Applying ERP and MES to Implement the IFRS 8 Operating Segments: A Steel Group’s Activity-Based Standard Costing Production Decision Model

Abstract

:1. Introduction

- Transparent information about interoperability and exchange between systems, machines, people, processes, and interfaces.

- Smart data for real-time decision making enhance operational capabilities through data acquisition and processing technology.

- A set of sensors are distributed in smart factories, not only for monitoring and tracking all operations, but also for automatically acquiring all data from all various sources.

- In the production process, provide the smart decision-making ability to meet the needs of timely actions, such as, “Machines-to-Machines (M2M)”, which receive their commands and provide their work cycle information to achieve smart autonomy and flexibility for each machine.

2. Research Background

2.1. The Concept of Industry 4.0

2.2. Integrating a Concept of Smart Operation between MES and ERP

3. ABSC in a Smart ERP and MES

3.1. Brief of ABC Theory

3.2. Brief of ABSC in ERP and MES Systems

3.3. ABSC in a Smart Factory

3.4. Standard Costs for Smart Products

3.5. Production Decision Model of ABSC and IFRS 8 Operating Segments in a Smart Factory

4. Formulation of an ABSC Mixed Decision through IFRS 8 for a Steel Group

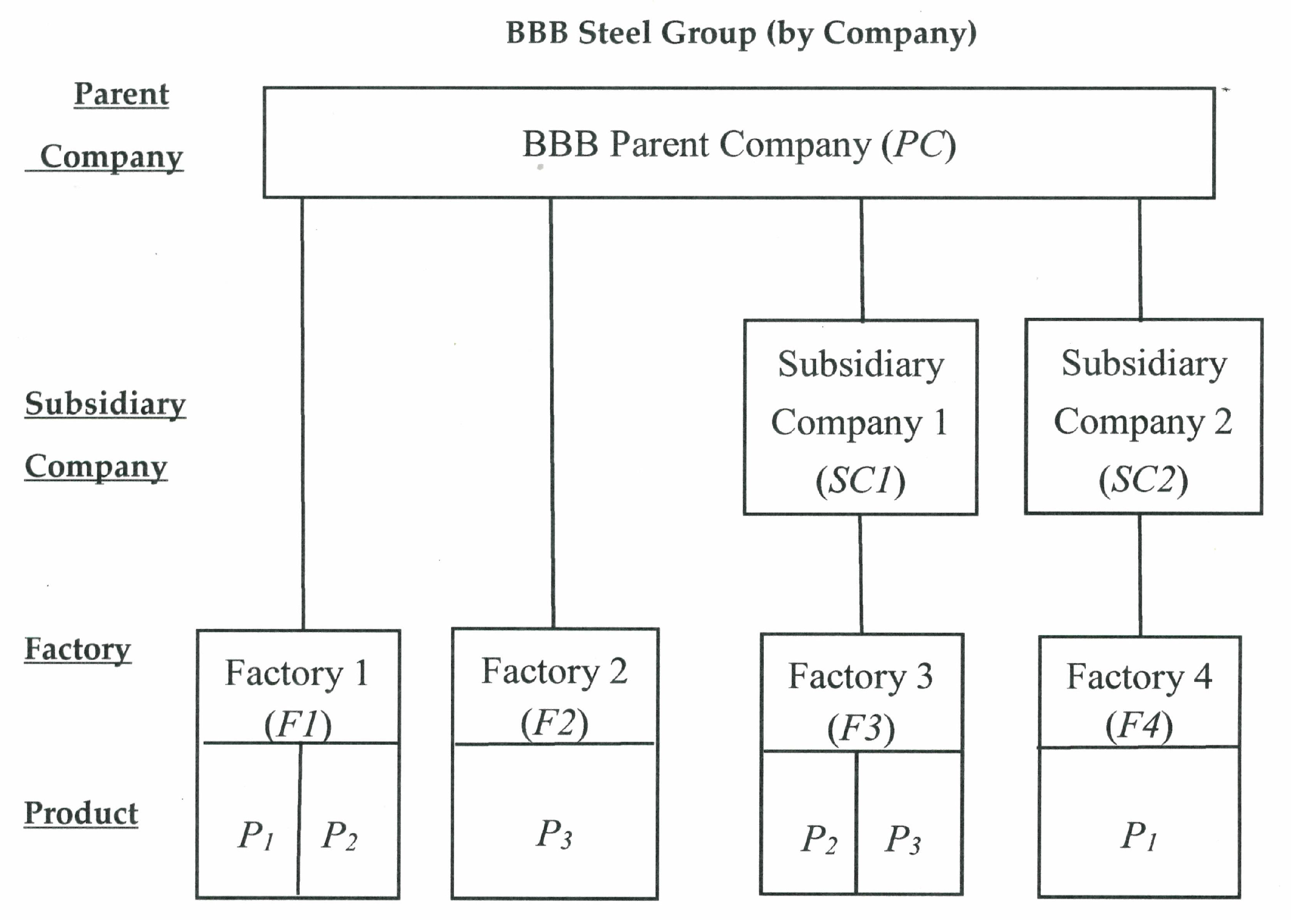

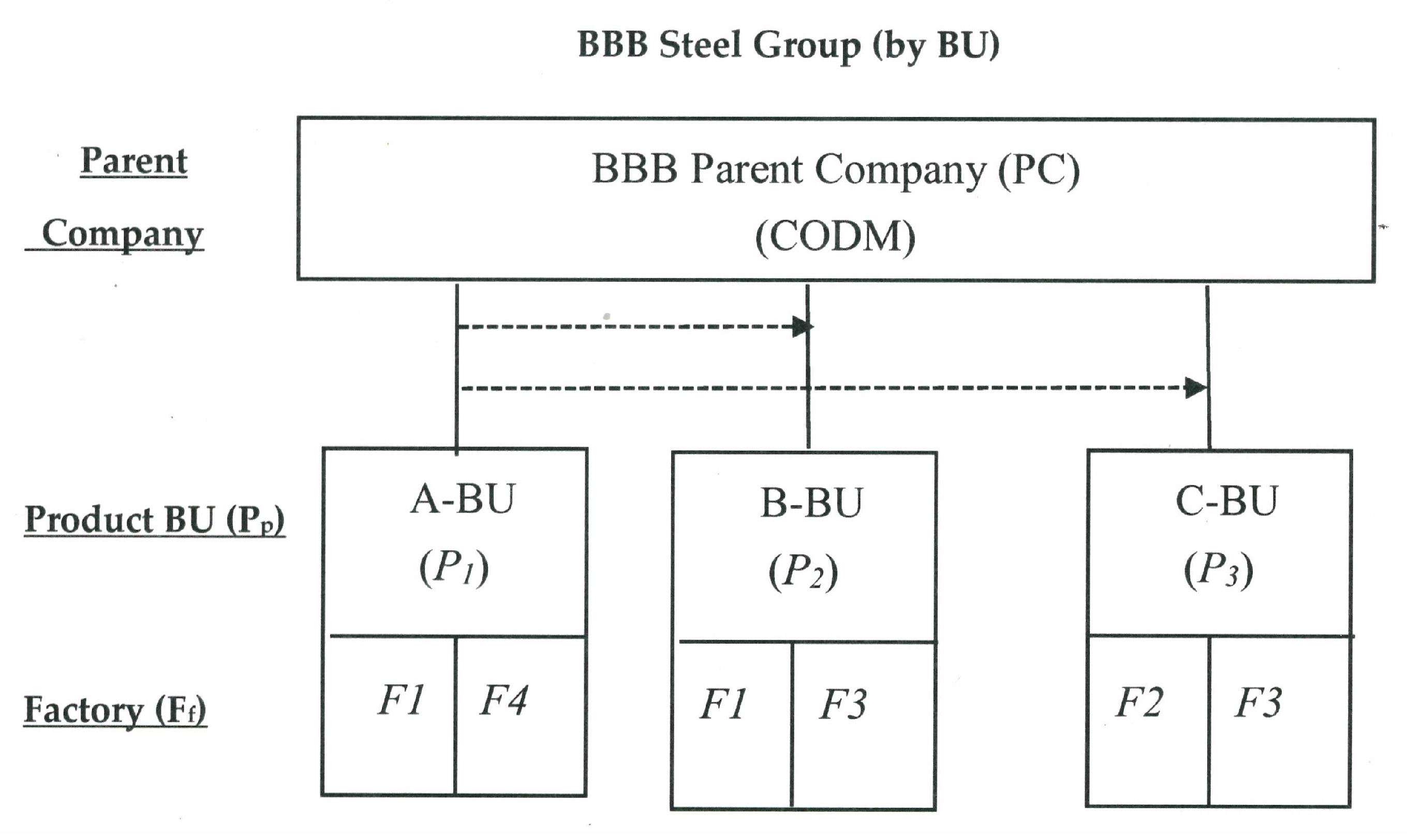

4.1. Describing Production Processes for a Steel Group

4.2. Steel Group Cost Categories for the ABSC Mixed Decision Model

- Revenue: Including sales products, byproducts, intersegment sales (selling P1 to other relational companies in the same group), and the transfer of internal products (transfer of P1 to the same company for B-BU or C-BU);

- Material costs: Including steel scrap for EAF (Electric Arc Furnace) manufacturing, and Iron ore and coal for BF (Blast Furnace) traditional manufacturing;

- Labor cost: Including normal and overtime direct labor cost, and indirect labor cost for EAF;

- Electrical power cost: Only suitable for high electrical power cost in the steelmaking process by using EAF equipment. Electricity bills for other processes are not important, so their electrical power costs are included in other costs.

- CO2 emission cost: Including carbon tax and carbon right costs;

- Machine costs: Allocating and installing all machines with smart data in the related working process; however, the machine cost is fixed;

- Other costs: Other indirect costs using only the percentage of revenue-customer;

4.3. Assumptions

- Following the IFRS 8 standards [3], total revenue including: External sales, semi-manufactured goods of P1 (for selling different BU, including the same company or related company in the same group), and byproducts (for selling slag or furnace slag);

- Different direct raw materials are used in different manufacturing methods; and the recycling byproduct of steel scrap also become its direct material;

