to-peer energy market: Application for a neighborhood trial in Perth, Australia. Smart Cities 2020, 3, 1072–1099. [Google Scholar] [CrossRef]

- Algarvio, H.; Lopes, F.; Santana, J. Strategic Operation of Hydroelectric Power Plants in Energy Markets: A Model and a Study on the Hydro-Wind Balance. Fluids 2020, 5, 209. [Google Scholar] [CrossRef]

- Ramírez, F.; Honrubia-Escribano, A.; Gómez-Lázaro, E.; Pham, D. Combining feed-in tariffs and net-metering schemes to balance development in adoption of photovoltaic energy: Comparative economic assessment and policy implications for European countries. Energy Policy 2017, 102, 440–452. [Google Scholar] [CrossRef]

- Evangelopoulou, S.; De Vita, A.; Zazias, G.; Capros, P. Energy system modelling of carbon-neutral hydrogen as an enabler of sectoral integration within a decarbonization pathway. Energies 2019, 12, 2551. [Google Scholar] [CrossRef] [Green Version]

- ERSE. Tariffs and Prices—Electricity. Available online: https://www.erse.pt/en/activities/market-regulation/tariffs-and-prices-electricity/ (accessed on 18 March 2021).

- Portuguese Government. Renewable Capacity Auctions. Portuguese. Available online: https://leiloes-renovaveis.gov.pt/ (accessed on 18 March 2021).

- Algarvio, H.; Lopes, F.; Santana, J. Bilateral contracting in multi-agent energy markets: Forward contracts and risk management. In Proceedings of the International Conference on Practical Applications of Agents and Multi-Agent Systems, Salamanca, Spain, 3–5 June 2015; Springer International Publishing: Cham, Switzerland, 2015; pp. 260–269. [Google Scholar]

- Bhat, A.; Dhamaniya, B.; Chhillar, P.; Korukonda, T.; Rawat, G.; Pathak, S. Analysing the prospects of perovskite solar cells within the purview of recent scientific advancements. Crystals 2018, 8, 242. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| Player | NRMSE | Average Deviation |

|---|---|---|

| Wind Farm | 13.49 | 43.33 |

| Agg. Wind Farms | 8.03 | 25.79 |

| Large-scale Solar PV | 15.00 | 60.00 |

| Agg. Solar PV | 6.00 | 24.00 |

| Small-scale Solar PV | 21.00 | 85.00 |

| Agg. Consumers | 8.00 | 19.00 |

| Agg. Consumers with self-consumption (PV) | 6.50 | 15.50 |

| Player | Engagement | Benefits from | Contributes to |

|---|---|---|---|

| Consumer (M) | Demand Market participation | Lower costs and forecast errors | Lower balancing needs and costs |

| Prosumer (M) | Demand and supply Market participation | Lower costs and forecast errors | Lower balancing needs, costs and grid usage |

| VRE (P) | Microgrid trades Supply | Lower forecast errors and less penalties paid | Lower balancing needs and costs, and less costs with CO2 emissions because of CO2 licenses |

| HPP (P) | Microgrid trades Scarcity supply and excess demand | Lower prices for pumping | Any balancing needs and costs, and potential any costs with CO2 emissions because of CO2 licenses |

| DSO (M or P) | Energy management | Less congestions | Lower distribution grid costs |

| Option | Engagement | Contributes to | Potential Benefits the System with |

|---|---|---|---|

| EVs | Smart charging | Energy balance and lower costs | Lower balancing needs, costs and grid usage |

| BESS | Storage management | Energy balance and lower costs | Lower balancing needs, costs and grid usage |

| DR | Smart consumption | Energy balance, lower costs and economic incentives | Lower balancing needs, costs, grid usage and congestions incidences |

| District heating | Smart storage and centralized heating | Energy balance and storage at lower prices | Electrification and lower balancing needs and costs |

| District cooling | Smart centralized cooling | Energy balance and lower prices | Electrification and lower balancing needs and costs |

| P2P markets | Trading with neighbour balancing zones | Energy balance and avoid grid usage | Lower balancing needs, costs, grid usage and losses |

| Trades with SOs | Participation in ancillary services | Economic incentives | Security, stability and guarantee of supply |

| Sector coupling | Trades with other sectors | Avoid curtailments | Electrification and lower costs |