- Direct labor will be relevant to manufacturing methods, production processes, and machine hours;

- Conforming to government policies, including basic wage, overtime hours, carbon tax, and carbon right costs;

- Direct costs, including: Raw material, labor, electrical power cost, and CO2 emission;

- Smart machines will run automatically by being embedded into various smart data, while the machine cost is fixed;

- Indirect costs are not related to the production processes, but all smart products must share the costs at a fixed percentage of external sales.

4.4. Notations

4.5. Mathematical Programming Model

4.5.1. Integrated Models

QP2 = QP21 + QP23;

QP3 = QP32 + QP33;

(H2 − H1) ≤ 22 * (NL1 + NL2 + NL3); (H3 − H1) ≤ 40 * (NL1 + NL2 + NL3);

4.5.2. Sales Amount Following IFRS 8 Standards

4.5.3. Direct Material Cost

4.5.4. Semi-Manufactured Goods

4.5.5. Direct Labor Cost

4.5.6. Other Fixed Labor Costs

4.5.7. Direct Electricity Power Cost

4.5.8. Machine Cost

4.5.9. CO2 Emission Cost

4.5.10. Other Indirect Costs

5. Illustrative Case Study

5.1. Strategy Model for Group Organization

Smart Data and Sales Forecast

5.2. Process Planning

5.3. Direct Material and Semi-Manufactured Goods

5.4. Direct Labor for Unit-Level

Indirect Labor for Batch-Level

5.5. Electricity Power Cost only for EAF

5.6. Machine Hours and Cost

5.7. CO2 Emission Quantity and Cost

5.8. Other Indirect Costs

5.9. Designing a Measurement Report for Reportable Segments in the ERP system

6. Systemizing Case Study and Following IFRS 8 and ABSC Production Decision

6.1. Designing the Reportable Segments Financial Statements Following IFRS 8 and ABSC

6.2. Comparing Product P1 in the Different Factories

6.3. Comparing the Unit and Cost Structure Analysis of P1

6.4. Sensitivity Analysis on Carbon Emission Reduction Goal of Environmental Sustainability

7. Discussion

8. Conclusions

- (1)

- Presenting the ABSC to replace the traditional standard costing method with more detailed standards under Industry 4.0;

- (2)

- Presenting a methodology of operation planning and control for the international enterprise group under Industry 4.0;

- (3)

- Presenting an approach of integrating ERP and MES to conduct the IFRS 8 operating segments reporting under Industry 4.0.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Erol, S.; Sihn, W. Intelligent production planning and control in the cloud—Towards a scalable software architecture. Procedia CIRP 2017, 62, 571–576. [Google Scholar] [CrossRef]

- Liua, F.C.; Hsub, H.T.; Yenc, D.C. Technology executives in the changing accounting information environment: Impact of IFRS adoption on CIO compensation. Inf. Manag. 2018, 55, 877–889. [Google Scholar] [CrossRef]

- Deloitte, Standards, IFRS 8-Operating Segments. Available online: https://www.iasplus.com/en/standards/ifrs/ifrs8 (accessed on 15 April 2020).

- Tsai, W.H.; Lan, S.H.; Huang, C.T. Activity-based standard costing product-mix decision in the future digital era: Green recycling steel-scrap material for steel industry. Sustainability 2019, 11, 899. [Google Scholar] [CrossRef] [Green Version]

- Jian, Q.; Ying, L.; Roger, G. A categorical framework of manufacturing for industry 4.0 and beyond. Procedia CIRP 2016, 52, 173–178. [Google Scholar]

- Xiaoa, J.; Wua, Y.; Xiea, K.; Hub, Q. Managing the e-commerce disruption with IT-based innovations: Insights from strategic renewal perspectives. Inf. Manag. 2019, 56, 122–139. [Google Scholar] [CrossRef]

- Moutaz, H.; Ahmed, E. The readiness of ERP systems for the factory of the future. Procedia Comput. Sci. 2015, 64, 721–728. [Google Scholar]

- Jurgen, K. Manufacturing Execution System-MES; Springer: Berlin/Heidelberg, Germany; New York, NY, USA, 2007. [Google Scholar]

- Bauer, W.; Hämmerle, M.; Schlund, S.; Vocke, C. Transforming to a hyper-connected society and economy—Towards an “Industry 4.0”. Procedia Manuf. 2015, 3, 417–424. [Google Scholar] [CrossRef]

- Stock, T.; Seliger, G. Opportunities of sustainable manufacturing in Industry 4.0. Procedia CIRP 2016, 40, 536–541. [Google Scholar] [CrossRef] [Green Version]

- Merkel, L.; Atug, J.; Merhar, L.; Schultz, C.; Stefan Braunreuther, G. Reinhart, teaching smart production: An insight into the learning factory for cyber-physical production systems (LVP). Procedia Manuf. 2017, 9, 269–274. [Google Scholar] [CrossRef]

- Seitz, K.-F.; Nyhuis, P. Cyber-physical production systems combined with logistic models—A learning factory concept for an improved production planning and control. Procedia CIRP 2015, 32, 92–97. [Google Scholar] [CrossRef] [Green Version]

- Uhlemann, T.H.-J.; Lehmann, C.; Steinhilper, R. The digital twin: Realizing the cyber-physical production system for industry 4.0. Procedia CIRP 2017, 61, 335–340. [Google Scholar] [CrossRef]

- Adamson, G.; Wang, L.; Moore, P. Feature-based control and information framework for adaptive and distributed manufacturing in cyber physical systems. J. Manuf. Syst. 2017, 43, 305–315. [Google Scholar] [CrossRef]

- Albers, A.; Gladysz, B.; Pinner, T.; Butenko, V.; Stürmlinger, T. Procedure for defining the system of objectives in the initial phase of an industry 4.0 project focusing on intelligent quality control systems. Procedia CIRP 2016, 52, 262–267. [Google Scholar] [CrossRef] [Green Version]

- Kans, M.; Ingwald, A. Business model development towards service management 4.0. Procedia CIRP 2016, 47, 489–494. [Google Scholar] [CrossRef]

- Neuer, M.J.; Marchiori, F.; Ebel, A.; Matskanis, N.; Piedimonti, L.; Wolff, A.; Mathis, G. Dynamic reallocation and rescheduling of steel products using agents with strategical anticipation and virtual market structures. IFAC Pap. 2016, 49, 232–237. [Google Scholar] [CrossRef]

- Weyer, S.; Meyer, T.; Ohmer, M.; Gorecky, D.; Zuhlke, D. Future modeling and simulation of CPS-based factories: An example from the automotive industry. IFAC Pap. 2016, 49, 97–102. [Google Scholar] [CrossRef]

- Küsters, D.; Praß, N.; Gloy, Y.-S. Textile learning factory 4.0—Preparing Germany’s textile industry for the digital future. Procedia Manuf. 2017, 9, 214–221. [Google Scholar] [CrossRef]

- Constantinescu, C.L.; Francalanza, E.; Matarazzo, D.; Balkan, O. Information support and interactive planning in the digital factory: Approach and industry-driven evaluation. Procedia CIRP 2014, 25, 269–275. [Google Scholar] [CrossRef]

- Constantinescu, C.L.; Francalanza, E.; Matarazzo, D. Towards knowledge capturing and innovative human-system interface in an open-source factory modelling and simulation environment. Procedia CIRP 2015, 33, 23–28. [Google Scholar] [CrossRef]

- Uhlemann, T.H.-J.; Schock, C.; Lehmann, C.; Freiberger, S.; Steinhilper, R. The digital twin: Demonstrating the potential of real time data acquisition in production systems. Procedia Manuf. 2017, 9, 113–120. [Google Scholar] [CrossRef]

- Maribel, Y.S.; Jorge, O.S.; Carina, A.; Francisca, V.L.; Eduarda, C.; Carlos, C.; Bruno, M.; Joao, G. A big data system supporting bosch braga industry 4.0 strategy. Int. J. Inf. Manag. 2017, 37, 750–760. [Google Scholar]

- Sauer, O. Information technology for the factory of the future-state of the art and need for action. Procedia CIRP 2014, 25, 293–296. [Google Scholar] [CrossRef]

- Friedemann, M.; Trapp, T.U.; Stoldt, J.; Langer, T.; Putz, M. A framework for information-driven manufacturing. Procedia CIRP 2016, 57, 38–43. [Google Scholar] [CrossRef]

- Quint, F.; Sebastian, K.; Gorecky, D. A mixed-reality learning environment. Procedia Comput. Sci. 2015, 75, 43–48. [Google Scholar] [CrossRef] [Green Version]

- Brandenburger, J.; Colla, V.; Nastasi, G.; Ferro, F.; Schirm, C.; Melcher, J. Big data solution for quality monitoring and improvement on flat steel production. IFAC Pap. 2016, 49, 055–060. [Google Scholar] [CrossRef]

- Hammer, M.; Somers, K.; Karre, H.; Ramsauer, C. Profit per hour as a target process control parameter for manufacturing systems enabled by big data analytics and industry 4.0 infrastructure. Procedia CIRP 2017, 63, 715–720. [Google Scholar] [CrossRef]

- Elragal, A. ERP and big data: The inept couple. Procedia Technol. 2014, 16, 242–249. [Google Scholar] [CrossRef] [Green Version]

- IFRS. Why Global Accounting Standards? Available online: https://www.ifrs.org/use-around-the-world/why-global-accounting-standards/ (accessed on 15 April 2020).

- IFRS. IFRS Standards and IFRIC Interpretations. Available online: https://www.ifrs.org/issued-standards/ (accessed on 15 April 2020).

- Tsai, W.H. Project management accounting using activity-based costing approach. Handb. Technol. Manag. 2010, 1, 469–488. [Google Scholar]

- Tsai, W.H.; Lin, T.W. A mathematical programming approach to analyze the activity-based costing product-mix decision with capacity expansions. Appl. Manag. Sci. 2004, 11, 163–178. [Google Scholar]

- Bauerdick, C.J.H.; Helfert, M.; Menz, B.; Abele, E. A common software framework for energy data based monitoring and controlling for machine power peak reduction and workpiece quality improvements. Procedia CIRP 2017, 61, 359–364. [Google Scholar] [CrossRef]

- Fleischmann, H.; Kohl, J.; Franke, J. A modular architecture for the design of condition monitoring processes. Procedia CIRP 2016, 57, 410–415. [Google Scholar] [CrossRef]

- Trusculescu, A.; Draghici, A.; Albulescu, C.T. Key metrics and key drivers in the valuation of public enterprise resource planning companies. Procedia Comput. Sci. 2015, 65, 917–923. [Google Scholar] [CrossRef]

- Goguelin, S.; Colaco, J.; Dhokia, V.; Schaefer, D. Smart manufacturability analysis for digital product development. Procedia CIRP 2017, 60, 56–64. [Google Scholar] [CrossRef] [Green Version]