| Technology | Market Value of Year 0 | |||

|---|---|---|---|---|

| Wind | 47.15 | 36.05 | 35.87 | 32.90 |

| Solar PV | 53.41 | 40.49 | 40.29 | 36.95 |

| Hydro | 51.29 | 48.10 | 47.86 | 43.90 |

| Option | Details | Wind | Solar PV | Hydro |

|---|---|---|---|---|

| Forward | Price (€/MWh) | 37.82 | 44.41 | 49.17 |

| Quantity (MWh) | 212 | 212 | 212 | |

| PPA | Price | Day-ahead | Day-ahead | Day-ahead (−10%) |

| Power (MW) | 848 | 1077 | 446 | |

| Self-Consumption | Small-scale LCOE (€/MWh) | - | 90 | - |

| Large-scale LCOE (€/MWh) | - | 11.14–30 | - | |

| Power (MW) | - | 1077 | - |

| Technology | Market Value €/MWh | Production TWh | Capacity Factor % | Renewable Resource Index |

|---|---|---|---|---|

| Wind | 40.67 | 21.76 | 26.22 | 1.00 |

| Solar PV | 48.45 | 0.80 | 22.05 | - |

| Hydro | 44.21 | 16.63 | 18.73 | 0.70 |

| Option | Technology | Carbon-Neutral Index | Energy Sustainability Index |

|---|---|---|---|

| Forwards | Wind Solar PV Hydro | 0.98 | 0.85 |

| 0.72 | 0.85 | ||

| 1.00 | 0.85 | ||

| Wind + PV | 0.99 | 0.85 | |

| All | 1.00 | 0.85 | |

| PPA | Wind Solar PV Hydro | 1.00 | 0.65 |

| 1.00 | 0.53 | ||

| 1.00 | 1.00 | ||

| Self-consumption | Solar PV | 1.00 | 0.53 |

| Player | Details | Energy- Part (€/MWh) | Other-Part (€/MWh) | Total Cost (€/MWh) | Technology Remuneration (€/MWh) |

|---|---|---|---|---|---|

| Consumer | Retail Tariff | 59.60 | 103.73 | 163.33 | - |

| Consumer with self-consumption (small-scale PV) | Retail Tariff and PV cost (90 €/MWh) | 101.81 | 35.70 | 137.51 | - |

| Consumers | Market-based | 50.98 | 98.33 | 149.31 | - |

| Consumers with self-consumption (small-scale PV) | Market-based and PV cost (90 €/MWh) | 98.38 | 25.89 | 124.27 | - |

| Consumers with self-consumption (large-scale PV) | Market-based and PV cost (11.14 €/MWh) | 7.43 | 29.86 | 37.29 | - |

| Consumers with self-consumption (large-scale PV) | Market-based and PV cost (30.00 €/MWh) | 29.18 | 29.86 | 59.04 | - |

| Wind | Market-based | - | - | - | 33.87 |

| PV | Market-based | - | - | - | 40.54 |

| Hydro | Market-based | - | - | - | 39.52 |

| Consumers and Wind | Forwards and Market-based | 42.69 | 98.33 | 141.02 | 37.09 |

| Consumers and Wind | PPA and Market-based | 52.59 | 98.33 | 150.92 | 40.67 |

| Consumers and PV | Forwards and Market-based | 49.48 | 97.53 | 147.01 | 50.31 |

| Consumers and PV | PPA and Market-based | 50.54 | 92.48 | 143.02 | 48.45 |

| Consumers and Hydro | Forwards and Market-based | 53.36 | 98.33 | 151.69 | 47.04 |

| Consumers and Hydro | PPA and Market-based | 52.78 | 98.33 | 151.11 | 39.99 |

| Consumers and all Technologies | Forwards and Market-based | 45.18 | 98.32 | 143.50 | - |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Algarvio, H. The Role of Local Citizen Energy Communities in the Road to Carbon-Neutral Power Systems: Outcomes from a Case Study in Portugal. Smart Cities 2021, 4, 840-863. https://doi.org/10.3390/smartcities4020043

Algarvio H. The Role of Local Citizen Energy Communities in the Road to Carbon-Neutral Power Systems: Outcomes from a Case Study in Portugal. Smart Cities. 2021; 4(2):840-863. https://doi.org/10.3390/smartcities4020043

Chicago/Turabian StyleAlgarvio, Hugo. 2021. "The Role of Local Citizen Energy Communities in the Road to Carbon-Neutral Power Systems: Outcomes from a Case Study in Portugal" Smart Cities 4, no. 2: 840-863. https://doi.org/10.3390/smartcities4020043

APA StyleAlgarvio, H. (2021). The Role of Local Citizen Energy Communities in the Road to Carbon-Neutral Power Systems: Outcomes from a Case Study in Portugal. Smart Cities, 4(2), 840-863. https://doi.org/10.3390/smartcities4020043