- Tsai, W.H. Activity-based costing model for joint products’. Comput. Ind. Eng. 1996, 31, 725–729. [Google Scholar] [CrossRef]

- Hold, P.; Erol, S.; Reisinger, G.; Sihn, W. Planning and evaluation of digital assistance systems. Procedia Manuf. 2017, 9, 143–150. [Google Scholar] [CrossRef]

- Tsai, W.H. A technical note on using work sampling to estimate the effort on activities under activity-based costing. Int. J. Prod. Econ. 1996, 43, 11–16. [Google Scholar] [CrossRef]

- Simons, S.; Abé, P.; Neser, S. Learning in the AutFab—The fully automated industrie 4.0 learning factory of the university of applied sciences darmstadt. Procedia Manuf. 2017, 9, 81–88. [Google Scholar] [CrossRef]

- Gregori, F.; Papettia, A.; Pandolfib, M.; Peruzzinic, M.; Germania, M. Digital manufacturing systems: A framework to improve social sustainability of a production site. Procedia CIRP 2017, 63, 436–442. [Google Scholar] [CrossRef]

- Dataversity, Big Data vs. Smart Data. Available online: https://www.dataversity.net/big-data-vs-smart-data/ (accessed on 15 April 2020).

- Accounting Coach. What Is a Standard Cost? Available online: https://www.accountingcoach.com/blog/what-is-a-standard-cost (accessed on 15 April 2020).

- Demi, S.; Haddara, M. Do cloud ERP systems retire? An ERP lifecycle perspective. Procedia Comput. Sci. 2018, 138, 587–594. [Google Scholar] [CrossRef]

- Tung Ho Steel Enterprise CORP, Profile, CSR, Products. Available online: http://www.tunghosteel.com/EN/HomeEg/about/intro (accessed on 15 April 2020).

- American Iron and Steel Institute, Steel Production, Recycling. Available online: http://www.steel.org/about-aisi/industry-profile.aspx (accessed on 15 April 2020).

- Bedolla, J.S.; D’Antonio, G.; Chiabert, P. A novel approach for teaching IT tools within learning factories. Procedia Manuf. 2017, 9, 175–181. [Google Scholar] [CrossRef] [Green Version]

- Business Dictionary Business Unit. Available online: www.businessdictionary.com/definition/business-unit.html (accessed on 15 April 2020).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Codes | Descriptions |

|---|---|

| PC | BBB Parent Company (PC); |

| SCs | Subsidiary Company (SC), s: index (s = 1,2); |

| Ff | Factory (F), f: index (f = 1,2,3,4); |

| Pp | Products (P), p index (p = 1,2,3); P1 = A or P2 = B or P3 = C; |

| Pp-BU | Product-BU (Business Unit), for example, A-BU, B-BU and C-BU; |

| Codes | Descriptions |

|---|---|

| UPp/NTD1000 | The unit selling price of product (UP) for customers; p index (p = 1,2,3); UP1 = $14, UP2 = $18, UP3 = $20.5; |

| uP1/NTD1000 | The unit selling price of P1 (A-BU) for internal in the same group (P1 for selling to B-BU or C-BU); uP1 = $13.5; |

| QPpf | The selling quantity of products (QPp) for customers and from different factories (f), for example, QP11, QP14, QP21, QP23, QP32 and QP33; QP1 = QP11 + QP14; QP2 = QP21 + QP23; QP3 = QP32 + QP33; |

| qP1 | The total quantity (qP1) of P1 (A-BU) for transfers and intersegment sales for B-BU or C-BU; for example, internal transfer (QP111 and QP112) and intersegment sales (QP113); qP1 = (QP111 + QP112 + QP113) = (QP21 + QP23) * T2 + (QP32 + QP33) * T3; |

| Mm | Purchasing material (Mm) including steel scrap, iron ore and coal; the material index (m = 1,2,3), for example, M1, M2 and M3; |

| QMm | The purchasing quantity (QMm) of material including steel scrap, iron ore and coal; the material index (m = 1,2,3), for example, QM1, QM2 and QM3; |

| rMm | Manufacturing steel billet by adapting modern EAF way or traditional BF method in the steel making process. The different Manufacturing methods also adapt different material with different requirement of the mth material for one unit of steel billet (P1); the material index (m = 1,2,3), for example, the standard requirement of steel scrap, iron ore and coal are rM1, rM2 and rM3, respectively. P1 has two different produced types that the BOM is total different, one is rM1 for EAF and another is (rM2 + rM3) for BF process. |

| UMm/NTD1000 | The unit purchasing cost (UM) of direct materials, the material index (m = 1,2,3), for example, UM1, UM2, UM3; UM1 = $9.1, UM2 = $3.2, UM3 = $2.2; |

| CMm | The total purchasing cost (CM) of each direct materials, the material index (m = 1,2,3), for example, CM1, CM2, CM3; |

| B | Inputting quantity of steel scrap each batch in the steel making process in the factory 1(F1); B = 100 tons; |

| R | the outputting quantity of P1 each batch in the steel making process in the factory 1(F1); R = 90 tons; |

| X | the number of batch for inputting batch of steel scrap in the factory 1(F1) in a period; |

| Tp | The standard requirement of output for the pth product after the semi-manufactured goods of P1; T2 = 1.02, T3 = 1.03; |

| Sb | Byproducts (S), including slag, furnace slag and steel scrap; b: index (b = 1,2,3); for example, S1, S2 and S3; |

| QSb | The quantity of byproducts (QS), including slag, furnace slag and steel scrap; b index (b = 1,2,3); for example, QS1, QS2 and QS3; QS1 = X * (B − R); QS2 = 0.5 * QP14; QS3 = (QP11 + qP1) − (QP2 + QP3); |

| USb/NTD1000: | The unit selling price of byproducts (US), b index (b = 1,2,3) US1 and US2 for selling, US3 for recycling material; US1 = $0.3, US2 = $0.03, US3 = $9.1; |

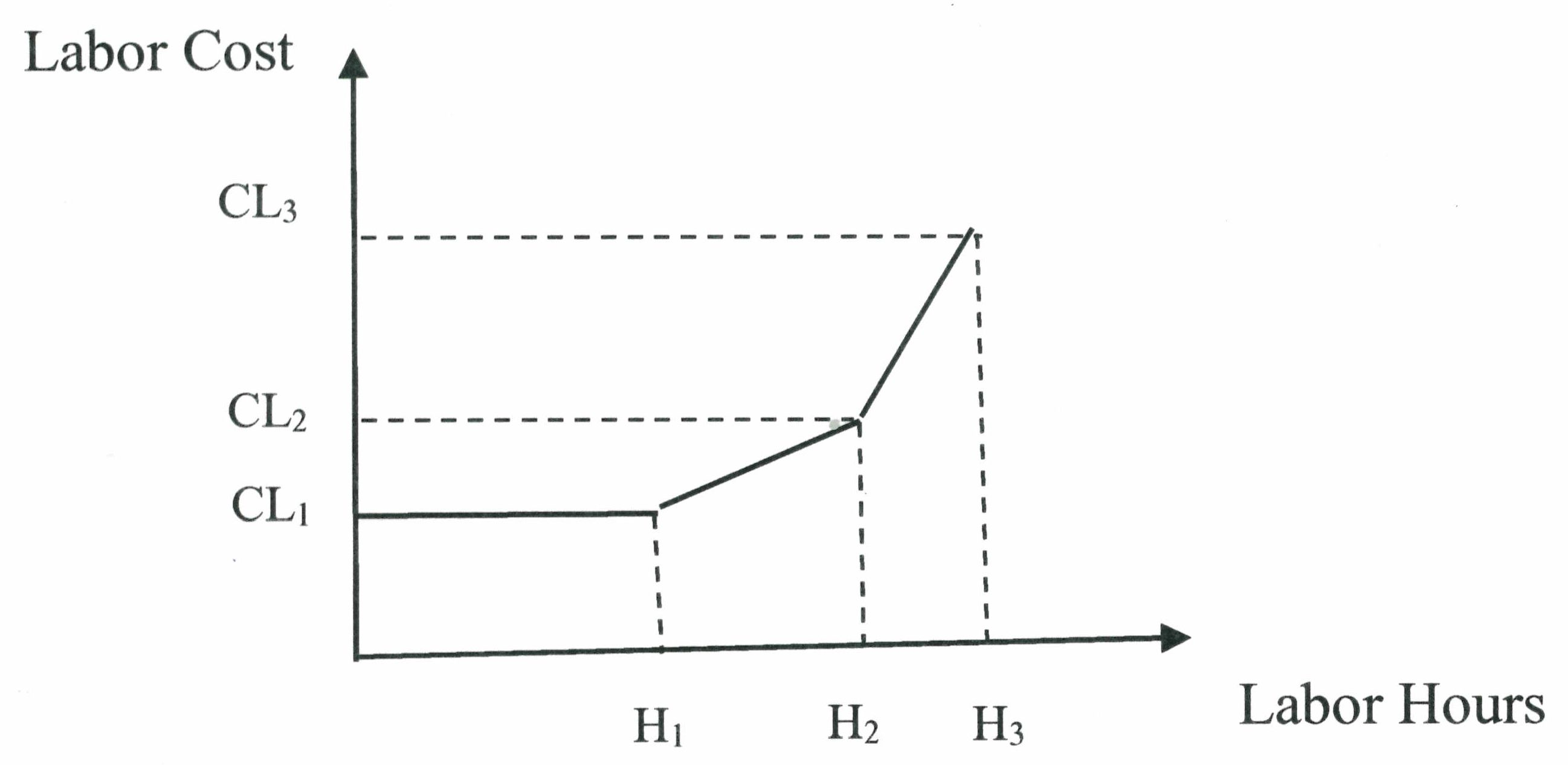

| H | Total labor direct hours (H) including the basic hours (H1), overtime hours (H2 − H1) and holiday-overtime hours (H3 − H2); |

| NL, NLf | The total direct labor number is NL for a group; NLf for each factory NL1(F1 = 150), NL2(F2 = 250), NL3(F3 = 300), NL4(F4 = 400); NL = NL1 + NL2 + NL3 + NL4; |

| α,β | The monthly minimum wage each direct labor, α for Taiwan’s each labor and β for Vietnam’s each labor; α = NTD26,400, β = NTD6000; |

| CL, CL1, CL2, CL3: | Total labor costs (CL) including the basic direct labor cost (CL1), overtime labor cost (CL2-CL1) and holiday-overtime labor cost (CL3-CL2); CL1 equals the number of direct labors (NL) * the basic wage (α) each labor. |

| Ah, Bh, Ch: | The standard running hours each ton for P1(Ah = 2), P2(Bh = 1.5) and P3(Ch = 2) for unit-level of direct labor hours. |

| Ab | The standard running hours each batch for P1(Ab) for batch-level of indirect labor hours. |

| αh1-3, βh | The monthly normal direct hours for each direct labor αh1 (176H), overtime’s hours αh2 (22H) and holiday-overtime’s hours αh3 (18H) only for Taiwan’s labor hours each month, βh (200H) for Vietnam’s each labor hours per month. |

| αd, βd | The monthly working days, αd (22 days) for Taiwan’s working days each month,βd (25 days) for Vietnam’s working days each month. |

| θ1-3 | Wage rate for Taiwan’s each direct labor; normal per hour (θ1 = NTD150), overtime’s (θ2 = NTD225), holiday-overtime’s (θ3 = NTD300); |

| λ1-3 | Wage rate for Vietnam’s each direct labor; normal per hour (λ1 = NTD30), overtime’s (λ2 = NTD45), holiday-overtime’s (λ3 = NTD60); |

| NIL | The total number of indirect labor for EAF; (NIL = 70); |

| CLs/NTD1000 | It is the total labor cost of EAF. Each indirect labor is twice times the salary of direct labor. CLs = NIL * 2; |

| CLv/NTD1000 | Total labor cost in a month in Vietnam (F4): CLv = [(NL4 * β) + (30 − βd) * 8 * NL4 * λ3] = (300 * $6000)/1000 +(30 − 25) * 8 * 300 * $60/1000 = $1800 + $720 = $2520; |

| Ed | Each batch requires the electric degree of Ed; Ed = 45; |

| UE/NTD1000 | Unit cost of electric power, UE = $2.6; |

| CE/NTD1000 | The total electric cost in a period CE = Ed * X * $UE; |

| Ihp | The machine hours including batch-level of P1, unit-level of P1, P2, and P3; Ih0 = Ab * X, Ih1 = Ah(2) * QP14, Ih2 = Bh(1.5) * QP2, Ih3 = Ch(2) * QP3; |

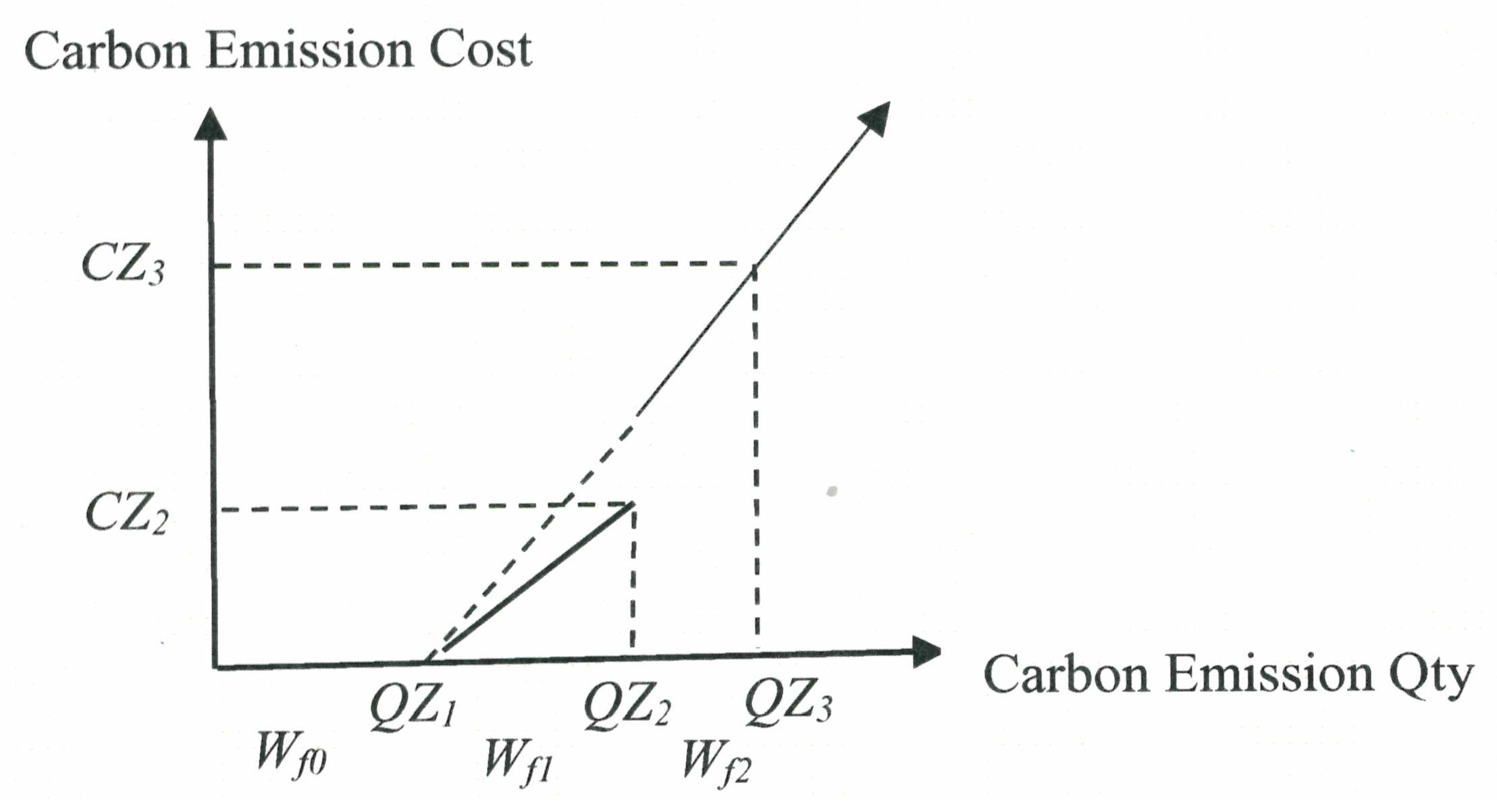

| EQf, QZ1, QZ2 | EQf is the total carbon quantity for factory f, but arrive at QZ1 and QZ2 that its cost is different. |

| Wf1,Wf2 | Both are an actual total carbon quantity, Wf1 less than QZ1, Wf2 between QZ1 and QZ2. The f (f = 1 or 4) is only for factory 1 or 4; |

| CZ2, CZ3 | That is the total carbon cost for EAF and BF depend on the carbon quantity at QZ2 or QZ3. |

| RZ, RZ1, RZ2 | The percent of carbon quantity for producing P1 by EAF or BF; RZ1 for EAF, RZ2 for BF, 4 * RZ1 = RZ2; RZ1 = 40%; |

| UZ1, UZ2 | The unit cost of carbon, when arrive at QZ1 and QZ2, respectively; |

| CIf | The machine costs are fixed for each factory, f index (f = 1,2,3,4); |

| rp | Other indirect costs use each product only as the rp percentage of customer revenue to represent the total amount of other indirect costs, p index (p = 1,2,3); |

| CGf | The other indirect costs for each factory by using each product only as the rp percentage of customer revenue, f index (f = 1,2,3,4); |

| Company-Code | Factory-Code | Sales Forecast (tons) | ||||

|---|---|---|---|---|---|---|

| A-BU/P1 | B-BU/P2 | C-BU/P3 | ||||

| QP1 = QP11 + QP14; qP1 = QP111 + QP112 + QP113 | QP2 = QP21 + QP23 | QP3 = QP32 + QP33 | ||||

| Customers | Transfers | Intersegment Sales | Sales | Sales | ||

| PC | F1 | QP11 | QP111 | QP21 | ||

| F2 | QP112 | QP32 | ||||

| SC1 | F3 | QP113 | QP23 | QP33 | ||

| SC2 | F4 | QP14 | ||||

| Descriptions | PC | SC1 | SC2 | |||

|---|---|---|---|---|---|---|

| F1 | F2 | F3 | F4 | |||

| P1 (A-BU) | P2 (B-BU) | P3 (C-BU) | P2 (B-BU) | P3 (C-BU) | P1 (A-BU) | |

| A1. external customers | QP11 * UP1 | QP21 * UP2 | QP32 * * UP3 | QP23 * UP2 | QP33 * UP3 | QP14 * UP1 |

| A2. intersegment sales | QP113 * uP1 | |||||

| A3. transfers | (QP111 + QP112) * uP1 | |||||

| A4. byproducts | QS1 * US1 | QS2 * US2 | ||||

| A.Revenue = A1 + A2 + A3 + A4 | ||||||

| B. semi-manufactured goods | QP111 * uP1 | QP112 * uP1 | QP113 * uP1 | |||

| C1. Purchasing material | QM1 * UM1 | QM2 * UM2 + QM3 * UM3 | ||||

| C2. byproduct | (QS3 * UM1) | QS3 * UM1 | ||||

| C. Material cost C = C1 − C2 or C = B − C2 | only for P1 from F1 (QP111 + QP112 + QP113) − (QS3 * UM1) only for P2 and P3 | |||||

| D. Labor cost | CLs = $ 3696 | CL1 + δ1(CL2 − CL1) + δ2(CL3 − CL1) | CL v = $ 2520 | |||

| E. Electrical cost | CE = Ed * X * UE | |||||

| F. CO2 cost | [π1 * UZ1 * (Wf1 − QZ1) + π2 * UZ2 * (Wf2 − QZ1)] only for P1 | |||||

| G. Machine costs | ||||||

| $42,000 | $3000 | $4500 | $3000 | $3500 | $8500 | |

| H. Other costs | only for external customers | |||||

| 3% * QP11 * UP1 | 5% * QP21 * UP2 | 5% * QP32 * UP3 | 5% * QP23 * UP2 | 5% * QP33 * UP3 | 3% * QP14 * UP1 | |

| I. Profit = A − C … −H | ||||||

| MAX ω = {[(QP11 + QP14) * 14] + [(QP21 + QP23) * 18] + [(QP32 + QP33) * 20.5] + [(QP111 + QP112 + QP113) * 13.5] + [(QS1 * 0.3) + (QS2 * 0.03)]} − {[(QP111 + QP112 + QP113) * 13.5 − QS3 * 9.1] − [(QM1 * 9.1) − (QS3 * 9.1)] + (QM2 * 3.2) + (QM3 * 2.2)} − {3960 + [6600 + r21 * (7837.5 − 6600) + r22 * (9187.5 − 6600)] + [7920 + r31 * (9405 − 7920) + r32 * (11,025 − 7920)] + (1800 + 720) + 3696} − (45 * 2.6 * X) − 64500 − [R11 * 60 * (W11 − 5000)/1000 + R12 * 90 * (W12 − 5000)/1000 − 2100] − [R41 * 60 * (W41 − 5000)/1000 + R42 * 90 * (W42 − 5000)/1000] − [(QP11 + QP14) * 14 * 0.03 + QP2 * 18 * 0.05 + QP3 * 20.5 * 0.05] |

| Subject to semi-manufactured goods qty: |

| QP111 = QP21 * 1.02; QP112 = QP32 * 1.03; QP113 = QP23 * 1.02 + QP33 * 1.03; qP1 = QP111 + QP112 + QP113; QM1 = 1.11 * (QP11 + qP1); QS1 = QM1 − (QP11 + qP1); QS2 = 0.5 * QP14; |

| Subject to sales qty: |

| QP2 = QP21 + QP23; QP3 = QP32 + QP33; QP11 ≤ 10,000; QP14 ≤ 36,000; QP21 ≤ 17,600; 14,000 ≤ QP23 ≤ 17,200; 22,000 ≤ QP32 ≤ 24,000; QP33 ≤ 19,300; |

| Subject to direct material: |

| QM1 = 100 * X; QM2 = 2.9 * QP14; QM3 = 0.9 * QP14; QS3 = qP1 − QP2 − QP3; X ≤ 950; QM2 ≤ 100,000; QM3 ≤ 50,000; |

| Subject to machine hour: |

| (20 + 60) * X ≤ 176 * 60 * 7; QP2 * 1.5 ≤ 52,000; QP3 * 2 ≤ 83,000; |

| Subject to direct labor for F1: |

| NL1 = 150; QP21 * 1.5 ≤ NL1 * 176; |

| Subject to direct labor for F2: |

| NL2 = 250; QP32 * 2 > NL2 * 176; QP32 * 2 ≤ NL2 * 216; QP32 * 2 = 44,000 + r21 * (49,500 − 44,000) + r22 * (54,000 − 44,000); r20 − y21 ≤ 0; r21 − y21 − y22 ≤ 0; r22 − y22 ≤ 0; r20 + r21 + r22 = 1; y21 + y22 = 1; |

| Subject to direct labor for F3: |

| NL3 = 300; (QP23 * 1.5) + (QP33 * 2) > NL3 * 176; (QP23 * 1.5) + (QP33 * 2) ≤ NL3 * 216; (QP23 * 1.5) + (QP33 * 2) = 52800 + r31 * (59400 − 52800) + r32 * (64800 − 52800); r30 − y31 ≤ 0; r31 − y31 − y32 ≤ 0; r32 − y32 ≤ 0; r30 + r31 + r32 = 1; y31 + y32 = 1; |

| Subject to direct labor for F4: |

| NL4 = 300; QP14 * 2 > NL4 * 200; QP14 * 2 ≤ NL4 * 240; |

| Subject to CO2 Emission for F1: |

| RZ1 = 0.4; (QP11 + qP1) * RZ1 = EQ1; EQ1 = R10 * W10 + R11 * W11 + R12 * W12; 0 < W10 ≤ 5000; 5000 < W11 ≤ 10,000; 10,000 < W12 ≤ 100,000; R10 + R11 + R12 = 1; |

| Subject to CO2 Emission for F4: |

| RZ4 = 1.6; QP14 * RZ4 = EQ4; EQ4 = R40 * W40 + R41 * W41 + R42 * W42; 0 < W40 ≤ 5000; 5000 < W41 ≤ 10,000; 10,000 < W42 ≤ 100,000); R40 + R41 + R42 = 1; |

| Optimal decision solution/NTD1000/ton: |

| ω = $536,370.8, QP11 = 1910, QP14 = 34,482, QP21 = 17,600, QP23 = 17,052, QP32 = 24,000, QP33 = 17,500, QP111 = 17,952, QP112 = 24,720, QP113 = 35,418, QS1 = 8800, QS2 = 17,241, QS3 = 1,938, QM1 = 88,800, QM2 = 99,997.8, QM3 = 31,033.8, R21 = 0.7272727, R31 = 0.7818519, R32 = 0.2181481, X = 888, R12 = 1, W12 = 32,000, R42 = 1, W42 = 55,171.2, Y21 = 1, Y22 = 0, Y31 = 0, Y32 = 1,EQ1 = 32,000,EQ4 = 55,171.2; |

| Descriptions | PC | SC1 | SC2 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| F1 | F2 | F3 | F4 | |||||||||

| P1 | P2 | P3 | P2 | P3 | P4 | |||||||

| (A-BU) | % | (B-BU) | % | (C-BU) | % | (B-BU) | % | (C-BU) | % | (A-BU) | % | |

| A1: External customers | 26,740 | 2.5 | 316,800 | 100 | 492,000 | 100 | 306,936 | 100 | 358,750 | 100 | 482,748 | 99.9 |

| A2: Intersegment sales | 478,143 | 44.1 | ||||||||||

| A3: Transfers | 576,072 | 53.2 | 0.0 | 0 | 0 | 0 | 0.0 | |||||

| A4: Byproducts | 2640 | 0.2 | 517 | 0.1 | ||||||||

| A. Revenues = A1 + A2 + A3 + A4 | 1,083,595 | 100 | 316,800 | 100 | 492,000 | 100 | 306,936 | 100 | 358,750 | 100 | 483,265 | 100 |

| B. Semi-manufactured goods | 242,352 | 76.5 | 333,720 | 67.8 | 234,806 | 76.5 | 243,338 | 67.8 | ||||

| C1: Purchasing material | 808,080 | 74.6 | 388,267 | 80.3 | ||||||||

| C2. Byproduct | 17,636 | −1.6 | 3203 | 1.0 | 6552 | 1.3 | 3103 | 1.0 | 4778 | 1.3 | ||

| Material cost (B − C2) | 239,149 | 75.5 | 327,168 | 66.5 | 231,702 | 75.5 | 238,560 | 66.5 | ||||

| Material cost (C = C1 − C2) | 790,444 | 72.9 | 388,267 | 80.3 | ||||||||

| D. Labor cost | 3696 | 0.3 | 3960 | 1.3 | 7500 | 1.5 | 4120 | 1.3 | 5638 | 1.6 | 2520 | 0.5 |

| E. Electrical cost | 103,896 | 9.6 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||

| F. CO2 cost | 330 | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 4515 | 0.9 | ||||

| G. Machine cost | 42,000 | 3.9 | 3000 | 0.9 | 4500 | 0.9 | 3000 | 1.0 | 3500 | 1.0 | 8500 | 1.8 |

| H. Other cost | 802 | 0.1 | 15,840 | 5.0 | 24,600 | 5.0 | 15,347 | 5.0 | 17,938 | 5.0 | 14,482 | 3.0 |

| I. Profit = A − C … −H | 142,427 | 13.1 | 54,851 | 17.3 | 128,232 | 26.1 | 52,767 | 17.2 | 93,114 | 26 | 64,980 | 13.4 |

| Descriptions | (A-BU) | % | (B-BU) | % | (C-BU) | % | Total | % |

|---|---|---|---|---|---|---|---|---|

| A1: External customers | 509,488 | 32.5 | 623,736 | 100 | 850,750 | 100 | 1,983,974 | 65.2 |

| A2: Intersegment sales | 478,143 | 30.5 | 478,143 | 15.7 | ||||

| A3: Transfers | 576,072 | 36.8 | 576,072 | 18.9 | ||||

| A4: Byproducts | 3157 | 0.2 | 3157 | 0.1 | ||||

| A. Revenues = A1 + A2 + A3 + A4 | 1,566,860 | 100 | 623,736 | 100 | 850,750 | 100 | 3,041,346 | 100 |

| For: Reportable segments | 52% | 20% | 28% | 100% | ||||

| B. Semi-manufactured goods | 477,158 | 76.5 | 577,058 | 67.8 | ||||

| C1: Purchasing material | 1,196,347 | 76.4 | ||||||

| C2. Byproduct | −17,636 | −1.1 | 6306 | 1.0 | 11,330 | 1.3 | ||

| Material cost (B − C2) | 470,851 | 75.5 | 565,728 | 66.5 | 1,036,579 | 34.1 | ||

| Material cost (C = C1 − C2) | 1,178,712 | 75.2 | 1,178,712 | 38.8 | ||||

| D. Labor cost | 6216 | 0.4 | 8080 | 1.3 | 13,138 | 1.5 | 27,434 | 0.9 |

| E. Electrical cost | 103,896 | 6.6 | 0.0 | 0.0 | 103,896 | 3.4 | ||

| F. CO2 cost | 4845 | 0.3 | 0.0 | 0.0 | 4845 | 0.2 | ||

| G. Machine cost | 50,500 | 3.2 | 6000 | 1.0 | 8000 | 0.9 | 64,500 | 2.1 |

| H. Other cost | 15,285 | 1.0 | 31,187 | 5.0 | 42,538 | 5.0 | 89,010 | 2.9 |

| I. Profit = A − C … −H | 207,407 | 13.2 | 107,618 | 17.3 | 221,346 | 26.0 | 536,370 | 17.6 |

| Descriptions | PC | SC2 | ||||||

|---|---|---|---|---|---|---|---|---|

| F1 | F4 | |||||||

| P1 | External | % | Internal | % | P1 | External | % | |

| (A-BU) | Unit | Unit | (A-BU) | Unit | ||||

| External sales Q’ty | 1910 | 34,482 | ||||||

| Internal sales Q’ty | 78,090 | |||||||

| A1: External customers | 26,740 | 14.00 | 100 | 482,748 | 14.00 | 100 | ||

| A2: Intersegment sales | 478,143 | 13.5 | 100 | |||||

| A3: Transfers | 576,072 | |||||||

| A4: Byproducts | 2640 | 517 | ||||||

| A. Revenues = A1 + A2 + A3 + A4 | 1,083,595 | 483,265 | ||||||

| B. Semi-manufactured goods | ||||||||

| C1: Purchasing material | 808,080 | 388,267 | ||||||

| C2. Byproduct | −17,636 | |||||||

| Material cost (B − C2) | ||||||||

| Material cost (C = C1 − C2) | 790,444 | 9.88 | 70.58 | 9.88 | 73.19 | 388,267 | 11.26 | 80.43 |

| D. Labor cost | 3696 | 0.05 | 0.33 | 0.05 | 0.34 | 2520 | 0.07 | 0.52 |

| E. Electrical cost | 103,896 | 1.30 | 9.28 | 1.30 | 9.62 | |||

| F. CO2 cost | 330 | 0.00 | 0.03 | 0.00 | 0.03 | 4515 | 0.13 | 0.94 |

| G. Machine cost | 42,000 | 0.53 | 3.75 | 0.53 | 3.89 | 8500 | 0.25 | 1.76 |

| H. Other cost | 802 | 0.42 | 3.0 | 0.00 | 14,482 | 0.42 | 3.00 | |

| I. Profit = A − C … −H | 142,427 | 1.83 | 13.04 | 1.75 | 12.93 | 64,980 | 1.87 | 13.35 |

| Unit: NTD 1000/ton | |||

|---|---|---|---|

| ULCEQ | Decrease ULCEQ | Profit | Decrease Profit |

| 88,000 | - | 536,370.8 | - |

| 87,500 | - | 536,370.8 | - |

| 87,171.2 | - | 536,370.8 | - |

| 87,000 | −171.2 | 536,130.2 | −240.6 |

| 86,500 | −671.2 | 535,444.4 | −926.4 |

| 86,000 | −1171.2 | 534,760.8 | −1610.0 |

| 85,500 | −1671.2 | 534,075.0 | −2295.8 |

| 85,000 | −2171.2 | 533,391.4 | −2979.4 |

| 84500 | −2671.2 | 532,705.7 | −3665.1 |

| 84,000 | −3171.2 | 532,022.1 | −4348.7 |

| 83500 | −3671.2 | 531,336.3 | −5034.5 |

| 83,000 | −4171.2 | 530,652.7 | −5718.1 |

| 82,500 | −4671.2 | 529,966.9 | −6403.9 |

| 82,000 | −5171.2 | 529,283.3 | −7087.5 |

| 81500 | −5671.2 | 528,597.5 | −7773.3 |

| 81,000 | −6171.2 | 527,913.9 | −8456.9 |

| 80500 | −6671.2 | 527,228.2 | −9142.6 |

| 80,000 | −7171.2 | 526,544.6 | −9826.2 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tsai, W.-H.; Lan, S.-H.; Lee, H.-L. Applying ERP and MES to Implement the IFRS 8 Operating Segments: A Steel Group’s Activity-Based Standard Costing Production Decision Model. Sustainability 2020, 12, 4303. https://doi.org/10.3390/su12104303

Tsai W-H, Lan S-H, Lee H-L. Applying ERP and MES to Implement the IFRS 8 Operating Segments: A Steel Group’s Activity-Based Standard Costing Production Decision Model. Sustainability. 2020; 12(10):4303. https://doi.org/10.3390/su12104303

Chicago/Turabian StyleTsai, Wen-Hsien, Shu-Hui Lan, and Hsiu-Li Lee. 2020. "Applying ERP and MES to Implement the IFRS 8 Operating Segments: A Steel Group’s Activity-Based Standard Costing Production Decision Model" Sustainability 12, no. 10: 4303. https://doi.org/10.3390/su12104303

APA StyleTsai, W. -H., Lan, S. -H., & Lee, H. -L. (2020). Applying ERP and MES to Implement the IFRS 8 Operating Segments: A Steel Group’s Activity-Based Standard Costing Production Decision Model. Sustainability, 12(10), 4303. https://doi.org/10.3390/su12104303